|

市場調査レポート

商品コード

1741049

自動駐車システムの市場機会、成長促進要因、産業動向分析、2025年~2034年予測Automated Parking System Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| 自動駐車システムの市場機会、成長促進要因、産業動向分析、2025年~2034年予測 |

|

出版日: 2025年04月28日

発行: Global Market Insights Inc.

ページ情報: 英文 190 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

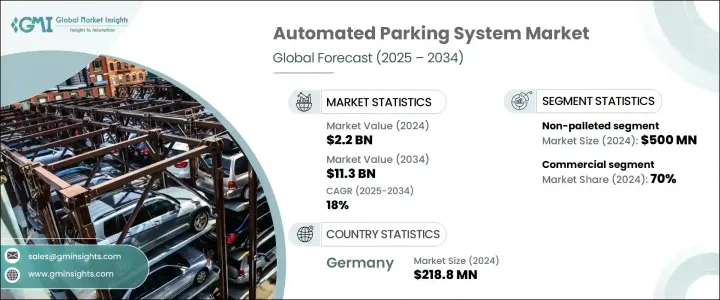

自動駐車システムの世界市場規模は、2024年に22億米ドルとなり、CAGR18%で成長し、2034年には113億米ドルに達すると予測されています。

この業界は、急速な都市化、人口密集都市における駐車場の限られた利用可能性、スマートで省スペースなインフラへのニーズの高まりなどを背景に、著しい急成長を遂げています。自動車台数の増加と不動産の縮小に伴い、都市はより効率的にスペースを管理する必要に迫られています。自動駐車システムは、土地利用を最適化し、交通の流れを合理化し、二酸化炭素排出量を削減することで、こうした課題に取り組む先進的なソリューションとして台頭してきています。これらのシステムは、人の介入を減らし、コンパクトで高効率な車両保管のアプローチを提供します。その結果、住宅や商業開発から病院や交通ハブまで、幅広い都市用途で導入が拡大しています。

自動駐車システムは、安全性を高め、スペース利用を改善し、環境への影響を最小限に抑えることができるため、人気を集めています。高度なオートメーションとロボット工学が組み込まれており、インテリジェントな車両の移動と保管が可能です。多段積み、自動車両ハンドリング、スロット管理などの機能により、これらのシステムは時間効率に優れ、環境にも優しいです。開発業者や不動産管理業者は、運営コストを削減し、限られた敷地面積で駐車容量を増やし、利用者にプレミアムな体験を提供するため、こうしたシステムを採用するケースが増えています。持続可能な都市インフラやスマートシティ構想への注目が高まる中、これらのシステムは、よりクリーンで効率的な都市モビリティに向けた世界の取り組みに合致しているため、需要はさらに高まっています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 22億米ドル |

| 予測金額 | 113億米ドル |

| CAGR | 18% |

プラットフォーム別に見ると、市場はパレット式と非パレット式に区分されます。ノンパレットのカテゴリーは、2024年の売上高が約5億米ドルで市場をリードしています。このセグメントの優位性は、省スペース設計と迅速な車両回収能力に起因しており、これらは交通量の多い大都市圏で特に重要です。パレット式とは異なり、非パレット式は支持台を必要とせず、ロボット工学とコンベア・システムを使用して車両を直接移動させるため、機械的なセットアップが簡素化され、狭い都市部のレイアウトにも柔軟に設置できます。高スループット・ソリューションが不可欠な商業ビル、空港、高層住宅開発で需要が伸びています。

エンドユーザーの観点から見ると、市場は住宅用と商業用に分かれています。2024年には、オフィスビル、小売センター、病院、ホスピタリティ施設での採用が牽引し、商業セグメントが70%の市場シェアを占める。これらの環境では、自動パーキングが収容力を強化し、混雑を緩和し、混雑した環境で車両への迅速なアクセスを提供する能力から多大な恩恵を受けています。都市の混雑と土地代の高騰により、企業は限られたスペースを最大限に活用する垂直または地下の駐車場構造に投資するようになっています。さらに、自動駐車場とスマートビル技術や強化されたセキュリティーシステムとの統合は、商業開発者にとって魅力的な選択肢となっています。

市場はタイプ別にも分類されており、2024年には半自動システムが大半のシェアを占める。半自動化システムの魅力は、コスト効率、迅速なセットアップ、使いやすさにあり、住宅と商業の両セグメントにおける多様な用途に適しています。これらのシステムは、完全自動化と手動制御のバランスを提供し、完全自動化のような高額な先行投資をすることなく、ユーザーエクスペリエンスの向上を実現します。メンテナンスの必要性が低く、ユーザーフレンドリーな特徴が、広く受け入れられる要因となっています。

システム構造の中では、無人搬送車(AGV)セグメントが2024年の世界市場をリードし、最大の収益シェアを生み出しました。AGVシステムは適応性が高く、複雑なレイアウトを正確に移動できるため、混雑した都市環境や大規模な商業プロジェクトに最適です。既存のインフラにシームレスに統合しながら、高度な自動化と柔軟性を実現するAGVの能力により、AGVは現代の駐車場課題に対する好ましいソリューションとなっています。AGVは、スループットとスペース利用を最大化することが重要な環境に特に適しています。

2024年の自動駐車システム市場では、ハードウェアが世界収益の最大シェアを占めました。これは、センサー、リフト、AGV、コンベアシステムなどの物理的なコンポーネントが不可欠なためであり、自動駐車の中核をなすものです。システムが高度化するにつれて、耐久性があり高性能なハードウェアに対する需要は、特に長期的な信頼性と大量の取り扱いを必要とするプロジェクトにおいて伸び続けています。

地域別では、ドイツが2024年の収益2億1,880万米ドルで欧州市場をリードし、2034年までのCAGRは16.9%と予測されています。同国の強力な自動車産業、スマートシティプロジェクトへの投資、先進的な都市インフラが、この分野でのリーダーシップに大きく貢献しています。さらに、世界中の企業が研究開発、戦略的パートナーシップ、最先端の製造技術に投資することで存在感を高めています。市場をリードする企業は、モジュール式のシステム設計、エネルギー効率、AIとIoT技術の統合に注力し、ユーザーエクスペリエンスと環境性能の両方を高めています。こうしたイノベーションが、次世代のスマートで持続可能な駐車場ソリューションの舞台を整えつつあります。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- サプライヤーの情勢

- ハードウェアプロバイダー

- ソフトウェアプロバイダー

- サービスプロバイダー

- テクノロジープロバイダー

- 最終用途

- 利益率分析

- サプライヤーの情勢

- トランプ政権による関税への影響

- 貿易への影響

- 貿易量の混乱

- 報復措置

- 業界への影響

- 供給側の影響(原材料)

- 主要原材料の価格変動

- サプライチェーンの再構築

- 生産コストへの影響

- 需要側の影響(販売価格)

- 最終市場への価格伝達

- 市場シェアの動向

- 消費者の反応パターン

- 供給側の影響(原材料)

- 戦略的な業界対応

- サプライチェーンの再構成

- 価格設定と製品戦略

- 貿易への影響

- テクノロジーとイノベーションの情勢

- 特許分析

- 規制情勢

- コスト内訳分析

- 主なニュースと取り組み

- 影響要因

- 促進要因

- 北米と欧州で自動運転車が増加

- 都市化の急速な進展

- アジア太平洋地域と中東におけるスマートシティプロジェクトの台頭

- 駐車システムにおける技術の進歩

- 業界の潜在的リスク&課題

- 高い開発コスト

- 複雑なメンテナンスとダウンタイムのリスク

- 促進要因

- 成長可能性分析

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 競合ポジショニングマトリックス

- 戦略的展望マトリックス

第5章 市場推計・予測:タイプ別、2021-2034

- 主要動向

- 完全自動化

- 半自動

第6章 市場推計・予測:構造別、2021-2034

- 主要動向

- AGVシステム

- サイロシステム

- タワーシステム

- レールガイドカート(RGC)システム

- パズルシステム

- シャトルシステム

第7章 市場推計・予測:提供別、2021-2034

- 主要動向

- ハードウェア

- ソフトウェア

- サービス

第8章 市場推計・予測:プラットフォーム別、2021-2034

- 主要動向

- パレット

- 非パレット

第9章 市場推計・予測:最終用途別、2021-2034

- 主要動向

- 住宅用

- 商業用

第10章 市場推計・予測:地域別、2021-2034

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- フランス

- 英国

- スペイン

- イタリア

- ロシア

- 北欧諸国

- アジア太平洋地域

- 中国

- インド

- 日本

- 韓国

- オーストラリア・ニュージーランド

- 東南アジア

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- アラブ首長国連邦

- 南アフリカ

- サウジアラビア

第11章 企業プロファイル

- AutoMotion Parking

- City Lift Parking

- Dayang Parking

- EITO&GLOBAL

- Fata Automation

- IHI

- Klaus Multiparking

- Lodgie

- MHE Demag

- Park Assist

- Parkmatic

- ParkPlus

- Robotic Parking

- Serva Transport

- Skyline Parking

- Stolzer Parking

- TAPS

- Unitronics

- Westfalia Parking

- Wohr Parking

The Global Automated Parking System Market was valued at USD 2.2 billion in 2024 and is estimated to grow at a CAGR of 18% to reach USD 11.3 billion by 2034. The industry is experiencing a significant surge, driven by rapid urbanization, limited availability of parking in densely populated cities, and a growing need for smart, space-saving infrastructure. With rising vehicle numbers and shrinking real estate, cities are facing mounting pressure to manage space more efficiently. Automated parking systems are emerging as a forward-thinking solution that tackles these challenges by optimizing land usage, streamlining traffic flow, and reducing carbon emissions. These systems provide a compact, highly efficient approach to vehicle storage with reduced reliance on human intervention. As a result, their deployment is expanding across a wide range of urban applications-from residential and commercial developments to hospitals and transport hubs.

Automated parking systems are gaining popularity due to their ability to enhance safety, improve space utilization, and minimize environmental impact. They incorporate advanced automation and robotics, allowing for intelligent vehicle movement and storage. Features such as multi-level stacking, automated vehicle handling, and slot management make these systems both time-efficient and environmentally friendly. Developers and property managers are increasingly turning to these systems to reduce operational costs, increase parking capacity in a confined footprint, and offer a premium experience to users. The rising focus on sustainable urban infrastructure and smart city initiatives is further fueling demand, as these systems align with global efforts toward cleaner, more efficient urban mobility.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $2.2 Billion |

| Forecast Value | $11.3 Billion |

| CAGR | 18% |

In terms of platform, the market is segmented into palleted and non-palleted systems. The non-palleted category led the market with approximately USD 500 million in revenue in 2024. This segment's dominance is attributed to its space-saving design and quicker vehicle retrieval capabilities, which are especially important in high-traffic metropolitan areas. Unlike palleted systems, non-palleted ones eliminate the need for a supporting platform and use robotics and conveyor systems to move vehicles directly, simplifying the mechanical setup and allowing for flexible installation in tight urban layouts. Demand is growing in commercial buildings, airports, and high-rise residential developments where high-throughput solutions are essential.

From an end-user perspective, the market is split between residential and commercial applications. In 2024, the commercial segment held a substantial 70% market share, driven by adoption in office buildings, retail centers, hospitals, and hospitality venues. These settings benefit immensely from automated parking's ability to enhance capacity, reduce congestion, and provide quicker access to vehicles in busy environments. Urban congestion and the high cost of land are pushing businesses to invest in vertical or underground parking structures that make the most of limited space. Furthermore, the integration of automated parking with smart building technologies and enhanced security systems makes it an attractive option for commercial developers.

The market is also categorized by type, with semi-automated systems accounting for the majority share in 2024. Their appeal lies in cost efficiency, quick setup, and ease of use, making them suitable for diverse applications across both residential and commercial segments. These systems offer a balance between full automation and manual control, providing enhanced user experience without the high upfront investment of fully automated alternatives. Their low maintenance requirements and user-friendly features contribute to their widespread acceptance.

Among system structures, the Automated Guided Vehicle (AGV) segment led the global market in 2024, generating the largest revenue share. AGV systems are highly adaptable and can navigate complex layouts with precision, making them ideal for crowded urban settings and large commercial projects. Their ability to integrate seamlessly into existing infrastructure while delivering high levels of automation and flexibility has made them a preferred solution for modern parking challenges. AGVs are particularly well-suited for environments where maximizing throughput and space utilization is critical.

In terms of offerings, hardware dominated the automated parking system market in 2024, accounting for the largest share of global revenue. This is due to the essential nature of physical components such as sensors, lifts, AGVs, and conveyor systems, which form the core of any automated parking operation. As systems become more sophisticated, demand for durable, high-performance hardware continues to grow, especially in projects that require long-term reliability and high-volume handling.

Regionally, Germany led the European market with USD 218.8 million in revenue in 2024 and is forecasted to grow at a CAGR of 16.9% through 2034. The country's strong automotive industry, investment in smart city projects, and advanced urban infrastructure contribute significantly to its leadership in this sector. Additionally, companies across the globe are scaling their presence by investing in research and development, strategic partnerships, and cutting-edge manufacturing techniques. Market leaders are focusing on modular system designs, energy efficiency, and integration of AI and IoT technologies to enhance both user experience and environmental performance. These innovations are setting the stage for the next generation of smart, sustainable parking solutions.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.1.1 Research approach

- 1.1.2 Data collection methods

- 1.2 Base estimates & calculations

- 1.2.1 Base year calculation

- 1.2.2 Key trends for market estimation

- 1.3 Forecast model

- 1.4 Primary research and validation

- 1.4.1 Primary sources

- 1.4.2 Data mining sources

- 1.5 Market scope & definition

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.1.1 Hardware providers

- 3.1.1.2 Software providers

- 3.1.1.3 Service providers

- 3.1.1.4 Technology providers

- 3.1.1.5 End Use

- 3.1.2 Profit margin analysis

- 3.1.1 Supplier landscape

- 3.2 Impact of Trump administration tariffs

- 3.2.1 Impact on trade

- 3.2.1.1 Trade volume disruptions

- 3.2.1.2 Retaliatory measures

- 3.2.2 Impact on industry

- 3.2.2.1 Supply-side impact (raw materials)

- 3.2.2.1.1 Price volatility in key materials

- 3.2.2.1.2 Supply chain restructuring

- 3.2.2.1.3 Production cost implications

- 3.2.2.2 Demand-side impact (selling price)

- 3.2.2.2.1 Price transmission to end markets

- 3.2.2.2.2 Market share dynamics

- 3.2.2.2.3 Consumer response patterns

- 3.2.2.1 Supply-side impact (raw materials)

- 3.2.3 Strategic industry responses

- 3.2.3.1 Supply chain reconfiguration

- 3.2.3.2 Pricing and product strategies

- 3.2.1 Impact on trade

- 3.3 Technology & innovation landscape

- 3.4 Patent analysis

- 3.5 Regulatory landscape

- 3.6 Cost breakdown analysis

- 3.7 Key news & initiatives

- 3.8 Impact forces

- 3.8.1 Growth drivers

- 3.8.1.1 Increasing autonomous vehicles in north america and europe

- 3.8.1.2 The rapid increase in urbanization

- 3.8.1.3 Rising smart city projects in asia pacific and middle east

- 3.8.1.4 Increasing technological advancements in parking systems

- 3.8.2 Industry pitfalls & challenges

- 3.8.2.1 High development cost

- 3.8.2.2 Complex maintenance and downtime risk

- 3.8.1 Growth drivers

- 3.9 Growth potential analysis

- 3.10 Porter's analysis

- 3.11 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Type, 2021 - 2034 ($Mn)

- 5.1 Key trends

- 5.2 Fully automated

- 5.3 Semi-automated

Chapter 6 Market Estimates & Forecast, By Structure, 2021 - 2034 ($Mn)

- 6.1 Key trends

- 6.2 AGV system

- 6.3 Silo system

- 6.4 Tower system

- 6.5 Rail Guided Cart (RGC) system

- 6.6 Puzzle system

- 6.7 Shuttle system

Chapter 7 Market Estimates & Forecast, By Offering, 2021 - 2034 ($Mn)

- 7.1 Key trends

- 7.2 Hardware

- 7.3 Software

- 7.4 Services

Chapter 8 Market Estimates & Forecast, By Platform, 2021 - 2034 ($Mn)

- 8.1 Key trends

- 8.2 Palleted

- 8.3 Non-palleted

Chapter 9 Market Estimates & Forecast, By End Use, 2021 - 2034 ($Mn)

- 9.1 Key trends

- 9.2 Residential

- 9.3 Commercial

Chapter 10 Market Estimates & Forecast, By Region, 2021 - 2034 ($Mn)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 France

- 10.3.3 UK

- 10.3.4 Spain

- 10.3.5 Italy

- 10.3.6 Russia

- 10.3.7 Nordics

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 South Korea

- 10.4.5 ANZ

- 10.4.6 Southeast Asia

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 MEA

- 10.6.1 UAE

- 10.6.2 South Africa

- 10.6.3 Saudi Arabia

Chapter 11 Company Profiles

- 11.1 AutoMotion Parking

- 11.2 City Lift Parking

- 11.3 Dayang Parking

- 11.4 EITO&GLOBAL

- 11.5 Fata Automation

- 11.6 IHI

- 11.7 Klaus Multiparking

- 11.8 Lodgie

- 11.9 MHE Demag

- 11.10 Park Assist

- 11.11 Parkmatic

- 11.12 ParkPlus

- 11.13 Robotic Parking

- 11.14 Serva Transport

- 11.15 Skyline Parking

- 11.16 Stolzer Parking

- 11.17 TAPS

- 11.18 Unitronics

- 11.19 Westfalia Parking

- 11.20 Wohr Parking