自動車用データロガーの市場機会、成長促進要因、産業動向分析、2025年~2034年予測

Automotive Data Logger Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034- 発行日

- ページ情報

- 英文 180 Pages

- 納期

- 2~3営業日

- 商品コード

- 1741047

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

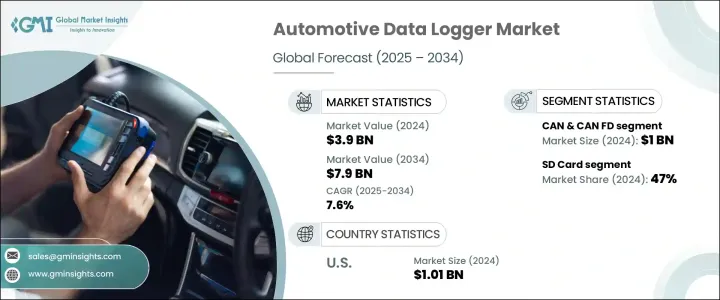

自動車用データロガーの世界市場規模は2024年に39億米ドルとなり、CAGR 7.6%で成長し、2034年には79億米ドルに達すると推定されます。

この成長は、コネクテッドカー技術の急速な開発、安全性と排ガス規制の強化、高度な車両診断とテレマティクスの需要の高まりによって形成されています。世界中の自動車メーカーが電気自動車や無人店舗に移行する中、データロガーは乗用車と商用車の両方のカテゴリーで性能データの収集、保存、分析において中心的な役割を果たしています。これらのデバイスは、バッテリー管理システム、インフォテインメント・ユニット、ADAS、ECUなどのさまざまなコンポーネントからデータを取得し、リアルタイムの追跡とシステム評価に不可欠なツールです。これらのデバイスを使用することで、車両の効率性と安全性を確保するために不可欠な予知保全、ソフトウェア・デバッグ、規制遵守、ドライバー行動の洞察が強化されます。自動車業界におけるIoTとクラウドベースのエコシステムの影響力が高まるにつれ、最新のデータロガーは遠隔操作と無線アップデートをサポートする能力が高まっており、コネクテッドモビリティと車両管理システムへのシームレスな統合を提供しています。

通信プロトコルの観点から、市場はCAN &CAN FD、LIN、FlexRay、イーサネットに区分されます。このうち、CAN &CAN FDカテゴリーは2024年に市場をリードし、約10億米ドルの収益を生み出しました。これらのプロトコルの優位性は、自動車業界全体で長年にわたって採用されてきたことに起因しています。CANは、数十年にわたり信頼性の高い車載通信規格として、エンジン制御や車両安全性などの分野で重要なシステム間のやり取りを促進してきました。アップグレードされたCAN FDバージョンは、より高いデータスループットを可能にし、特に最新の運転支援システムに関わる、よりデータ集約的な機能をサポートしています。CAN &CAN FDは、その広範な有用性、コスト効率、低レイテンシー機能により、車載診断およびテストアプリケーションに不可欠な存在であり続けています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 39億米ドル |

| 予測金額 | 79億米ドル |

| CAGR | 7.6% |

接続タイプ別に市場を見ると、USB、Bluetooth/Wi-Fi、SDカードなどがあります。2024年の市場シェアは47%で、SDカード・セグメントがリードしています。この傾向は、SDカードの信頼性、使いやすさ、手頃な価格によるものです。コンパクトなフォーマットで大容量のストレージを提供するSDカードは、テストや試験中に膨大な量の車両データを記録するのに適しています。そのプラグアンドプレイ設計は、セットアップを簡素化し、オフライン環境でのデータ抽出を可能にするため、無線インフラが制限されていたり、干渉の影響を受けやすかったりするプリプロダクション段階での貴重なツールとなります。

コンポーネント別に分類すると、市場はハードウェアとソフトウェアに分けられ、2024年にはハードウェアが圧倒的なシェアを占める。このセグメントは自動車用データロギングシステムの中核をなすもので、データ収集用のマイクロプロセッサー、データ保存用の大容量メモリー、データの完全性を維持するためのシグナルコンディショナー、リアルタイムモニタリング用のセンサーインターフェースで構成されます。これらのコンポーネントは、CAN、FlexRay、イーサネットなどのプロトコルを使用して、データロガーと車両システム間の通信を可能にします。メーカーは、電気自動車や自律走行車システムの複雑化に対応するため、これらのハードウェアプラットフォームを強化し続けており、実環境におけるマルチチャネル、高速、マルチプロトコル機能に対する需要が高まっています。

用途に基づき、市場は販売前と販売後の用途に分けられます。2024年には、販売前セグメントが支配的な分野として浮上しました。データロガーは、車両が市場に出る前に、性能、安全性、環境基準への適合を検証するために広く使用されています。エンジニアは、パワートレインを最適化し、ADAS機能を較正し、電気モデルのバッテリー効率を検証するために、設計とテストの段階で正確なデータ取得に依存しています。ポストセールスセグメントは、診断と予知保全における役割により成長しているもの、現在のところ市場全体のシェアに占める割合は小さいです。

エンドユーザーの観点からは、市場にはOEM、サービスステーション、規制当局、その他が含まれます。OEMセグメントが2024年に最大のシェアを占めたのは、メーカーが車両開発のライフサイクルを通じてデータロガーに大きく依存し続けているからです。プロトタイプから最終的な検証まで、データロガーは品質基準が一貫して満たされていることを確認するために使用されます。自動車がますます複雑な技術を取り入れるにつれて、OEMは、ECUの検証から次世代システムの統合まですべてを管理するために、洗練されたデータロギング・ソリューションに投資しています。

地域別では、米国が北米市場をリードし、2024年には10億1,000万米ドルの収益を記録し、予測期間中のCAGRは6.4%と予測されました。同国の強い地位は、急速な技術導入、強固な研究インフラ、電動モビリティやコネクテッドモビリティへの推進の高まりに起因します。米国全土の研究所、試験施設、メーカーは、技術革新、コンプライアンス、システム検証をサポートするために、最先端のデータロギング機器を導入し続けています。

業界全体では、合併、戦略的提携、センサー技術やリアルタイム分析への投資を通じて企業が前進しています。診断と性能追跡を合理化するスマートなIoT対応、ワイヤレス接続のデータロガーへのシフトが進んでいます。こうした技術革新は、自動車のバリューチェーン全体にわたって、信頼性を向上させ、より厳しい規制要求に対応し、より持続可能でインテリジェントな車両設計をサポートするのに役立っています。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- サプライヤーの情勢

- ハードウェアプロバイダー

- ソフトウェアプロバイダー

- テクノロジープロバイダー

- 最終用途

- 利益率分析

- サプライヤーの情勢

- トランプ政権による関税への影響

- 貿易への影響

- 貿易量の混乱

- 報復措置

- 業界への影響

- 供給側の影響(原材料)

- 主要原材料の価格変動

- サプライチェーンの再構築

- 生産コストへの影響

- 需要側の影響(販売価格)

- 最終市場への価格伝達

- 市場シェアの動向

- 消費者の反応パターン

- 供給側の影響(原材料)

- 戦略的な業界対応

- サプライチェーンの再構成

- 価格設定と製品戦略

- 貿易への影響

- テクノロジーとイノベーションの情勢

- 特許分析

- 規制情勢

- ユースケース

- 主なニュースと取り組み

- 影響要因

- 促進要因

- 電気自動車の生産と自動運転車のテストの増加

- 現代の自動車におけるADAS機能の需要の高まり

- リアルタイム車両データに対する需要の増加

- 環境への影響を軽減するための排出基準の急増

- 車両管理ソリューションの需要の高まり

- 業界の潜在的リスク&課題

- 高度なデータロガーの開発に必要な訓練を受けた人材の不足

- 促進要因

- 成長可能性分析

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 競合ポジショニングマトリックス

- 戦略的展望マトリックス

第5章 市場推計・予測:コンポーネント別、2021-2034

- 主要動向

- ハードウェア

- ソフトウェア

第6章 市場推計・予測:チャンネル別、2021-2034

- 主要動向

- CANおよびCAN FD

- リン

- フレックスレイ

- イーサネット

第7章 市場推計・予測:接続別、2021-2034

- 主要動向

- SDカード

- Bluetooth/Wi-Fi

- USB

第8章 市場推計・予測:用途別、2021-2034

- 主要動向

- 先行販売

- 販売後

- ADASと安全性

- 自動車保険

- 車両管理

- OBD

第9章 市場推計・予測:最終用途別、2021-2034

- 主要動向

- OEM

- サービスステーション

- 規制機関

- その他

第10章 市場推計・予測:地域別、2021-2034

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- 英国

- ドイツ

- フランス

- イタリア

- スペイン

- ベネルクス

- ロシア

- アジア太平洋地域

- 中国

- インド

- 日本

- 韓国

- 東南アジア

- オーストラリア・ニュージーランド

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- アラブ首長国連邦

- サウジアラビア

- 南アフリカ

第11章 企業プロファイル

- Aptiv

- Continental

- Danlaw

- Delphi

- Dewesoft

- dSPACE

- Elektrobit

- HEM Data

- Influx Technology

- Intrepid

- IPETRONIK

- Kistler

- MathWorks

- National Instruments

- NSM Solutions

- Racelogic

- Robert Bosch

- TT Tech

- Vector Informatik

- Xilinx

目次

The Global Automotive Data Logger Market was valued at USD 3.9 billion in 2024 and is estimated to grow at a CAGR of 7.6% to reach USD 7.9 billion by 2034. This growth is being shaped by the fast-paced development of connected car technologies, heightened safety and emissions regulations, and the rising demand for advanced vehicle diagnostics and telematics. As automakers worldwide transition toward electric and autonomous platforms, data loggers are playing a central role in gathering, storing, and analyzing performance data across both passenger and commercial vehicle categories. These devices are essential tools for real-time tracking and system evaluations, capturing data from various components like battery management systems, infotainment units, ADAS, and ECUs. Their use enhances predictive maintenance, software debugging, regulatory compliance, and driver behavior insights, which are all crucial for ensuring vehicle efficiency and safety. With the rising influence of IoT and cloud-based ecosystems in the automotive landscape, modern data loggers are increasingly capable of supporting remote operations and over-the-air updates, offering seamless integration into connected mobility and fleet management systems.

In terms of communication protocols, the market is segmented into CAN & CAN FD, LIN, FlexRay, and Ethernet. Among these, the CAN & CAN FD category led the market in 2024, generating approximately USD 1 billion in revenue. The dominance of these protocols stems from their longstanding adoption across the automotive industry. CAN has been a reliable in-vehicle communication standard for decades, facilitating critical system interactions in areas like engine control and vehicle safety. The upgraded CAN FD version allows higher data throughput and supports more data-intensive functions, especially those involving modern driving assistance systems. Their widespread utility, cost-efficiency, and low-latency capabilities continue to make CAN & CAN FD indispensable for in-vehicle diagnostics and testing applications.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $3.9 Billion |

| Forecast Value | $7.9 Billion |

| CAGR | 7.6% |

Looking at the market by connection type, options include USB, Bluetooth/Wi-Fi, and SD card. The SD card segment took the lead with a 47% market share in 2024. This preference is due to the SD card's reliability, ease of use, and affordability. Offering high-capacity storage in a compact format, SD cards are well-suited for logging vast volumes of vehicle data during tests and trials. Their plug-and-play design simplifies setup and allows data extraction in offline environments, making them valuable tools in pre-production phases where wireless infrastructure might be limited or vulnerable to interference.

When categorized by component, the market is divided into hardware and software, with hardware taking the dominant share in 2024. This segment represents the core of automotive data logging systems, consisting of microprocessors for data acquisition, high-capacity memory for data storage, signal conditioners to maintain data integrity, and sensor interfaces for real-time monitoring. These components enable communication between data loggers and vehicle systems using protocols like CAN, FlexRay, and Ethernet. Manufacturers continue to enhance these hardware platforms to meet the rising complexity of electric and autonomous vehicle systems, increasing demand for multi-channel, high-speed, and multi-protocol capabilities in real-world conditions.

Based on application, the market is split into pre-sale and post-sale uses. The pre-sale segment emerged as the dominant area in 2024. Data loggers are widely used before a vehicle reaches the market to validate performance, safety, and compliance with environmental standards. Engineers depend on accurate data capture during the design and testing stages to optimize powertrains, calibrate ADAS features, and verify battery efficiency in electric models. Though the post-sale segment is growing due to its role in diagnostics and predictive maintenance, it currently accounts for a smaller portion of the overall market share.

In terms of end users, the market includes OEMs, service stations, regulatory authorities, and others. The OEM segment held the largest share in 2024, as manufacturers continue to rely heavily on data loggers throughout the vehicle development lifecycle. From prototyping to final validation, data loggers are used to ensure quality standards are consistently met. As vehicles incorporate increasingly complex technologies, OEMs are investing in sophisticated data logging solutions to manage everything from ECU validation to next-gen system integration.

Regionally, the United States led the North American market, recording USD 1.01 billion in revenue in 2024, with a projected CAGR of 6.4% during the forecast period. The country's strong position stems from rapid technological adoption, robust research infrastructure, and an increasing push toward electric and connected mobility. Research labs, test facilities, and manufacturers across the U.S. continue to deploy cutting-edge data logging equipment to support innovation, compliance, and system validation.

Across the industry, companies are advancing through mergers, strategic collaborations, and investments in sensor technologies and real-time analytics. There's a growing shift toward smart, IoT-enabled, and wirelessly connected data loggers that streamline diagnostics and performance tracking. These innovations are helping organizations across the automotive value chain improve reliability, meet stricter regulatory demands, and support more sustainable and intelligent vehicle designs.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.1.1 Research approach

- 1.1.2 Data collection methods

- 1.2 Base estimates & calculations

- 1.2.1 Base year calculation

- 1.2.2 Key trends for market estimation

- 1.3 Forecast model

- 1.4 Primary research and validation

- 1.4.1 Primary sources

- 1.4.2 Data mining sources

- 1.5 Market scope & definition

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.1.1 Hardware providers

- 3.1.1.2 Software providers

- 3.1.1.3 Technology providers

- 3.1.1.4 End use

- 3.1.2 Profit margin analysis

- 3.1.1 Supplier landscape

- 3.2 Impact of Trump administration tariffs

- 3.2.1 Impact on trade

- 3.2.1.1 Trade volume disruptions

- 3.2.1.2 Retaliatory measures

- 3.2.2 Impact on industry

- 3.2.2.1 Supply-side impact (raw materials)

- 3.2.2.1.1 Price volatility in key materials

- 3.2.2.1.2 Supply chain restructuring

- 3.2.2.1.3 Production cost implications

- 3.2.2.2 Demand-side impact (selling price)

- 3.2.2.2.1 Price transmission to end markets

- 3.2.2.2.2 Market share dynamics

- 3.2.2.2.3 Consumer response patterns

- 3.2.2.1 Supply-side impact (raw materials)

- 3.2.3 Strategic industry responses

- 3.2.3.1 Supply chain reconfiguration

- 3.2.3.2 Pricing and product strategies

- 3.2.1 Impact on trade

- 3.3 Technology & innovation landscape

- 3.4 Patent analysis

- 3.5 Regulatory landscape

- 3.6 Use cases

- 3.7 Key news & initiatives

- 3.8 Impact forces

- 3.8.1 Growth drivers

- 3.8.1.1 Increasing electric vehicle production and autonomous vehicle testing

- 3.8.1.2 Rising demand for ADAS features in modern vehicles

- 3.8.1.3 Increasing demand for real-time vehicle data

- 3.8.1.4 Surge in emission norms to reduce environmental impact

- 3.8.1.5 Rising demand for fleet management solutions

- 3.8.2 Industry pitfalls & challenges

- 3.8.2.1 Lack of a trained workforce for the development of advanced data loggers

- 3.8.1 Growth drivers

- 3.9 Growth potential analysis

- 3.10 Porter's analysis

- 3.11 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Component, 2021 - 2034 (USD Million)

- 5.1 Key trends

- 5.2 Hardware

- 5.3 Software

Chapter 6 Market Estimates & Forecast, By Channel, 2021 - 2034 (USD Million)

- 6.1 Key trends

- 6.2 CAN & CAN FD

- 6.3 LIN

- 6.4 FlexRay

- 6.5 Ethernet

Chapter 7 Market Estimates & Forecast, By Connection, 2021 - 2034 (USD Million)

- 7.1 Key trends

- 7.2 SD Card

- 7.3 Bluetooth/Wi-Fi

- 7.4 USB

Chapter 8 Market Estimates & Forecast, By Application, 2021 - 2034 (USD Million)

- 8.1 Key trends

- 8.2 Pre-sale

- 8.3 Post-sale

- 8.3.1 ADAS and safety

- 8.3.2 Automotive insurance

- 8.3.3 Fleet management

- 8.3.4 OBD

Chapter 9 Market Estimates & Forecast, By End Use, 2021 - 2034 (USD Million)

- 9.1 Key trends

- 9.2 OEM

- 9.3 Service station

- 9.4 Regulatory bodies

- 9.5 others

Chapter 10 Market Estimates & Forecast, By Region, 2021 - 2034 (USD Million)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 UK

- 10.3.2 Germany

- 10.3.3 France

- 10.3.4 Italy

- 10.3.5 Spain

- 10.3.6 Benelux

- 10.3.7 Russia

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 South Korea

- 10.4.5 Southeast Asia

- 10.4.6 ANZ

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 MEA

- 10.6.1 UAE

- 10.6.2 Saudi Arabia

- 10.6.3 South Africa

Chapter 11 Company Profiles

- 11.1 Aptiv

- 11.2 Continental

- 11.3 Danlaw

- 11.4 Delphi

- 11.5 Dewesoft

- 11.6 dSPACE

- 11.7 Elektrobit

- 11.8 HEM Data

- 11.9 Influx Technology

- 11.10 Intrepid

- 11.11 IPETRONIK

- 11.12 Kistler

- 11.13 MathWorks

- 11.14 National Instruments

- 11.15 NSM Solutions

- 11.16 Racelogic

- 11.17 Robert Bosch

- 11.18 TT Tech

- 11.19 Vector Informatik

- 11.20 Xilinx

- 発行日

- 発行

- Global Market Insights Inc.

- ページ情報

- 英文 180 Pages

- 納期

- 2~3営業日