|

市場調査レポート

商品コード

1741028

油浸固定シャントリアクターの市場機会と促進要因、産業動向分析、2025年~2034年予測Oil Immersed Fixed Shunt Reactor Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| 油浸固定シャントリアクターの市場機会と促進要因、産業動向分析、2025年~2034年予測 |

|

出版日: 2025年04月21日

発行: Global Market Insights Inc.

ページ情報: 英文 125 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

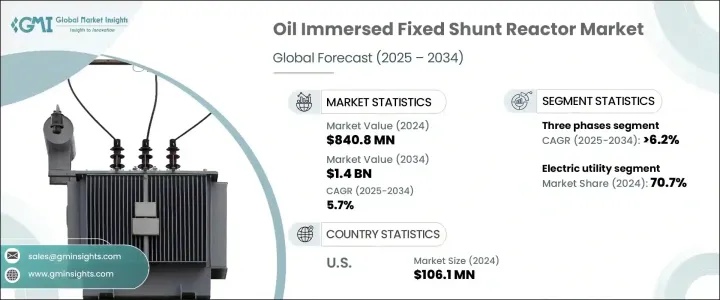

世界の油浸固定シャントリアクター市場は、2024年には8億4,080万米ドルとなり、CAGR 5.7%で成長し、2034年には14億米ドルに達すると予測されています。

これは、急速に進む新興国の工業化と都市開拓のペースが、電力消費の急増に拍車をかけているためです。世界の送電網は大きな変革期を迎えており、都市人口の増加、インフラの拡大、経済活動の加速化によって、エネルギー・システムに莫大な圧力がかかっています。政府や民間の利害関係者は、安定性や効率を損なうことなく増大する電力需要に対応するため、送配電網の近代化と拡大に注力しています。油入固定分路リアクトルは、電圧レベルを維持し、過電圧を制限し、送電網全体の無効電力を管理する費用効果の高いソリューションを提供するため、この進化の基本的な部分になりつつあります。産業界が高圧送電や再生可能エネルギー源の相互接続にシフトするにつれて、分路リアクトルの需要が顕著に増加しています。これらのデバイスは、損失を最小限に抑え、グリッドの信頼性を高める上で重要な役割を果たしています。

この市場は、エネルギー消費の増加によって成長しているだけでなく、発電と配電の方法に応じて進化しています。各国が経済や都市インフラの規模を拡大するにつれ、堅牢で効率的な送電システムが必要とされています。特に製造拠点や新しい都市居住地でのエネルギー需要の高まりは、無効電力補償装置への本格的な投資を促し、公益事業規模のプロジェクトにおける油入固定分路リアクトルの採用を後押ししています。電力網が太陽光や風力のような可変エネルギー源をますます統合するようになり、電圧や無効電力がしばしば変動するため、業界各社は強い追い風を目の当たりにしています。このため、固定分路リアクトルは電圧制御に不可欠であり、将来対応可能な送電網システムの中核部品となっています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 8億4,080万米ドル |

| 予測金額 | 14億米ドル |

| CAGR | 5.7% |

ここでの主要な成長要因のひとつは、世界の自然エネルギーへのシフトです。風力や太陽光のようなクリーンなエネルギー源が国家送電網に追加される中、その断続的な性質が不安定さをもたらすことが多いです。そこで油入固定分路リアクトルの出番となります。電圧変動と無効電力変動を補正することで、必要とされるバランシング・メカニズムを提供します。カーボンニュートラルの目標を目指す国が増えるにつれ、これらのリアクターは送電網近代化戦略における基幹資産としての地位を確保しつつあります。先進国も発展途上国も同様に、老朽化した電力インフラの交換やアップグレードの必要性を認識しており、固定分路リアクトルは、こうした資本集約的なアップグレード計画の最前線で中心的な役割を担っています。電力会社は、ダイナミックに進化するグリッド環境において、中断のないエネルギー伝送と運用の安定性向上を確保するために、これを導入しています。

三相リアクトルは、長距離の高圧送電線の電圧を安定させるという比類なき実用性により、2034年までのCAGRは6.2%となる見込みです。送電網の相互接続が進み、変動する再生可能電源からの高負荷を管理する必要があるため、三相油入分路リアクトルは、電力フローの最適化とエネルギー損失の防止に不可欠なものとなっています。これらのリアクトルは、複雑な負荷パターンに対応できるよう特別に設計されており、高需要シナリオにおいて送電システムの連続運転を維持するのに役立ちます。電力会社は、スマートグリッド構想やインフラ拡張プロジェクトの一環としてリアクターを統合しており、ネットワークを将来にわたって維持するために不可欠なツールとみなしています。

アプリケーションを見ると、2024年には電気事業セグメントが70.7%という圧倒的なシェアで世界市場をリードしており、その優位性はすぐには失われないと思われます。この勢いは、産業の成長、都市のスプロール化、電力システムのデジタル化の進行によるエネルギー需要の増加が後押ししています。電力会社は、送電損失を減らし、電圧レベルを安定させ、グリッドの効率を維持するソリューションに投資しています。これらのコンポーネントは、エネルギー配給の安全、安定、中断のない運用をサポートするものであり、これがグリッド運用者にとって最優先事項となっている理由です。

米国の油浸固定シャントリアクター市場の評価額は2024年に1億610万米ドルに達し、製品設計と技術の革新がペースを上げ続けているため、成長軌道は安定しています。主要メーカーは、熱効率の向上、運転騒音の低減、耐用年数の延長を実現した次世代リアクター・モデルを展開しています。このような製品の進歩は、国内の老朽化した送電インフラのアップグレードを目的とした連邦政府および州レベルのプログラムからも後押しされています。スマートグリッドプロジェクトや持続可能性を重視したエネルギー改革への投資が拡大する中、米国は世界市場成長の主要貢献国としての役割を固めつつあります。

世界の油入固定分路リアクトル市場の主要企業には、日立エネルギー、GE、シーメンス・エナジー、日新電機、GBE S.p.A.、東芝エネルギーシステム&ソリューション、CG Power &Industrial Solutions Ltd.、HYOSUNG HEAVY、Siemens Energy Co、HYOSUNG HEAVY INDUSTRIES、富士電機株式会社、SGB SMIT、GETRA S.p.A.、Shrihans Electricals Pvt.Ltd.、TMC TRANSFORMERS MANUFACTURING COMPANY、WEG。これらの企業は、世界な製造拠点を拡大し、先進的でグリッドに特化したリアクター設計を提供するために研究開発を加速させ、地域市場において電力会社やEPC企業と提携し、オーダーメードのソリューションを推進しています。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- トランプ政権の関税分析

- 貿易への影響

- 貿易量の混乱

- 報復措置

- 業界への影響

- 供給側の影響(原材料)

- 主要原材料の価格変動

- サプライチェーンの再構築

- 生産コストへの影響

- 需要側の影響(販売価格)

- 最終市場への価格伝達

- 市場シェアの動向

- 消費者の反応パターン

- 供給側の影響(原材料)

- 影響を受ける主要企業

- 戦略的な業界対応

- サプライチェーンの再構成

- 価格設定と製品戦略

- 政策関与

- 展望と今後の検討事項

- 貿易への影響

- 規制情勢

- 業界への影響要因

- 促進要因

- 業界の潜在的リスク&課題

- 成長可能性分析

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 戦略的展望

- イノベーションと持続可能性の情勢

第5章 市場規模・予測:フェーズ別、2021-2034

- 主要動向

- 単相

- 三相

第6章 市場規模・予測:最終用途別、2021-2034

- 主要動向

- 電力会社

- 再生可能エネルギー

第7章 市場規模・予測:地域別、2021-2034

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- 英国

- ドイツ

- フランス

- イタリア

- ロシア

- アジア太平洋地域

- 中国

- インド

- 日本

- オーストラリア

- 中東・アフリカ

- サウジアラビア

- アラブ首長国連邦

- カタール

- 南アフリカ

- ラテンアメリカ

- ブラジル

- アルゼンチン

第8章 企業プロファイル

- CG Power &Industrial Solutions Ltd.

- Fuji Electric Co.、Ltd.

- GBE S.p.A

- GE

- GETRA S.p.A.

- Hitachi Energy Ltd.

- HYOSUNG HEAVY INDUSTRIES

- NISSIN ELECTRIC Co.、Ltd.

- Shrihans Electricals Pvt. Ltd.

- Siemens Energy

- SGB SMIT

- TMC TRANSFORMERS MANUFACTURING COMPANY

- Toshiba Energy Systems &Solutions Corporation

- WEG

The Global Oil Immersed Fixed Shunt Reactor Market was valued at USD 840.8 million in 2024 and is estimated to grow at a CAGR of 5.7% to reach USD 1.4 billion by 2034, driven by the ongoing pace of industrialization and urban development in rapidly emerging nations fueling a surge in electricity consumption. The global power grid is undergoing a major transformation, where rising urban populations, expanding infrastructure, and accelerated economic activities are putting immense pressure on energy systems. Governments and private stakeholders are focusing on modernizing and expanding transmission and distribution networks to meet growing power demands without compromising stability or efficiency. Oil-immersed fixed shunt reactors are becoming a fundamental part of this evolution, as they offer a cost-effective solution to maintain voltage levels, limit over-voltages, and manage reactive power across the grid. As industries shift toward high-voltage transmission and interconnection of renewable energy sources, the demand for shunt reactors is witnessing a noticeable upswing. These devices play a vital role in minimizing losses and enhancing grid reliability, which is crucial for meeting the power quality expectations of modern economies.

You're looking at a market that's not only growing due to increased energy consumption but also evolving in response to how power is being generated and distributed. As countries scale up their economic and urban infrastructure, they require robust and efficient power transmission systems. That rising energy demand, especially across manufacturing hubs and new urban settlements, is pushing serious investment toward reactive power compensation equipment-driving the adoption of oil-immersed fixed shunt reactors across utility-scale projects. Industry players are witnessing strong tailwinds as power grids increasingly integrate variable energy sources like solar and wind, which often cause voltage and reactive power fluctuations. This makes fixed shunt reactors essential for voltage control, making them a core part of future-ready grid systems.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $840.8 Million |

| Forecast Value | $1.4 Billion |

| CAGR | 5.7% |

One of the major growth drivers here is the global shift to renewables. With clean energy sources like wind and solar being added to national grids, their intermittent nature often results in instability. That's where oil-immersed fixed shunt reactors come in-they provide a much-needed balancing mechanism by correcting voltage swings and reactive power variations. As more countries aim for carbon-neutral targets, these reactors are securing their position as mission-critical assets in grid modernization strategies. Developed and developing nations alike are recognizing the need to replace or upgrade aging power infrastructure, and fixed shunt reactors are front and center in these capital-intensive upgrade plans. Utilities are deploying them to ensure uninterrupted energy transmission and enhanced operational stability in a dynamically evolving grid environment.

The three-phase segment is expected to post a strong CAGR of 6.2% through 2034, thanks to its unmatched utility in stabilizing voltage across long-distance, high-voltage transmission lines. As power grids grow more interconnected and are required to manage higher loads from variable renewable sources, three-phase oil-immersed shunt reactors are becoming indispensable for optimizing power flow and preventing energy losses. These reactors are specifically engineered to handle complex load patterns and help maintain continuous operation of transmission systems in high-demand scenarios. Utilities are integrating them as part of smart grid initiatives and infrastructure expansion projects, viewing them as essential tools to future-proof their networks.

Looking at applications, the electric utility segment led the global market with a commanding 70.7% share in 2024, and that dominance isn't going away anytime soon. This momentum is being fueled by increasing energy requirements driven by industrial growth, urban sprawl, and the ongoing digitization of power systems. Electric utilities are investing in solutions that reduce transmission losses, stabilize voltage levels, and maintain grid efficiency-and fixed shunt reactors check all those boxes. These components support the safe, stable, and uninterrupted operation of energy distribution, which is why they've become a top priority for grid operators.

The United States Oil Immersed Fixed Shunt Reactor Market reached a valuation of USD 106.1 million in 2024, and the growth trajectory remains steady as innovation in product design and technology continues to pick up pace. Key manufacturers are rolling out next-gen reactor models with enhanced thermal efficiency, reduced operational noise, and extended service life. This product advancement is also getting a boost from both federal and state-level programs aimed at upgrading the country's aging transmission infrastructure. With growing investments in smart grid projects and sustainability-focused energy reforms, the US is solidifying its role as a major contributor to global market growth.

Leading players in the global oil-immersed fixed shunt reactor market include Hitachi Energy Ltd., GE, Siemens Energy, NISSIN ELECTRIC Co., Ltd., GBE S.p.A, Toshiba Energy Systems & Solutions Corporation, CG Power & Industrial Solutions Ltd., HYOSUNG HEAVY INDUSTRIES, Fuji Electric Co., Ltd., SGB SMIT, GETRA S.p.A., Shrihans Electricals Pvt. Ltd., TMC TRANSFORMERS MANUFACTURING COMPANY, and WEG. These companies are expanding their global manufacturing footprints, accelerating R&D to deliver advanced and grid-specific reactor designs, and partnering with utilities and EPC firms to drive tailored solutions in regional markets.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope & definitions

- 1.2 Market estimates & forecast parameters

- 1.3 Forecast calculation

- 1.4 Data sources

- 1.4.1 Primary

- 1.4.2 Secondary

- 1.4.2.1 Paid

- 1.4.2.2 Public

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Trump administration tariffs analysis

- 3.2.1 Impact on trade

- 3.2.1.1 Trade volume disruptions

- 3.2.1.2 Retaliatory measures

- 3.2.2 Impact on the industry

- 3.2.2.1 Supply-side impact (raw materials)

- 3.2.2.1.1 Price volatility in key materials

- 3.2.2.1.2 Supply chain restructuring

- 3.2.2.1.3 Production cost implications

- 3.2.2.2 Demand-side impact (selling price)

- 3.2.2.2.1 Price transmission to end markets

- 3.2.2.2.2 Market share dynamics

- 3.2.2.2.3 Consumer response patterns

- 3.2.2.1 Supply-side impact (raw materials)

- 3.2.3 Key companies impacted

- 3.2.4 Strategic industry responses

- 3.2.4.1.1 Supply chain reconfiguration

- 3.2.4.1.2 Pricing and product strategies

- 3.2.4.1.3 Policy engagement

- 3.2.5 Outlook and future considerations

- 3.2.1 Impact on trade

- 3.3 Regulatory landscape

- 3.4 Industry impact forces

- 3.4.1 Growth drivers

- 3.4.2 Industry pitfalls & challenges

- 3.5 Growth potential analysis

- 3.6 Porter's analysis

- 3.6.1 Bargaining power of suppliers

- 3.6.2 Bargaining power of buyers

- 3.6.3 Threat of new entrants

- 3.6.4 Threat of substitutes

- 3.7 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Strategic outlook

- 4.3 Innovation & sustainability landscape

Chapter 5 Market Size and Forecast, By Phase, 2021 - 2034 (USD Million)

- 5.1 Key trends

- 5.2 Single phase

- 5.3 Three phase

Chapter 6 Market Size and Forecast, By End Use, 2021 - 2034 (USD Million)

- 6.1 Key trends

- 6.2 Electric utility

- 6.3 Renewable energy

Chapter 7 Market Size and Forecast, By Region, 2021 - 2034 (USD Million)

- 7.1 Key trends

- 7.2 North America

- 7.2.1 U.S.

- 7.2.2 Canada

- 7.3 Europe

- 7.3.1 UK

- 7.3.2 Germany

- 7.3.3 France

- 7.3.4 Italy

- 7.3.5 Russia

- 7.4 Asia Pacific

- 7.4.1 China

- 7.4.2 India

- 7.4.3 Japan

- 7.4.4 Australia

- 7.5 Middle East & Africa

- 7.5.1 Saudi Arabia

- 7.5.2 UAE

- 7.5.3 Qatar

- 7.5.4 South Africa

- 7.6 Latin America

- 7.6.1 Brazil

- 7.6.2 Argentina

Chapter 8 Company Profiles

- 8.1 CG Power & Industrial Solutions Ltd.

- 8.2 Fuji Electric Co., Ltd.

- 8.3 GBE S.p.A

- 8.4 GE

- 8.5 GETRA S.p.A.

- 8.6 Hitachi Energy Ltd.

- 8.7 HYOSUNG HEAVY INDUSTRIES

- 8.8 NISSIN ELECTRIC Co., Ltd.

- 8.9 Shrihans Electricals Pvt. Ltd.

- 8.10 Siemens Energy

- 8.11 SGB SMIT

- 8.12 TMC TRANSFORMERS MANUFACTURING COMPANY

- 8.13 Toshiba Energy Systems & Solutions Corporation

- 8.14 WEG