|

市場調査レポート

商品コード

1699346

空芯分路リアクトル市場の機会、成長促進要因、産業動向分析、2025年~2034年の予測Air Core Shunt Reactor Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025-2034 |

||||||

カスタマイズ可能

|

|||||||

| 空芯分路リアクトル市場の機会、成長促進要因、産業動向分析、2025年~2034年の予測 |

|

出版日: 2025年02月24日

発行: Global Market Insights Inc.

ページ情報: 英文 128 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

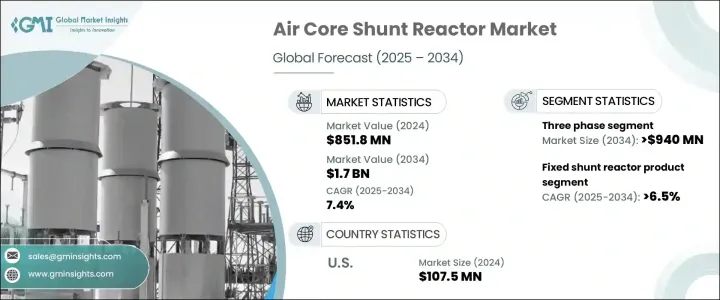

空芯分路リアクトルの世界市場は、2024年に8億5,180万米ドルに達し、2025年から2034年にかけてCAGR 7.4%で成長すると予測されています。

これらのリアクトルに対する需要の高まりは、送電インフラへの大規模な投資と、現在進行中の送電網近代化の取り組みによって後押しされています。送電網が複雑化し、風力や太陽光のような再生可能エネルギー源が勢いを増すにつれ、無効電力補償の必要性は高まり続けています。空芯分路リアクトルは、電圧レベルの安定化、電力損失の最小化、効率的なエネルギー伝送の確保において重要な役割を果たし、現代の電力ネットワークに不可欠なものとなっています。

世界の急速な都市化、工業化、電化の進展は、電力インフラの大幅な開発を促進しています。政府と民間企業は、送電網の信頼性を高め、急増する電力需要に対応するため、投資を強化しています。再生可能エネルギーの導入が加速する中、大規模な太陽光発電や風力発電の設置には堅牢なトランスミッションが必要となり、空芯分路リアクトルの市場見通しはさらに強まっています。長距離送電に広く使用されている高電圧直流(HVDC)システムも、このリアクトルの導入拡大に寄与しています。システムの安定性を向上させ、損失を削減する空芯分路リアクトルの能力により、世界中の公益事業者に好まれる選択肢となっています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 8億5,180万米ドル |

| 予測金額 | 17億米ドル |

| CAGR | 7.4% |

市場は、主に三相と単相の空芯分路リアクトルの2種類に区分されます。このうち、三相セグメントが業界を支配しており、最大の市場シェアを占め、強い成長の可能性を示しています。2034年までに、このセグメントは高電圧トランスミッション・ネットワークへの広範な応用により、9億4,000万米ドルに達すると予想されます。三相空芯シャントリアクトルは、電圧変動の安定化と送電損失の低減に重要な役割を果たし、再生可能エネルギーの統合やHVDC送電システムに不可欠です。エネルギー転換への取り組みが世界中で強化されるにつれて、三相リアクトルの需要は、特に大規模な公益事業プロジェクトで急増すると予想されます。

空芯分流リアクトルはさらに固定型と可変型に分類され、固定型は堅調な成長が見込まれます。トランスミッションによると、このセグメントの2034年までのCAGRは6.5%であり、これは高圧送電用途における固定分路リアクトルの費用対効果と信頼性が原動力となっています。これらのリアクトルは無効電力に安定した補償を提供し、送電網の効率と信頼性を確保します。エネルギー・グリッドが拡大・進化するにつれて、系統の安定性を維持し、電圧の不安定を防止する固定分路リアクトルの役割はますます重要になっています。

米国の空芯シャントリアクトル市場の2024年の市場規模は1億750万米ドルで、今後数年間は着実な成長が見込まれます。市場拡大の主な要因は、エネルギー統合の進展と国家送電網内の近代化努力です。風力発電所や太陽光発電所などの再生可能エネルギープロジェクトをサポートするための大容量トランスミッションの建設が、固定および可変分路リアクトルの需要を促進しています。送電網の回復力を強化し、送電損失を最小限に抑えることにますます焦点が当てられるようになり、空芯分流リアクトルへの投資は増加の一途をたどっています。これらのリアクトルは、需要ピーク時の配電管理において重要な役割を果たし、進化する米国の電力インフラにおいて不可欠なコンポーネントとして位置づけられています。

目次

第1章 調査手法と調査範囲

- 市場の定義

- 基本推定と計算

- 予測計算

- データソース

第2章 エグゼクティブサマリー

第3章 業界洞察

- エコシステム分析

- 規制状況

- 業界への影響要因

- 促進要因

- 業界の潜在的リスク&課題

- 成長ポテンシャル分析

- ポーター分析

- PESTEL分析

第4章 競合情勢

- 戦略ダッシュボード

- イノベーションと持続可能性の展望

第5章 市場規模・予測:フェーズ別、2021年~2034年

- 主要動向

- 単相

- 三相

第6章 市場規模・予測:製品別、2021年~2034年

- 主要動向

- 固定シャントリアクトル

- 可変シャントリアクトル

第7章 市場規模・予測:最終用途別、2021年~2034年

- 主要動向

- 電気事業

- 再生可能エネルギー

第8章 市場規模・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- 英国

- ドイツ

- フランス

- イタリア

- ロシア

- アジア太平洋

- 中国

- インド

- 日本

- オーストラリア

- 中東・アフリカ

- サウジアラビア

- アラブ首長国連邦

- カタール

- 南アフリカ

- ラテンアメリカ

- ブラジル

- アルゼンチン

第9章 企業プロファイル

- Coil Innovation

- GE

- GETRA

- Hilkar

- Hitachi Energy

- Hyosung Heavy Industries

- MindCore Technologies

- Nissin Electric

- Phoenix Electric

- SGB SMIT

- Siemens Energy

- Shrihans Electricals

- TMC Transformers Manufacturing Company

- Toshiba Energy Systems &Solutions

The Global Air Core Shunt Reactor Market reached USD 851.8 million in 2024 and is projected to grow at a CAGR of 7.4% from 2025 to 2034. The rising demand for these reactors is fueled by significant investments in power transmission infrastructure and ongoing grid modernization efforts. As power grids become more complex and renewable energy sources like wind and solar gain momentum, the need for reactive power compensation continues to grow. Air core shunt reactors play a crucial role in stabilizing voltage levels, minimizing power losses, and ensuring efficient energy transmission, making them indispensable in modern electricity networks.

Rapid urbanization, industrialization, and increased electrification worldwide are driving substantial developments in power infrastructure. Governments and private sector players are ramping up investments to enhance grid reliability and accommodate the surging demand for electricity. With renewable energy adoption accelerating, large-scale solar and wind power installations require robust transmission networks, further strengthening the market outlook for air core shunt reactors. High-voltage direct current (HVDC) systems, widely used for long-distance electricity transmission, are also contributing to the growing deployment of these reactors. The ability of air core shunt reactors to improve system stability and reduce losses makes them a preferred choice for utility providers globally.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $851.8 Million |

| Forecast Value | $1.7 Billion |

| CAGR | 7.4% |

The market is segmented into two primary types: three-phase and single-phase air core shunt reactors. Among these, the three-phase segment dominates the industry, holding the largest market share and showing strong growth potential. By 2034, this segment is expected to reach USD 940 million, driven by its widespread application in high-voltage transmission networks. Three-phase air core shunt reactors play a vital role in stabilizing voltage fluctuations and reducing transmission losses, making them essential for renewable energy integration and HVDC transmission systems. As energy transition efforts intensify worldwide, demand for three-phase reactors is expected to surge, especially in large-scale utility projects.

Air core shunt reactors are further classified into fixed and variable types, with the fixed segment expected to experience robust growth. Forecasts indicate a CAGR of 6.5% through 2034 for this segment, driven by the cost-effectiveness and reliability of fixed shunt reactors in high-voltage transmission applications. These reactors provide stable compensation for reactive power, ensuring grid efficiency and reliability. As energy grids expand and evolve, the role of fixed shunt reactors in maintaining system stability and preventing voltage instability becomes increasingly crucial.

The US air core shunt reactor market was valued at USD 107.5 million in 2024, with steady growth anticipated in the coming years. Market expansion is largely attributed to advancements in energy integration and modernization efforts within the national grid. The construction of high-capacity transmission lines to support renewable energy projects, including wind and solar farms, is driving demand for fixed and variable shunt reactors. With an increasing focus on enhancing grid resilience and minimizing transmission losses, investments in air core shunt reactors continue to rise. These reactors play a crucial role in managing electricity distribution during peak demand periods, positioning them as essential components in the evolving US power infrastructure landscape.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market definitions

- 1.2 Base estimates & calculations

- 1.3 Forecast calculation

- 1.4 Data sources

- 1.4.1 Primary

- 1.4.2 Secondary

- 1.4.2.1 Paid

- 1.4.2.2 Public

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Regulatory landscape

- 3.3 Industry impact forces

- 3.3.1 Growth drivers

- 3.3.2 Industry pitfalls & challenges

- 3.4 Growth potential analysis

- 3.5 Porter's analysis

- 3.5.1 Bargaining power of suppliers

- 3.5.2 Bargaining power of buyers

- 3.5.3 Threat of new entrants

- 3.5.4 Threat of substitutes

- 3.6 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Strategic dashboard

- 4.2 Innovation & sustainability landscape

Chapter 5 Market Size and Forecast, By Phase, 2021 – 2034 (USD Million)

- 5.1 Key trends

- 5.2 Single phase

- 5.3 Three phase

Chapter 6 Market Size and Forecast, By Product, 2021 – 2034 (USD Million)

- 6.1 Key trends

- 6.2 Fixed shunt reactors

- 6.3 Variable shunt reactors

Chapter 7 Market Size and Forecast, By End Use, 2021 – 2034 (USD Million)

- 7.1 Key trends

- 7.2 Electric utility

- 7.3 Renewable energy

Chapter 8 Market Size and Forecast, By Region, 2021 – 2034 (USD Million)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 UK

- 8.3.2 Germany

- 8.3.3 France

- 8.3.4 Italy

- 8.3.5 Russia

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 Australia

- 8.5 Middle East & Africa

- 8.5.1 Saudi Arabia

- 8.5.2 UAE

- 8.5.3 Qatar

- 8.5.4 South Africa

- 8.6 Latin America

- 8.6.1 Brazil

- 8.6.2 Argentina

Chapter 9 Company Profiles

- 9.1 Coil Innovation

- 9.2 GE

- 9.3 GETRA

- 9.4 Hilkar

- 9.5 Hitachi Energy

- 9.6 Hyosung Heavy Industries

- 9.7 MindCore Technologies

- 9.8 Nissin Electric

- 9.9 Phoenix Electric

- 9.10 SGB SMIT

- 9.11 Siemens Energy

- 9.12 Shrihans Electricals

- 9.13 TMC Transformers Manufacturing Company

- 9.14 Toshiba Energy Systems & Solutions