自動車用E/Eアーキテクチャの市場機会、成長促進要因、産業動向分析、2025年~2034年予測

Automotive E-E (Electronic/Electrical) Architecture Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034- 発行日

- ページ情報

- 英文 170 Pages

- 納期

- 2~3営業日

- 商品コード

- 1741005

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

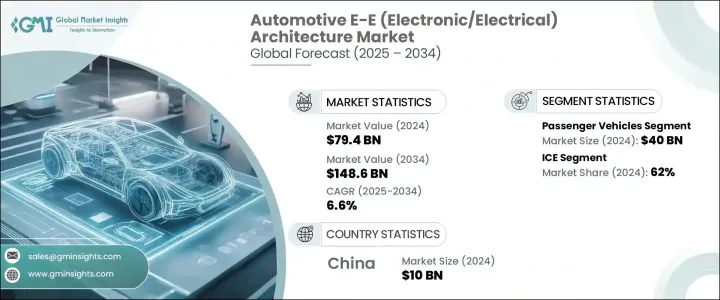

世界の自動車用E/Eアーキテクチャ市場は、2024年には794億米ドルとなり、電気自動車(EV)の普及拡大、車両接続性の向上、自律走行技術に対する需要の高まりなどを背景に、CAGR6.6%で成長し、2034年までには1,486億米ドルに達すると予測されています。

自動車用E/E(電気・電子)アーキテクチャは、パワートレインやインフォテインメントからADAS(先進運転支援システム)やコネクティビティソリューションに至るまで、あらゆるものを管理し、現代の自動車の重要な機能を支えています。ゾーン型および集中型アーキテクチャへの移行は、配線の複雑さを軽減し、データ処理速度を向上させ、AI、機械学習、V2X通信などの高度な技術のシームレスな統合を可能にすることで、車両性能を向上させます。

集中型コンピューティングプラットフォームは、コネクテッドカーや自律走行車のセンサー、カメラ、通信ネットワークから生成される膨大なデータをサポートするために不可欠になっています。さらに、持続可能なモビリティの推進と、ユーロ7や中国VIなどの規制基準の厳格化により、自動車メーカーはエネルギー効率、サイバーセキュリティ、コンプライアンスを高めるためにE/Eシステムの再設計を促しています。さらに、持続可能なモビリティの推進と、欧州のEuro 7やアジアのChina VIなどの規制基準の厳格化により、自動車メーカーは、より高いエネルギー効率、サイバーセキュリティ、規制遵守のためにE/Eシステムの再設計を促しています。このような規制の進化は、車両の排出ガス低減だけでなく、車両の安全性、コネクティビティ、データセキュリティに対するより高い基準も要求しています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024年 |

| 予測年 | 2025年~2034年 |

| 開始金額 | 794億米ドル |

| 予測金額 | 1,486億米ドル |

| CAGR | 6.6% |

自動車用E/Eアーキテクチャ市場は主にタイプ別に区分され、2024年には分散型E/Eアーキテクチャが367億米ドルを稼ぎ出しリードします。分散型アーキテクチャは、さまざまな車両機能を制御する複数の独立した電子制御ユニット(ECU)を特徴とし、その柔軟性、統合の容易さ、拡張性により広く採用されています。この設計により、自動車メーカーはネットワーク全体をオーバーホールすることなく、特定の車両システムを個別にアップグレードできます。しかし、車両のソフトウエア化とデータ集約化が進むにつれて、業界は、集中制御、データ管理の改善、システムの複雑性の低減、配線コストの削減を実現するドメインアーキテクチャやゾーンアーキテクチャへと徐々に移行しつつあります。

車両タイプ別では、乗用車が2024年に436億米ドルを占め、最大の市場シェアを獲得しました。ADAS(先進運転支援システム)、次世代インフォテインメントシステム、コネクティビティサービス、電動パワートレインなどのプレミアム機能を搭載したパーソナルカーに対する需要の高まりが、このセグメントにおける高度なE/Eアーキテクチャの採用に拍車をかけています。先進的なアーキテクチャは、さまざまな車両システム間のシームレスな通信を可能にし、運転支援機能を強化し、車両診断を改善し、自律走行機能を可能にし、全体的な運転体験を向上させます。

アジア太平洋の自動車用E/Eアーキテクチャ市場は、急速な電気自動車(EV)の普及、スマートシティ構想、中国、日本、韓国の強力な自動車製造拠点に牽引され、2024年には279億5,000万米ドルに達しました。中国は、積極的なEV政策、広範なスマートインフラ開拓、新興国市場のEVブランドの成長により、引き続きこの地域市場をリードしています。日本と韓国は、自律走行車技術や5G対応V2X通信システムに多額の投資を行っており、先進的なE/Eアーキテクチャの必要性をさらに高めています。政府のインセンティブ、EV導入のための補助金、次世代モビリティソリューションへのRandDの多額の投資は、この地域全体で最新の拡張可能なE/Eシステムの統合を加速させています。

Robert Bosch GmbH、Continental AG、Aptiv PLC、ZF Friedrichshafen AG、Denso Corporationなどの大手企業は、競争力を維持するために、RandDに積極的に投資し、戦略的パートナーシップを結び、モジュール式のソフトウェア定義E/Eプラットフォームを開発しています。サイバーセキュリティ、スケーラビリティ、エネルギー管理の強化に重点を置くことで、次世代の自動車用電気・電子アーキテクチャが世界的に定義されようとしています。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- 業界エコシステム分析

- サプライヤーの情勢

- E/Eアーキテクチャプロバイダー

- 部品供給業者

- 販売代理店

- 最終用途

- トランプ政権による関税への影響

- 貿易への影響

- 貿易量の混乱

- 報復措置

- 業界への影響

- 供給側の影響(原材料)

- 主要原材料の価格変動

- サプライチェーンの再構築

- 生産コストへの影響

- 需要側の影響(販売価格)

- 最終市場への価格伝達

- 市場シェアの動向

- 消費者の反応パターン

- 供給側の影響(原材料)

- 影響を受ける主要企業

- 戦略的な業界対応

- サプライチェーンの再構成

- 価格設定と製品戦略

- 政策関与

- 展望と今後の検討事項

- 貿易への影響

- 利益率分析

- テクノロジーとイノベーションの情勢

- 特許分析

- 価格分析

- 主なニュースと取り組み

- 規制情勢

- 影響要因

- 成長促進要因

- 電気自動車(EV)の需要増加

- 車両の安全性と規制基準への注目が高まる

- ADAS(先進運転支援システム)(ADAS)の導入増加

- コネクテッドカーとV2X(車車間通信)通信の需要

- 業界の潜在的リスク&課題

- 高度なE/Eアーキテクチャの開発は複雑でコストがかかる

- 車両の接続性向上に伴うサイバーセキュリティリスク

- 成長促進要因

- 成長可能性分析

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 競合ポジショニングマトリックス

- 戦略的展望マトリックス

第5章 市場推計・予測:タイプ別、2021年~2034年

- 主要動向

- 分散型E/Eアーキテクチャ

- ドメインE/Eアーキテクチャ

- ゾーンアーキテクチャ

第6章 市場推計・予測:車両別、2021年~2034年

- 主要動向

- 乗用車

- ハッチバック

- セダン

- SUV

- 商用車

- 小型商用車(LCV)

- 中型商用車(MCV)

- 大型商用車(HCV)

第7章 市場推計・予測:推進力別、2021年~2034年

- 主要動向

- ICE

- 電気自動車

- バッテリー電気自動車(BEV)

- プラグインハイブリッド電気自動車(PHEV)

- ハイブリッド電気自動車(HEV)

第8章 市場推計・予測:コンポーネント別、2021年~2034年

- 主要動向

- 電子制御ユニット(ECU)

- 配電ボックス

- アクチュエータ・センサー

- 通信インターフェース

- 配線ハーネス

- その他

第9章 市場推計・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- 英国

- ドイツ

- フランス

- イタリア

- スペイン

- ロシア

- 北欧諸国

- アジア太平洋

- 中国

- インド

- 日本

- オーストラリア

- 韓国

- 東南アジア

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- アラブ首長国連邦

- 南アフリカ

- サウジアラビア

第10章 企業プロファイル

- Aptiv

- Continental

- Denso

- Faurecia

- Harman International

- Hitachi Astemo

- Hyundai Mobis

- Infineon Technologies

- Lear

- Magna International

- Marelli

- NXP Semiconductors

- Panasonic

- Renesas Electronics

- Robert Bosch

- STMicroelectronics

- Texas Instruments

- Valeo

- Visteon

- ZF Friedrichshafen

目次

The Global Automotive E-E Architecture Market was valued at USD 79.4 billion in 2024 and is estimated to grow at a CAGR of 6.6%, reaching USD 148.6 billion by 2034, driven by the rising adoption of electric vehicles (EVs), increasing vehicle connectivity, and the growing demand for autonomous driving technologies. Automotive E-E (Electrical and Electronics) architecture underpins the critical functions of modern vehicles, managing everything from powertrains and infotainment to advanced driver-assistance systems (ADAS) and connectivity solutions. The shift towards zonal and centralized architectures enhances vehicle performance by reducing wiring complexity, improving data processing speeds, and enabling seamless integration of sophisticated technologies such as AI, machine learning, and V2X communication.

Centralized computing platforms are becoming essential for supporting the massive data generated by sensors, cameras, and communication networks in connected and autonomous vehicles. Moreover, the push for sustainable mobility and stricter regulatory standards, such as Euro 7 and China VI, is prompting automakers to redesign their E-E systems for greater energy efficiency, cybersecurity, and compliance. Moreover, the push for sustainable mobility and stricter regulatory standards, such as Euro 7 in Europe and China VI in Asia, is prompting automakers to redesign their E-E systems for greater energy efficiency, cybersecurity, and regulatory compliance. These evolving regulations demand not only lower vehicle emissions but also higher standards for vehicle safety, connectivity, and data security.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $79.4 Billion |

| Forecast Value | $148.6 Billion |

| CAGR | 6.6% |

The Automotive E-E Architecture Market is primarily segmented by type, with distributed E/E architecture leading in 2024, generating USD 36.7 billion. Distributed architectures, characterized by multiple independent electronic control units (ECUs) controlling various vehicle functions, have been widely adopted due to their flexibility, ease of integration, and scalability. This design allows automakers to independently upgrade specific vehicle systems without overhauling the entire network. However, as vehicles become increasingly software-defined and data-intensive, the industry is gradually transitioning toward domain and zonal architectures, which offer centralized control, improved data management, lower system complexity, and reduced wiring costs.

Based on vehicle type, passenger vehicles captured the largest market share in 2024, accounting for USD 43.6 billion. The rising demand for personal vehicles equipped with premium features such as Advanced Driver Assistance Systems (ADAS), next-generation infotainment systems, connectivity services, and electric powertrains is fueling the adoption of sophisticated E-E architectures in this segment. Advanced architectures allow seamless communication between various vehicle systems, enhancing driver assistance capabilities, improving vehicle diagnostics, enabling autonomous features, and elevating the overall driving experience.

Asia Pacific Automotive E-E Architecture Market reached USD 27.95 billion in 2024, driven by rapid electric vehicle (EV) adoption, smart city initiatives, and strong automotive manufacturing bases in China, Japan, and South Korea. China continues to lead the regional market due to its aggressive EV policies, extensive smart infrastructure development, and growing domestic EV brands. Japan and South Korea invest heavily in autonomous vehicle technologies and 5G-enabled V2X communication systems, further boosting the need for advanced E-E architectures. Government incentives, subsidies for EV adoption, and substantial RandD investments in next-generation mobility solutions are accelerating the integration of modern, scalable E-E systems across the region.

Major players such as Robert Bosch GmbH, Continental AG, Aptiv PLC, ZF Friedrichshafen AG, and Denso Corporation are actively investing in RandD, forming strategic partnerships, and developing modular, software-defined E-E platforms to stay competitive. The focus on enhancing cybersecurity, scalability, and energy management is set to define the next generation of automotive electrical and electronic architectures worldwide.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.1.1 Research approach

- 1.1.2 Data collection methods

- 1.2 Base estimates & calculations

- 1.2.1 Base year calculation

- 1.2.2 Key trends for market estimation

- 1.3 Forecast model

- 1.4 Primary research and validation

- 1.4.1 Primary sources

- 1.4.2 Data mining sources

- 1.5 Market scope & definition

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Supplier landscape

- 3.2.1 E-E architecture providers

- 3.2.2 Component providers

- 3.2.3 Distributors

- 3.2.4 End Use

- 3.3 Impact of trump administration tariffs

- 3.3.1 Impact on trade

- 3.3.1.1 Trade volume disruptions

- 3.3.1.2 Retaliatory measures

- 3.3.2 Impact on industry

- 3.3.2.1 Supply-side impact (raw materials)

- 3.3.2.1.1 Price volatility in key materials

- 3.3.2.1.2 Supply chain restructuring

- 3.3.2.1.3 Production cost implications

- 3.3.2.2 Demand-side impact (selling price)

- 3.3.2.2.1 Price transmission to end markets

- 3.3.2.2.2 Market share dynamics

- 3.3.2.2.3 Consumer response patterns

- 3.3.2.1 Supply-side impact (raw materials)

- 3.3.3 Key companies impacted

- 3.3.4 Strategic industry responses

- 3.3.4.1 Supply chain reconfiguration

- 3.3.4.2 Pricing and product strategies

- 3.3.4.3 Policy engagement

- 3.3.5 Outlook & future considerations

- 3.3.1 Impact on trade

- 3.4 Profit margin analysis

- 3.5 Technology & innovation landscape

- 3.6 Patent analysis

- 3.7 Pricing analysis

- 3.8 Key news & initiatives

- 3.9 Regulatory landscape

- 3.10 Impact forces

- 3.10.1 Growth drivers

- 3.10.1.1 Growing demand for electric vehicles (EVs)

- 3.10.1.2 Increasing focus on vehicle safety and regulatory standards

- 3.10.1.3 Rising adoption of Advanced Driver Assistance Systems (ADAS)

- 3.10.1.4 Demand for connected cars and vehicle-to-everything (V2X) communication

- 3.10.2 Industry pitfalls & challenges

- 3.10.2.1 High complexity and cost of developing advanced E/E architectures

- 3.10.2.2 Cybersecurity risks associated with increasing vehicle connectivity

- 3.10.1 Growth drivers

- 3.11 Growth potential analysis

- 3.12 Porter's analysis

- 3.13 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Type, 2021 - 2034 ($Bn)

- 5.1 Key trends

- 5.2 Distributed E/E architecture

- 5.3 Domain E/E architecture

- 5.4 Zonal architecture

Chapter 6 Market Estimates & Forecast, By Vehicle, 2021 - 2034 ($Bn)

- 6.1 Key trends

- 6.2 Passenger vehicles

- 6.2.1 Hatchback

- 6.2.2 Sedan

- 6.2.3 SUV

- 6.3 Commercial vehicles

- 6.3.1 Light Commercial Vehicles (LCV)

- 6.3.2 Medium Commercial Vehicles (MCV)

- 6.3.3 Heavy Commercial Vehicles (HCV)

Chapter 7 Market Estimates & Forecast, By Propulsion, 2021 - 2034 ($Bn)

- 7.1 Key trends

- 7.2 ICE

- 7.3 Electric vehicles

- 7.3.1 Battery Electric Vehicles (BEV)

- 7.3.2 Plug-in Hybrid Electric Vehicles (PHEV)

- 7.3.3 Hybrid Electric Vehicles (HEV)

Chapter 8 Market Estimates & Forecast, By Component, 2021 - 2034 ($Bn)

- 8.1 Key trends

- 8.2 Electronic Control Units (ECUs)

- 8.3 Power distribution boxes

- 8.4 Actuators and sensors

- 8.5 Communication interfaces

- 8.6 Wiring harnesses

- 8.7 Others

Chapter 9 Market Estimates & Forecast, By Region, 2021 - 2034 ($Bn)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 UK

- 9.3.2 Germany

- 9.3.3 France

- 9.3.4 Italy

- 9.3.5 Spain

- 9.3.6 Russia

- 9.3.7 Nordics

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.4.6 Southeast Asia

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 MEA

- 9.6.1 UAE

- 9.6.2 South Africa

- 9.6.3 Saudi Arabia

Chapter 10 Company Profiles

- 10.1 Aptiv

- 10.2 Continental

- 10.3 Denso

- 10.4 Faurecia

- 10.5 Harman International

- 10.6 Hitachi Astemo

- 10.7 Hyundai Mobis

- 10.8 Infineon Technologies

- 10.9 Lear

- 10.10 Magna International

- 10.11 Marelli

- 10.12 NXP Semiconductors

- 10.13 Panasonic

- 10.14 Renesas Electronics

- 10.15 Robert Bosch

- 10.16 STMicroelectronics

- 10.17 Texas Instruments

- 10.18 Valeo

- 10.19 Visteon

- 10.20 ZF Friedrichshafen

- 発行日

- 発行

- Global Market Insights Inc.

- ページ情報

- 英文 170 Pages

- 納期

- 2~3営業日