自動車用エッジコンピューティングの市場機会、成長促進要因、産業動向分析、予測、2025年~2034年

Automotive Edge Computing Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034- 発行日

- ページ情報

- 英文 170 Pages

- 納期

- 2~3営業日

- 商品コード

- 1766187

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

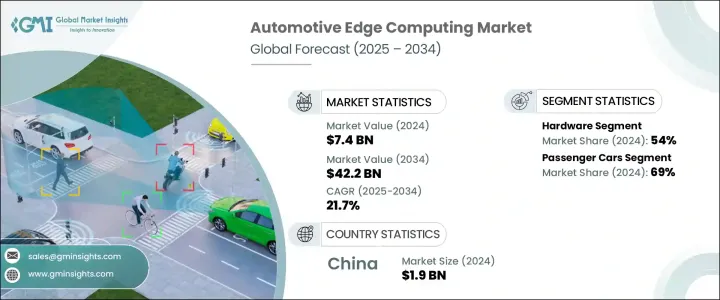

自動車用エッジコンピューティングの世界市場規模は、2024年に74億米ドルと評価され、2034年には422億米ドルに達し、CAGRで21.7%の成長が予測されています。

自動車産業が急速に進化するにつれて、自動車は膨大な量のデータをリアルタイムで処理できるインテリジェントなプラットフォームになりつつあります。この変革は、自動運転技術やコネクテッドモビリティソリューションの急増によって推進されています。その結果、従来の集中型コンピューティングモデルからエッジベースのデータ処理へと大きくシフトしています。

自動車用エッジコンピューティングは、複雑な車載機能を管理するために必要な低レイテンシーと高帯域幅を提供することで、このシフトをサポートする極めて重要な役割を果たしています。エッジコンピューティングは、現代の自動車の安全かつ効率的な運用に不可欠なリアルタイムの意思決定能力を強化します。コネクテッド機能の普及と高度な車載センサーの利用拡大は、データの爆発的な増加に寄与しており、車載分析と即時対応システムへの切迫したニーズを生み出しています。エッジコンピューティングは、データを遠方のクラウドセンターにルーティングするのではなく、車両が情報源で分析し、それに基づいて行動することを可能にします。これにより、ネットワークの混雑と応答時間が軽減され、パフォーマンス、安全性、信頼性が向上します。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 74億米ドル |

| 予測金額 | 422億米ドル |

| CAGR | 21.7% |

これは、運転支援、予知保全、インテリジェントな経路計画などのアプリケーションに不可欠になりつつあります。メーカーがソフトウェア中心の車両アーキテクチャに移行する中、次世代モビリティのために構築された拡張性が高く、安全で効率的な輸送システムを構築するには、先進的なエッジプラットフォームの統合が不可欠となります。

コンポーネントの観点から、市場はハードウェア、ソフトウェア、サービスに分類されます。ハードウェアは、2024年には世界市場シェアの54%近くを占める主要セグメントに浮上し、予測期間を通じて22%を超えるCAGRで成長すると予測されています。高性能コンピューティングユニット、AIに最適化されたプロセッサ、車載グレードのモジュールの導入が増加していることは、複雑なデータストリームを処理するエッジハードウェアの重要性が高まっていることを裏付けています。これらのコンポーネントは、リアルタイムのモニタリングや自律走行ナビゲーションなどのアプリケーションの継続的な処理能力を確保しながら、過酷な車両環境に耐えられるように設計されています。

車両別では、市場は乗用車と商用車に分けられます。乗用車は2024年に市場総収益の約69%を占め、支配的な地位を占めています。このセグメントは、2025年から2034年にかけてCAGR23%以上で拡大すると見られています。乗用車における統合デジタル機能、パーソナライズされたドライバー体験、ADAS(先進運転支援システム)への需要の高まりが、エッジコンピューティング技術の導入を促進しています。これらの車両は、さまざまな組み込みシステムからのデータ入力を管理し、ユーザー体験と車両の安全性の両方を向上させるリアルタイムの意思決定を可能にする、堅牢な処理能力を必要としています。

展開モードに基づき、業界はクラウドベースとオンプレミスのソリューションに区分されます。クラウドベースの導入は、その柔軟性、拡張性、幅広いコネクテッドビークル機能をサポートする能力により、引き続き市場で大きなシェアを占めています。これらのプラットフォームは、シームレスなソフトウェア統合、リモート更新、集中調整を可能にし、自律走行や車両管理における新たな使用事例に不可欠です。こうしたプラットフォームの普及は、ダイナミックなルート最適化、インフォテインメント配信、予測診断などのサービスをサポートするビークルツークラウドインフラへの依存度の高まりによって後押しされています。

地域別では、中国が2024年の世界の自動車用エッジコンピューティング市場をリードし、約19億米ドルの収益を上げ、アジア太平洋市場の約63%を占めました。同国は、世界最大の自動車生産国としての地位と相まって、スマートモビリティ構想の急速な拡大により、エッジ技術採用の最前線に位置しています。政府の強力な支援、電気自動車の急速な市場開拓、コネクテッドビークルシステムの大規模な展開が、この地域の市場成長を引き続き後押ししています。

自動車メーカーとテクノロジープロバイダーが、より高速でインテリジェントな分散型処理システムを優先しているため、自動車用エッジコンピューティングの状況は構造的な変革期を迎えています。特に安全性が重視される運転環境では、瞬時のデータ解釈に対する要求が高まっており、自動車内での情報処理方法の根本的な見直しが促されています。各社は現在、AI機能、軽量データ処理フレームワーク、堅牢なセキュリティプロトコルを車載環境に直接統合することに注力しています。これらの進歩は、未加工のセンサー出力を、リアルタイムで対応可能な意味のある洞察に変換し、より安全で、適応性が高く、効率的な交通システムを実現するように設計されています。

目次

第1章 調査手法

- 市場の範囲と定義

- 調査デザイン

- 調査アプローチ

- データ収集方法

- データマイニングソース

- 世界

- 地域/国

- 基本推定と計算

- 基準年計算

- 市場予測の主な動向

- 1次調査と検証

- 一次情報

- 予測モデル

- 調査の前提と限界

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- サプライヤーの情勢

- 利益率分析

- コスト構造

- 各段階での付加価値

- バリューチェーンに影響を与える要因

- ディスラプション

- 業界への影響要因

- 促進要因

- 自動運転車とコネクテッドカーの需要の高まり

- 車載センサーからのデータ量の増加

- 強化されたインフォテインメントと車内体験

- 道路安全とデータのローカライゼーションに関する政府規制

- 業界の潜在的リスク&課題

- 初期インフラコストが高め

- データプライバシーとコンプライアンスの複雑さ

- 市場機会

- 意思決定のためのAIとMLの統合

- スマートシティとV2Xエコシステムの拡大

- 促進要因

- 成長可能性分析

- 規制情勢

- 北米

- 欧州

- アジア太平洋地域

- ラテンアメリカ

- 中東・アフリカ

- ポーター分析

- PESTEL分析

- テクノロジーとイノベーションの情勢

- 現在の技術動向

- 新興技術

- コスト内訳分析

- ソフトウェア開発およびライセンシング費用

- 導入と統合のコスト

- 保守・サポート費用

- サイバーセキュリティとコンプライアンスのコスト

- トレーニングと変更管理コスト

- 特許分析

- 持続可能性と環境側面

- 持続可能な慣行

- 廃棄物削減戦略

- 生産におけるエネルギー効率

- 環境に優しい取り組み

- カーボンフットプリントの考慮

- ユースケース

- 最良のシナリオ

- 消費者行動と採用動向

- ユーザーエクスペリエンスとインターフェースの動向

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 北米

- 欧州

- アジア太平洋地域

- ラテンアメリカ航空

- 中東・アフリカ

- 主要市場企業の競合分析

- 競合ポジショニングマトリックス

- 戦略的展望マトリックス

- 主な発展

- 合併と買収

- パートナーシップとコラボレーション

- 新製品の発売

- 拡張計画と資金調達

第5章 市場推定・予測:コンポーネント別、2021年~2034年

- 主要動向

- ハードウェア

- エッジノード

- ゲートウェイ

- エッジサーバー

- ソフトウェア

- エッジデバイス管理

- アナリティクス・処理ソフトウェア

- セキュリティソフトウェア

- サービス

- プロフェッショナル

- システム統合・展開

- コンサルティング・戦略

- トレーニング・サポート

- マネージド

- リモートモニタリング・管理

- メンテナンス・アップデート

- セキュリティ管理

- プロフェッショナル

第6章 市場推定・予測:車両別、2021年~2034年

- 主要動向

- 乗用車

- セダン

- ハッチバック

- SUV

- 商用車

- 小型

- 中型

- 大型

第7章 市場推定・予測:展開モード別、2021年~2034年

- 主要動向

- クラウドベース

- オンプレミス

第8章 市場推定・予測:企業規模別、2021年~2034年

- 主要動向

- 中小企業

- 大企業

第9章 市場推定・予測:アプリケーション別、2021年~2034年

- 主要動向

- 自動運転・コネクテッドドライビング

- 車内エクスペリエンス・インフォテインメント

- 予測メンテナンス・診断

- 車両・トラフィック管理

- サイバーセキュリティ・データ保護

第10章 市場推定・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- スペイン

- 北欧諸国

- ロシア

- アジア太平洋地域

- 中国

- インド

- 日本

- オーストラリア

- 韓国

- 東南アジア

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- 南アフリカ

- サウジアラビア

- アラブ首長国連邦

第11章 企業プロファイル

- Amazon

- Arteris IP

- Autotalks

- Bosch Group

- Cisco

- ETAS GmbH

- FogHorn Systems

- GreenWave Systems

- Hewlett Packard Enterprise(HPE)

- Huawei

- IBM

- Infineon Technologies

- Intel

- Microsoft

- Mobileye

- NVIDIA

- NXP Semiconductors

- Qualcomm Technologies

- Siemens

- Teradata

目次

The Global Automotive Edge Computing Market was valued at USD 7.4 billion in 2024 and is estimated to grow at a CAGR of 21.7% to reach USD 42.2 billion by 2034. As the automotive industry rapidly evolves, vehicles are increasingly becoming intelligent platforms capable of processing vast amounts of data in real time. This transformation is being driven by the surge in autonomous driving technologies and connected mobility solutions. As a result, there is a significant shift away from traditional centralized computing models to edge-based data processing, which places computational power closer to the source-inside the vehicle itself.

Automotive edge computing is playing a pivotal role in supporting this shift by delivering the low latency and high bandwidth required to manage complex in-vehicle functions. It enhances real-time decision-making capabilities critical to the safe and efficient operation of modern vehicles. The proliferation of connected features and the growing use of advanced in-vehicle sensors are contributing to an explosion of data, creating a pressing need for on-board analytics and instant response systems. Rather than routing data to distant cloud centers, edge computing empowers vehicles to analyze and act on information at the source, reducing network congestion and response time while enhancing performance, safety, and reliability.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $7.4 Billion |

| Forecast Value | $42.2 Billion |

| CAGR | 21.7% |

This is becoming essential for applications such as driver assistance, predictive maintenance, and intelligent route planning. As manufacturers transition toward software-centric vehicle architectures, the integration of advanced edge platforms becomes vital for creating scalable, secure, and efficient transportation systems built for the next generation of mobility.

In terms of components, the market is categorized into hardware, software, and services. Hardware emerged as the leading segment in 2024, contributing nearly 54% of the global market share, and is anticipated to grow at a CAGR exceeding 22% throughout the forecast period. The rising deployment of high-performance computing units, AI-optimized processors, and automotive-grade modules underscores the growing importance of edge hardware in handling complex data streams. These components are engineered to endure extreme vehicle environments while ensuring continuous processing power for applications like real-time monitoring and autonomous navigation.

By vehicle type, the market is divided into passenger cars and commercial vehicles. Passenger cars held a dominant position in 2024, accounting for approximately 69% of the total market revenue. This segment is set to expand at a CAGR of over 23% between 2025 and 2034. The increasing demand for integrated digital features, personalized driver experiences, and advanced driver-assist systems in passenger vehicles is driving the uptake of edge computing technologies. These vehicles require robust processing capabilities to manage data inputs from various embedded systems, enabling real-time decisions that improve both user experience and vehicle safety.

Based on deployment mode, the industry is segmented into cloud-based and on-premises solutions. Cloud-based deployment continues to command a significant share of the market due to its flexibility, scalability, and ability to support a wide range of connected vehicle functions. These platforms allow seamless software integration, remote updates, and centralized coordination, which are critical for emerging use cases in autonomous driving and fleet management. Their widespread adoption is being propelled by the increasing reliance on vehicle-to-cloud infrastructure that supports services like dynamic route optimization, infotainment delivery, and predictive diagnostics.

Regionally, China led the global automotive edge computing market in 2024, generating around USD 1.9 billion in revenue and capturing roughly 63% of the Asia Pacific market. The country's rapid expansion in smart mobility initiatives, coupled with its position as the world's largest automotive producer, has positioned it at the forefront of edge technology adoption. Strong governmental support, fast-paced development in electric vehicles, and massive deployment of connected vehicle systems continue to bolster market growth in the region.

The automotive edge computing landscape is undergoing a structural transformation as automakers and technology providers prioritize faster, more intelligent, and decentralized processing systems. Growing requirements for instantaneous data interpretation, especially in safety-sensitive driving conditions, are prompting a fundamental rethinking of how information is handled within vehicles. Companies are now focused on integrating AI capabilities, lightweight data processing frameworks, and robust security protocols directly into in-vehicle environments. These advancements are designed to transform raw sensor outputs into meaningful insights that can be acted upon in real time, thus enabling safer, more adaptive, and more efficient transportation systems.

Table of Contents

Chapter 1 Methodology

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis, 2021 – 2034

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Component

- 2.2.3 Vehicle

- 2.2.4 Deployment mode

- 2.2.5 Enterprise size

- 2.2.6 Application

- 2.3 TAM Analysis, 2025-2034

- 2.4 CXO perspectives: strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin analysis

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Growing demand for autonomous and connected vehicles

- 3.2.1.2 Increasing data volume from in-vehicle sensors

- 3.2.1.3 Enhanced infotainment and in-vehicle experience

- 3.2.1.4 Government regulations for road safety and data localization

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High initial infrastructure cost

- 3.2.2.2 Data privacy & compliance complexities

- 3.2.3 Market opportunities

- 3.2.3.1 Integration with AI and ML for decision-making

- 3.2.3.2. Smart city & V2 X ecosystem expansion

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Cost breakdown analysis

- 3.8.1 Software development & licensing cost

- 3.8.2 Deployment & integration cost

- 3.8.3 Maintenance & support cost

- 3.8.4 Cybersecurity & compliance cost

- 3.8.5 Training & change management cost

- 3.9 Patent analysis

- 3.10 Sustainability and environmental aspects

- 3.10.1 Sustainable practices

- 3.10.2 Waste reduction strategies

- 3.10.3 Energy efficiency in production

- 3.10.4 Eco-friendly Initiatives

- 3.10.5 Carbon footprint considerations

- 3.11 Use cases

- 3.12 Best-case scenario

- 3.13 Consumer behaviour & adoption trends

- 3.14 User experience & interface trends

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 LATAM

- 4.2.5 MEA

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategic outlook matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans and funding

Chapter 5 Market Estimates & Forecast, By Component, 2021 - 2034 ($Mn)

- 5.1 Key trends

- 5.2 Hardware

- 5.2.1 Edge nodes

- 5.2.2 Gateways

- 5.2.3 Edge servers

- 5.3 Software

- 5.3.1 Edge device management

- 5.3.2 Analytics & processing software

- 5.3.3 Security software

- 5.4 Services

- 5.4.1 Professional

- 5.4.1.1 System integration & deployment

- 5.4.1.2 Consulting & strategy

- 5.4.1.3 Training & support

- 5.4.2 Managed

- 5.4.2.1 Remote monitoring & management

- 5.4.2.2 Maintenance & updates

- 5.4.2.3 Security management

- 5.4.1 Professional

Chapter 6 Market Estimates & Forecast, By Vehicle, 2021 - 2034 ($Mn)

- 6.1 Key trends

- 6.2 Passenger cars

- 6.2.1 Sedans

- 6.2.2 Hatchbacks

- 6.2.3 SUVs

- 6.3 Commercial vehicles

- 6.3.1 Light duty

- 6.3.2 Medium duty

- 6.3.3 Heavy duty

Chapter 7 Market Estimates & Forecast, By Deployment Mode, 2021 - 2034 ($Mn)

- 7.1 Key trends

- 7.2 Cloud-based

- 7.3 On-premises

Chapter 8 Market Estimates & Forecast, By Enterprise Size, 2021 - 2034 ($Mn)

- 8.1 Key trends

- 8.2 SME

- 8.3 Large enterprises

Chapter 9 Market Estimates & Forecast, By Application, 2021 - 2034 ($Mn)

- 9.1 Key trends

- 9.2 Autonomous and connected driving

- 9.3 In-vehicle experience & infotainment

- 9.4 Predictive maintenance & diagnostics

- 9.5 Fleet & traffic management

- 9.6 Cybersecurity & data protection

Chapter 10 Market Estimates & Forecast, By Region, 2021 - 2034 ($Mn)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Italy

- 10.3.5 Spain

- 10.3.6 Nordics

- 10.3.7 Russia

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 Australia

- 10.4.5 South Korea

- 10.4.6 Southeast Asia

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 MEA

- 10.6.1 South Africa

- 10.6.2 Saudi Arabia

- 10.6.3 UAE

Chapter 11 Company Profiles

- 11.1 Amazon

- 11.2 Arteris IP

- 11.3 Autotalks

- 11.4 Bosch Group

- 11.5 Cisco

- 11.6 ETAS GmbH

- 11.7 FogHorn Systems

- 11.8 GreenWave Systems

- 11.9 Hewlett Packard Enterprise (HPE)

- 11.10 Huawei

- 11.11 IBM

- 11.12 Infineon Technologies

- 11.13 Intel

- 11.14 Microsoft

- 11.15 Mobileye

- 11.16 NVIDIA

- 11.17 NXP Semiconductors

- 11.18 Qualcomm Technologies

- 11.19 Siemens

- 11.20 Teradata

- 発行日

- 発行

- Global Market Insights Inc.

- ページ情報

- 英文 170 Pages

- 納期

- 2~3営業日