|

市場調査レポート

商品コード

1740991

自動車ローン組成ソフトウェアの市場機会、成長促進要因、業界動向分析、2025年~2034年予測Auto Loan Origination Software Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| 自動車ローン組成ソフトウェアの市場機会、成長促進要因、業界動向分析、2025年~2034年予測 |

|

出版日: 2025年04月29日

発行: Global Market Insights Inc.

ページ情報: 英文 170 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

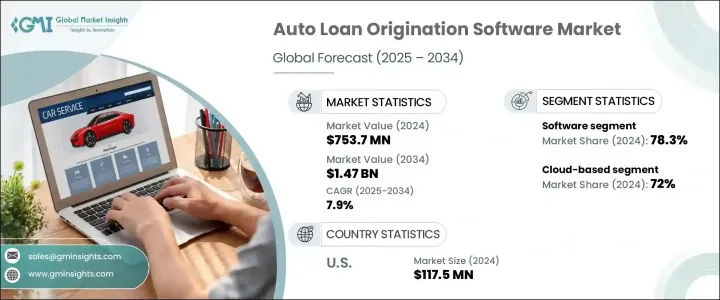

自動車ローン組成ソフトウェアの世界市場規模は、2024年に7億5,370万米ドルとなり、CAGR 7.9%で成長し、2034年には14億7,000万米ドルに達すると予測されています。

より効率的で正確、かつシームレスな融資プロセスへの需要が高まる中、金融機関はデジタル化が進む今日の世界で消費者の期待に応えるべくテクノロジーに注目しています。自動車ローン組成ソフトウェアは、申込受付、書類確認、信用評価、最終承認などの複雑な作業を自動化する上で重要な役割を果たし、金融機関にエンドツーエンドのデジタル融資ソリューションを提供しています。この市場は、借り手の満足度を向上させながら、処理時間や業務上のオーバーヘッドを削減することを目指す貸し手が増えるにつれて、勢いを増しています。この成長を後押ししている主な要因は、顧客体験への注目が高まっていることです。借り手は今日、迅速な承認、最小限の事務処理、個別化されたサービスを期待しており、ローン組成プラットフォームはまさにそれを可能にしています。合理的で透明性が高く、直感的なデジタル・レンディング・ジャーニーを提供するこれらのソリューションは、競争が激化する市場で金融機関が顧客を引き付け、維持するのに役立っています。金融機関はまた、安全で拡張性があり、高度なカスタマイズが可能な適応性の高いソリューションを優先しているため、借り手の行動や規制が変化する中でも機敏に対応することができます。ローン申し込みのデジタル・チャネルの普及に伴い、柔軟性の高いクラウドベースのシステムの必要性がこれまで以上に高まっています。

市場は構成要素に基づいてソフトウェアとサービスに区分されます。2024年の市場シェアはソフトウェアが約78.3%を占め、予測期間を通じてCAGR 8.3%以上で成長すると予測されます。ソフトウェア・プラットフォームは、その拡張性、柔軟性、申請から承認までのローン処理を合理化する能力から好まれています。これらのシステムは、リスク分析、本人確認、信用スコアリングといった時間のかかる作業を自動化し、既存の金融インフラにシームレスに統合できるように設計されています。金融機関は、AIベースのスコアリング・モデル、CRMシステム、リアルタイムの申請追跡などの高度な機能を組み合わせたインテリジェント・プラットフォームを選択する傾向が強まっています。こうした統合ソリューションは、融資実行プロセスを迅速化するだけでなく、より安全でコンプライアンスに準拠した融資エコシステムにも貢献しています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 7億5,370万米ドル |

| 予測金額 | 14億7,000万米ドル |

| CAGR | 7.9% |

デプロイメント別に見ると、市場はオンプレミスとクラウドベースのプラットフォームに分かれます。2024年には、クラウドベースの展開が72%という圧倒的なシェアで市場をリードし、2034年まで8.4%以上の成長率を維持すると予想されています。金融機関は、動的なスケーリング、リアルタイムの更新、システム間のシームレスな統合をサポートする能力により、クラウド・ソリューションをますます好むようになっています。クラウドを活用することで、金融機関はインフラ・コストを削減し、定期的なセキュリティ・パッチの恩恵を受け、従業員と顧客の双方にとってより良いアクセスを可能にすることができます。また、これらのプラットフォームは、データプライバシーを強化し、国内外の規制へのコンプライアンスを円滑にするため、データ主導の金融という現在の状況において特に魅力的なものとなっています。

用途別では、市場は乗用車向けローンと商用車向けローンに分かれています。乗用車向けセグメントは用途別内訳でリードしており、このカテゴリーで処理される自動車ローンの量が多いことから、今後も優位性が続くと予測されます。個人向けの自動車ローンを探している借り手の大半は、簡単で迅速なデジタル・プロセスを求めており、これらのプラットフォームはそれを実現するのに十分な設備が整っています。個人消費者の間では、簡素化されたモバイル・ファーストのローン申請システムに対する需要が特に強く、金融機関はオリジネーション・ソフトウェアを採用またはアップグレードする際、乗用車セグメントを優先する傾向にあります。

地域的には、北米が世界の自動車ローン組成ソフトウェア市場をリードしており、米国は2024年に約1億1,750万米ドルの売上を計上し、地域シェアの約79.6%を占める。同国の自動車購入台数の多さ、自動車融資のためのクレジットの普及、高度な金融インフラがこの優位性に寄与しています。米国の金融機関はまた、AI対応システム、デジタル文書処理、リアルタイム分析を急速に導入しており、同国を自動車融資技術における重要なイノベーターとして位置付けています。

市場の進化に伴い、ソフトウェア・プロバイダーは、データ・セキュリティと透明性に対するニーズの高まりに対応するため、エンド・ツー・エンドの暗号化、リアルタイムの不正検知、自動コンプライアンス・チェックなどの機能を優先しています。人工知能と機械学習は現在、信用リスク分析、融資の意思決定、ポートフォリオの最適化の中心となっています。保険会社、ディーラー、規制機関を含むサードパーティのエコシステムとの統合は、リアルタイムのコラボレーションと統一されたローンエクスペリエンスをさらに可能にしています。このようなテクノロジーの変革は、自動車融資をより迅速で効率的な、顧客重視のプロセスへと再構築しています。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- サプライヤーの情勢

- 金融機関および貸し手

- ソフトウェアプロバイダー

- サービスプロバイダー

- 最終用途

- トランプ政権による関税への影響

- 貿易への影響

- 貿易量の混乱

- 報復措置

- 業界への影響

- 供給側の影響(原材料)

- 主要原材料の価格変動

- サプライチェーンの再構築

- 生産コストへの影響

- 需要側の影響(顧客へのコスト)

- 最終市場への価格伝達

- 市場シェアの動向

- 消費者の反応パターン

- 供給側の影響(原材料)

- 影響を受ける主要企業

- 戦略的な業界対応

- サプライチェーンの再構成

- 価格設定と製品戦略

- 政策関与

- 展望と今後の検討事項

- 貿易への影響

- 利益率分析

- テクノロジーとイノベーションの情勢

- 特許分析

- 主なニュースと取り組み

- ユースケース

- コスト構造分析

- 影響要因

- 促進要因

- 合理化された効率的なローン処理ソリューションの需要

- 顧客体験と満足度の向上に重点を置く

- ソフトウェアの導入を促進する規制コンプライアンス要件

- 拡張性のためにクラウドベースのソリューションに移行する

- 業界の潜在的リスク&課題

- 機密情報の取り扱いにおけるプライバシーの懸念

- 規制の変更によりソフトウェアのアップデートが頻繁に必要になる

- 促進要因

- 成長可能性分析

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 競合ポジショニングマトリックス

- 戦略的展望マトリックス

第5章 市場推計・予測:コンポーネント別、2021-2034

- 主要動向

- ソフトウェア

- サービス

第6章 市場推計・予測:展開別、2021-2034

- 主要動向

- オンプレミス

- クラウドベース

第7章 市場推計・予測:用途別、2021-2034

- 主要動向

- 乗用車

- セダン

- ハッチバック

- SUV

- 商用車

- 軽作業

- 中型

- ヘビーデューティー

第8章 市場推計・予測:企業規模別、2021-2034

- 主要動向

- 中小企業

- 大企業

第9章 市場推計・予測:最終用途別、2021-2034

- 主要動向

- 銀行

- 信用組合

- 住宅ローン貸し手とブローカー

- その他

第10章 市場推計・予測:地域別、2021-2034

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- 英国

- ドイツ

- フランス

- イタリア

- スペイン

- ロシア

- 北欧諸国

- アジア太平洋地域

- 中国

- インド

- 日本

- 韓国

- オーストラリア・ニュージーランド

- 東南アジア

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- アラブ首長国連邦

- サウジアラビア

- 南アフリカ

第11章 企業プロファイル

- Avant

- Axcess Consulting Group

- Black Knight Technologies

- Byte Software

- Calyx Technology

- Financial Industry Computer Systems

- Finastra

- Fiserv

- ICE Mortgage Technology

- ISGN Corporation

- Juris Technologies

- Lending Qb

- Mortgage Builder Software

- Mortgage Cadence

- Pegasystems

- SPARK

- Tavant

- Turnkey Lender

- VSC

- Wipro

The Global Auto Loan Origination Software Market was valued at USD 753.7 million in 2024 and is estimated to grow at a CAGR of 7.9% to reach USD 1.47 billion by 2034. As demand rises for more efficient, accurate, and seamless lending processes, financial institutions are turning to technology to meet consumer expectations in today's digitally driven world. Auto loan origination software plays a vital role in automating complex tasks such as application intake, document verification, credit evaluation, and final approval, offering lenders an end-to-end digital lending solution. The market is gaining momentum as more lenders aim to cut down on processing time and operational overhead while improving borrower satisfaction. A key factor fueling this growth is the rising focus on customer experience. Borrowers today expect quick approvals, minimal paperwork, and personalized services, and loan origination platforms are enabling exactly that. By providing streamlined, transparent, and intuitive digital lending journeys, these solutions help financial institutions attract and retain customers in an increasingly competitive market. Institutions are also prioritizing secure, scalable, and adaptive solutions that offer a high degree of customization, allowing them to remain agile amid changing borrower behaviors and evolving regulations. With the growing popularity of digital channels for loan applications, the need for flexible and cloud-based systems has become more critical than ever.

The market is segmented based on components into software and services. In 2024, the software category held a dominant market share of approximately 78.3% and is projected to grow at a CAGR exceeding 8.3% throughout the forecast period. Software platforms are gaining preference for their scalability, flexibility, and ability to streamline loan processing from application to approval. These systems are engineered to automate time-intensive tasks such as risk analysis, identity validation, and credit scoring, integrating seamlessly into existing financial infrastructure. Financial organizations are increasingly opting for intelligent platforms that combine advanced functionalities, including AI-based scoring models, CRM systems, and real-time application tracking. These integrated solutions not only speed up the origination process but also contribute to a more secure and compliant lending ecosystem.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $753.7 Million |

| Forecast Value | $1.47 Billion |

| CAGR | 7.9% |

Deployment-wise, the market is split into on-premises and cloud-based platforms. In 2024, cloud-based deployment led the market with a commanding 72% share and is expected to maintain a growth rate of over 8.4% through 2034. Lenders are increasingly favoring cloud solutions due to their ability to support dynamic scaling, real-time updates, and seamless integration across systems. By leveraging the cloud, institutions can cut down on infrastructure costs, benefit from regular security patches, and enable better access for both employees and customers. These platforms also enhance data privacy and facilitate smoother compliance with local and international regulations, making them particularly attractive in the current landscape of data-driven finance.

In terms of application, the market is divided between loans for passenger cars and commercial vehicles. The passenger car segment leads the application breakdown and is forecasted to continue its dominance due to the large volume of auto loans processed in this category. Most borrowers looking for personal vehicle financing seek easy and quick digital processes, which these platforms are well-equipped to deliver. The demand for simplified, mobile-first loan application systems is particularly strong among individual consumers, pushing lenders to prioritize the passenger vehicle segment when adopting or upgrading their origination software.

Geographically, North America leads the global auto loan origination software market, with the United States contributing around USD 117.5 million in revenue and accounting for roughly 79.6% of the regional share in 2024. The country's large volume of vehicle purchases, widespread use of credit for auto financing, and advanced financial infrastructure have contributed to this dominance. Financial institutions in the U.S. are also rapidly embracing AI-enabled systems, digital document handling, and real-time analytics, positioning the nation as a key innovator in auto lending technology.

As the market evolves, software providers are prioritizing features such as end-to-end encryption, real-time fraud detection, and automated compliance checks to meet the growing need for data security and transparency. Artificial intelligence and machine learning are now central to credit risk analysis, loan decisioning, and portfolio optimization. Integration with third-party ecosystems-including insurance firms, dealerships, and regulatory bodies-is further enabling real-time collaboration and a unified loan experience. This technology transformation is reshaping auto lending into a more responsive, efficient, and customer-focused process.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.1.1 Research approach

- 1.1.2 Data collection methods

- 1.2 Base estimates and calculations

- 1.2.1 Base year calculation

- 1.2.2 Key trends for market estimates

- 1.3 Forecast model

- 1.4 Primary research & validation

- 1.4.1 Primary sources

- 1.4.2 Data mining sources

- 1.5 Market definitions

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis, 2021 - 2034

- 2.2 Business trends

- 2.2.1 Total Addressable Market (TAM), 2025-2034

- 2.3 Regional trends

- 2.4 Component trends

- 2.5 Deployment trends

- 2.6 Application trends

- 2.7 Enterprise Size trends

- 2.8 End use trends

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Supplier landscape

- 3.2.1 Financial Institutions and Lenders

- 3.2.2 Software provider

- 3.2.3 Service provider

- 3.2.4 End use

- 3.3 Impact of trump administration tariffs

- 3.3.1 Trade impact

- 3.3.1.1 Trade volume disruptions

- 3.3.1.2 Retaliatory measures

- 3.3.2 Impact on industry

- 3.3.2.1 Supply-side impact (raw materials)

- 3.3.2.1.1 Price volatility in key materials

- 3.3.2.1.2 Supply chain restructuring

- 3.3.2.1.3 Production cost implications

- 3.3.2.2 Demand-side impact (Cost to customers)

- 3.3.2.2.1 Price transmission to end markets

- 3.3.2.2.2 Market share dynamics

- 3.3.2.2.3 Consumer response patterns

- 3.3.2.1 Supply-side impact (raw materials)

- 3.3.3 Key companies impacted

- 3.3.4 Strategic industry responses

- 3.3.4.1 Supply chain reconfiguration

- 3.3.4.2 Pricing and product strategies

- 3.3.4.3 Policy engagement

- 3.3.5 Outlook & future considerations

- 3.3.1 Trade impact

- 3.4 Profit margin analysis

- 3.5 Technology & innovation landscape

- 3.6 Patent analysis

- 3.7 Key news & initiatives

- 3.8 Use cases

- 3.9 Cost structure analysis

- 3.10 Impact on forces

- 3.10.1 Growth drivers

- 3.10.1.1 Demand for streamlined efficient loan processing solutions

- 3.10.1.2 Focus on enhancing customer experience and satisfaction

- 3.10.1.3 Regulatory compliance requiremen driving software adoption

- 3.10.1.4 Shift toward cloud-based solutions for scalability

- 3.10.2 Industry pitfalls & challenges

- 3.10.2.1 Privacy concerns in handling sensitive information

- 3.10.2.2 Regulatory changes lead to frequent software updates

- 3.10.1 Growth drivers

- 3.11 Growth potential analysis

- 3.12 Porter's analysis

- 3.13 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Component, 2021 - 2034 ($Mn)

- 5.1 Key trends

- 5.2 Software

- 5.3 Services

Chapter 6 Market Estimates & Forecast, By Deployment, 2021 - 2034 ($Mn)

- 6.1 Key trends

- 6.2 On-premises

- 6.3 Cloud-based

Chapter 7 Market Estimates & Forecast, By Application, 2021 - 2034 ($Mn)

- 7.1 Key trends

- 7.2 Passenger cars

- 7.2.1 Sedans

- 7.2.2 Hatchbacks

- 7.2.3 SUV

- 7.3 Commercial vehicles

- 7.3.1 Light duty

- 7.3.2 Medium duty

- 7.3.3 Heavy duty

Chapter 8 Market Estimates & Forecast, By Enterprise Size, 2021 - 2034 ($Mn)

- 8.1 Key trends

- 8.2 SME

- 8.3 Large enterprises

Chapter 9 Market Estimates & Forecast, By End Use, 2021 - 2034 ($Mn)

- 9.1 Key trends

- 9.2 Banks

- 9.3 Credit unions

- 9.4 Mortgage lenders & brokers

- 9.5 Others

Chapter 10 Market Estimates & Forecast, By Region, 2021 - 2034 ($Mn)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 UK

- 10.3.2 Germany

- 10.3.3 France

- 10.3.4 Italy

- 10.3.5 Spain

- 10.3.6 Russia

- 10.3.7 Nordics

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 South Korea

- 10.4.5 ANZ

- 10.4.6 Southeast Asia

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 MEA

- 10.6.1 UAE

- 10.6.2 Saudi Arabia

- 10.6.3 South Africa

Chapter 11 Company Profiles

- 11.1 Avant

- 11.2 Axcess Consulting Group

- 11.3 Black Knight Technologies

- 11.4 Byte Software

- 11.5 Calyx Technology

- 11.6 Financial Industry Computer Systems

- 11.7 Finastra

- 11.8 Fiserv

- 11.9 ICE Mortgage Technology

- 11.10 ISGN Corporation

- 11.11 Juris Technologies

- 11.12 Lending Qb

- 11.13 Mortgage Builder Software

- 11.14 Mortgage Cadence

- 11.15 Pegasystems

- 11.16 SPARK

- 11.17 Tavant

- 11.18 Turnkey Lender

- 11.19 VSC

- 11.20 Wipro