|

市場調査レポート

商品コード

1740936

電動公共交通システムの市場機会、成長促進要因、産業動向分析、2025~2034年予測Electric Public Transport System Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| 電動公共交通システムの市場機会、成長促進要因、産業動向分析、2025~2034年予測 |

|

出版日: 2025年04月17日

発行: Global Market Insights Inc.

ページ情報: 英文 190 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

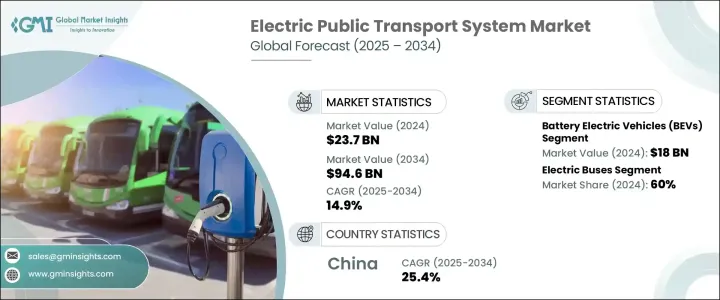

世界の電動公共交通システム市場は、2024年に237億米ドルと評価され、都市密度の増加、環境規制の強化、クリーンモビリティソリューションへの世界の機運を背景に、CAGR 14.9%で成長し、2034年には946億米ドルに達すると予測されています。

世界中の政府や交通機関は、排出量の増加、渋滞、都市のスプロール化に対処するため、持続可能なスマート交通システムへの移行を優先しています。都市の高密度化と人口急増に伴い、エネルギー効率に優れ、低排出ガスな公共交通ネットワークの需要は、重要な優先事項となっています。自動化、デジタル化、ゼロ・エミッション技術を組み合わせた電動公共交通システムは、都市モビリティの未来を再定義しつつあります。各都市は、何百万人もの通勤者にシームレスでコネクテッドな移動体験を提供するため、電動化車両、最新のインフラ、インテリジェントな交通管理システムに多額の投資を行っています。バッテリー技術、テレマティクス、ワイヤレス充電の革新は、電動車両の運行効率と信頼性をさらに高めています。スマートシティ構想が世界的に拡大する中、電気公共交通は次世代都市交通エコシステムの基幹として台頭しており、公共通勤をより環境に優しく、より速く、よりスマートにします。

都市が二酸化炭素排出量を削減し、交通インフラをアップグレードすることを目指しているため、路面電車、バス、地下鉄など、公共部門による電気公共交通への投資は急速に加速しています。電化とデジタル接続や自動化が組み合わさることで、都市のモビリティは一変し、高度な機能と効率性が日々の交通運行にもたらされています。電動公共交通ネットワークは現在、インテリジェントな路線計画、ゼロ・エミッション車両、リアルタイムの車両追跡システムを統合しています。運行事業者は、バッテリー管理システム、急速充電ソリューション、回生ブレーキなどの省エネ技術を採用し、運行コストの削減とパフォーマンスの向上を図っています。同時に、ADAS(先進運転支援システム)、車内監視システム、統合デジタルチケット販売など、利用者重視のイノベーションに対する需要も高まっています。これらのアップグレードは、輸送の安全性と乗客の快適性を高めるだけでなく、乗客への訴求力を高める。無線ソフトウェア・アップデート、軽量複合材料、無線エネルギー伝送システムなどの技術革新が、市場の成長軌道を加速させています。化石燃料を使用する輸送手段から電気代替手段が着実に取って代わる中、市場は持続可能性、自動化、通勤体験の改善に焦点を当てた継続的な技術革新で活況を呈しています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 237億米ドル |

| 予測金額 | 946億米ドル |

| CAGR | 14.9% |

バッテリー電気自動車(BEV)分野は、2024年に180億米ドルを生み出し、電動公共交通システム分野の推進力カテゴリーの中で最大のシェアを確保しました。BEVの持続的なリーダーシップは、加速する電動都市モビリティへのシフトと結びついており、そこでは低排出ガス目標が、インテリジェントでユーザー中心の車載技術に対する需要の高まりと完全に合致しています。BEVは、ゼロテールパイプエミッション、低メンテナンスニーズ、リアルタイムルート更新、対話型ダッシュボード、ADAS(先進運転支援システム)などのデジタルイノベーションとの容易な統合を提供し、車両を近代化する自治体にとって最良の選択肢となっています。

車両タイプの中では、電気バス・セグメントが2024年の市場シェアの60%を占め、電気公共交通の最も広く採用されているモードとして際立っています。このリーダーシップは、世界の環境政策の波、政府補助金の増加、公共充電ネットワークの加速度的拡大に支えられています。最新の電気バスは、持続可能なモビリティにとどまらず、静電容量式タッチスクリーン、直感的なドライバー用ディスプレイ、アダプティブ照明、人間工学に基づいた内装など、ドライバーの体感と乗客の快適性を高めるスマートな機能を提供しています。拡張性とコスト効率に優れているため、クリーンで大容量の交通機関に対する需要が急増している人口密集都市に最適です。

中国電動公共交通システム市場は、2024年に30億米ドルを生み出し、2034年まで25.4%の著しいCAGRで成長すると予測されています。この分野における中国の優位性は、持続可能なモビリティとスマートシティ開発を支持する積極的な国家戦略によって強化されています。巨額の政府資金、急速な都市化、大規模な大量輸送電化計画により、中国はイノベーションの最前線に位置し続けています。地方当局は、大容量の電気バス車両と、バッテリー管理システム、AIを活用したスケジューリング、クラウドベースのモニタリング、自律走行機能を統合したインテリジェントな交通エコシステムに多額の投資を行っており、これらすべてがダウンタイムの削減、ルートの最適化、車両ライフサイクルの延長に役立っています。

世界電動公共交通システム市場の主要企業には、VDL Bus &Coach、BYD、Yutong Bus、Heliox、EasyMile、Tata Motors、Hitachi Rail、Siemens Mobility、Alstom、Volvoが含まれます。主要企業は、モジュール式電動プラットフォームに投資し、相互運用可能な充電システムを開発し、都市交通機関と戦略的パートナーシップを結ぶことで、市場での地位を強化しています。また、エネルギーに最適化された電気自動車で製品ポートフォリオを拡大し、ADAS、テレマティクス、車両管理ソフトウェアに研究開発努力を集中することで、機敏性を維持し、世界市場で進化する規制、運用、環境要件に対応しています。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- サプライヤーの情勢

- 原材料供給者

- 部品供給業者

- 製造業者

- テクノロジープロバイダー

- 流通チャネル分析

- 最終用途

- 利益率分析

- サプライヤーの情勢

- トランプ政権による関税への影響

- 貿易への影響

- 貿易量の混乱

- 報復措置

- 業界への影響

- 供給側の影響(原材料)

- 主要原材料の価格変動

- サプライチェーンの再構築

- 生産コストへの影響

- 需要側の影響(販売価格)

- 最終市場への価格伝達

- 市場シェアの動向

- 消費者の反応パターン

- 供給側の影響(原材料)

- 戦略的な業界対応

- サプライチェーンの再構成

- 価格設定と製品戦略

- 貿易への影響

- テクノロジーとイノベーションの情勢

- 特許分析

- 規制情勢

- コスト内訳分析

- 主なニュースと取り組み

- 影響要因

- 促進要因

- 車載コネクティビティとUXの需要の高まり

- 材料と製造における技術の進歩

- 電気自動車と自動運転車の成長

- OEMは軽量化と設計統合に注力

- 業界の潜在的リスク&課題

- 高い生産コスト

- 耐久性と環境感度

- 促進要因

- 成長可能性分析

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 競合ポジショニングマトリックス

- 戦略的展望マトリックス

第5章 市場推計・予測:交通手段別、2021-2034

- 主要動向

- 電気バス

- 電気機関車

- 電気フェリー

- 電気タクシー/配車サービス

第6章 市場推計・予測:推進力別、2021-2034

- 主要動向

- バッテリー電気自動車(BEV)

- プラグインハイブリッド電気自動車(PHEV)

- 燃料電池電気自動車(FCEV)

第7章 市場推計・予測:充電することで、2021-2034

- 主要動向

- デポ充電

- 機会課金

- ワイヤレス充電

- バッテリー交換

第8章 市場推計・予測:用途別、2021-2034

- 主要動向

- 政府交通局

- 民間の船舶運航業者

- 官民パートナーシップ(PPP)

- 空港および産業輸送事業者

- その他

第9章 市場推計・予測:地域別、2021-2034

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- フランス

- 英国

- スペイン

- イタリア

- ロシア

- 北欧諸国

- アジア太平洋地域

- 中国

- インド

- 日本

- 韓国

- オーストラリア・ニュージーランド

- 東南アジア

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- アラブ首長国連邦

- 南アフリカ

- サウジアラビア

第10章 企業プロファイル

- ABB

- Alexander Dennis

- Alstom

- Ashok Leyland

- BYD

- CAF

- CRRC

- EasyMile

- Heliox

- Hitachi Rail

- Keolis

- Navya

- Proterra

- Schneider Electric

- Siemens eMobility

- Soltaro

- Tata Motors

- VDL Bus &Coach

- Volvo

- Yutong Bus

The Global Electric Public Transport System Market was valued at USD 23.7 billion in 2024 and is estimated to grow at a CAGR of 14.9% to reach USD 94.6 billion by 2034, driven by increased urban density, stricter environmental regulations, and the global momentum toward clean mobility solutions. Governments and transit agencies worldwide are prioritizing the shift to sustainable, smart transportation systems to combat rising emissions, congestion, and urban sprawl. As cities grow denser and populations surge, the demand for energy-efficient, low-emission public transport networks is becoming a critical priority. Electric public transport systems, combining automation, digitalization, and zero-emission technology, are redefining the future of urban mobility. Cities are investing heavily in electrified fleets, modern infrastructure, and intelligent traffic management systems to create seamless, connected travel experiences for millions of commuters. Innovation in battery technologies, telematics, and wireless charging is further enhancing the operational efficiency and reliability of electric fleets. As smart city initiatives expand globally, electric public transportation is emerging as the backbone of next-generation urban transit ecosystems, making public commuting greener, faster, and smarter.

Public sector investments in electric mass transit-including trams, buses, and metros-are rapidly accelerating as cities aim to lower carbon footprints and upgrade transportation infrastructure. Electrification combined with digital connectivity and automation is transforming urban mobility, bringing advanced functionality and greater efficiency into daily transit operations. Electric public transport networks are now integrating intelligent route planning, zero-emission vehicles, and real-time fleet tracking systems. Operators are adopting energy-saving technologies such as battery management systems, fast-charging solutions, and regenerative braking to drive down operating costs and boost performance. Simultaneously, demand is rising for rider-focused innovations like advanced driver assistance, onboard surveillance systems, and integrated digital ticketing. These upgrades not only enhance transit safety and passenger comfort but also increase ridership appeal. Technological breakthroughs, including over-the-air software updates, lightweight composite materials, and wireless energy transfer systems, are accelerating the market growth trajectory. As electric alternatives steadily replace fossil-fuel-based transit modes, the market is thriving with continuous innovations focused on improving sustainability, automation, and commuter experience.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $23.7 Billion |

| Forecast Value | $94.6 Billion |

| CAGR | 14.9% |

The battery electric vehicles (BEVs) segment generated USD 18 billion in 2024, securing the largest share among propulsion categories within the electric public transport system sector. Their sustained leadership is tied to the accelerating shift toward electric urban mobility, where low-emission goals align perfectly with the rising demand for intelligent, user-centric onboard technology. BEVs offer zero tailpipe emissions, lower maintenance needs, and easy integration with digital innovations such as real-time route updates, interactive dashboards, and advanced driver assistance systems, making them the top choice for municipalities modernizing their fleets.

Among vehicle types, the electric buses segment dominated with a 60% market share in 2024, standing out as the most widely adopted mode of electric public transport. This leadership is backed by a global wave of environmental policies, increasing government subsidies, and accelerated expansion of public charging networks. Modern electric buses go beyond sustainable mobility, offering smart features like capacitive touchscreens, intuitive driver displays, adaptive lighting, and ergonomic interiors that enhance both driver experience and passenger comfort. Their scalability and cost-efficiency make them ideal for densely populated cities where demand for clean, high-capacity transit is soaring.

The China Electric Public Transport System Market generated USD 3 billion in 2024 and is forecasted to grow at a remarkable CAGR of 25.4% through 2034. China's dominance in the sector is reinforced by aggressive national strategies favoring sustainable mobility and smart city development. Massive government funding, rapid urbanization, and extensive mass transit electrification plans continue to place China at the forefront of innovation. Local authorities are investing heavily in high-capacity electric bus fleets and intelligent traffic ecosystems that integrate battery management systems, AI-powered scheduling, cloud-based monitoring, and autonomous driving capabilities, all helping to reduce downtime, optimize routes, and extend vehicle lifecycles.

Major players in the Global Electric Public Transport System Market include VDL Bus & Coach, BYD, Yutong Bus, Heliox, EasyMile, Tata Motors, Hitachi Rail, Siemens Mobility, Alstom, and Volvo. Leading companies are strengthening their market positions by investing in modular electric platforms, developing interoperable charging systems, and forming strategic partnerships with urban transit agencies. They are also expanding product portfolios with energy-optimized electric vehicles and focusing R&D efforts on ADAS, telematics, and fleet management software to stay agile and meet evolving regulatory, operational, and environmental requirements across global markets.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.1.1 Research approach

- 1.1.2 Data collection methods

- 1.2 Base estimates & calculations

- 1.2.1 Base year calculation

- 1.2.2 Key trends for market estimation

- 1.3 Forecast model

- 1.4 Primary research and validation

- 1.4.1 Primary sources

- 1.4.2 Data mining sources

- 1.5 Market scope & definition

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.1.1 Raw material providers

- 3.1.1.2 Component providers

- 3.1.1.3 Manufacturers

- 3.1.1.4 Technology providers

- 3.1.1.5 Distribution channel analysis

- 3.1.1.6 End use

- 3.1.2 Profit margin analysis

- 3.1.1 Supplier landscape

- 3.2 Impact of Trump administration tariffs

- 3.2.1 Trade impact

- 3.2.1.1 Trade volume disruptions

- 3.2.1.2 Retaliatory measures

- 3.2.2 Impact on industry

- 3.2.2.1 Supply-side impact (raw materials)

- 3.2.2.1.1 Price volatility in key materials

- 3.2.2.1.2 Supply chain restructuring

- 3.2.2.1.3 Production cost implications

- 3.2.2.2 Demand-side impact (selling price)

- 3.2.2.2.1 Price transmission to end markets

- 3.2.2.2.2 Market share dynamics

- 3.2.2.2.3 Consumer response patterns

- 3.2.2.1 Supply-side impact (raw materials)

- 3.2.3 Strategic industry responses

- 3.2.3.1 Supply chain reconfiguration

- 3.2.3.2 Pricing and product strategies

- 3.2.1 Trade impact

- 3.3 Technology & innovation landscape

- 3.4 Patent analysis

- 3.5 Regulatory landscape

- 3.6 Cost breakdown analysis

- 3.7 Key news & initiatives

- 3.8 Impact forces

- 3.8.1 Growth drivers

- 3.8.1.1 Rising demand for in-vehicle connectivity and UX

- 3.8.1.2 Technological advancements in materials & manufacturing

- 3.8.1.3 Growth in electric and autonomous vehicles

- 3.8.1.4 OEM focus on weight reduction and design integration

- 3.8.2 Industry pitfalls & challenges

- 3.8.2.1 High Production Costs

- 3.8.2.2 Durability and Environmental Sensitivity

- 3.8.1 Growth drivers

- 3.9 Growth potential analysis

- 3.10 Porter's analysis

- 3.11 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Mode of Transport, 2021 - 2034 ($Mn, Units)

- 5.1 Key trends

- 5.2 Electric buses

- 5.3 Electric trains

- 5.4 Electric ferries

- 5.5 Electric taxis/ride-hailing

Chapter 6 Market Estimates & Forecast, By Propulsion, 2021 - 2034 ($Mn, Units)

- 6.1 Key trends

- 6.2 Battery Electric Vehicles (BEV)

- 6.3 Plug-in Hybrid Electric Vehicles (PHEV)

- 6.4 Fuel Cell Electric Vehicles (FCEV)

Chapter 7 Market Estimates & Forecast, By Charging, 2021 - 2034 ($Mn, Units)

- 7.1 Key trends

- 7.2 Depot charging

- 7.3 Opportunity charging

- 7.4 Wireless charging

- 7.5 Battery swapping

Chapter 8 Market Estimates & Forecast, By Application, 2021 - 2034 ($Mn, Units)

- 8.1 Key trends

- 8.2 Government transit authorities

- 8.3 Private fleet operators

- 8.4 Public-Private Partnerships (PPPs)

- 8.5 Airport & industrial transit operators

- 8.6 Others

Chapter 9 Market Estimates & Forecast, By Region, 2021 - 2034 ($Mn, Units)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 France

- 9.3.3 UK

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Russia

- 9.3.7 Nordics

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 South Korea

- 9.4.5 ANZ

- 9.4.6 Southeast Asia

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 MEA

- 9.6.1 UAE

- 9.6.2 South Africa

- 9.6.3 Saudi Arabia

Chapter 10 Company Profiles

- 10.1 ABB

- 10.2 Alexander Dennis

- 10.3 Alstom

- 10.4 Ashok Leyland

- 10.5 BYD

- 10.6 CAF

- 10.7 CRRC

- 10.8 EasyMile

- 10.9 Heliox

- 10.10 Hitachi Rail

- 10.11 Keolis

- 10.12 Navya

- 10.13 Proterra

- 10.14 Schneider Electric

- 10.15 Siemens eMobility

- 10.16 Soltaro

- 10.17 Tata Motors

- 10.18 VDL Bus & Coach

- 10.19 Volvo

- 10.20 Yutong Bus