|

市場調査レポート

商品コード

1740926

ポリエチレン透明バリア包装フィルムの市場機会、成長促進要因、産業動向分析、2025年~2034年予測Polyethylene (PE) Transparent Barrier Packaging Films Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| ポリエチレン透明バリア包装フィルムの市場機会、成長促進要因、産業動向分析、2025年~2034年予測 |

|

出版日: 2025年04月15日

発行: Global Market Insights Inc.

ページ情報: 英文 185 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

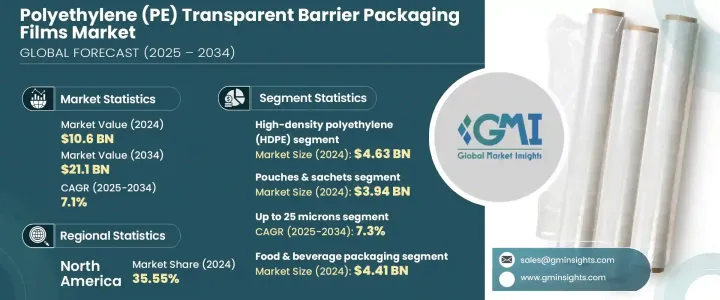

ポリエチレン透明バリア包装フィルムの世界市場は、2024年に106億米ドルと評価され、高性能な包装ソリューションを必要とする便利で耐久性のある包装商品への需要の高まりにより、CAGR 7.1%で成長し、2034年には211億米ドルに達すると予測されています。

持続可能で軽量かつコスト効率の高いパッケージングに対する消費者の嗜好の高まりが、各業界におけるポリエチレン(PE)透明バリアフィルムへの移行を加速させています。食品、化粧品、医薬品の各業界では、賞味期限の延長と製品の完全性がより重視されており、先進パッケージング・ソリューションに対する需要は急速に高まっています。PE透明バリアフィルムは、製品の視認性と柔軟性を維持しながら、湿気、酸素、汚染物質から優れた保護を提供します。

金属やガラスのような従来の素材とは異なり、これらのフィルムは輸送コストの削減、環境フットプリントの削減、リサイクル性の向上といった大きな利点を備えており、将来を見据えたブランドにとって最良の選択肢となっています。さらに、環境にやさしくリサイクル可能な素材の使用を促進する世界の規制の強化により、業界は循環型経済の目標に沿った包装設計の革新を迫られています。持続可能性が企業の重要課題として取り上げられ続ける中、メーカーは高性能でリサイクルしやすい単一素材のソリューションを提供することにますます注力しています。環境問題に対する消費者の意識の高まりも、予測期間を通じて市場の力強い成長軌道を後押しする大きな要因となっています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 106億米ドル |

| 予測金額 | 211億米ドル |

| CAGR | 7.1% |

市場はタイプ別にメタロセンポリエチレン(mPE)、直鎖状低密度ポリエチレン(LLDPE)、低密度ポリエチレン(LDPE)、高密度ポリエチレン(HDPE)に区分されます。2024年の市場規模は46億3,000万米ドルで、HDPEがこのセグメントをリードしています。優れた耐久性と優れたバリア性で知られるHDPEは、特に食品や医薬品の分野で、繊細な製品の包装に好まれる素材です。その化学的・酸素的バリア機能は、食品の安全性と保存安定性を高めるために不可欠です。市場が持続可能性に大きく傾く中、共押出HDPEフィルムの採用動向が勢いを増しており、リサイクル性が向上し、材料の簡素化努力も後押ししています。

厚さに関しては、100ミクロン以上、50~100ミクロン、25~50ミクロン、25ミクロン以下があります。25ミクロンまでのカテゴリーは、2025年から2034年にかけてCAGR 7.3%で成長すると予測されています。これらの極薄フィルムは、その卓越した水分・ガスバリア性により、スナック菓子、焼き菓子、医薬品の包装にますます好まれています。企業は、費用対効果と製品の鮮度を確保しつつ、厳しい環境基準に合わせるため、この厚さ範囲の単一素材フィルムを採用する方向に急速に進んでいます。

ドイツのポリエチレン透明バリア包装フィルム市場は、2034年までにCAGR 32.77%という驚異的な成長率で拡大し、最も急成長している地域市場のひとつになると予測されています。この目覚しい成長の背景には、ドイツ包装法に基づく先進的なリサイクル法があり、選別とリサイクルを簡素化する単一素材ポリエチレンフィルムの普及を後押ししています。持続可能な産業慣行におけるドイツのリーダーシップと強力な規制の後押しが、市場の将来のペースを作っています。

ポリエチレン透明バリア包装フィルムの世界市場における主要企業には、Berry Global Inc.、Jindal Poly Films Ltd.、Sealed Air Corporation、Amcor Plcなどがあります。これらの企業は高度な製造技術に多額の投資を行い、リサイクル可能なフィルムや生分解性フィルムのポートフォリオを拡大し、戦略的パートナーシップを結んで技術革新を推進しています。高性能な単一素材フィルムの開発と、共押出技術による生産プロセスの最適化に重点的に取り組むことで、世界市場での地位を強化する一方、進化する規制需要にも対応しています。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- 業界への影響要因

- 促進要因

- 持続可能な包装への需要の高まり

- 厳しい環境規制

- バリア性とリサイクル性を向上させる技術の進歩

- 食品・飲料、化粧品、医薬品業界での採用増加

- プラスチック汚染に対する意識の高まり

- 業界の潜在的リスク&課題

- 従来のプラスチックに比べて生産コストが高く、拡張性が限られている

- 多層フィルム構造によるリサイクルの複雑さ

- 促進要因

- 成長可能性分析

- 規制情勢

- テクノロジーの情勢

- 将来の市場動向

- ギャップ分析

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 主要市場企業の競合分析

- 競合ポジショニングマトリックス

- 戦略ダッシュボード

第5章 市場推計・予測:タイプ別、2021-2034

- 主要動向

- 低密度ポリエチレン(LDPE)

- 高密度ポリエチレン(HDPE)

- 直鎖状低密度ポリエチレン(LLDPE)

- メタロセンポリエチレン(mPE)

第6章 市場推計・予測:包装形態別、2021-2034

- 主要動向

- ポーチとサシェ

- ラップ&蓋フィルム

- バッグ&ライナー

- シュリンク&ストレッチフィルム

- クラムシェルとブリスターパック

- 真空およびガス置換包装(MAP)フィルム

第7章 市場推計・予測:厚さ別、2021-2034

- 最大25ミクロン

- 25~50ミクロン

- 50~100ミクロン

- 100ミクロン以上

第8章 市場推計・予測:最終用途産業別、2021-2034

- 主要動向

- 食品および飲料の包装

- 医薬品および医療用包装

- パーソナルケアおよび化粧品のパッケージ

- 工業用包装

- 電子機器パッケージ

第9章 市場推計・予測:地域別、2021-2034

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- 英国

- ドイツ

- フランス

- スペイン

- イタリア

- アジア太平洋地域

- 中国

- インド

- 日本

- オーストラリア・ニュージーランド

- 韓国

- ラテンアメリカ

- ブラジル

- メキシコ

- 中東・アフリカ

- アラブ首長国連邦

- サウジアラビア

- 南アフリカ

第10章 企業プロファイル

- Amcor Plc

- Arena Products、Inc.

- Berry Global Inc.

- BIO Packaging Films

- Celplast Metallized Products Ltd.

- Cosmo Films Ltd.

- Dai Nippon Printing Co.、Ltd.

- DuPont Teijin Films USA

- Glenroy、Inc.

- Innovia Films

- Jindal Poly Films Ltd.

- Mondi Plc

- Plastissimo Film Co.

- ProAmpac

- Schur Flexibles Group

- Sealed Air Corporation

- SUDPACK Verpackungen GmbH &Co. KG

- Toray Plastics(America)、Inc.

- UFlex Limited

- Winpak Ltd.

The Global Polyethylene Transparent Barrier Packaging Films Market was valued at USD 10.6 billion in 2024 and is estimated to grow at a CAGR of 7.1% to reach USD 21.1 billion by 2034, driven by the rising demand for convenient, durable packaged goods that require high-performance packaging solutions. Growing consumer preference for sustainable, lightweight, and cost-effective packaging is accelerating the transition toward polyethylene (PE) transparent barrier films across industries. With businesses across food, cosmetics, and pharmaceuticals placing a stronger emphasis on shelf life extension and product integrity, the demand for advanced packaging solutions is rapidly escalating. PE transparent barrier films deliver excellent protection against moisture, oxygen, and contaminants while maintaining product visibility and flexibility.

Unlike traditional materials like metal and glass, these films offer significant advantages such as lower transportation costs, reduced environmental footprint, and better recyclability, making them a top choice for forward-looking brands. In addition, stricter global regulations promoting the use of eco-friendly and recyclable materials are pushing industries to innovate packaging designs in line with circular economy goals. As sustainability continues to dominate corporate agendas, manufacturers are increasingly focused on delivering mono-material solutions that are both high-performing and easily recyclable. The growing awareness among consumers about environmental issues is also a major catalyst, propelling the market's robust growth trajectory through the forecast period.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $10.6 Billion |

| Forecast Value | $21.1 Billion |

| CAGR | 7.1% |

The market is segmented by type into metallocene polyethylene (mPE), linear low-density polyethylene (LLDPE), low-density polyethylene (LDPE), and high-density polyethylene (HDPE). HDPE led the segment in 2024 with a market value of USD 4.63 billion. Known for its excellent durability and superior barrier resistance, HDPE is a preferred material for packaging sensitive products, especially in the food and pharmaceutical sectors. Its chemical and oxygen barrier capabilities make it vital for enhancing food safety and shelf stability. As the market leans heavily toward sustainability, the trend of adopting co-extruded HDPE films is gaining momentum, offering better recyclability and supporting material simplification efforts.

In terms of thickness, the market includes above 100 microns, 50-100 microns, 25-50 microns, and up to 25 microns. The up to 25 microns category is projected to grow at a CAGR of 7.3% from 2025 to 2034. These ultra-thin films are increasingly favored for packaging snacks, baked goods, and pharmaceuticals due to their exceptional moisture and gas barrier properties. Companies are rapidly moving toward adopting mono-material films in this thickness range to align with strict environmental standards while ensuring cost-effectiveness and product freshness.

Germany's Polyethylene Transparent Barrier Packaging Films Market is projected to expand at a staggering CAGR of 32.77% by 2034, emerging as one of the fastest-growing regional markets. This impressive growth is fueled by the country's progressive recycling laws under the German Packaging Act, driving widespread adoption of mono-material polyethylene films that simplify sorting and recycling. Germany's leadership in sustainable industrial practices and strong regulatory push is setting the pace for the market's future.

Leading players in the Global Polyethylene Transparent Barrier Packaging Films Market include Berry Global Inc., Jindal Poly Films Ltd., Sealed Air Corporation, and Amcor Plc. These companies are investing heavily in advanced manufacturing technologies, expanding their portfolios with recyclable and biodegradable films, and forming strategic partnerships to drive innovation. A sharp focus on developing high-performance mono-material films and optimizing production processes through co-extrusion techniques is helping them strengthen global market positions while meeting evolving regulatory demands.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Base estimates and calculations

- 1.3.1 Base year calculation

- 1.3.2 Key trends for market estimation

- 1.4 Forecast model

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.5.2 Data mining sources

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising demand for sustainable packaging

- 3.2.1.2 Stringent environmental regulations

- 3.2.1.3 Technological advancements improving barrier properties and recyclability

- 3.2.1.4 Increasing adoption of food & beverage, cosmetics, and pharmaceutical industries

- 3.2.1.5 Increasing awareness of plastic pollution.

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High production costs & limited scalability compared to traditional plastics

- 3.2.2.2 Recycling complexities due to multilayer film structures

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.5 Technology landscape

- 3.6 Future market trends

- 3.7 Gap analysis

- 3.8 Porter's analysis

- 3.9 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategy dashboard

Chapter 5 Market Estimates and Forecast, By Type, 2021 - 2034 ($ Mn & Kilo Tons)

- 5.1 Key trends

- 5.2 Low-density polyethylene (LDPE)

- 5.3 High-density polyethylene (HDPE)

- 5.4 Linear low-density polyethylene (LLDPE)

- 5.5 Metallocene polyethylene (mPE)

Chapter 6 Market Estimates and Forecast, By Packaging Format, 2021 - 2034 ($ Mn & Kilo Tons)

- 6.1 Key trends

- 6.2 Pouches & sachets

- 6.3 Wraps & lidding films

- 6.4 Bags & liners

- 6.5 Shrink & stretch films

- 6.6 Clamshells & blister packs

- 6.7 Vacuum & modified atmosphere packaging (MAP) films

Chapter 7 Market Estimates and Forecast, By Thickness, 2021 - 2034 ($ Mn & Kilo Tons)

- 7.1 Up to 25 microns

- 7.2 25–50 microns

- 7.3 50–100 microns

- 7.4 Above 100 microns

Chapter 8 Market Estimates and Forecast, By End Use Industry, 2021 - 2034 ($ Mn & Kilo Tons)

- 8.1 Key trends

- 8.2 Food & beverage packaging

- 8.3 Pharmaceutical & medical packaging

- 8.4 Personal care & cosmetics packaging

- 8.5 Industrial packaging

- 8.6 Electronics packaging

Chapter 9 Market Estimates and Forecast, By Region, 2021 - 2034 ($ Mn & Kilo Tons)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 UK

- 9.3.2 Germany

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 ANZ

- 9.4.5 South Korea

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.6 Middle East and Africa

- 9.6.1 UAE

- 9.6.2 Saudi Arabia

- 9.6.3 South Africa

Chapter 10 Company Profiles

- 10.1 Amcor Plc

- 10.2 Arena Products, Inc.

- 10.3 Berry Global Inc.

- 10.4 BIO Packaging Films

- 10.5 Celplast Metallized Products Ltd.

- 10.6 Cosmo Films Ltd.

- 10.7 Dai Nippon Printing Co., Ltd.

- 10.8 DuPont Teijin Films USA

- 10.9 Glenroy, Inc.

- 10.10 Innovia Films

- 10.11 Jindal Poly Films Ltd.

- 10.12 Mondi Plc

- 10.13 Plastissimo Film Co.

- 10.14 ProAmpac

- 10.15 Schur Flexibles Group

- 10.16 Sealed Air Corporation

- 10.17 SUDPACK Verpackungen GmbH & Co. KG

- 10.18 Toray Plastics (America), Inc.

- 10.19 UFlex Limited

- 10.20 Winpak Ltd.