|

市場調査レポート

商品コード

1740826

透明包装の市場機会、成長促進要因、産業動向分析、2025年~2034年予測Transparent Packaging Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| 透明包装の市場機会、成長促進要因、産業動向分析、2025年~2034年予測 |

|

出版日: 2025年04月16日

発行: Global Market Insights Inc.

ページ情報: 英文 180 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

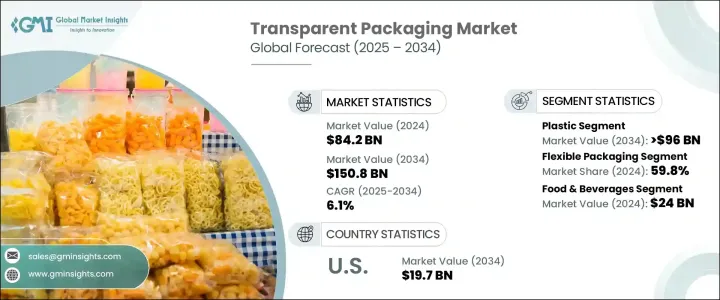

世界の透明包装市場は、2024年には842億米ドルとなり、eコマース分野の急速な拡大や、製品の視認性を高め、消費者の信頼を構築するパッケージに対する需要の高まりを背景に、CAGR 6.1%で成長し、2034年には1,508億米ドルに達すると予測されています。

消費者の嗜好が進化するにつれ、ブランドは製品を保護するだけでなく、買い物客と視覚的につながるパッケージを優先するようになっています。透明包装は、特に食品、飲食品、パーソナルケア、エレクトロニクスなどの分野で、製品の品質、鮮度、真正性を明確に伝えるために不可欠なものとなっています。競争の激しい市場で差別化を図ろうとする企業にとって、透明なパッケージは重要なマーケティング・ツールとなっています。また、持続可能なソリューションへの動向は、市場情勢を再構築しており、メーカーは環境基準に合わせ、環境意識の高まる消費者層に対応するため、リサイクル可能な素材や生分解性素材に焦点を当てています。透明包装のソリューションは、現代の消費者にアピールする耐久性、持続可能性、高級感のある美しさを提供しながら、オンラインとオフラインのショッピング体験のギャップを埋め、オムニチャネル小売戦略において重要な役割を果たしています。

ポリエチレンテレフタレート(PET)、ポリエチレン(PE)、ポリプロピレン(PP)などの透明包装素材は、その優れた透明性、弾力性、リサイクル性により、大きな支持を得ています。オンライン・ショッピングへのシフトにより、保護性を損なうことなく商品を効果的に見せるパッケージへのニーズが高まっています。さらに、持続可能性を重視するあまり、企業は環境に関する義務や消費者の期待に応えるため、生分解性素材やリサイクル可能な素材を使った技術革新に取り組んでいます。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 842億米ドル |

| 予測金額 | 1,508億米ドル |

| CAGR | 6.1% |

最近の貿易政策が透明包装市場にハードルをもたらしています。米国政権が中国やメキシコなどの国からの輸入品に関税をかけたことで、PET、PE、PP樹脂などの主要原材料のコストが上昇しています。生産コストの上昇は、透明包装ソリューションの価格上昇につながっています。これに対応するため、企業はサプライチェーンを多様化し、代替サプライヤーを探し、関税の影響を管理し競争力を維持するために国内生産能力を増強しています。

PET、PE、PP材料を含むプラスチック分野は、プラスチックの軽量性、コスト効率、耐久性に後押しされ、2034年までに960億米ドルを生み出すと予測されています。特にPETとPPは、その卓越した透明性で珍重され、消費者は封を切らずに製品を検査できるため、製品の魅力と信頼性が高まる。リサイクル可能なプラスチックや生分解性プラスチックの技術革新も、プラスチック包装を環境意識の高いバイヤーにとってより持続可能で魅力的な選択肢にしています。

フレキシブル包装は、PE、PP、PET素材の汎用性とコスト効率に牽引され、2024年には59.8%のシェアを占め、市場を独占しました。軽量で弾力性のある軟包装は、医薬品、パーソナルケア、飲食品に適しており、耐タンパー性、再密封性、製品の視認性を高めています。

米国の透明包装市場は2034年までに197億米ドルに達すると予測されており、これはeコマース活動の急増と環境に優しいパッケージングへの需要の高まりが後押ししています。飲食品セクターは依然として最大の貢献者であり、透明で密封可能な包装が消費者の信頼を高め、オーガニック食品や調理済み食品の消費拡大を支えています。

世界の透明包装業界の主要プレーヤーには、Futamura Group、NatureWorks LLC、Amcor plc、Biome Bioplastics、Bio Futura、Corbion、Genpak、IIC AG、FKuR、ITC Packaging、Novamont S.p.A.、Sealed Air Corporation、J. Landworth Company、Stora Enso、TIPA LTD、Tetra Pak International S.A.、Walki Group Oy、Xiamen Changsu Industrial Co.各社は、サプライチェーンの多様化、自動化の促進、貿易政策のシフトの注視、データ主導型戦略の活用、持続可能な素材や革新的なパッケージデザインといった付加価値の提供に注力することで、関税の課題を乗り切り、競争力を維持しています。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- トランプ政権の関税分析

- 貿易への影響

- 貿易量の混乱

- 報復措置

- 業界への影響

- 供給側の影響(原材料)

- 主要原材料の価格変動

- サプライチェーンの再構築

- 生産コストへの影響

- 需要側の影響(販売価格)

- 最終市場への価格伝達

- 市場シェアの動向

- 消費者の反応パターン

- 供給側の影響(原材料)

- 影響を受ける主要企業

- 戦略的な業界対応

- サプライチェーンの再構成

- 価格設定と製品戦略

- 政策関与

- 展望と今後の検討事項

- 貿易への影響

- 業界への影響要因

- 促進要因

- eコマース業界の成長

- 持続可能な包装の人気の高まり

- 包装材料の進歩

- 医薬品部門の拡大

- プレミアムおよび高級パッケージの需要の急増

- 業界の潜在的リスク&課題

- 環境問題とプラスチック廃棄物に対する規制圧力

- 高い生産コストと材料の制限

- 促進要因

- 成長可能性分析

- 規制情勢

- テクノロジーの情勢

- 将来の市場動向

- ギャップ分析

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 主要市場企業の競合分析

- 競合ポジショニングマトリックス

- 戦略ダッシュボード

第5章 市場推計・予測:材料別、2021-2034

- 主要動向

- プラスチック

- PET(ポリエチレンテレフタレート)

- PP(ポリプロピレン)

- PVC(ポリ塩化ビニル)

- バイオプラスチック(PLA、PHA)

- リサイクルプラスチック

- ガラス

- ハイブリッド

第6章 市場推計・予測:包装形態別、2021-2034

- 主要動向

- 硬質包装

- ボトルと瓶

- トレイと容器

- クラムシェル

- フレキシブル包装

- ポーチとサシェ

- バッグ&ラップ

- フィルム

- その他

第7章 市場推計・予測:最終用途産業別、2021-2034

- 主要動向

- 食品と飲料

- 食べ物

- 生鮮食品

- 加工食品

- 乳製品

- ベーカリー&菓子類

- 飲み物

- 水とソフトドリンク

- アルコール飲料

- ジュースと乳製品飲料

- 食べ物

- 消費財

- エレクトロニクス

- 家庭用品

- 医薬品

- 医薬品

- 医療機器

- パーソナルケア&化粧品

- スキンケア

- ヘアケア

- メイクアップ

- その他

第8章 市場推計・予測:地域別、2021-2034

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- スペイン

- イタリア

- アジア太平洋地域

- 中国

- インド

- 日本

- オーストラリア

- 韓国

- ラテンアメリカ

- ブラジル

- メキシコ

- 中東・アフリカ

- サウジアラビア

- 南アフリカ

- アラブ首長国連邦

第9章 企業プロファイル

- Amcor plc

- Bio Futura

- Biome Bioplastics

- Corbion

- FKuR

- Futamura Group

- Genpak

- IIC AG

- ITC Packaging

- J. Landworth Company

- NatureWorks LLC

- Novamont S.p.A.

- Sealed Air Corporation

- Stora Enso

- Tetra Pak International S.A.

- TIPA LTD

- Walki Group Oy

- Xiamen Changsu Industrial Co.、Ltd.

The Global Transparent Packaging Market was valued at USD 84.2 billion in 2024 and is estimated to grow at a CAGR of 6.1% to reach USD 150.8 billion by 2034, driven by the rapid expansion of the e-commerce sector and the rising demand for packaging that enhances product visibility and builds consumer trust. As consumer preferences evolve, brands are increasingly prioritizing packaging that not only protects products but also visually connects with shoppers. Transparent packaging has become essential for delivering a clear view of product quality, freshness, and authenticity, especially across sectors like food, beverages, personal care, and electronics. With companies striving to differentiate themselves in a highly competitive marketplace, clear packaging has emerged as a vital marketing tool. The trend toward sustainable solutions is also reshaping the market landscape, with manufacturers focusing on recyclable and biodegradable materials to align with environmental standards and meet the growing eco-conscious consumer base. Transparent packaging solutions are playing a critical role in omnichannel retail strategies, bridging the gap between online and offline shopping experiences while offering durability, sustainability, and premium aesthetics that appeal to modern consumers.

Transparent packaging materials, including polyethylene terephthalate (PET), polyethylene (PE), and polypropylene (PP), are gaining significant traction for their excellent clarity, resilience, and recyclability. The shift toward online shopping has intensified the need for packaging that showcases products effectively without compromising protection. In addition, a strong emphasis on sustainability is pushing companies to innovate with biodegradable and recyclable materials to satisfy environmental mandates and consumer expectations.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $84.2 Billion |

| Forecast Value | $150.8 Billion |

| CAGR | 6.1% |

Recent trade policies have created hurdles for the transparent packaging market. The U.S. administration's tariffs on imports from countries like China and Mexico have pushed up the cost of key raw materials such as PET, PE, and PP resins. Rising production costs are leading to higher prices for transparent packaging solutions. In response, companies are diversifying supply chains, seeking alternative suppliers, and ramping up domestic production capabilities to manage the tariff impact and maintain competitiveness.

The plastics segment, which includes PET, PE, and PP materials, is forecasted to generate USD 96 billion by 2034, fueled by plastics' lightweight, cost-efficiency, and durability. PET and PP, in particular, are prized for their exceptional transparency, allowing consumers to inspect products without breaking seals, thus enhancing product appeal and trust. Innovations in recyclable and biodegradable plastics are also making plastic packaging a more sustainable and attractive choice for eco-conscious buyers.

Flexible packaging dominated the market, holding a 59.8% share in 2024, driven by the versatility and cost-efficiency of PE, PP, and PET materials. Lightweight and resilient, flexible packaging is well-suited for pharmaceuticals, personal care, and food and beverage products, offering tamper resistance, resealability, and enhanced product visibility.

The U.S. Transparent Packaging Market is projected to reach USD 19.7 billion by 2034, fueled by surging e-commerce activities and the growing demand for eco-friendly packaging. The food and beverage sector remains the top contributor, with transparent, sealable packaging boosting consumer confidence and supporting the rising consumption of organic and ready-to-eat foods.

Key players in the Global Transparent Packaging Industry include Futamura Group, NatureWorks LLC, Amcor plc, Biome Bioplastics, Bio Futura, Corbion, Genpak, IIC AG, FKuR, ITC Packaging, Novamont S.p.A., Sealed Air Corporation, J. Landworth Company, Stora Enso, TIPA LTD, Tetra Pak International S.A., Walki Group Oy, and Xiamen Changsu Industrial Co., Ltd. Companies are navigating tariff challenges by diversifying supply chains, boosting automation, closely monitoring trade policy shifts, leveraging data-driven strategies, and focusing on value-added offerings such as sustainable materials and innovative packaging designs to maintain a competitive edge.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Base estimates and calculations

- 1.3.1 Base year calculation

- 1.3.2 Key trends for market estimation

- 1.4 Forecast model

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.5.2 Data mining sources

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Trump administration tariffs analysis

- 3.2.1 Impact on trade

- 3.2.1.1 Trade volume disruptions

- 3.2.1.2 Retaliatory measures

- 3.2.2 Impact on the industry

- 3.2.2.1 Supply-side impact (Raw Materials)

- 3.2.2.1.1 Price volatility in key materials

- 3.2.2.1.2 Supply chain restructuring

- 3.2.2.1.3 Production cost implications

- 3.2.2.2 Demand-side impact (selling price)

- 3.2.2.2.1 Price transmission to end markets

- 3.2.2.2.2 Market share dynamics

- 3.2.2.2.3 Consumer response patterns

- 3.2.2.1 Supply-side impact (Raw Materials)

- 3.2.3 Key companies impacted

- 3.2.4 Strategic industry responses

- 3.2.4.1.1 Supply chain reconfiguration

- 3.2.4.1.2 Pricing and product strategies

- 3.2.4.1.3 Policy engagement

- 3.2.5 Outlook and future considerations

- 3.2.1 Impact on trade

- 3.3 Industry impact forces

- 3.3.1 Growth drivers

- 3.3.1.1 Growth in e-commerce industry

- 3.3.1.2 Rising popularity of sustainable packaging

- 3.3.1.3 Advancements in packaging materials

- 3.3.1.4 Expansion of the pharmaceutical sector

- 3.3.1.5 Surge in premium & luxury packaging demand

- 3.3.2 Industry pitfalls and challenges

- 3.3.2.1 Environmental concerns & regulatory pressure on plastic waste

- 3.3.2.2 High production costs & material limitations

- 3.3.1 Growth drivers

- 3.4 Growth potential analysis

- 3.5 Regulatory landscape

- 3.6 Technology landscape

- 3.7 Future market trends

- 3.8 Gap analysis

- 3.9 Porter's analysis

- 3.10 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategy dashboard

Chapter 5 Market Estimates and Forecast, By Material, 2021 - 2034 ($ Mn & Million Tons)

- 5.1 Key trends

- 5.2 Plastics

- 5.2.1 PET (polyethylene terephthalate)

- 5.2.2 PP (polypropylene)

- 5.2.3 PVC (polyvinyl chloride)

- 5.2.4 Bioplastics (PLA, PHA)

- 5.2.5 Recycled plastics

- 5.3 Glass

- 5.4 Hybrid

Chapter 6 Market Estimates and Forecast, By Packaging Type, 2021 - 2034 ($ Mn & Million Tons)

- 6.1 Key trends

- 6.2 Rigid packaging

- 6.2.1 Bottles & jars

- 6.2.2 Trays & containers

- 6.2.3 Clamshells

- 6.3 Flexible packaging

- 6.3.1 Pouches & sachets

- 6.3.2 Bags & wraps

- 6.3.3 Films

- 6.3.4 Others

Chapter 7 Market Estimates and Forecast, By End Use Industry, 2021 - 2034 ($ Mn & Million Tons)

- 7.1 Key trends

- 7.2 Food and beverage

- 7.2.1 Food

- 7.2.1.1 Fresh food

- 7.2.1.2 Processed food

- 7.2.1.3 Dairy products

- 7.2.1.4 Bakery & confectionery

- 7.2.2 Beverage

- 7.2.2.1 Water & soft drinks

- 7.2.2.2 Alcoholic beverages

- 7.2.2.3 Juices & dairy drinks

- 7.2.1 Food

- 7.3 Consumer goods

- 7.3.1 Electronics

- 7.3.2 Household products

- 7.4 Pharmaceuticals

- 7.4.1 Pharmaceuticals

- 7.4.2 Medical devices

- 7.5 Personal care & cosmetics

- 7.5.1 Skincare

- 7.5.2 Haircare

- 7.5.3 Makeup

- 7.6 Others

Chapter 8 Market Estimates and Forecast, By Region, 2021 - 2034 ($ Mn & Million Tons)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.6 Middle East and Africa

- 8.6.1 Saudi Arabia

- 8.6.2 South Africa

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 Amcor plc

- 9.2 Bio Futura

- 9.3 Biome Bioplastics

- 9.4 Corbion

- 9.5 FKuR

- 9.6 Futamura Group

- 9.7 Genpak

- 9.8 IIC AG

- 9.9 ITC Packaging

- 9.10 J. Landworth Company

- 9.11 NatureWorks LLC

- 9.12 Novamont S.p.A.

- 9.13 Sealed Air Corporation

- 9.14 Stora Enso

- 9.15 Tetra Pak International S.A.

- 9.16 TIPA LTD

- 9.17 Walki Group Oy

- 9.18 Xiamen Changsu Industrial Co., Ltd.