|

市場調査レポート

商品コード

1708222

包装用ハイバリアフィルム市場の機会、成長促進要因、産業動向分析、2025年~2034年の予測High Barrier Packaging Films Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| 包装用ハイバリアフィルム市場の機会、成長促進要因、産業動向分析、2025年~2034年の予測 |

|

出版日: 2025年03月26日

発行: Global Market Insights Inc.

ページ情報: 英文 185 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

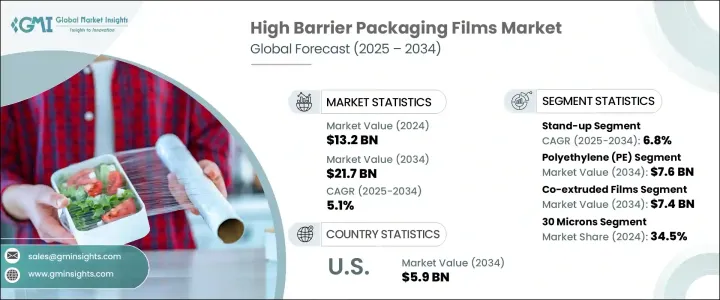

包装用ハイバリアフィルムの世界市場は2024年に132億米ドルを創出し、医薬品分野の急成長、eコマースの拡大、オンライン食品宅配サービスの人気の高まりに牽引され、2025年から2034年にかけてCAGR 5.1%で成長すると予想されています。

製薬会社が革新と拡大を続ける中、繊細な製品を保護する先進パッケージング・ソリューションの必要性がより重要になっています。包装用ハイバリアフィルムは、医薬品の保存期間を延ばしながら、湿気や酸素、その他の汚染物質に対する最適な保護を保証します。さらに、急成長するeコマース業界とオンライン食品宅配サービスの急増は、輸送中や保管中に製品の完全性を維持する高性能パッケージングへの需要をさらに煽っています。安全で衛生的、持続可能な包装に対する消費者の期待の高まりも市場成長に寄与しています。さらに、環境に対する意識の高まりが、循環型経済の目標に沿うため、リサイクル可能、生分解性、バリア性の高い素材への投資をメーカーに促しています。

この市場には、スタンドアップパウチ、フラットパウチ、バッグとサック、ブリスターとクラムシェル、ラップとリディングフィルム、サシェとスティックパックなど、さまざまな包装形態が含まれます。中でもスタンドアップパウチは2034年までのCAGRが6.8%と最も高い成長が予測されています。この成長は、特にスナック菓子や調理済み食品など、軽量でバリア性の高い軟包装に対する消費者の嗜好の高まりによるところが大きいです。製造業者は利便性と持続可能性に対する消費者の要求に応えるため、高品質のリサイクル可能な素材を採用し、高度なリシーラブル機能を統合するようになってきています。プラスチック廃棄物に対する環境への懸念が強まる中、業界各社は製品の安全性と鮮度を維持しながら環境への影響を減らすパッケージングソリューションを開発しています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 132億米ドル |

| 予測金額 | 217億米ドル |

| CAGR | 5.1% |

包装用ハイバリアフィルム市場は、材料別にポリエチレン(PE)、ポリプロピレン(PP)、ポリエチレンテレフタレート(PET)、ポリ塩化ビニリデン(PVDC)、エチレンビニルアルコール(EVOH)、ポリアミド(ナイロン)、その他に区分されます。ポリエチレン(PE)がこのセグメントを支配し、2034年までに76億米ドルに達すると予想されます。規制要件や顧客の期待に応えるため、企業が持続可能な慣行を重視しているため、リサイクル可能なバイオベースのPE材料への顕著なシフトが進行中です。各メーカーは、優れた酸素バリア性と水分バリア性を備えた革新的なモノマテリアルPEフィルムを開発し、持続可能性を促進しながら製品保護を実現しています。このようなPE材料の先進パッケージングは、このセグメントの成長を促進し、環境に配慮したパッケージングに対する需要の高まりに対応しています。

北米の包装用ハイバリアフィルム市場は2024年に38.4%のシェアを占め、コンビニエンス食品と調理済み食品の需要増に後押しされています。消費者の嗜好が賞味期限と鮮度を長持ちさせる包装食品にシフトするにつれて、ハイバリア包装ソリューションの需要は伸び続けています。同地域では、包装済み冷凍食品、スナック菓子、食品トレーの消費が顕著に増加しており、これが高バリア性包装フィルムの採用をさらに後押ししています。さらに、この地域は技術革新に重点を置いており、持続可能で環境に優しいパッケージング・ソリューションへのニーズの高まりと相まって、北米の市場支配的地位を維持すると予想されます。

目次

第1章 調査手法と調査範囲

第2章 エグゼクティブサマリー

第3章 業界洞察

- エコシステム分析

- 業界への影響要因

- 促進要因

- eコマースとオンライン食品デリバリーの成長

- 製薬産業の拡大

- 真空包装とガス置換包装(MAP)の需要増加

- 乳製品・食肉包装業界の拡大

- 急速な都市化とライフスタイルの変化が包装商品を牽引

- 業界の潜在的リスク&課題

- 高度バリアフィルムの高い製造コスト

- 原料供給に影響を及ぼす石油化学製品価格の変動

- 促進要因

- 成長可能性分析

- 規制状況

- 技術情勢

- 今後の市場動向

- ギャップ分析

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業シェア分析

- 主要市場プレーヤーの競合分析

- 競合のポジショニングマトリックス

- 戦略ダッシュボード

第5章 市場推計・予測:材料タイプ別、2021年~2034年

- 主要動向

- ポリエチレン(PE)

- ポリプロピレン(PP)

- ポリエチレンテレフタレート(PET)

- ポリ塩化ビニリデン(PVDC)

- エチレンビニルアルコール(EVOH)

- ポリアミド(ナイロン)

- その他

第6章 市場推計・予測:包装形態別、2021年~2034年

- 主要動向

- スタンディングパウチ

- フラットパウチ

- バッグ&サック

- ブリスター&クラムシェル

- ラップ・蓋フィルム

- 小袋・スティックパック

第7章 市場推計・予測:技術別、2021年~2034年

- 主要動向

- 共押出フィルム

- メタライズドフィルム

- スパッタリングフィルム

- 原子層蒸着(ALD)フィルム

- ラミネートフィルム

第8章 市場推計・予測:膜厚別、2021年~2034年

- 主要動向

- 30ミクロン未満

- 30~50ミクロン

- 50~70ミクロン

- 70ミクロン以上

第9章 市場推計・予測:用途タイプ別、2021年~2034年

- 主要動向

- 生鮮食品包装

- 加工食品包装

- 飲料包装

- ヘルスケア製品

- パーソナルケアと化粧品

- 工業用部品

- 農産物

第10章 市場推計・予測:最終用途産業別、2021年~2034年

- 主要動向

- 飲食品

- 医薬品・医療

- 電子・半導体

- 工業用

- その他

第11章 市場推計・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- スペイン

- イタリア

- オランダ

- アジア太平洋

- 中国

- インド

- 日本

- オーストラリア

- 韓国

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- サウジアラビア

- 南アフリカ

- アラブ首長国連邦

第12章 企業プロファイル

- 3M

- ACG

- Amcor

- Bemis Manufacturing

- Berry Global

- Celplast Metallized Products

- Cosmo Films

- Innovia Films

- Jindal Poly Films

- Klockner Pentaplast

- Mitsubishi Chemical Advanced Materials

- Mondi

- Oike

- Perlen Packaging

- Sealed Air

- Sigma Plastics Group

- Sonoco Products

- Toppan

- Toray Plastics

- Uflex

- Winpak

The Global High Barrier Packaging Films Market generated USD 13.2 billion in 2024 and is expected to grow at a CAGR of 5.1% from 2025 to 2034, driven by the rapid growth of the pharmaceutical sector, the expansion of e-commerce, and the increasing popularity of online food delivery services. As pharmaceutical companies continue to innovate and expand, the need for advanced packaging solutions that protect sensitive products becomes more critical. High barrier packaging films ensure optimal protection against moisture, oxygen, and other contaminants while extending the shelf life of pharmaceuticals. Moreover, the booming e-commerce industry and the surge in online food delivery services have further fueled the demand for high-performance packaging that maintains product integrity during shipping and storage. Rising consumer expectations for secure, hygienic, and sustainable packaging have also contributed to market growth. Additionally, increasing environmental awareness is driving manufacturers to invest in recyclable, biodegradable, and high-barrier materials to align with circular economy goals.

The market encompasses a variety of packaging formats, including stand-up pouches, flat pouches, bags and sacks, blisters and clamshells, wraps and lidding films, and sachets and stick packs. Among these, stand-up pouches are projected to experience the highest growth, with a CAGR of 6.8% through 2034. This growth is largely attributed to the rising consumer preference for lightweight, high-barrier flexible packaging, particularly for snacks and ready-to-eat meals. Manufacturers are increasingly adopting high-quality recyclable materials and integrating advanced resealable features to meet consumer demands for convenience and sustainability. As environmental concerns about plastic waste intensify, industry players are developing packaging solutions that reduce environmental impact while maintaining product safety and freshness.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $13.2 Billion |

| Forecast Value | $21.7 Billion |

| CAGR | 5.1% |

In terms of material type, the high barrier packaging films market is segmented into polyethylene (PE), polypropylene (PP), polyethylene terephthalate (PET), polyvinylidene chloride (PVDC), ethylene vinyl alcohol (EVOH), polyamide (nylon), and others. Polyethylene (PE) is expected to dominate the segment, reaching USD 7.6 billion by 2034. A notable shift is underway towards recyclable and bio-based PE materials as companies emphasize sustainable practices to meet regulatory requirements and customer expectations. Manufacturers are developing innovative mono-material PE films that offer superior oxygen and moisture barriers, ensuring product protection while promoting sustainability. These advancements in PE materials are driving the growth of this segment and catering to the rising demand for environmentally responsible packaging.

North America High Barrier Packaging Films Market held a 38.4% share in 2024, propelled by increasing demand for convenience foods and ready-to-eat meals. As consumer preferences shift towards packaged foods that provide extended shelf life and freshness, the demand for high-barrier packaging solutions continues to grow. The region is witnessing a notable rise in the consumption of prepackaged frozen meals, snacks, and food trays, which further boosts the adoption of high barrier packaging films. Additionally, the region's strong emphasis on innovation, combined with the growing need for sustainable and eco-friendly packaging solutions, is expected to maintain North America's dominant position in the market.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Base estimates and calculations

- 1.3.1 Base year calculation

- 1.3.2 Key trends for market estimation

- 1.4 Forecast model

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.5.2 Data mining sources

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Growth in e-commerce and online food delivery

- 3.2.1.2 Expansion of pharmaceutical industry

- 3.2.1.3 Rising demand for vacuum and modified atmosphere packaging (MAP)

- 3.2.1.4 Expansion of the dairy and meat packaging industry

- 3.2.1.5 Rapid urbanization and changing lifestyles driving packaged goods

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High production costs of advanced barrier films

- 3.2.2.2 Volatility in petrochemical prices affecting raw material supply

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.5 Technology landscape

- 3.6 Future market trends

- 3.7 Gap analysis

- 3.8 Porter's analysis

- 3.9 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategy dashboard

Chapter 5 Market Estimates & Forecast, By Material Type, 2021 - 2034 (USD Billion & Kilo Tons)

- 5.1 Key trends

- 5.2 Polyethylene (PE)

- 5.3 Polypropylene (PP)

- 5.4 Polyethylene Terephthalate (PET)

- 5.5 Polyvinylidene Chloride (PVDC)

- 5.6 Ethylene Vinyl Alcohol (EVOH)

- 5.7 Polyamide (Nylon)

- 5.8 Others

Chapter 6 Market Estimates & Forecast, By Packaging Format, 2021 - 2034 (USD Billion & Kilo Tons)

- 6.1 Key trends

- 6.2 Stand-up pouches

- 6.3 Flat pouches

- 6.4 Bags & sacks

- 6.5 Blisters & clamshells

- 6.6 Wraps & lidding films

- 6.7 Sachets & stick packs

Chapter 7 Market Estimates & Forecast, By Technology, 2021 - 2034 (USD Billion & Kilo Tons)

- 7.1 Key trends

- 7.2 Co-extruded films

- 7.3 Metallized films

- 7.4 Sputtered films

- 7.5 Atomic Layer Deposition (ALD) Films

- 7.6 Laminated films

Chapter 8 Market Estimates & Forecast, By Film Thickness, 2021 - 2034 (USD Billion & Kilo Tons)

- 8.1 Key trends

- 8.2 Up to 30 microns

- 8.3 30-50 microns

- 8.4 50-70 microns

- 8.5 Above 70 microns

Chapter 9 Market Estimates & Forecast, By Application Type, 2021 - 2034 (USD Billion & Kilo Tons)

- 9.1 Key trends

- 9.2 Fresh food packaging

- 9.3 Processed food packaging

- 9.4 Beverage packaging

- 9.5 Healthcare products

- 9.6 Personal care & cosmetics

- 9.7 Industrial components

- 9.8 Agricultural products

Chapter 10 Market Estimates & Forecast, By End Use Industry, 2021 - 2034 (USD Billion & Kilo Tons)

- 10.1 Key trends

- 10.2 Food & beverages

- 10.3 Pharmaceuticals & medical

- 10.4 Electronics & semiconductor

- 10.5 Industrial

- 10.6 Others

Chapter 11 Market Estimates and Forecast, By Region, 2021 - 2034 (USD Billion & Kilo Tons)

- 11.1 Key trends

- 11.2 North America

- 11.2.1 U.S.

- 11.2.2 Canada

- 11.3 Europe

- 11.3.1 Germany

- 11.3.2 UK

- 11.3.3 France

- 11.3.4 Spain

- 11.3.5 Italy

- 11.3.6 Netherlands

- 11.4 Asia Pacific

- 11.4.1 China

- 11.4.2 India

- 11.4.3 Japan

- 11.4.4 Australia

- 11.4.5 South Korea

- 11.5 Latin America

- 11.5.1 Brazil

- 11.5.2 Mexico

- 11.5.3 Argentina

- 11.6 Middle East and Africa

- 11.6.1 Saudi Arabia

- 11.6.2 South Africa

- 11.6.3 UAE

Chapter 12 Company Profiles

- 12.1 3M

- 12.2 ACG

- 12.3 Amcor

- 12.4 Bemis Manufacturing

- 12.5 Berry Global

- 12.6 Celplast Metallized Products

- 12.7 Cosmo Films

- 12.8 Innovia Films

- 12.9 Jindal Poly Films

- 12.10 Klockner Pentaplast

- 12.11 Mitsubishi Chemical Advanced Materials

- 12.12 Mondi

- 12.13 Oike

- 12.14 Perlen Packaging

- 12.15 Sealed Air

- 12.16 Sigma Plastics Group

- 12.17 Sonoco Products

- 12.18 Toppan

- 12.19 Toray Plastics

- 12.20 Uflex

- 12.21 Winpak