eVTOL航空機の市場機会と成長促進要因、産業動向分析、2025~2034年予測

eVTOL Aircraft Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034- 発行日

- ページ情報

- 英文 189 Pages

- 納期

- 2~3営業日

- 商品コード

- 1740913

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

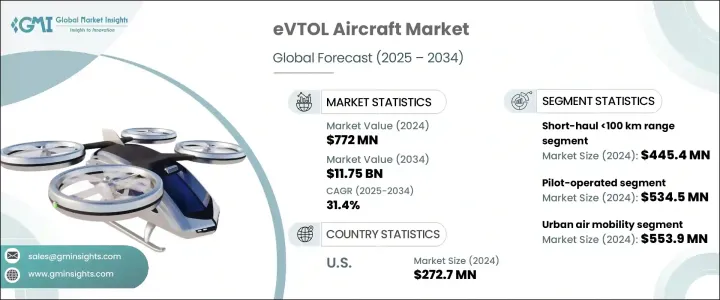

eVTOL航空機の世界市場規模は、2024年に7億7,200万米ドルとなり、CAGR 31.4%で成長し、2034年には117億5,000万米ドルに達すると予測されています。

都市化の急速な進展が道路の混雑を促進し、従来の輸送手段の効率を低下させています。このシフトは、代替モビリティ・オプションへの大きな関心を促しており、eVTOLは短時間で効率的なポイント・ツー・ポイント移動の有力なソリューションとして台頭しています。政府や都市計画担当者は、近代的なインフラ整備の一環としてこれらの航空機を積極的に奨励し、官民パートナーシップを活用して導入を支援しています。また、最適化された都市交通システムが全体的な経済パフォーマンスに貢献するとの認識も高まっています。一方、持続可能性を求める世界の動きは、電動モビリティへの移行を加速させ、今日の環境意識の高い市場におけるeVTOL技術の関連性をさらに高めています。

しかし、ある課題が市場の成長軌道を弱めています。鉄鋼、アルミニウム、航空宇宙部品などの主要輸入素材に課された関税は生産コストを押し上げ、特に国際的なサプライチェーンに依存しているメーカーに影響を及ぼしています。こうしたコスト上昇は、特に価格に敏感な市場において、競争力のある価格設定を行うことを困難にしています。生産コストの上昇は消費者にも転嫁され、小売価格の上昇を引き起こしています。さらに、サプライチェーンの中断が最終納品を遅らせ、買い手に不確実性をもたらし、普及率を鈍らせています。このようなハードルにもかかわらず、海外との競合が減少したことで、地元メーカーには成長の余地が生まれ、優位性が見られるようになりました。長期的には、より多くの企業が国内調達に目を向け、サプライチェーンを再構築することで、世界な混乱の影響を受けにくくなり、業界の再編成が進むと予想されます。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 7億7,200万米ドル |

| 予測金額 | 117億5,000万米ドル |

| CAGR | 31.4% |

eVTOLは、地上輸送の非効率性に対する現実的な回答として、ますます注目されています。道路交通を迂回し、迅速な直行ルートを可能にするeVTOLの能力は、特に都市部の通勤者にとって魅力的な価値提案となります。これらの航空機は垂直に離着陸するように設計されているため、スペースが限られた都市環境には理想的です。各国政府も、都市のモビリティを変革する可能性を認め、長期的な交通計画に組み込もうとしています。クリーンな輸送が国内および国際的な優先事項となるにつれ、電動航空機は規制の後押しと民間投資の両面から支持を集めています。

バッテリー技術と電気推進システムの革新は、eVTOLをより商業的に実行可能なものにする上で極めて重要な役割を果たしています。リチウムイオンバッテリーや新興の固体バッテリーの進歩は、飛行距離を延ばし、安全性を高め、ペイロード容量を増大させています。同時に、新素材と効率的な推進設計により、全体的な運用コストが低下しています。こうした改善により、航空宇宙や自動車分野の大手企業は、都市部での航空モビリティに長期的な可能性を見いだし、投資を呼び寄せています。開発者はまた、持続可能性の目標を達成しながら航空機の性能を向上させるため、軽量複合材を使用したり、エネルギー効率の高いモーター技術を模索したりしています。

航続距離別では、短距離(100kmまで)セグメントが2024年に4億4,540万米ドルを占める。このカテゴリーは、特に短時間で頻繁なフライトを必要とする使用事例において、都市内および地域の空の旅に最も実用的なソリューションとして勢いを増しています。これらの航空機は、エアタクシー、医療輸送、物流などの用途に適しています。バッテリーの改良は、積載量を増やしながら飛行時間を延ばすのに役立っています。政府や民間企業は、離着陸ゾーンのような支援インフラに投資しているが、騒音、規制、社会的信用に関する課題にはまだ対処する必要があります。

自律性別に見ると、パイロット操縦のeVTOLが2024年の評価額5億3,450万米ドルで市場をリードしています。これらのモデルは、社会的信用が高く、規制当局の承認がスムーズなため、商業展開の初期段階では好まれます。訓練されたパイロットが必要なため運用コストは増加するが、安全性と制御性も確保できます。各社は、オペレーターをサポートし作業負荷を軽減するため、ユーザーフレンドリーなインターフェースと半自動コックピットシステムを優先しています。これらの航空機は、完全な自律性への足がかりとなり、最終的にはより高度なシステムをサポートする信頼性と運航データの構築に役立ちます。

地域別需要では、米国が2024年の評価額2億7,270万米ドルで市場を独占しました。同国は、技術革新を受け入れる文化に支えられ、レガシーな航空宇宙企業と機敏な新興企業による強力なエコシステムを提供しています。バッテリーと自動化技術に重点を置いた調査努力が市場を前進させています。航空交通管制や国民感情といった統合の課題が残る一方で、モビリティ企業との提携やインフラ投資を通じて、eVTOLサービスの商業化に向けた国のコミットメントは明白です。

メーカー各社は、エネルギー効率の高い設計への投資、航空機騒音の低減、自動化の統合など、競争力を維持するための戦略的措置を講じています。航空交通管理や予知保全にAIを活用し、運航を合理化しているところもあります。貨物、医療輸送、プレミアム航空旅行といったニッチ分野向けのカスタマイズは、重要な動向になりつつあります。同時に、合併、提携、規制当局との協力は、企業が事業を拡大し、認証プロセスをナビゲートするのに役立っています。デジタルツインやロボット工学のような新しい技術も、生産ライン全体のコスト削減と安全性の向上に役立っています。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- トランプ政権の関税分析

- 貿易への影響

- 貿易量の混乱

- 報復措置

- 業界への影響

- 供給側の影響

- 価格変動

- サプライチェーンの再構築

- 生産コストへの影響

- 需要側の影響

- 最終市場への価格伝達

- 市場シェアの動向

- 消費者の反応パターン

- 供給側の影響

- 影響を受ける主要企業

- 戦略的な業界対応

- サプライチェーンの再構成

- 価格設定と製品戦略

- 政策関与

- 展望と今後の検討事項

- 貿易への影響

- 業界への影響要因

- 促進要因

- 都市の混雑と効率的な移動の必要性

- バッテリーと電気推進技術の進歩

- 環境の持続可能性と排出削減目標

- 増加する投資と戦略的パートナーシップ

- 業界の潜在的リスク&課題

- 高い開発コスト

- 規制当局の承認の遅延

- 促進要因

- 成長可能性分析

- 規制情勢

- テクノロジーの情勢

- 将来の市場動向

- ギャップ分析

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 主要市場企業の競合分析

- 競合ポジショニングマトリックス

- 戦略ダッシュボード

第5章 市場推計・予測:範囲別、2021-2034

- 主要動向

- 短距離100 km未満

- 中距離100~300 km

- 長距離300 km以上

第6章 市場推計・予測:自立レベル別、2021-2034

- 主要動向

- パイロット操作

- 遠隔操縦

- 完全自律型

第7章 市場推計・予測:用途別、2021-2034

- 主要動向

- 都市型航空モビリティ

- 救急ヘリコプター

- 観光とレジャー

- その他

第8章 市場推計・予測:地域別、2021 –2034

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- スペイン

- イタリア

- オランダ

- アジア太平洋地域

- 中国

- インド

- 日本

- オーストラリア

- 韓国

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- サウジアラビア

- 南アフリカ

- アラブ首長国連邦

第9章 企業プロファイル

- Joby Aviation

- Archer Aviation Inc.

- EHang

- Volocopter

- Lilium

- BETA Technologies

- Vertical Aerospace

- Wisk Aero

- Supernal、LLC

- Eve Air Mobility

- Autoflight

- Overair、Inc.

- AeroMobil

- SkyDrive Inc.

- Jaunt Air Mobility LLC.

- Urban Aeronautics

- Bell Textron Inc.

- DORONI AEROSPACE INC. ALL

- Guangdong Huitian Aerospace Technology Co.、Ltd.

目次

The Global eVTOL Aircraft Market was valued at USD 772 million in 2024 and is estimated to grow at a CAGR of 31.4% to reach USD 11.75 billion by 2034. The rapid pace of urbanization is driving up road congestion, making traditional transport modes less efficient. This shift is prompting significant interest in alternative mobility options, with eVTOLs emerging as a leading solution for short, efficient, point-to-point travel. Governments and city planners are actively encouraging these aircraft as part of modern infrastructure development, leveraging public-private partnerships to support implementation. There's also growing acknowledgment that an optimized urban transport system can contribute to overall economic performance. Meanwhile, the global push for sustainability is accelerating the transition toward electric-powered mobility, further boosting the relevance of eVTOL technology in today's eco-conscious markets.

However, certain challenges have tempered the market's growth trajectory. Tariffs imposed on key imported materials such as steel, aluminum, and aerospace components have driven up production costs, particularly impacting manufacturers relying on international supply chains. These increased costs have made it harder for companies to offer competitive pricing, especially in a market that is highly price sensitive. Higher production expenses are also being passed on to consumers, causing retail prices to climb. Additionally, supply chain interruptions have delayed final deliveries, creating uncertainty for buyers and slowing adoption rates. Despite these hurdles, local manufacturers have seen an advantage, as reduced foreign competition gives them more room to grow. Over the long term, the industry is expected to recalibrate, with more companies turning to domestic sourcing and reconfiguring supply chains to become less vulnerable to global disruptions.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $772 Million |

| Forecast Value | $11.75 Billion |

| CAGR | 31.4% |

eVTOLs are increasingly being viewed as a practical answer to the inefficiencies of ground-based transportation. Their ability to bypass road traffic and enable swift, direct routes offers a compelling value proposition, especially for urban commuters. These aircraft are designed to land and take off vertically, making them ideal for city environments with limited space. Governments are also acknowledging their potential to transform urban mobility and are integrating them into long-term transportation planning. As clean transportation becomes a national and international priority, electric aviation is gaining support through both regulatory backing and private investment.

Innovation in battery technology and electric propulsion systems is playing a pivotal role in making eVTOLs more commercially viable. Advances in lithium-ion and emerging solid-state batteries are extending flight range, enhancing safety, and increasing payload capacity. At the same time, new materials and efficient propulsion designs are lowering overall operational costs. These improvements are attracting investments from major players in the aerospace and automotive sectors, who see long-term potential in urban air mobility. Developers are also using lightweight composites and exploring energy-efficient motor technologies to enhance aircraft performance while meeting sustainability goals.

By range, the short-haul (up to 100 km) segment accounted for USD 445.4 million in 2024. This category is gaining momentum as the most practical solution for intra-city and regional air travel, especially for use cases requiring quick, frequent flights. These aircraft are well-suited for applications like air taxis, medical transportation, and logistics. Battery improvements are helping extend flight times while increasing payload capacity. Governments and private firms are investing in supporting infrastructure like takeoff and landing zones, though challenges related to noise, regulation, and public trust still need to be addressed.

When broken down by autonomy, pilot-operated eVTOLs led the market in 2024 with a valuation of USD 534.5 million. These models are preferred during the initial stages of commercial deployment due to greater public trust and smoother regulatory approval. While the requirement for trained pilots increases operational costs, it also ensures safety and control, which is critical as the technology gains broader acceptance. Companies are prioritizing user-friendly interfaces and semi-automated cockpit systems to support operators and reduce workload. These aircraft serve as a stepping stone to full autonomy, helping to build credibility and operational data that will eventually support more advanced systems.

In terms of regional demand, the U.S. dominated the market with a valuation of USD 272.7 million in 2024. The country offers a strong ecosystem of legacy aerospace firms and agile startups, supported by a culture that embraces technological innovation. Research efforts focused on battery and automation technologies are pushing the market forward. While integration challenges like air traffic control and public sentiment remain, the country's commitment to commercializing eVTOL services is evident through partnerships with mobility companies and infrastructure investments.

Manufacturers are taking strategic steps to remain competitive by investing in energy-efficient designs, reducing aircraft noise, and integrating automation. Some are leveraging AI for air traffic management and predictive maintenance to streamline operations. Customization for niche sectors like cargo, medical transport, and premium air travel is becoming a key trend. At the same time, mergers, partnerships, and collaborations with regulatory authorities are helping firms scale operations and navigate certification processes. Emerging technologies like digital twins and robotics are also helping reduce costs and increase safety across production lines.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Base estimates and calculations

- 1.3.1 Base year calculation

- 1.3.2 Key trends for market estimation

- 1.4 Forecast model

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.5.2 Data mining sources

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Trump administration tariffs analysis

- 3.2.1 Impact on trade

- 3.2.1.1 Trade volume disruptions

- 3.2.1.2 Retaliatory measures

- 3.2.2 Impact on the industry

- 3.2.2.1 Supply-side impact

- 3.2.2.1.1 Price volatility

- 3.2.2.1.2 Supply chain restructuring

- 3.2.2.1.3 Production cost implications

- 3.2.2.2 Demand-side impact

- 3.2.2.2.1 Price transmission to end markets

- 3.2.2.2.2 Market share dynamics

- 3.2.2.2.3 Consumer response patterns

- 3.2.2.1 Supply-side impact

- 3.2.3 Key companies impacted

- 3.2.4 Strategic industry responses

- 3.2.4.1 Supply chain reconfiguration

- 3.2.4.2 Pricing and product strategies

- 3.2.4.3 Policy engagement

- 3.2.5 Outlook and future considerations

- 3.2.1 Impact on trade

- 3.3 Industry impact forces

- 3.3.1 Growth drivers

- 3.3.1.1 Urban congestion and need for efficient mobility

- 3.3.1.2 Advancements in battery and electric propulsion technologies

- 3.3.1.3 Environmental sustainability and emission reduction goals

- 3.3.1.4 Rising investments and strategic partnerships

- 3.3.2 Industry pitfalls and challenges

- 3.3.2.1 High development costs

- 3.3.2.2 Regulatory approval delays

- 3.3.1 Growth drivers

- 3.4 Growth potential analysis

- 3.5 Regulatory landscape

- 3.6 Technology landscape

- 3.7 Future market trends

- 3.8 Gap analysis

- 3.9 Porter's analysis

- 3.10 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategy dashboard

Chapter 5 Market Estimates & Forecast, By Range, 2021-2034 (USD Million & Units)

- 5.1 Key trends

- 5.2 Short-Haul <100 km

- 5.3 Medium-Haul 100-300 km

- 5.4 Long-Haul >300 km

Chapter 6 Market Estimates & Forecast, By Autonomy Level, 2021-2034 (USD Million & Units)

- 6.1 Key trends

- 6.2 Pilot-operated

- 6.3 Remote-piloted

- 6.4 Fully autonomous

Chapter 7 Market Estimates & Forecast, By Application, 2021-2034 (USD Million & Units)

- 7.1 Key trends

- 7.2 Urban air mobility

- 7.3 Air ambulance

- 7.4 Tourism & leisure

- 7.5 Others

Chapter 8 Market Estimates and Forecast, By Region, 2021 – 2034 (USD Million & Units)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Netherlands

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.6 Middle East and Africa

- 8.6.1 Saudi Arabia

- 8.6.2 South Africa

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 Joby Aviation

- 9.2 Archer Aviation Inc.

- 9.3 EHang

- 9.4 Volocopter

- 9.5 Lilium

- 9.6 BETA Technologies

- 9.7 Vertical Aerospace

- 9.8 Wisk Aero

- 9.9 Supernal, LLC

- 9.10 Eve Air Mobility

- 9.11 Autoflight

- 9.12 Overair, Inc.

- 9.13 AeroMobil

- 9.14 SkyDrive Inc.

- 9.15 Jaunt Air Mobility LLC.

- 9.16 Urban Aeronautics

- 9.17 Bell Textron Inc.

- 9.18 DORONI AEROSPACE INC. ALL

- 9.19 Guangdong Huitian Aerospace Technology Co., Ltd.

- 発行日

- 発行

- Global Market Insights Inc.

- ページ情報

- 英文 189 Pages

- 納期

- 2~3営業日