複合段ボールチューブ包装の市場機会、成長促進要因、産業動向分析、2025~2034年予測

Composite Cardboard Tube Packaging Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034- 発行日

- ページ情報

- 英文 170 Pages

- 納期

- 2~3営業日

- 商品コード

- 1740909

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

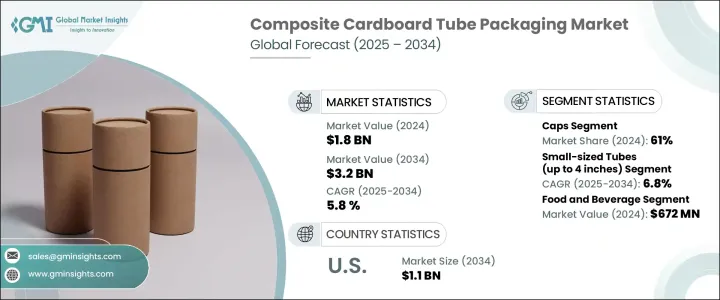

世界の複合段ボールチューブ包装市場は、2024年に18億米ドルと評価され、環境に優しい包装への需要の高まりとeコマースの活発化により、CAGR 5.8%で成長し、2034年には32億米ドルに達すると推定されています。

各業界の企業は持続可能なソリューションへの意識的なシフトを進めており、複合段ボールチューブは、耐久性、リサイクル性、製品のプレゼンテーションを向上させる魅力的なビジュアルアピールなど、すべての条件を満たしているため、強い支持を集めています。美容、パーソナルケアから食品、工業製品に至るまで、ブランドは機能性だけでなく差別化のためにチューブ包装に目を向けています。市場の進化は、最小限の廃棄物、再利用可能な包装、より良い開封体験を好む消費者行動の変化によっても後押しされています。環境に配慮したソリューションへの需要が高まるにつれ、メーカーはデザインのカスタマイズ、素材強度の向上、循環型経済モデルとの連携に注力し、市場はより大きなイノベーションを目の当たりにすることになると予想されます。D2C(消費者直販)小売の成長、サブスクリプションボックスサービスの台頭、円筒形包装フォーマットの贈答用製品の広範な人気が、総体的にこの勢いを形成しています。複合段ボールチューブは、棚陳列でのアピールを高めると同時に、環境に良い影響を残したいと考えているブランドにとって、実用的でスタイリッシュなソリューションとなります。企業がESGへのコミットメントと持続可能性の指標を倍増させる中、この包装形態は世界的なサプライチェーンで急速に好まれる選択肢になりつつあります。

しかしながら、市場は依然として無視できないハードルに直面しています。もともと米国の貿易政策の下で導入された輸入原材料や輸入部品に対する関税は、製造コストの顕著な高騰につながっており、メーカーは岐路に立たされています。コスト増を吸収するか、消費者向けの価格を引き上げるか、あるいは高い輸入関税を避けるために地元サプライヤーに軸足を移すか等、これらの転換により、サプライチェーンの最適化、国産または代替原材料の調達先探し、サプライヤーとのパートナーシップの再評価への注目が高まっています。その上、国際貿易と物流の継続的な混乱は、在庫戦略の回復力を試し続けています。企業は、安定性を確保するために、俊敏な在庫システムへの投資を増やし、調達方法を多様化しています。材料調達、自動化、業務効率の革新は、不安定な市場情勢の中で競争に勝ち残り、利幅を維持するための重要な差別化要因として浮上しています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024年 |

| 予測年 | 2025~2034年 |

| 開始金額 | 18億米ドル |

| 予測金額 | 32億米ドル |

| CAGR | 5.8% |

製品タイプ別では、キャップ部門が2024年の世界複合段ボールチューブ包装市場を61%の圧倒的シェアで牽引しました。キャップの人気は、消費者の使いやすさを維持しながら、輸送中の製品の安全性を確保する安全な密閉機能によるものです。また、軽量キャップはコスト効率の良い輸送をサポートし、材料の使用量を最小限に抑えることで持続可能性の目標にも合致しています。さらに、ブランドはこのフォーマットを活用し、手触りの良い仕上げ、エンボス加工のロゴ、QRコード、スマートラベリング技術によって顧客体験を向上させています。機能的な安全性と高級なデザイン要素を融合できるため、キャップは、保護とブランディングの両方が同様に重要な、特に食品、化粧品、パーソナルケアの分野で、複数の業界で優位に立つことができます。

最大4インチの小型チューブは、最も急成長しているセグメントとして牽引力を増しており、2034年までのCAGRは6.8%で拡大すると予測されています。この需要に寄与しているのは、特にスキンケア、美容、持ち運び可能な食品において、コンパクトで旅行しやすい包装オプションへの消費者のシフトです。これらのチューブは持ち運びに便利で使いやすいだけでなく、耐久性やブランド体験を高める高級感も備えています。消費者がミニマリズムとエココンシャスなアピールを兼ね備えた包装を求める中、小型チューブは機能性とフォルムの両面で成果を上げています。

米国の複合段ボールチューブ包装市場は、持続可能な包装に対する意識の高まりと強固なeコマースエコシステムによって、2034年までに11億米ドルに達すると予想されています。国内メーカーは、棚の視認性を高めながら規制基準を満たすリサイクル可能な生分解性チューブのイノベーションに投資することで、成長を加速させています。これらの新しいデザインは、ブランドが重量と体積を最適化することで輸送の排出を削減し、より優れた構造設計によって製品の安全性を高めるのに役立っています。プラスチック使用に関する規制が厳しくなるにつれ、企業は信頼性が高く、コンプライアンスに適合し、ブランドに優しいソリューションとして段ボールチューブに注目しています。

Sonoco、Smurfit Kappa Group、Paper Tubes &Sales、Visican Ltd、Marshall Paper Tube Co., Inc.などの大手企業は、市場での足跡を強化する戦略を積極的に展開しています。自動化された生産ラインを導入して生産量を増やし、人件費を削減すること、原材料を確保するために提携すること、ニッチ市場に対応するために製品のカスタマイズを拡大すること、リサイクル率を高めることなどがその例です。また、ブランドとエンドユーザーの双方に共感してもらえるような、デザイン、持続可能性、性能を融合させた単一の包装ソリューションを提供するイノベーションにも力を注いでいます。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- トランプ政権の関税分析

- 貿易への影響

- 貿易量の混乱

- 報復措置

- 業界への影響

- 供給側の影響(原材料)

- 主要原材料の価格変動

- サプライチェーンの再構築

- 生産コストへの影響

- 需要側の影響(販売価格)

- 最終市場への価格伝達

- 市場シェアの動向

- 消費者の反応パターン

- 影響を受ける主要企業

- 戦略的な業界対応

- サプライチェーンの再構成

- 価格設定と製品戦略

- 政策関与

- 展望と今後の検討事項

- 貿易への影響

- 業界への影響要因

- 促進要因

- 持続可能でリサイクル可能な包装ソリューションに対する消費者の嗜好の高まり

- eコマース普及率の上昇による保護輸送チューブの需要増加

- 独自のブランド差別化を求めるプレミアムブランドのカスタマイズニーズの高まり

- 化粧品、医薬品、特殊食品分野での用途拡大

- 持続可能な包装への注目の高まり

- 業界の潜在的リスク&課題

- 原材料価格の変動による製造マージンへの影響

- 代替包装ソリューションとの競合

- 促進要因

- 成長可能性分析

- 規制情勢

- テクノロジーの情勢

- 将来の市場動向

- ギャップ分析

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 主要市場企業の競合分析

- 競合ポジショニングマトリックス

- 戦略ダッシュボード

第5章 市場推計・予測:クロージャータイプ別、2021~2034年

- 主要動向

- キャップ

- 蓋

第6章 市場推計・予測:サイズ別、2021~2034年

- 主要動向

- 小型チューブ(最大4インチ)

- 中型チューブ(4~10インチ)

- 大型チューブ(10インチ以上)

第7章 市場推計・予測:最終用途産業別、2021~2034年

- 主要動向

- 食品・飲料

- 医薬品

- 化粧品・パーソナルケア

- 化学薬品

- その他

第8章 市場推計・予測:地域別、2021~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- スペイン

- イタリア

- オランダ

- アジア太平洋地域

- 中国

- インド

- オーストラリア

- 韓国

- 日本

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- サウジアラビア

- アラブ首長国連邦

- 南アフリカ

第9章 企業プロファイル

- Ace Paper Tube Corp

- CBT Packaging

- Chicago Mailing Tube Co.

- Darpac P/L

- Hansen Packaging

- Heartland Products Group

- Marshall Paper Tube Co.、Inc.

- Paper Tubes &Sales

- Smurfit Kappa Group

- Sonoco

- Valk Industries

- Visican Ltd

目次

The Global Composite Cardboard Tube Packaging Market was valued at USD 1.8 billion in 2024 and is estimated to grow at a CAGR of 5.8% to reach USD 3.2 billion by 2034, driven by the growing demand for eco-friendly packaging and the rise in e-commerce activity. Businesses across industries are making conscious shifts toward sustainable solutions, and composite cardboard tubes are gaining strong traction as they check off all the right boxes-durability, recyclability, and an attractive visual appeal that enhances product presentation. From beauty and personal care to food and industrial goods, brands are turning to tube packaging not just for function but for differentiation. The market's evolution is also being fueled by changing consumer behaviors that favor minimal waste, reusable packaging, and a better unboxing experience. As demand for environmentally responsible solutions climbs, the market is expected to witness greater innovation, with manufacturers focusing on customizing designs, improving material strength, and aligning with circular economy models. The growth of D2C (direct-to-consumer) retail, rising subscription box services, and the widespread popularity of gifting products in cylindrical packaging formats are collectively shaping the momentum. Composite cardboard tubes serve as a practical and stylish solution for brands looking to leave a positive environmental impact while boosting shelf appeal. As companies double down on ESG commitments and sustainability metrics, this packaging format is fast becoming a preferred option across global supply chains.

That said, the market still faces hurdles that can't be ignored. Tariffs on imported raw materials and components, originally introduced under earlier U.S. trade policies, have led to a noticeable spike in production costs. Manufacturers are at a crossroads-either absorb the added costs, increase prices for consumers, or pivot to local suppliers to avoid high import duties. This shift has intensified the focus on optimizing supply chains, finding domestic or alternative raw material sources, and reevaluating supplier partnerships. On top of that, ongoing disruptions in international trade and logistics continue to test the resilience of inventory strategies. Companies are increasingly investing in agile inventory systems and diversifying sourcing methods to ensure stability. Innovation in material sourcing, automation, and operational efficiency has emerged as a critical differentiator in staying ahead of the competition and maintaining margins in a volatile market landscape.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $1.8 Billion |

| Forecast Value | $3.2 Billion |

| CAGR | 5.8% |

In terms of product type, the caps segment led the global composite cardboard tube packaging market with a dominant 61% share in 2024. Their popularity is largely due to secure closure features that ensure product safety during shipping while maintaining ease of use for consumers. Lightweight caps also support cost-effective transportation and align well with sustainability goals by minimizing material usage. Additionally, brands are leveraging this format to enhance customer experience through tactile finishes, embossed logos, QR codes, and smart labeling technologies. The ability to blend functional security with high-end design elements gives caps an edge across multiple verticals-particularly in food, cosmetics, and personal care-where both protection and branding are equally critical.

Small-sized tubes measuring up to 4 inches are gaining traction as the fastest-growing segment, projected to expand at a CAGR of 6.8% through 2034. What is fueling this demand is the consumer shift toward compact, travel-friendly packaging options, especially in skincare, beauty, and on-the-go food products. These tubes are not only portable and user-friendly but also provide durability and a premium touch that elevates brand experience. As consumers seek packaging that combines minimalism with eco-conscious appeal, small tubes are delivering on both fronts-functionality and form.

The United States Composite Cardboard Tube Packaging Market is expected to reach USD 1.1 billion by 2034, driven by heightened awareness of sustainable packaging and a robust e-commerce ecosystem. Domestic manufacturers are stepping up by investing in recyclable, biodegradable tube innovations that meet regulatory benchmarks while enhancing shelf visibility. These new designs are helping brands cut down on transportation emissions by optimizing weight and volume and are boosting product safety with better structural design. As regulations around plastic usage become more stringent, businesses are gravitating toward cardboard tubes as a reliable, compliant, and brand-friendly solution.

Leading players such as Sonoco, Smurfit Kappa Group, Paper Tubes & Sales, Visican Ltd, and Marshall Paper Tube Co., Inc. are actively deploying strategies to strengthen their footprint in the market. These include embracing automated production lines to ramp up output and cut labor costs, partnering for secure raw material access, expanding product customization to serve niche markets, and integrating higher percentages of recycled content. To stay relevant and ahead, they are banking heavily on innovation-blending design, sustainability, and performance into a single packaging solution that resonates with both brands and end users.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Base estimates and calculations

- 1.3.1 Base year calculation

- 1.3.2 Key trends for market estimation

- 1.4 Forecast model

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.5.2 Data mining sources

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Trump administration tariffs analyisis

- 3.2.1 Impact on trade

- 3.2.1.1 Trade volume disruptions

- 3.2.1.2 Retaliatory measures

- 3.2.1.3 Impact on the industry

- 3.2.1.4 Supply-side impact (raw materials)

- 3.2.1.4.1.1 Price volatility in key materials

- 3.2.1.4.1.2 Supply chain restructuring

- 3.2.1.4.1.3 Production cost implications

- 3.2.1.5 Demand-side impact (selling price)

- 3.2.1.5.1.1 Price transmission to end markets

- 3.2.1.5.1.2 Market share dynamics

- 3.2.1.5.1.3 Consumer response patterns

- 3.2.1.6 Key companies impacted

- 3.2.1.7 Strategic industry responses

- 3.2.1.7.1.1 Supply chain reconfiguration

- 3.2.1.7.1.2 Pricing and product strategies

- 3.2.1.7.1.3 Policy engagement

- 3.2.1.8 Outlook and future considerations

- 3.2.1 Impact on trade

- 3.3 Industry impact forces

- 3.3.1 Growth drivers

- 3.3.1.1 Growing consumer preference for sustainable and recyclable packaging solutions

- 3.3.1.2 Rising e-commerce penetration driving demand for protective shipping tubes

- 3.3.1.3 Increasing customization needs for premium brands seeking unique brand differentiation

- 3.3.1.4 Expanding applications in cosmetics, pharmaceuticals and specialty food sectors

- 3.3.1.5 Increasing focus on sustainable packaging

- 3.3.2 Industry pitfalls and challenges

- 3.3.2.1 Volatility in raw material prices impacting manufacturing margins

- 3.3.2.2 Competition from alternative packaging solutions

- 3.3.1 Growth drivers

- 3.4 Growth potential analysis

- 3.5 Regulatory landscape

- 3.6 Technology landscape

- 3.7 Future market trends

- 3.8 Gap analysis

- 3.9 Porter's analysis

- 3.10 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategy dashboard

Chapter 5 Market Estimates and Forecast, By Closure Type, 2021 - 2034 ($ Mn & Units)

- 5.1 Key trends

- 5.2 Caps

- 5.3 Lids

Chapter 6 Market Estimates and Forecast, By Size, 2021 - 2034 ($ Mn & Units)

- 6.1 Key trends

- 6.2 Small-sized tubes (up to 4 inches)

- 6.3 Medium-sized tubes (4 to 10 inches)

- 6.4 Large-sized tubes (over 10 inches)

Chapter 7 Market Estimates and Forecast, By End Use Industry, 2021 - 2034 ($ Mn & Units)

- 7.1 Key trends

- 7.2 Food and Beverage

- 7.3 Pharmaceuticals

- 7.4 Cosmetics and Personal Care

- 7.5 Chemicals

- 7.6 Others

Chapter 8 Market Estimates and Forecast, By Region, 2021 - 2034 ($ Mn & Units)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Netherlands

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Australia

- 8.4.4 South Korea

- 8.4.5 Japan

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.6 Middle East and Africa

- 8.6.1 Saudi Arabia

- 8.6.2 U.A.E.

- 8.6.3 South Africa

Chapter 9 Company Profiles

- 9.1 Ace Paper Tube Corp

- 9.2 CBT Packaging

- 9.3 Chicago Mailing Tube Co.

- 9.4 Darpac P/L

- 9.5 Hansen Packaging

- 9.6 Heartland Products Group

- 9.7 Marshall Paper Tube Co., Inc.

- 9.8 Paper Tubes & Sales

- 9.9 Smurfit Kappa Group

- 9.10 Sonoco

- 9.11 Valk Industries

- 9.12 Visican Ltd

- 発行日

- 発行

- Global Market Insights Inc.

- ページ情報

- 英文 170 Pages

- 納期

- 2~3営業日