|

市場調査レポート

商品コード

1740886

自動車用ガス封入ショックアブソーバーの市場機会、成長促進要因、産業動向分析、2025~2034年予測Automotive Gas Charged Shock Absorber Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| 自動車用ガス封入ショックアブソーバーの市場機会、成長促進要因、産業動向分析、2025~2034年予測 |

|

出版日: 2025年04月24日

発行: Global Market Insights Inc.

ページ情報: 英文 190 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

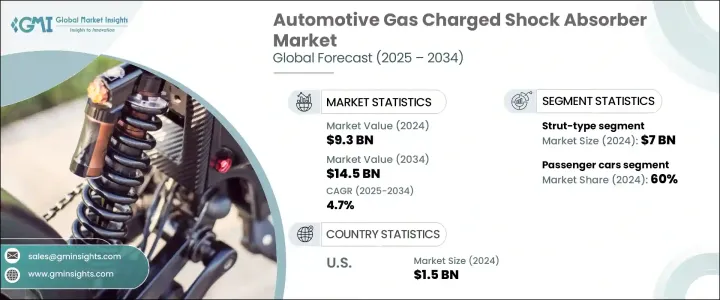

自動車用ガス封入ショックアブソーバーの世界市場規模は、2024年に93億米ドルとなり、乗り心地の向上、優れた車両ハンドリング、多様な地形でのより安全な運転体験に対する消費者の期待の高まりに支えられ、CAGR 4.7%で成長し、2034年には145億米ドルに達すると推定されます。

自動車メーカーが先進的なサスペンション・システムへのシフトを続ける中、ガスチャージ式ショック・アブソーバーのような高性能部品の需要が大きく伸びています。これらのアブソーバーは、特に高速走行やオフロード走行において、振動を低減し、車両の安定性を高め、スムーズな乗り心地を実現する上で重要な役割を果たしています。

自動車技術の進化に伴い、消費者は現在、自動車に快適性と性能の両方を求めるようになっており、その結果、先進的なダンピングシステムが自動車工学の最前線に位置づけられています。高級車セグメントの世界の拡大、都市部の交通渋滞の増加、長距離運転の習慣の急増は、総合的に、より優れたショック管理システムの必要性を煽っています。ガスチャージ式ショックアブソーバーは、通気や発泡に対する耐性を提供することにより、従来の油圧式ショックに比べて重要な利点を提供し、連続運転やアグレッシブな運転でも安定した性能を保証します。自動車セクターが電動化とスマート・ビークル・システムに傾倒するにつれ、これらのアブソーバーは、エネルギー効率やバッテリーの航続距離を損なうことなく、動的負荷をサポートするよう調整されています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 93億米ドル |

| 予測金額 | 145億米ドル |

| CAGR | 4.7% |

パフォーマンス重視の車両プラットフォーム、特にSUVやクロスオーバーの急速な普及に伴い、ガスチャージ式ショックアブソーバーは乗用車と商用車の両方のカテゴリーで標準的な部品になりつつあります。高度な減衰効率を実現し、さまざまな荷重や条件下で最適なバランスを維持するその能力は、今日のサスペンション・システムに不可欠なものとなっています。これらのショックアブソーバーは、より良いハンドリング、ボディロールの低減、ピッチコントロールの改善、全体的な滑らかな乗り心地を求める消費者ニーズの高まりに応えるために設計されています。自動車メーカーは、性能を差別化し、高級な乗り心地を求める需要に応えるため、新型車にガスチャージ式アブソーバーを組み込んでいます。このような嗜好の高まりは、道路状況や運転に対する期待が大きく異なる都市部と農村部の両方で顕著であり、ガスチャージド・システムの多用途性をさらに実証しています。

乗用車セグメントは、マイカー所有率の上昇、可処分所得の増加、中間所得層の拡大に牽引され、2024年には60%の圧倒的シェアを占めました。消費者は、快適性、安定性、ハンドリングが改善された自動車を優先するようになっており、特に毎日の通勤や長距離移動に適しています。自動車販売が好調な新興国では、シームレスなドライビング体験を提供する自動車を購入者が求めているため、プレミアムサスペンションコンポーネントへの注目が高まっています。ガスチャージ式ショックアブソーバーは、より優れた減衰特性を提供することでこの需要に応え、快適性、制御性、安全性を目的とした最新の自動車プラットフォームで好まれる選択肢となっています。

取り付けタイプ別では、ストラットタイプのガス・チャージド・ショック・アブソーバーが2024年の評価額70億米ドルで市場をリードしています。これらのコンポーネントは、コイルスプリングとショックアブソーバーを1つのコンパクトなユニットに統合した一体型構造のため、広く採用されています。この構成は、フロント・サスペンションのレイアウトにおけるスペース効率をサポートし、車両全体の重量を軽減して燃費と排出ガスの低減に貢献します。また、取り付けの容易さやメンテナンスの簡素化も実現しており、ストラットタイプのショックアブソーバーは、大規模な自動車製造において費用対効果の高いソリューションとなっています。

北米自動車用ガス封入ショックアブソーバー市場は2024年に15億米ドルを占め、2025年から2034年にかけてCAGR 4.9%で成長すると予測されています。この成長の背景には、この地域の好調な自動車生産、大手OEMの存在、高耐久性サスペンションシステムを必要とするピックアップやクロスオーバーのような大型車への嗜好の高まりがあります。また、電動化を推進する同地域は、軽量化とエネルギー効率をサポートしながら、最新のドライブトレイン要件に適合する高度なショックアブソーバーの需要を押し上げています。

Hitachi Astemo、HL Mando、Gabriel India、KYB、Showa、ZF Friedrichshafen、Chassis Brakes、Endurance Technologies、Cofap、Tennecoなどの主要企業は、技術革新と戦略的提携を通じて市場での地位を積極的に強化しています。これらの企業は、ショックアブソーバーの性能を高めるために研究開発に多額の投資を行い、製造拠点を世界的に拡大し、OEMと重要なパートナーシップを結んでいます。また、多くの企業が、路面からのフィードバックや運転行動に基づいてリアルタイムの適応性を提供する電子制御減衰システムを開発することで、スマートカーや自律走行車の未来に合わせて、提供する製品を多様化しています。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- サプライヤーの情勢

- 原材料供給者

- 部品供給業者

- 製造業者

- テクノロジープロバイダー

- 流通チャネル分析

- 最終用途

- 利益率分析

- サプライヤーの情勢

- トランプ政権による関税への影響

- 貿易への影響

- 貿易量の混乱

- 報復措置

- 業界への影響

- 供給側の影響(原材料)

- 主要原材料の価格変動

- サプライチェーンの再構築

- 生産コストへの影響

- 需要側の影響(販売価格)

- 最終市場への価格伝達

- 市場シェアの動向

- 消費者の反応パターン

- 供給側の影響(原材料)

- 戦略的な業界対応

- サプライチェーンの再構成

- 価格設定と製品戦略

- 貿易への影響

- テクノロジーとイノベーションの情勢

- 特許分析

- 規制情勢

- コスト内訳分析

- 価格動向

- 地域

- 車両

- 主なニュースと取り組み

- 影響要因

- 促進要因

- 乗り心地と操縦安定性への需要の高まり

- 電気自動車とハイブリッド車の普及の増加

- サスペンションシステムの技術的進歩

- 世界の自動車生産の拡大

- 業界の潜在的リスク&課題

- 油圧ショックアブソーバーに比べてコストが高め

- 厳格な環境および安全規制

- 促進要因

- 成長可能性分析

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 競合ポジショニングマトリックス

- 戦略的展望マトリックス

第5章 市場推計・予測:技術別、2021-2034

- 主要動向

- ツインチューブガス

- モノチューブガス

第6章 市場推計・予測:最終用途別、2021-2034

- 主要動向

- 乗用車

- ハッチバック

- セダン

- SUV

- 商用車

- 小型商用車(LCV)

- 中型商用車(MCV)

- 大型商用車(HCV)

第7章 市場推計・予測:マウント、2021-2034

- 主要動向

- ストラット型

- 伸縮式

第8章 市場推計・予測:販売チャネル別2021-2034

- 主要動向

- OEM

- アフターマーケット

第9章 市場推計・予測:地域別、2021-2034

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- フランス

- 英国

- スペイン

- イタリア

- ロシア

- 北欧諸国

- アジア太平洋地域

- 中国

- インド

- 日本

- 韓国

- オーストラリア・ニュージーランド

- 東南アジア

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- アラブ首長国連邦

- 南アフリカ

- サウジアラビア

第10章 企業プロファイル

- AL-KO Fahrzeugtechnik

- Bilstein

- Chassis Brakes

- Cofap

- Endurance

- Gabriel

- Hitachi Astemo

- ITW

- Jiangsu Huachuan

- KYB

- Liuzhou Shuangfei

- Magneti Marelli

- Mando

- Ride Control

- S&T Motiv

- Showa

- Tenneco

- Tokico

- YSS Suspension

- ZF Friedrichshafen

The Global Automotive Gas Charged Shock Absorber Market was valued at USD 9.3 billion in 2024 and is estimated to grow at a CAGR of 4.7% to reach USD 14.5 billion by 2034, supported by rising consumer expectations for enhanced ride comfort, superior vehicle handling, and safer driving experiences across diverse terrains. As automakers continue to shift toward advanced suspension systems, the demand for high-performance components like gas-charged shock absorbers is gaining significant traction. These absorbers play a key role in reducing vibrations, enhancing vehicle stability, and delivering smoother rides, especially in high-speed and off-road conditions.

With evolving automotive technologies, consumers now expect their vehicles to offer both comfort and performance, which has placed advanced damping systems at the forefront of vehicle engineering. The global expansion of premium vehicle segments, growing urban traffic congestion, and a surge in long-distance driving habits are collectively fueling the need for better shock management systems. Gas-charged shock absorbers provide a crucial advantage over traditional hydraulic shocks by offering resistance to aeration and foaming, which ensures consistent performance under continuous or aggressive driving. As the automotive sector leans more into electrification and smart vehicle systems, these absorbers are being tailored to support dynamic loads without compromising energy efficiency or battery range.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $9.3 Billion |

| Forecast Value | $14.5 Billion |

| CAGR | 4.7% |

With the rapid adoption of performance-focused vehicle platforms, particularly SUVs and crossovers, gas-charged shock absorbers are becoming a standard component in both passenger and commercial vehicle categories. Their ability to deliver advanced damping efficiency and maintain optimal balance under varying loads and conditions makes them indispensable in today's suspension systems. These shock absorbers are engineered to meet the growing consumer need for better handling, reduced body roll, improved pitch control, and overall smoother rides. Automakers are integrating gas-charged absorbers into newer models to differentiate performance features and meet the demand for premium ride quality. This growing preference is evident in both urban and rural settings, where road conditions and driving expectations vary significantly, further validating the versatility of gas-charged systems.

The passenger vehicle segment commanded a dominant 60% share in 2024, driven by the increasing rate of personal car ownership, rising disposable incomes, and an expanding middle-class demographic. Consumers are prioritizing vehicles that offer improved comfort, stability, and handling-particularly for daily commutes and longer journeys. In emerging economies, where car sales are booming, the focus on premium suspension components is intensifying as buyers look for vehicles that deliver a seamless driving experience. Gas-charged shock absorbers meet this demand by providing better damping characteristics, making them a preferred choice in modern vehicle platforms aimed at comfort, control, and safety.

Based on mounting type, strut-type gas charged shock absorbers led the market with a valuation of USD 7 billion in 2024. These components are widely adopted due to their integrated construction, which combines the coil spring and shock absorber into one compact unit. This configuration supports space efficiency in front suspension layouts and helps reduce the vehicle's overall weight, contributing to fuel efficiency and lower emissions. The design also offers ease of installation and simplified maintenance, making strut-type shock absorbers a cost-effective solution for large-scale automotive manufacturing.

The North America Automotive Gas Charged Shock Absorber Market accounted for USD 1.5 billion in 2024 and is projected to grow at a CAGR of 4.9% from 2025 to 2034. This growth is backed by strong regional vehicle production, the presence of major OEMs, and a rising preference for larger vehicles like pickups and crossovers that demand high-durability suspension systems. The region's push toward electrification is also boosting demand for advanced shock absorbers that align with modern drivetrain requirements while supporting weight reduction and energy efficiency.

Leading companies such as Hitachi Astemo, HL Mando, Gabriel India, KYB, Showa, ZF Friedrichshafen, Chassis Brakes, Endurance Technologies, Cofap, and Tenneco are actively strengthening their market positions through innovation and strategic collaborations. These players are investing heavily in R&D to enhance shock absorber performance, expand their manufacturing footprint globally, and form key partnerships with OEMs. Many are also diversifying their offerings by developing electronically controlled damping systems that provide real-time adaptability based on road feedback and driving behavior, aligning with the future of smart and autonomous vehicles.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.1.1 Research approach

- 1.1.2 Data collection methods

- 1.2 Base estimates & calculations

- 1.2.1 Base year calculation

- 1.2.2 Key trends for market estimation

- 1.3 Forecast model

- 1.4 Primary research and validation

- 1.4.1 Primary sources

- 1.4.2 Data mining sources

- 1.5 Market scope & definition

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.1.1 Raw material providers

- 3.1.1.2 Component providers

- 3.1.1.3 Manufacturers

- 3.1.1.4 Technology providers

- 3.1.1.5 Distribution channel analysis

- 3.1.1.6 End use

- 3.1.2 Profit margin analysis

- 3.1.1 Supplier landscape

- 3.2 Impact of Trump administration tariffs

- 3.2.1 Impact on trade

- 3.2.1.1 Trade volume disruptions

- 3.2.1.2 Retaliatory measures

- 3.2.2 Impact on industry

- 3.2.2.1 Supply-side impact (raw materials)

- 3.2.2.1.1 Price volatility in key materials

- 3.2.2.1.2 Supply chain restructuring

- 3.2.2.1.3 Production cost implications

- 3.2.2.2 Demand-side impact (selling price)

- 3.2.2.2.1 Price transmission to end markets

- 3.2.2.2.2 Market share dynamics

- 3.2.2.2.3 Consumer response patterns

- 3.2.2.1 Supply-side impact (raw materials)

- 3.2.3 Strategic industry responses

- 3.2.3.1 Supply chain reconfiguration

- 3.2.3.2 Pricing and product strategies

- 3.2.1 Impact on trade

- 3.3 Technology & innovation landscape

- 3.4 Patent analysis

- 3.5 Regulatory landscape

- 3.6 Cost breakdown analysis

- 3.7 Price trend

- 3.7.1 Region

- 3.7.2 Vehicle

- 3.8 Key news & initiatives

- 3.9 Impact forces

- 3.9.1 Growth drivers

- 3.9.1.1 Growing demand for ride comfort & handling stability

- 3.9.1.2 Rising adoption of electric and hybrid vehicles

- 3.9.1.3 Technological advancements in suspension systems

- 3.9.1.4 Expansion of global automotive production

- 3.9.2 Industry pitfalls & challenges

- 3.9.2.1 Higher cost compared to hydraulic shock absorbers

- 3.9.2.2 Stringent environmental & safety regulations

- 3.9.1 Growth drivers

- 3.10 Growth potential analysis

- 3.11 Porter's analysis

- 3.12 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Technology, 2021 - 2034 ($Mn, Units)

- 5.1 Key trends

- 5.2 Twin-tube gas

- 5.3 Monotube gas

Chapter 6 Market Estimates & Forecast, By End Use, 2021 - 2034 ($Mn, Units)

- 6.1 Key trends

- 6.2 Passenger cars

- 6.2.1 Hatchback

- 6.2.2 Sedan

- 6.2.3 SUV

- 6.3 Commercial vehicles

- 6.3.1 Light Commercial Vehicles (LCV)

- 6.3.2 Medium Commercial Vehicles (MCV)

- 6.3.3 Heavy Commercial Vehicles (HCV)

Chapter 7 Market Estimates & Forecast, By Mount, 2021 - 2034 ($Mn, Units)

- 7.1 Key trends

- 7.2 Strut-type

- 7.3 Telescopic

Chapter 8 Market Estimates & Forecast, By Sales Channel 2021 - 2034 ($Mn, Units)

- 8.1 Key trends

- 8.2 OEM

- 8.3 Aftermarket

Chapter 9 Market Estimates & Forecast, By Region, 2021 - 2034 ($Mn, Units)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 France

- 9.3.3 UK

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Russia

- 9.3.7 Nordics

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 South Korea

- 9.4.5 ANZ

- 9.4.6 Southeast Asia

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 MEA

- 9.6.1 UAE

- 9.6.2 South Africa

- 9.6.3 Saudi Arabia

Chapter 10 Company Profiles

- 10.1 AL-KO Fahrzeugtechnik

- 10.2 Bilstein

- 10.3 Chassis Brakes

- 10.4 Cofap

- 10.5 Endurance

- 10.6 Gabriel

- 10.7 Hitachi Astemo

- 10.8 ITW

- 10.9 Jiangsu Huachuan

- 10.10 KYB

- 10.11 Liuzhou Shuangfei

- 10.12 Magneti Marelli

- 10.13 Mando

- 10.14 Ride Control

- 10.15 S&T Motiv

- 10.16 Showa

- 10.17 Tenneco

- 10.18 Tokico

- 10.19 YSS Suspension

- 10.20 ZF Friedrichshafen