|

市場調査レポート

商品コード

1740769

炭素繊維製船体の市場機会、成長促進要因、産業動向分析、2025年~2034年予測Carbon Fiber Boat Hulls Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| 炭素繊維製船体の市場機会、成長促進要因、産業動向分析、2025年~2034年予測 |

|

出版日: 2025年04月24日

発行: Global Market Insights Inc.

ページ情報: 英文 220 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

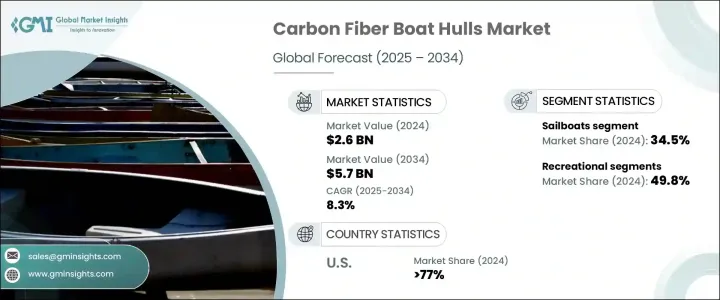

世界の炭素繊維製船体市場は、2024年には26億米ドルと評価され、CAGR 8.3%で成長し、2034年には57億米ドルに達すると推定されています。

この急成長の背景には、レクリエーションと商業の両分野で、軽量で高性能な船舶に対する世界の欲求の高まりがあります。海洋愛好家、防衛事業体、オフショア事業者が、より高速で燃料効率が高く、耐食性に優れたソリューションを求めるなか、炭素繊維製船体が理想的な材料として浮上しています。炭素繊維複合材料は、その優れた強度対重量比、強化された耐久性、および長期的な性能の利点により、従来の材料に取って代わり、市場は技術的なシフトを経験しています。さらに、高級水上バイクに対する消費支出の増加や、環境に配慮した観光への関心の高まりが、先進的で燃料効率の高い船舶の需要を後押ししています。炭素繊維は抵抗を減らし、船舶の応答性を向上させる能力があるため、ヨットレースやセーリングなどの性能重視の分野では特に魅力的です。環境に優しい推進技術への志向の高まりは、海事分野における排出削減を促進する厳しい規制枠組みと相まって、世界的に炭素繊維製船体の採用をさらに加速させています。

自律型および無人海上車両への投資が炭素繊維製船体市場を大きく押し上げています。監視、海洋調査、オフショア保守など、これらの用途には、高度なナビゲーションシステムとペイロードの統合をサポートできる耐久性と構造的堅牢性を備えた材料が必要です。炭素繊維複合材料は、耐腐食性、軽量構造、次世代海洋技術の複雑な運用要件に適合する構造的完全性を提供し、これらの条件をすべて満たします。官民を問わず、過酷な海洋環境における船舶の性能を高める炭素繊維製船体に注目が集まっています。この動向により、防衛機関、深海探査会社、海洋研究機関が調達仕様に炭素繊維製船体を含めるようになり、2034年までの市場の安定を支える信頼性の高い成長需要基盤が形成されています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 26億米ドル |

| 予測金額 | 57億米ドル |

| CAGR | 8.3% |

共同出資の技術革新助成金や技術加速装置を含む政府および民間のイニシアティブも、炭素繊維を海洋インフラに統合する上で極めて重要な役割を果たしています。これらのプログラムは、次世代船体への先端複合材の採用を合理化し、レクリエーション、商業、防衛の各海洋分野での運用排出量とコストの削減に役立っています。

2024年の炭素繊維製船体市場は、ボートのタイプ別にセールボート、ヨット、フィッシングボート、軍用ボート、レスキューボート、その他のカテゴリーに区分されました。セイルボートが34.5%と最大のシェアを占めており、これは複合材製造技術の大きな進歩により、性能を向上させながら製造コストを削減し続けていることによる。帆船は、レジャー用セーリングと競合レースへの関心の高まりにより、このセグメントを支配しています。炭素繊維の使用は、流体力学的抵抗を低減し、操縦性を向上させる。さらに、環境意識の高まりが消費者を風力発電船に向かわせており、炭素繊維構造によって比類のない耐塩水性と燃費経済性が実現されています。

市場を用途別に分類すると、主にレクリエーション用、商業用、軍事・防衛用、その他に分けられます。レジャー用途が49.8%と圧倒的なシェアを占め、次いで商業用途となっています。トップクラスのスピード、燃費、美観を備えた洗練された高性能船に対する消費者の嗜好が高まっているため、炭素繊維はレジャーボートでますます人気が高まっています。炭素繊維の船体は特に高級ヨットやヨットに適しており、軽量構造と卓越した耐久性を提供します。この動向は、カスタマイズされた性能重視のマリン体験を求める富裕層の増加に後押しされています。

米国の炭素繊維製船体市場だけでも、2024年の市場規模は4億1,000万米ドルです。米国政府は、この分野の経済的重要性が高まっていることを反映して、NAICS分類に繊維強化複合材製ボートのカテゴリーを追加する改正を提案しています。この動きにより、規制の明確化、データの追跡、業界全体の的を絞った投資が強化されることが期待されます。炭素繊維製船体の需要は、燃費効率と環境コンプライアンスをサポートする軽量で高性能な船舶の必要性によって、すべての地域で高まっています。

炭素繊維製船体の世界市場における主要企業には、Durham Boat, North Sea Boats, DCB Performance Boats, Scout Boats, and SAERTEX Stadeなどがあります。これらの企業は、より高い強度、軽量化、耐久性の向上を提供する次世代炭素繊維複合材料を設計するために最先端の技術を採用しています。彼らの焦点は、最も過酷な海洋条件下でもスピード、燃料節約、メンテナンスの軽減を実現する、豪華で性能重視の水上バイクに対する需要の高まりに応えることです。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- バリューチェーンに影響を与える要因

- 利益率分析

- ディスラプション

- 将来の展望

- 製造業者

- 販売代理店

- サプライヤーの情勢

- 利益率分析

- 主なニュースと取り組み

- 規制情勢

- 影響要因

- 促進要因

- 軽量で燃費効率の高い船舶の需要増加

- 炭素繊維製造および複合材料技術の進歩

- 業界の潜在的リスク&課題

- リサイクルと環境問題

- 高い材料費と生産コスト

- 促進要因

- トランプ政権の関税の影響- 構造化された概要

- 貿易への影響

- 貿易量の混乱

- 報復措置

- 業界への影響

- 供給側の影響(原材料)

- 主要原材料の価格変動

- サプライチェーンの再構築

- 生産コストへの影響

- 需要側の影響(販売価格)

- 最終市場への価格伝達

- 市場シェアの動向

- 消費者の反応パターン

- 影響を受ける主要企業

- 戦略的な業界対応

- サプライチェーンの再構成

- 価格設定と製品戦略

- 政策関与

- 貿易への影響

- 展望と今後の検討事項

- 成長可能性分析

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 競合ポジショニングマトリックス

- 戦略的展望マトリックス

第5章 市場推計・予測:船種別、2021-2034

- 主要動向

- 帆船

- ヨット

- 漁船

- 軍用船

- 救助艇

- その他

第6章 市場推計・予測:船体タイプ別、2021-2034

- 主要動向

- 単殻型船

- 複数船体

- 滑走船体

- 排水型船体

- 半排水型船体

- その他

第7章 市場推計・予測:用途別、2021-2034

- 主要動向

- 娯楽用

- 商業用

- 軍事・防衛

- その他

第8章 市場推計・予測:地域別、2021-2034

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- スペイン

- イタリア

- オランダ

- アジア太平洋地域

- 中国

- インド

- 日本

- オーストラリア

- 韓国

- ラテンアメリカ

- ブラジル

- メキシコ

- 中東・アフリカ

- サウジアラビア

- 南アフリカ

- アラブ首長国連邦

第9章 企業プロファイル

- Arrow Shark RC

- Carbon

- DCB Performance Boat

- Durham Boat

- Ghostworks Marine

- North Sea Boats

- Oxean Marine

- SAERTEX Stade

- Scout Boats

- TFL North America

The Global Carbon Fiber Boat Hulls Market was valued at USD 2.6 billion in 2024 and is estimated to grow at a CAGR of 8.3% to reach USD 5.7 billion by 2034. This surge is fueled by a growing global appetite for lightweight, high-performance marine vessels across both recreational and commercial sectors. As marine enthusiasts, defense entities, and offshore operators seek faster, more fuel-efficient, and corrosion-resistant solutions, carbon fiber hulls are emerging as the ideal material choice. The market is experiencing a technological shift, with carbon fiber composites replacing traditional materials due to their superior strength-to-weight ratio, enhanced durability, and long-term performance benefits. Additionally, increased consumer spending on luxury watercraft and rising interest in environmentally conscious tourism are driving the demand for advanced, fuel-efficient vessels. Carbon fiber's ability to reduce drag and improve vessel responsiveness makes it especially appealing in performance-oriented segments like yacht racing and sailing. The growing inclination toward green propulsion technologies, combined with stringent regulatory frameworks promoting emission reductions in the maritime sector, is further accelerating the adoption of carbon fiber hulls worldwide.

Investments in autonomous and unmanned marine vehicles are significantly boosting the carbon fiber boat hulls market. These applications, spanning surveillance, oceanographic research, and offshore maintenance, require durable, structurally robust materials capable of supporting advanced navigation systems and payload integration. Carbon fiber composites check all these boxes, offering corrosion resistance, lightweight construction, and structural integrity that aligns with the complex operational requirements of next-gen marine technology. Public and private sector entities alike are turning to carbon fiber hulls for their ability to enhance vessel performance in extreme marine environments. This trend has led defense agencies, deep-sea exploration firms, and marine research institutions to include carbon fiber hulls in their procurement specifications-creating a reliable and growing demand base that will support market stability through 2034.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $2.6 Billion |

| Forecast Value | $5.7 Billion |

| CAGR | 8.3% |

Government and private initiatives, including co-funded innovation grants and technology accelerators, are also playing a pivotal role in integrating carbon fiber into marine infrastructure. These programs are streamlining the adoption of advanced composites for next-generation hulls, helping reduce operational emissions and costs across recreational, commercial, and defense marine segments.

In 2024, the carbon fiber boat hulls market was segmented by boat type into sailboats, yachts, fishing boats, military boats, rescue boats, and other categories. Sailboats held the largest share at 34.5%, driven by major advances in composite fabrication technologies that continue to reduce manufacturing costs while enhancing performance. Sailboats dominate the segment due to increased interest in leisure sailing and competitive racing. The use of carbon fiber reduces hydrodynamic drag and enhances maneuverability, both crucial factors in sailing efficiency. Additionally, growing eco-consciousness is pushing consumers toward wind-powered vessels, where carbon fiber construction provides unmatched saltwater resistance and fuel economy.

When segmented by application, the market is primarily divided into recreational, commercial, military and defense, and others. Recreational applications dominate with a commanding 49.8% share, followed by commercial use. Carbon fiber is increasingly popular in leisure boating due to the rising consumer preference for sleek, high-performance vessels with top-tier speed, fuel economy, and aesthetic appeal. Carbon fiber hulls are particularly well-suited for high-end sailboats and yachts, offering lightweight construction and exceptional durability. This trend is being propelled by the growing number of high-net-worth individuals seeking customized, performance-driven marine experiences.

The U.S. Carbon Fiber Boat Hulls Market alone was valued at USD 410 million in 2024. The U.S. government is proposing a revision of the NAICS classification to include a more specific category for fiber-reinforced composite boat building-reflecting the sector's rising economic significance. This move is expected to enhance regulatory clarity, data tracking, and targeted investments across the industry. The demand for carbon fiber boat hulls is rising across all regions, driven by the need for lightweight, high-performance vessels that support fuel efficiency and environmental compliance.

Leading players in the global carbon fiber boat hulls market include Durham Boat, North Sea Boats, DCB Performance Boats, Scout Boats, and SAERTEX Stade. These companies are adopting cutting-edge technologies to engineer next-level carbon fiber composites that offer greater strength, reduced weight, and improved durability. Their focus is to meet the rising demand for luxury and performance-driven watercraft that deliver speed, fuel savings, and reduced maintenance in even the harshest marine conditions.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope & definition

- 1.2 Base estimates & calculations

- 1.3 Forecast calculation

- 1.4 Data sources

- 1.4.1 Primary

- 1.4.2 Secondary

- 1.4.2.1 Paid sources

- 1.4.2.2 Public sources

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.5.2 Data mining sources

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Factor affecting the value chain

- 3.1.2 Profit margin analysis

- 3.1.3 Disruptions

- 3.1.4 Future outlook

- 3.1.5 Manufacturers

- 3.1.6 Distributors

- 3.2 Supplier landscape

- 3.3 Profit margin analysis

- 3.4 Key news & initiatives

- 3.5 Regulatory landscape

- 3.6 Impact forces

- 3.6.1 Growth drivers

- 3.6.1.1 Rising demand for lightweight and fuel-efficient vessels

- 3.6.1.2 Advancements in carbon fiber manufacturing and composites technology

- 3.6.2 Industry pitfalls & challenges

- 3.6.2.1 Recycling and environmental concerns

- 3.6.2.2 High material and production costs

- 3.6.1 Growth drivers

- 3.7 Impact of trump administration tariffs – structured overview

- 3.7.1 Impact on trade

- 3.7.1.1 Trade volume disruptions

- 3.7.1.2 Retaliatory measures

- 3.7.2 Impact on the industry

- 3.7.2.1 Supply-side impact (raw materials)

- 3.7.2.2 Price volatility in key materials

- 3.7.2.3 Supply chain restructuring

- 3.7.2.4 Production cost implications

- 3.7.2.5 Demand-side impact (selling price)

- 3.7.2.6 Price transmission to end markets

- 3.7.2.7 Market share dynamics

- 3.7.2.8 Consumer response patterns

- 3.7.3 Key companies impacted

- 3.7.4 Strategic industry responses

- 3.7.4.1 Supply chain reconfiguration

- 3.7.4.2 Pricing and product strategies

- 3.7.4.3 Policy engagement

- 3.7.1 Impact on trade

- 3.8 Outlook and future considerations

- 1.1 Growth potential analysis

- 1.2 Porter's analysis

- 1.3 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 1.4 Introduction

- 1.5 Company market share analysis

- 1.6 Competitive positioning matrix

- 1.7 Strategic outlook matrix

Chapter 5 Market Estimates and Forecast, By Boat Type, 2021 - 2034 (USD Billion) (Kilo Tons)

- 1.8 Key trends

- 1.9 Sailboats

- 1.10 Yachts

- 1.11 Fishing boats

- 1.12 Military boats

- 1.13 Rescue boats

- 1.14 Others

Chapter 6 Market Estimates and Forecast, By Hull Type, 2021 - 2034 (USD Billion) (Kilo Tons)

- 1.15 Key trends

- 1.16 Monohull

- 1.17 Multihull

- 1.18 Planing hull

- 1.19 Displacement hull

- 1.20 Semi-displacement hull

- 1.21 Others

Chapter 7 Market Estimates and Forecast, By Application, 2021 - 2034 (USD Billion) (Kilo Tons)

- 1.22 Key trends

- 1.23 Recreational

- 1.24 Commercial

- 1.25 Military & defense

- 1.26 Others

Chapter 8 Market Estimates and Forecast, By Region, 2021 - 2034 (USD Billion) (Kilo Tons)

- 1.27 Key trends

- 1.28 North America

- 1.28.1 U.S.

- 1.28.2 Canada

- 1.29 Europe

- 1.29.1 Germany

- 1.29.2 UK

- 1.29.3 France

- 1.29.4 Spain

- 1.29.5 Italy

- 1.29.6 Netherlands

- 1.30 Asia Pacific

- 1.30.1 China

- 1.30.2 India

- 1.30.3 Japan

- 1.30.4 Australia

- 1.30.5 South Korea

- 1.31 Latin America

- 1.31.1 Brazil

- 1.31.2 Mexico

- 1.32 Middle East and Africa

- 1.32.1 Saudi Arabia

- 1.32.2 South Africa

- 1.32.3 UAE

Chapter 9 Company Profiles

- 9.1 Arrow Shark RC

- 9.2 Carbon

- 9.3 DCB Performance Boat

- 9.4 Durham Boat

- 9.5 Ghostworks Marine

- 9.6 North Sea Boats

- 9.7 Oxean Marine

- 9.8 SAERTEX Stade

- 9.9 Scout Boats

- 9.10 TFL North America