航空機用センサーの市場機会、成長促進要因、産業動向分析、2025年~2034年予測

Aircraft Sensors Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034- 発行日

- ページ情報

- 英文 192 Pages

- 納期

- 2~3営業日

- 商品コード

- 1740760

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

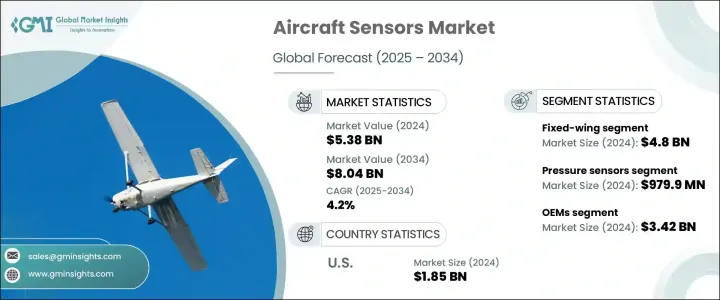

航空機用センサーの世界市場規模は、2024年に53億8,000万米ドルとなり、CAGR 4.2%で成長し、2034年には80億4,000万米ドルに達すると予測されています。

この市場拡大の大きな原動力となっているのは、航空業界が燃費効率向上にますます注力するようになっていることであり、その結果、革新的で信頼性の高いセンサー技術に対する需要が高まっています。これらのセンサーは、航空機の性能を最適化し、安全性を高め、民間航空と軍事航空の両方で使用される高度なシステムをサポートする上で重要な役割を果たしています。しかし、地政学的な緊張や、航空機センサー部品への関税を含む貿易制限により、サプライチェーンに大きな混乱が生じています。こうした混乱は、多くのセンサーメーカーの製造コストを押し上げ、利益率を圧迫するとともに、航空機納入の遅れにつながっています。

ここ数年に課された関税は特に北米のメーカーに影響を与え、一部の企業は国内での操業の縮小を余儀なくされました。一方、欧州のサプライヤーはサプライチェーンの見直しと再構築を余儀なくされ、短期的な非効率を生み出しました。他方、アジアの製造業は輸入品への依存度を下げるために現地生産能力を開発し、生産の地域化に向けた世界的動向を示唆しました。再調達はサプライチェーンの一部安定化に役立ったが、市場全体では、特定のセンサー技術、特に無人システムで使用されるセンサーの取り込みが鈍化しました。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 53億8,000万米ドル |

| 予測金額 | 80億4,000万米ドル |

| CAGR | 4.2% |

一方、無人航空機(UAV)や電動垂直離着陸機(eVTOL)などの急成長分野では、センサー需要が急増しています。これらのプラットフォームでは、ナビゲーション、障害物回避、操作の安全性のために高度に専門化されたセンサーが必要とされます。これらの技術が普及するにつれ、特に都市部や商業利用事例では、超高信頼性とエネルギー効率に優れたセンサーの必要性が高まり続けると思われます。さらに、自動化レベルの向上と人工知能の統合により、メーカーは自律機能やリアルタイムの意思決定をサポートできる、より洗練されたセンサーシステムの開発を進めています。

もう一つの大きな成長要因は、航空会社や整備業者による予知保全プログラムの実施にあります。これらのプログラムは、IoT対応センサーに依存して航空機システムをリアルタイムで監視し、摩耗や損傷の兆候を早期に検出します。このアプローチにより、予期せぬメンテナンスイベントが大幅に減少し、航空機の耐用年数が延びる。振動、音響、腐食を測定するセンサーは、古い機体の監視に特に有効です。これらの技術は、事後保全から事前保全への移行を可能にし、アフターマーケット分野の需要を押し上げています。

一方、防衛予算は世界的に増加の一途をたどっており、次世代航空機に適した頑丈で高性能なセンサーの需要に拍車をかけています。軍用機は、レーダー、電子戦、赤外線画像センサーなど、過酷な条件下で作動しなければならない先端技術に依存しています。ステルス技術やドローン能力への投資の増加は、防衛分野におけるセンサーの技術革新を加速させており、広範な航空機用センサー市場の中で最も急成長している分野の一つとなっています。

競争力を維持するために、メーカーは燃費の良い航空機や自律型プラットフォームに合わせた軽量でエネルギー効率の良いセンサー技術の研究開発を優先しています。MEMSとLiDARベースのシステム開発は、各社がUAVと自動飛行のニーズを満たすことを目指し、勢いを増しています。AIを搭載したIoTセンサーを使った予知保全能力の強化も、特に運用寿命が終わりに近づいている航空機にとっては中心的な焦点になりつつあります。

2024年には、固定翼航空機センサーセグメントが市場全体の48億米ドルを占めました。これらの航空機は、商業用と軍事用の両方で幅広く使用されているため、世界の需要の大半を占めています。このカテゴリーのセンサーは、飛行制御、エンジン監視、燃料管理に不可欠です。より技術的に進んだ航空機の導入に伴い、軽量でデータ駆動型のセンサーの採用が加速しています。さらに、監視や軍事作戦における高耐久性UAVの使用の増加により、高性能センサーシステムの必要性がさらに高まっています。

機内圧力、エンジン性能、油圧システムの完全性維持に不可欠な圧力センサーは、センサータイプ別で最大のシェアを占め、2024年の評価額は9億7,990万米ドルでした。これらのセンサーは、あらゆるタイプの航空機に幅広く適用されるため、航空業界では定番となっています。技術の進歩により、これらのコンポーネントは小型化、耐久性、電力効率が向上し、最新の航空機システムにおける役割の拡大に寄与しています。

エンドユーザー別では、2024年にはOEMセグメントが34億2,000万米ドルで市場をリードしました。これらのOEMメーカーは、新たに開発された航空機システムに高信頼性センサーを組み込む役割を担っています。彼らは、エンジン診断、アビオニクス、高度な飛行制御センサーに重点を置いています。しかし、認証の遅れや原材料の不足といった課題は、彼らの業務効率に影響を与え続けています。

地域別では、米国が2024年に18億5,000万米ドルの評価額で航空機用センサー市場を独占しました。同国は、強固な製造能力と多額の防衛投資によって航空宇宙技術革新をリードしており、最先端センサーの旺盛な需要を確実なものにしています。規制の枠組みも、安全性と予知保全技術の継続的改善を促し、市場全体の成長に寄与しています。

競合情勢は依然として激しく、主要企業は合計で48.5%の市場シェアを占めています。これらの企業は、AIを強化し、カスタマイズ可能で環境に優しいセンサーソリューションの開発に資源を投入し、市場の需要と進化する規制基準の両方に対応しています。これらの企業の戦略には、アライアンスの形成、デジタル製造プロセスの採用、製品ラインの多様化などが含まれ、従来のジェット機から新興の自律型航空機システムまで、さまざまな航空機プラットフォームをサポートしています。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- トランプ政権の関税分析

- 貿易への影響

- 貿易量の混乱

- 報復措置

- 業界への影響

- 供給側の影響

- 価格変動

- サプライチェーンの再構築

- 生産コストへの影響

- 需要側の影響

- 最終市場への価格伝達

- 市場シェアの動向

- 消費者の反応パターン

- 供給側の影響

- 影響を受ける主要企業

- 戦略的な業界対応

- サプライチェーンの再構成

- 価格設定と製品戦略

- 政策関与

- 展望と今後の検討事項

- 貿易への影響

- 業界への影響要因

- 促進要因

- 燃費効率の高い航空機の需要増加

- 無人航空機(UAV)とeVTOLの成長

- 予測保守の導入増加

- 軍事近代化と宇宙探査

- 業界の潜在的リスク&課題

- 高い研究開発費

- 厳格な認証の遅延

- 促進要因

- 成長可能性分析

- 規制情勢

- テクノロジーの情勢

- 将来の市場動向

- ギャップ分析

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 主要市場企業の競合分析

- 競合ポジショニングマトリックス

- 戦略ダッシュボード

第5章 市場推計・予測:機種別、2021-2034

- 主要動向

- 固定翼

- 回転翼

第6章 市場推計・予測:センサータイプ別、2021-2034

- 主要動向

- 圧力センサー

- 温度センサー

- 力センサー

- トルクセンサー

- 速度センサー

- 位置・変位センサー

- レベルセンサー

- 近接センサー

- フローセンサー

- 光学センサー

- モーションセンサー

- レーダーセンサー

- GPSセンサー

- その他

第7章 市場推計・予測:最終用途別、2021-2034

- 主要動向

- OEM

- アフターマーケット

- 防衛・宇宙機関

第8章 市場推計・予測:地域別、2021 –2034

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- スペイン

- イタリア

- オランダ

- アジア太平洋地域

- 中国

- インド

- 日本

- オーストラリア

- 韓国

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- サウジアラビア

- 南アフリカ

- アラブ首長国連邦

第9章 企業プロファイル

- Honeywell International Inc.

- Safran S.A.

- Thales

- TE Connectivity

- Collins Aerospace

- RTX

- Meggitt PLC.

- AMETEK.Inc.

- Curtiss-Wright Corporation

- L3Harris Technologies、Inc.

- Saywell International

- Garmin Ltd.

- HBK、Inc

- PCB Piezotronics

- Kistler Group

- Bosch Sensortec GmbH

- Eaton

- Baker Hughes Company

- Humanetics

目次

The Global Aircraft Sensors Market was valued at USD 5.38 billion in 2024 and is estimated to grow at a CAGR of 4.2% to reach USD 8.04 billion by 2034. A major force behind this expansion is the aviation industry's increasing focus on improving fuel efficiency, which has led to higher demand for innovative and reliable sensor technologies. These sensors play a critical role in optimizing aircraft performance, enhancing safety, and supporting advanced systems used in both commercial and military aviation. However, geopolitical tensions and trade restrictions, including tariffs on aircraft sensor components, have caused significant supply chain disruptions. These disruptions have driven up manufacturing costs and strained profit margins for many sensor producers, while also leading to delays in aircraft deliveries.

Tariffs imposed in recent years particularly impacted North American manufacturers, prompting some companies to shift operations back domestically. Meanwhile, European suppliers were forced to reevaluate and restructure their supply chains, creating short-term inefficiencies. On the other hand, manufacturers in Asia developed local capabilities to reduce reliance on imports, signaling a global trend toward regionalizing production. Although reshoring helped stabilize some aspects of the supply chain, the overall market experienced slower uptake in certain sensor technologies, especially those used in unmanned systems.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $5.38 Billion |

| Forecast Value | $8.04 Billion |

| CAGR | 4.2% |

In contrast, demand for sensors has surged in rapidly growing segments such as unmanned aerial vehicles (UAVs) and electric vertical takeoff and landing (eVTOL) aircraft. These platforms require highly specialized sensors for navigation, obstacle avoidance, and operational safety. As these technologies become more prevalent, particularly in urban and commercial use cases, the need for ultra-reliable and energy-efficient sensors will continue to rise. Furthermore, increasing levels of automation and integration of artificial intelligence are pushing manufacturers to develop more sophisticated sensor systems that can support autonomous functions and real-time decision-making.

Another major growth driver lies in the implementation of predictive maintenance programs by airlines and maintenance providers. These programs rely on IoT-enabled sensors to monitor aircraft systems in real time, detecting early signs of wear and tear. This approach significantly reduces unexpected maintenance events and extends aircraft service life. Sensors that measure vibration, sound, and corrosion are particularly useful in monitoring older fleets. These technologies are enabling a shift from reactive to proactive maintenance, boosting demand in the aftermarket segment.

Meanwhile, defense budgets worldwide continue to rise, fueling demand for rugged, high-performance sensors suitable for next-generation aircraft. Military aircraft depend on advanced technologies such as radar, electronic warfare, and thermal imaging sensors that must operate in extreme conditions. Increased investments in stealth technologies and drone capabilities are accelerating sensor innovation in the defense sector, making it one of the fastest-growing areas within the broader aircraft sensors market.

To maintain competitiveness, manufacturers are prioritizing research and development in lightweight, energy-efficient sensor technologies tailored for fuel-efficient aircraft and autonomous platforms. The development of MEMS and LiDAR-based systems is gaining momentum as companies aim to meet the needs of UAVs and automated flight. Enhancing predictive maintenance capabilities using AI-powered IoT sensors is also becoming a central focus, especially for fleets approaching the end of their operational lifespan.

In 2024, the fixed-wing aircraft sensor segment accounted for USD 4.8 billion of the total market value. These aircraft dominate global demand due to their extensive use across both commercial and military applications. Sensors in this category are essential for flight control, engine monitoring, and fuel management. With the introduction of more technologically advanced aircraft, the adoption of lightweight, data-driven sensors has accelerated. Additionally, the growing use of high-endurance UAVs in surveillance and military operations has further amplified the need for high-performance sensor systems.

Pressure sensors, which are vital for maintaining cabin pressure, engine performance, and hydraulic system integrity, represented the largest share by sensor type with a valuation of USD 979.9 million in 2024. These sensors are a staple in aviation due to their wide application across all aircraft types. Technological advancements have made these components smaller, more durable, and more power-efficient, contributing to their expanding role in modern aircraft systems.

On the end-user front, the OEM segment led the market in 2024 with a value of USD 3.42 billion. These original equipment manufacturers are responsible for integrating high-reliability sensors into newly developed aircraft systems. They focus on engine diagnostics, avionics, and advanced flight control sensors. However, challenges such as certification delays and raw material shortages continue to impact their operational efficiency.

Regionally, the United States dominated the aircraft sensors market with a valuation of USD 1.85 billion in 2024. The country's leadership in aerospace innovation, driven by robust manufacturing capabilities and significant defense investments, ensures strong demand for cutting-edge sensors. Regulatory frameworks also encourage continuous improvement in safety and predictive maintenance technologies, contributing to overall market growth.

The competitive landscape remains intense, with leading companies holding a combined 48.5% market share. These firms are channeling resources into developing AI-enhanced, customizable, and eco-friendly sensor solutions, aligning with both market demand and evolving regulatory standards. Their strategies include forming alliances, adopting digital manufacturing processes, and diversifying their product lines to support various aircraft platforms, from traditional jets to emerging autonomous aerial systems.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Base estimates and calculations

- 1.3.1 Base year calculation

- 1.3.2 Key trends for market estimation

- 1.4 Forecast model

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.5.2 Data mining sources

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Trump administration tariffs analysis

- 3.2.1 Impact on trade

- 3.2.1.1 Trade volume disruptions

- 3.2.1.2 Retaliatory measures

- 3.2.2 Impact on the industry

- 3.2.2.1 Supply-side impact

- 3.2.2.1.1 Price volatility

- 3.2.2.1.2 Supply chain restructuring

- 3.2.2.1.3 Production cost implications

- 3.2.2.2 Demand-side impact

- 3.2.2.2.1 Price transmission to end markets

- 3.2.2.2.2 Market share dynamics

- 3.2.2.2.3 Consumer response patterns

- 3.2.2.1 Supply-side impact

- 3.2.3 Key companies impacted

- 3.2.4 Strategic industry responses

- 3.2.4.1 Supply chain reconfiguration

- 3.2.4.2 Pricing and product strategies

- 3.2.4.3 Policy engagement

- 3.2.5 Outlook and future considerations

- 3.2.1 Impact on trade

- 3.3 Industry impact forces

- 3.3.1 Growth drivers

- 3.3.1.1 Increasing demand for fuel-efficient aircraft

- 3.3.1.2 Growth of unmanned aerial vehicles (UAVs) and eVTOLs

- 3.3.1.3 Rising adoption of predictive maintenance

- 3.3.1.4 Military modernization and space exploration

- 3.3.2 Industry pitfalls and challenges

- 3.3.2.1 High R&D costs

- 3.3.2.2 Stringent certification delays

- 3.3.1 Growth drivers

- 3.4 Growth potential analysis

- 3.5 Regulatory landscape

- 3.6 Technology landscape

- 3.7 Future market trends

- 3.8 Gap analysis

- 3.9 Porter's analysis

- 3.10 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategy dashboard

Chapter 5 Market Estimates & Forecast, By Aircraft Type, 2021-2034 (USD Million & Thousand Units)

- 5.1 Key trends

- 5.2 Fixed-wing

- 5.3 Rotary-wing

Chapter 6 Market Estimates & Forecast, By Sensor Type, 2021-2034 (USD Million & Thousand Units)

- 6.1 Key trends

- 6.2 Pressure sensors

- 6.3 Temperature sensors

- 6.4 Force sensors

- 6.5 Torque sensors

- 6.6 Speed sensors

- 6.7 Position & displacement sensors

- 6.8 Level sensors

- 6.9 Proximity sensors

- 6.10 Flow sensors

- 6.11 Optical sensors

- 6.12 Motion sensors

- 6.13 Radar sensors

- 6.14 Gps sensors

- 6.15 Others

Chapter 7 Market Estimates & Forecast, By End Use, 2021-2034 (USD Million & Thousand Units)

- 7.1 Key trends

- 7.2 OEMs

- 7.3 Aftermarket

- 7.4 Defense & space agencies

Chapter 8 Market Estimates and Forecast, By Region, 2021 – 2034 (USD Million & Thousand Units)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Netherlands

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.6 Middle East and Africa

- 8.6.1 Saudi Arabia

- 8.6.2 South Africa

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 Honeywell International Inc.

- 9.2 Safran S.A.

- 9.3 Thales

- 9.4 TE Connectivity

- 9.5 Collins Aerospace

- 9.6 RTX

- 9.7 Meggitt PLC.

- 9.8 AMETEK.Inc.

- 9.9 Curtiss-Wright Corporation

- 9.10 L3Harris Technologies, Inc.

- 9.11 Saywell International

- 9.12 Garmin Ltd.

- 9.13 HBK, Inc

- 9.14 PCB Piezotronics

- 9.15 Kistler Group

- 9.16 Bosch Sensortec GmbH

- 9.17 Eaton

- 9.18 Baker Hughes Company

- 9.19 Humanetics

- 発行日

- 発行

- Global Market Insights Inc.

- ページ情報

- 英文 192 Pages

- 納期

- 2~3営業日