ハイブリッドEスクーターの市場機会、成長促進要因、産業動向分析、2025年~2034年予測

Hybrid E-Scooter Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034- 発行日

- ページ情報

- 英文 170 Pages

- 納期

- 2~3営業日

- 商品コード

- 1740754

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

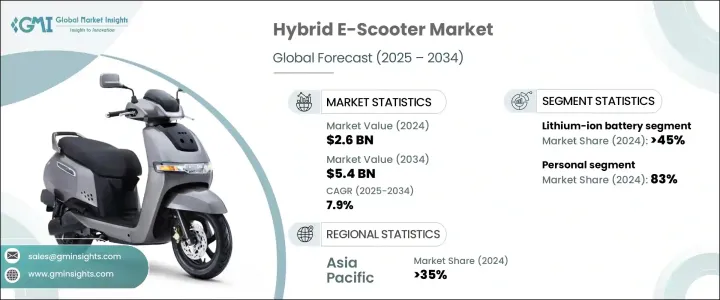

ハイブリッドEスクーターの世界市場規模は、2024年には26億米ドルとなり、バッテリー技術の進歩、モーター効率の向上、環境意識の高まりを背景に、CAGR 7.9%で成長し、2034年には54億米ドルに達すると予測されています。

ハイブリッドEスクーター業界は、都市のモビリティが持続可能性と利便性に強く焦点を当てながら進化を続けているため、大きな勢いを増しています。都市が混雑し、燃料価格が不安定になる中、消費者は性能や航続距離に妥協しない、よりスマートで環境に優しい代替手段を積極的に探しています。電動技術と燃料技術を組み合わせたハイブリッドEスクーターは、充電インフラに完全に依存することなく長距離の移動を求める個人にとって、信頼できるソリューションとして台頭しつつあります。こうしたデュアルモードのスクーターは、都市部の通勤者、配達員、効率性、手頃な価格、二酸化炭素排出量の削減を求める日常的なユーザーに比類ない柔軟性を提供します。

クリーンな輸送手段への投資の増加と、電動モビリティに対する政府の支援の高まりが、この市場の将来を形成しています。現在、州や連邦政府の数多くの政策が、消費者やメーカーのコスト負担を軽減する税制優遇措置やインセンティブ、補助金を提供しています。同時に、官民の利害関係者は、ハイブリッドモビリティをサポートする統合充電・給油インフラを構築する取り組みを強化しています。シェアードモビリティプラットフォームの成長とラストマイルデリバリーサービスの採用拡大も、ハイブリッドEスクーターの販売を促進する上で極めて重要な役割を果たしています。この動向は、迅速かつ手頃な価格で、排ガス規制を遵守した交通手段が強く求められている、人口密度の高い都市ハブにおいて特に顕著です。ハイブリッドEスクーターは単なるライフスタイルのアップグレードではなく、よりスマートな都市モビリティを実現するための戦略的ツールになりつつあります。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 26億米ドル |

| 予測金額 | 54億米ドル |

| CAGR | 7.9% |

ハイブリッドEスクーターは、ライダーが電気モードと燃料モードをシームレスに切り替えられるようにすることで、際立った優位性を提供します。この二重機能により、航続距離の延長、充電不安の軽減、交通量の多いゾーンでのスムーズな乗車体験が保証されます。都市部のライダーやギグエコノミーで働く人々は、メンテナンスが簡単でありながら高性能な乗り物を必要としているため、こうした利点に特に惹かれています。リチウムイオンバッテリーの使用が増加していることも、需要に拍車をかけています。エネルギー密度が高く、充電時間が短く、寿命が長いことで知られるこのバッテリーは、ハイブリッドスクーターの実用性を大幅に向上させる。軽量でコンパクトな設計は、操作性を向上させ、エネルギー効率を高め、現代の通勤者のニーズに完全に合致しています。

環境への配慮も成長の重要な原動力です。大気の質が悪化し、気候変動が激化する中、世界各国の政府は自動車公害を抑制するため、排出ガス規制を強化しています。ハイブリッドEスクーターは、ガソリンのみのスクーターに比べて排出ガスが大幅に少なく、環境意識の高い消費者の間で急速に普及しつつあります。これらのスクーターは、航続距離やパワーを犠牲にすることなく、よりクリーンな交通手段への需要を満たすものであり、高排出ガス車の規制を強化している地域では魅力的なソリューションとなっています。消費者は、短距離から中距離の移動において、費用対効果が高く環境に優しい選択肢としてハイブリッドEスクーターを選ぶようになってきています。

市場は主にバッテリーの種類によって区分され、2024年にはリチウムイオンバッテリーが主導権を握り、10億米ドルの収益を生み出します。これらのバッテリーは、エネルギー効率、耐久性、安定した性能を発揮する能力で支持されています。リチウムイオンバッテリーは、より小型で軽量なユニットに多くの電力を詰め込むことができるため、全体的な航続距離を伸ばし、車両重量を減らすことができます。

最終用途別では、個人用ハイブリッドEスクーターが2024年に83%のシェアを占め、市場を独占しました。都市化が進み、柔軟な通勤手段に対する需要が高まっているため、消費者は費用効率が高く、低排出ガスである個人用交通手段を求めています。これらのスクーターは、短距離は電動で、長距離は燃料でアシストしてくれるため、毎日の都市移動に理想的です。従来のスクーターや自動車に比べて燃料費や維持費が安いため、予算に敏感な消費者は特にスクーターに魅力を感じています。

アジア太平洋のハイブリッドEスクーター市場は2024年に35%のシェアを占めたが、これは同地域の二輪車への依存度の高さと人口密度の高い都市部のおかげです。交通渋滞が増加し、駐車可能な場所が限られているため、ハイブリッドEスクーターは非常に実用的で環境に優しい代替交通手段となっています。特に中国は、その強力な現地生産能力、強固なサプライチェーン、有利な政府規制により、業界をリードし続けています。

Yadea Group、Yamaha、Kymco、NIU Technologiesなどの主要企業は、製品革新に多額の投資を行い、生産ラインを拡大し、販売チャネルを強化しています。これらの企業は、消費者の高まる期待に応えるべく、エネルギー効率が高く、高度な機能を備えたユーザー中心のスクーターの開発に注力しています。世界市場での存在感を高め、競合情勢で優位に立つためには、現地の流通業者や国際的なサプライヤーとの戦略的提携が不可欠です。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- サプライヤーの情勢

- 原材料サプライヤー

- 部品サプライヤー

- テクノロジープロバイダー

- 最終用途

- 利益率分析

- トランプ政権による関税への影響

- 貿易への影響

- 貿易量の混乱

- 報復措置

- 業界への影響

- 供給側の影響(原材料)

- 主要原材料の価格変動

- サプライチェーンの再構築

- 生産コストへの影響

- 需要側の影響(販売価格)

- 最終市場への価格伝達

- 市場シェアの動向

- 消費者の反応パターン

- 供給側の影響(原材料)

- 影響を受ける主要企業

- 戦略的な業界対応

- サプライチェーンの再構成

- 価格設定と製品戦略

- 政策関与

- 展望と今後の検討事項

- 貿易への影響

- テクノロジーとイノベーションの情勢

- 特許分析

- 価格分析

- 地域

- バッテリー

- 主なニュースと取り組み

- 規制情勢

- 影響要因

- 促進要因

- 配送・物流における商用利用

- 航続距離の不安とインフラのギャップ

- 環境規制と排出基準

- バッテリーとモーターの効率における技術的進歩

- 業界の潜在的リスク&課題

- 初期コストが高め

- メンテナンスの問題

- 促進要因

- 成長可能性分析

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 競合ポジショニングマトリックス

- 戦略的展望マトリックス

第5章 市場推計・予測:バッテリー別、2021-2034

- 主要動向

- リチウムイオン電池

- 鉛蓄電池

- ニッケル水素

- 全固体電池

第6章 市場推計・予測:距離別、2021-2034

- 主要動向

- 短距離(15~30 km)

- 中距離(31~60 km)

- 長距離(60 km以上)

第7章 市場推計・予測:販売チャネル別、2021-2034

- 主要動向

- オンライン

- オフライン

第8章 市場推計・予測:最終用途別、2021-2034

- 主要動向

- 個人用

- 商業用

第9章 市場推計・予測:地域別、2021-2034

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- 英国

- ドイツ

- フランス

- イタリア

- スペイン

- ロシア

- 北欧諸国

- アジア太平洋地域

- 中国

- インド

- 日本

- オーストラリア

- 韓国

- 東南アジア

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- アラブ首長国連邦

- 南アフリカ

- サウジアラビア

第10章 企業プロファイル

- Gogoro

- Green Tiger Mobility

- Honda

- Jiangsu Xinri E-Vehicle

- Kymco

- Meladath Auto Components

- NIU Technologies

- Okinawa Autotech

- Piaggio Group

- Sanyang Motor

- Silence Urban Ecomobility

- Sunra Electric Vehicle

- Verge Motors

- Yadea Group

- Yamaha

- Zhejiang Luyuan Electric Vehicle

目次

The Global Hybrid E-Scooter Market was valued at USD 2.6 billion in 2024 and is estimated to grow at a CAGR of 7.9% to reach USD 5.4 billion by 2034, driven by advancements in battery technology, improved motor efficiency, and rising environmental awareness. The hybrid e-scooter industry is gaining significant momentum as urban mobility continues to evolve with a strong focus on sustainability and convenience. With cities becoming more congested and fuel prices remaining volatile, consumers are actively looking for smarter, greener alternatives that do not compromise on performance or range. Hybrid e-scooters, which combine electric and fuel-powered technologies, are emerging as a reliable solution for individuals seeking extended travel distances without being entirely dependent on charging infrastructure. These dual-mode scooters provide unmatched flexibility for urban commuters, delivery personnel, and everyday users who demand efficiency, affordability, and a lower carbon footprint.

Rising investments in clean transportation, coupled with growing government support for electric mobility, are shaping the future of this market. Numerous state and federal policies now offer tax rebates, incentives, and subsidies that reduce the cost burden for consumers and manufacturers alike. At the same time, public and private stakeholders are ramping up efforts to create integrated charging and refueling infrastructure to support hybrid mobility. The growth of shared mobility platforms and the increasing adoption of last-mile delivery services have also played a pivotal role in driving hybrid e-scooter sales. This trend is particularly noticeable in densely populated urban hubs where quick, affordable, and emission-compliant transport is in high demand. Hybrid e-scooters are not just a lifestyle upgrade-they're fast becoming a strategic tool for achieving smarter urban mobility.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $2.6 Billion |

| Forecast Value | $5.4 Billion |

| CAGR | 7.9% |

Hybrid e-scooters offer a distinct edge by allowing riders to switch seamlessly between electric and fuel modes. This dual functionality ensures a longer range, reduced charging anxiety, and a smoother riding experience in traffic-heavy zones. Urban riders and gig economy workers are especially drawn to these benefits, as they need vehicles that are low-maintenance yet high-performing. The rising use of lithium-ion batteries has further fueled the demand. Known for their higher energy density, faster charging time, and extended lifespan, these batteries significantly enhance the practicality of hybrid scooters. Their lightweight and compact design improves handling and boosts energy efficiency, aligning perfectly with the needs of modern-day commuters.

Environmental concerns are another key growth driver. As air quality worsens and climate change intensifies, governments worldwide are enforcing stricter emission norms to curb vehicular pollution. Hybrid e-scooters, which emit significantly less than their gasoline-only counterparts, are quickly becoming the go-to option for eco-conscious consumers. These scooters meet the demand for cleaner transport without compromising on range or power, making them an attractive solution in regions that are clamping down on high-emission vehicles. Consumers are increasingly choosing hybrid e-scooters as a cost-effective and environmentally friendly alternative for short to mid-range travel.

The market is primarily segmented by battery type, with lithium-ion batteries taking the lead in 2024, generating USD 1 billion in revenue. These batteries are favored for their energy efficiency, durability, and ability to deliver consistent performance. They pack more power into a smaller, lighter unit, helping boost the overall range and reducing the vehicle's weight, which in turn improves fuel efficiency and maneuverability-critical features for urban use.

By end-use, personal hybrid e-scooters dominated the market with an 83% share in 2024. Urbanization and rising demand for flexible commuting options are pushing consumers toward personal transport solutions that are both cost-efficient and low-emission. These scooters offer electric riding for short distances and fuel-powered assistance for longer routes, making them ideal for daily city travel. Budget-conscious consumers are especially drawn to them due to their lower fuel and maintenance costs compared to traditional scooters or cars.

The Asia Pacific Hybrid E-Scooter Market accounted for 35% share in 2024, thanks to the region's heavy reliance on two-wheelers and its densely populated urban centers. With increasing traffic congestion and limited parking availability, hybrid e-scooters present a highly practical and eco-friendly transport alternative. China, in particular, continues to lead the way due to its strong local manufacturing capabilities, robust supply chain, and favorable government regulations.

Key players such as Yadea Group, Yamaha, Kymco, and NIU Technologies are investing heavily in product innovation, expanding their production lines, and strengthening distribution channels. These companies focus on creating energy-efficient, user-centric scooters with advanced features, aiming to meet rising consumer expectations. Strategic partnerships with both local distributors and international suppliers are central to boosting their global market presence and staying ahead in the competitive landscape.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.1.1 Research approach

- 1.1.2 Data collection methods

- 1.2 Base estimates & calculations

- 1.2.1 Base year calculation

- 1.2.2 Key trends for market estimation

- 1.3 Forecast model

- 1.4 Primary research and validation

- 1.4.1 Primary sources

- 1.4.2 Data mining sources

- 1.5 Market scope & definition

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Supplier landscape

- 3.2.1 Raw material suppliers

- 3.2.2 Component suppliers

- 3.2.3 Technology providers

- 3.2.4 End-use

- 3.3 Profit margin analysis

- 3.4 Impact of Trump administration tariffs

- 3.4.1 Impact on trade

- 3.4.1.1 Trade volume disruptions

- 3.4.1.2 Retaliatory measures

- 3.4.2 Impact on industry

- 3.4.2.1 Supply-side impact (raw materials)

- 3.4.2.1.1 Price volatility in key materials

- 3.4.2.1.2 Supply chain restructuring

- 3.4.2.1.3 Production cost implications

- 3.4.2.2 Demand-side impact (selling price)

- 3.4.2.2.1 Price transmission to end markets

- 3.4.2.2.2 Market share dynamics

- 3.4.2.2.3 Consumer response patterns

- 3.4.2.1 Supply-side impact (raw materials)

- 3.4.3 Key companies impacted

- 3.4.4 Strategic industry responses

- 3.4.4.1 Supply chain reconfiguration

- 3.4.4.2 Pricing and product strategies

- 3.4.4.3 Policy engagement

- 3.4.5 Outlook & future considerations

- 3.4.1 Impact on trade

- 3.5 Technology & innovation landscape

- 3.6 Patent analysis

- 3.7 Pricing analysis

- 3.7.1 Region

- 3.7.2 Battery

- 3.8 Key news & initiatives

- 3.9 Regulatory landscape

- 3.10 Impact forces

- 3.10.1 Growth drivers

- 3.10.1.1 Commercial use in delivery & logistics

- 3.10.1.2 Range anxiety & infrastructure gaps

- 3.10.1.3 Environmental regulations & emission norms

- 3.10.1.4 Technological advancements in battery and motor efficiency

- 3.10.2 Industry pitfalls & challenges

- 3.10.2.1 High initial cost

- 3.10.2.2 Maintenance issues

- 3.10.1 Growth drivers

- 3.11 Growth potential analysis

- 3.12 Porter's analysis

- 3.13 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Battery, 2021 - 2034 ($Bn, Units)

- 5.1 Key trends

- 5.2 Lithium-ion battery

- 5.3 Lead-acid batter

- 5.4 Nickel-metal hydride

- 5.5 Solid-state battery

Chapter 6 Market Estimates & Forecast, By Range Capacity, 2021 - 2034 ($Bn, Units)

- 6.1 Key trends

- 6.2 Short range (15-30 km)

- 6.3 Medium range (31-60 km)

- 6.4 Long range (above 60 km)

Chapter 7 Market Estimates & Forecast, By Sales Channel, 2021 - 2034 ($Bn, Units)

- 7.1 Key trends

- 7.2 Online

- 7.3 Offline

Chapter 8 Market Estimates & Forecast, By End Use, 2021 - 2034 ($Bn, Units)

- 8.1 Key trends

- 8.2 Personal

- 8.3 Commercial

Chapter 9 Market Estimates & Forecast, By Region, 2021 - 2034 ($Bn, Units)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 UK

- 9.3.2 Germany

- 9.3.3 France

- 9.3.4 Italy

- 9.3.5 Spain

- 9.3.6 Russia

- 9.3.7 Nordics

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.4.6 Southeast Asia

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 MEA

- 9.6.1 UAE

- 9.6.2 South Africa

- 9.6.3 Saudi Arabia

Chapter 10 Company Profiles

- 10.1 Gogoro

- 10.2 Green Tiger Mobility

- 10.3 Honda

- 10.4 Jiangsu Xinri E-Vehicle

- 10.5 Kymco

- 10.6 Meladath Auto Components

- 10.7 NIU Technologies

- 10.8 Okinawa Autotech

- 10.9 Piaggio Group

- 10.10 Sanyang Motor

- 10.11 Silence Urban Ecomobility

- 10.12 Sunra Electric Vehicle

- 10.13 Verge Motors

- 10.14 Yadea Group

- 10.15 Yamaha

- 10.16 Zhejiang Luyuan Electric Vehicle

- 発行日

- 発行

- Global Market Insights Inc.

- ページ情報

- 英文 170 Pages

- 納期

- 2~3営業日