|

市場調査レポート

商品コード

1721574

生検装置の市場機会、成長促進要因、産業動向分析、2025年~2034年予測Biopsy Devices Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| 生検装置の市場機会、成長促進要因、産業動向分析、2025年~2034年予測 |

|

出版日: 2025年04月11日

発行: Global Market Insights Inc.

ページ情報: 英文 136 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

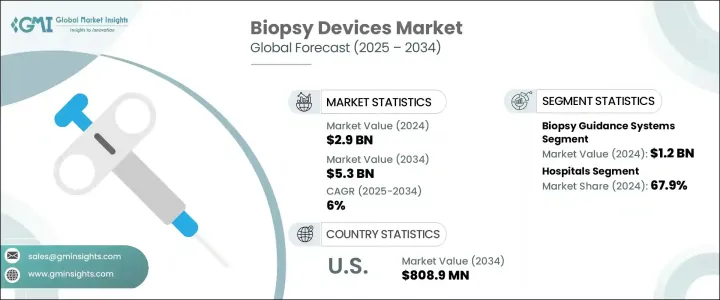

生検装置の世界市場は、2024年には29億米ドルとなり、CAGR6%で成長し、2034年には53億米ドルに達すると予測されています。

生検装置は、診断評価のための組織サンプルの抽出を可能にすることで、現代のヘルスケアにおいて重要な役割を果たしています。これらのツールは、幅広い病状の同定と分析をサポートし、しばしば悪性腫瘍の検出と確認に役立っています。慢性疾患、特にがんの世界の負担の増加は、高度な診断ソリューションの需要を押し上げています。早期発見、正確な診断、タイムリーな治療計画が重視されるようになり、生検装置の役割はこれまで以上に重要になっています。画像ガイド下および低侵襲手技への選好の高まりは、生検技術の絶え間ない革新をもたらし、精度のさらなる向上と患者の回復時間の短縮につながっています。

現在、より多くのヘルスケア専門家が、精度、使いやすさ、リアルタイムのモニタリングを提供する機器にシフトしています。病院や診断センターもこのシフトに迅速に対応しており、ワークフローの合理化と治療成績の向上に役立っています。先進診断医療に対する世界の認識とアクセスの高まりが、先進経済諸国と新興経済諸国を問わず生検装置の採用に拍車をかけています。がん診断の改善に焦点を当てた政府の取り組みやヘルスケア改革も市場拡大に寄与しています。さらに、手技件数が増加の一途をたどる中、医療提供者は現代の臨床需要に合致した効率的で患者中心の生検ソリューションに投資しています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024年 |

| 予測年 | 2025年~2034年 |

| 開始金額 | 29億米ドル |

| 予測金額 | 53億米ドル |

| CAGR | 6% |

市場は製品タイプ別に針生検ガン、生検ガイダンスシステム、生検鉗子、生検針、その他関連機器に区分されます。このうち、生検ガイダンスシステムが最大のシェアを占め、2024年には12億米ドルの売上を計上します。生検ガイダンスシステムは、リアルタイムイメージングと正確なターゲティングが可能であるため、正確性と最小限の侵襲性を必要とする手技に理想的です。これらのシステムは現在、小さい組織や到達が困難な組織の位置確認やサンプリングに効果的な可視化が不可欠な臨床ワークフローに不可欠なものと見なされています。異なる画像モダリティ間の互換性が強化された生検ガイダンスシステムは、ヘルスケア専門家が手技ミスを減らし、患者の安全性を高めるのに役立っています。これらのツールは病院や診断センターの環境にますます組み込まれるようになってきており、その多機能性によりスループットが向上し、全体的な治療成績が最適化されてきています。

エンドユーザーの観点から、生検装置市場は病院、外来手術センター、その他の環境に分類されます。病院が支配的なユーザーセグメントとして浮上し、2024年には市場全体の収益の67.9%を占め、2034年には36億米ドルに達すると市場収益推計・予測されています。病院は、ハイエンドの画像診断機器と高度な生検技術を実施できる熟練した人材を利用できるため、引き続き採用の面でリードしています。複雑な診断症例における正確でリアルタイムの組織サンプリングの必要性が高まっているため、病院はこれらの手技に適した環境となっています。慢性疾患や高度診断に関連した入院患者の増加が、病院をより高度な生検システムへの投資に駆り立てています。さらに、このような環境ではロボット支援や低侵襲手技の利用が著しく伸びており、効率と患者満足度の両方が向上しています。病院はまた、集学的治療アプローチの中心的な拠点となりつつあり、そこでは精密な診断が基礎的な役割を担っています。

地域別では、北米が依然として世界の生検装置市場に大きく貢献しています。特に米国は力強い市場成長を示しており、生検装置の売上高は2023年の4億5,190万米ドルから2034年までには8億890万米ドルに増加すると予測されています。この成長の背景には、確立されたヘルスケアインフラ、高い手技件数、高度な診断介入をサポートする有利な保険適用があります。積極的な償還環境により、入院患者施設も外来患者施設も大きな経済的障壁なく最新の生検技術を導入することができ、複数の医療現場で広く利用されるようになっています。

競合情勢には、技術、製品革新、戦略的買収への継続的な投資を通じて牙城を維持する世界的リーダー企業が複数存在します。既存プレーヤーは、強固なポートフォリオと統合診断ソリューションへのコミットメントにより、市場のかなりの部分を占めています。その一方で、新規参入企業や中堅メーカーは、対象を絞った臨床用途に対応するコスト効率の高い専用機器に注力することで、地歩を固めつつあります。高精度かつ低侵襲の診断ツールへの関心が高まる中、生検装置業界は、現代ヘルスケアの進化する需要に合わせた継続的な進歩が期待されています。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- 業界エコシステム分析

- 業界への影響要因

- 成長促進要因

- 世界中でがんの発生率が上昇

- 生検装置における技術の進歩

- 有利な償還シナリオ

- 乳がんに関する意識の向上

- 業界の潜在的リスク・課題

- 生検後の合併症のリスク

- 熟練したヘルスケア専門家の不足

- 成長促進要因

- 成長可能性分析

- 規制情勢

- 技術的情勢

- 将来の市場動向

- ギャップ分析

- ポーターの分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 企業マトリックス分析

- 主要市場企業の競合分析

- 競合ポジショニングマトリックス

- 戦略ダッシュボード

第5章 市場推計・予測:製品タイプ別、2021年~2034年

- 主要動向

- 生検ガイダンスシステム

- マニュアル

- ロボット

- 針式生検ガン

- 真空補助生検(VAB)装置

- 細針吸引生検(FNAB)装置

- コア針生検(CNB)デバイス

- 生検針

- 使い捨て

- 再利用可能

- 生検鉗子

- 一般的な生検鉗子

- ホット生検鉗子

- その他の製品タイプ

- ブラシ

- キュレット

- パンチ

第6章 市場推計・予測:最終用途別、2021年~2034年

- 主要動向

- 病院

- 外来手術センター

- その他の用途

第7章 市場推計・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- スペイン

- イタリア

- オランダ

- アジア太平洋

- 中国

- インド

- 日本

- オーストラリア

- 韓国

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- サウジアラビア

- 南アフリカ

- アラブ首長国連邦

第8章 企業プロファイル

- Argon Medical Devices

- B. Braun Melsungen

- Becton、Dickinson、and Company

- Boston Scientific

- Cardinal Health

- Cook Group

- Devicor Medical Products

- FUJIFILM

- Hologic

- INRAD

- Medtronic

- Olympus Corporation

- Stryker Corporation

The Global Biopsy Devices Market was valued at USD 2.9 billion in 2024 and is estimated to grow at a CAGR of 6% to reach USD 5.3 billion by 2034. Biopsy devices serve a critical role in modern healthcare by allowing the extraction of tissue samples for diagnostic evaluation. These tools support the identification and analysis of a wide range of medical conditions, often being instrumental in detecting and confirming malignancies. The increasing global burden of chronic diseases, particularly cancer, is pushing the demand for advanced diagnostic solutions. With rising emphasis on early detection, accurate diagnosis, and timely treatment planning, the role of biopsy devices has become more important than ever. The growing preference for image-guided and minimally invasive procedures has led to continuous innovation in biopsy technologies, further improving accuracy and reducing patient recovery time.

More healthcare professionals are now shifting toward devices that offer precision, ease of use, and real-time monitoring. Hospitals and diagnostic centers are also adapting quickly to this shift, which is helping streamline workflows and improve outcomes. Increasing global awareness and access to advanced diagnostic care are fueling the adoption of biopsy equipment across developed and emerging economies. Government initiatives and healthcare reforms focused on improving cancer diagnostics are also contributing to market expansion. Moreover, as procedural volumes continue to rise, providers are investing in efficient, patient-centric biopsy solutions that align with modern clinical demands.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $2.9 Billion |

| Forecast Value | $5.3 Billion |

| CAGR | 6% |

The market is segmented by product type into needle-based biopsy guns, biopsy guidance systems, biopsy forceps, biopsy needles, and other associated devices. Among these, biopsy guidance systems held the largest share, generating revenue worth USD 1.2 billion in 2024. Their rising use is largely due to their ability to deliver real-time imaging and precise targeting, making them ideal for procedures requiring accuracy and minimal invasiveness. These systems are now seen as integral to clinical workflows where effective visualization is essential for locating and sampling tissues that are small or difficult to reach. With enhanced compatibility across different imaging modalities, biopsy guidance systems are helping healthcare professionals reduce procedural errors and boost patient safety. These tools are increasingly being integrated into hospital and diagnostic center environments, where their multi-functional capabilities are improving throughput and optimizing overall outcomes.

From the end-user perspective, the biopsy devices market is categorized into hospitals, ambulatory surgical centers, and other settings. Hospitals emerged as the dominant user segment, accounting for 67.9% of the overall market revenue in 2024, with projections estimating the value to reach USD 3.6 billion by 2034. Hospitals continue to lead in terms of adoption due to their access to high-end imaging equipment and skilled personnel capable of performing advanced biopsy techniques. The increasing need for accurate, real-time tissue sampling in complex diagnostic cases makes hospitals a preferred setting for these procedures. The rise in admissions related to chronic diseases and advanced diagnostics is pushing hospitals to invest in more sophisticated biopsy systems. Additionally, there has been significant growth in the use of robotic-assisted and minimally invasive procedures within these environments, improving both efficiency and patient satisfaction. Hospitals are also becoming central hubs for multidisciplinary treatment approaches, where precise diagnostics play a foundational role.

In regional terms, North America remains a leading contributor to the global biopsy devices market. The United States, in particular, has demonstrated strong market growth, with biopsy device revenue expected to rise from USD 451.9 million in 2023 to USD 808.9 million by 2034. This growth can be attributed to a well-established healthcare infrastructure, high procedural volumes, and favorable insurance coverage that supports advanced diagnostic interventions. Positive reimbursement environments enable both in-patient and out-patient facilities to adopt the latest biopsy technologies without significant financial barriers, promoting widespread use across multiple care settings.

The competitive landscape features several global leaders who maintain a stronghold through continued investments in technology, product innovation, and strategic acquisitions. Established players hold a considerable portion of the market thanks to their robust portfolios and commitment to integrated diagnostic solutions. At the same time, newer entrants and mid-tier manufacturers are gaining ground by focusing on cost-effective, specialized devices catering to targeted clinical applications. With growing interest in precision-guided, less invasive diagnostic tools, the biopsy devices industry is expected to see ongoing advancements tailored to the evolving demands of modern healthcare.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Base estimates and calculations

- 1.3.1 Base year calculation

- 1.3.2 Key trends for market estimation

- 1.4 Forecast model

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.5.2 Data mining sources

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising incidence of cancer across the globe

- 3.2.1.2 Technological advancements in biopsy devices

- 3.2.1.3 Favorable reimbursement scenario

- 3.2.1.4 Increasing awareness regarding breast cancer

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Risk of complications after biopsy

- 3.2.2.2 Dearth of skilled healthcare professionals

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.5 Technological landscape

- 3.6 Future market trends

- 3.7 Gap analysis

- 3.8 Porter’s analysis

- 3.9 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Strategy dashboard

Chapter 5 Market Estimates and Forecast, By Product Type, 2021 - 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Biopsy guidance systems

- 5.2.1 Manual

- 5.2.2 Robotic

- 5.3 Needle based biopsy guns

- 5.3.1 Vacuum-assisted biopsy (VAB) devices

- 5.3.2 Fine needle aspiration biopsy (FNAB) devices

- 5.3.3 Core needle biopsy (CNB) devices

- 5.4 Biopsy needles

- 5.4.1 Disposable

- 5.4.2 Reusable

- 5.5 Biopsy forceps

- 5.5.1 General biopsy forceps

- 5.5.2 Hot biopsy forceps

- 5.6 Other product types

- 5.6.1 Brushes

- 5.6.2 Curettes

- 5.6.3 Punches

Chapter 6 Market Estimates and Forecast, By End Use, 2021 - 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Hospitals

- 6.3 Ambulatory surgical centers

- 6.4 Other end use

Chapter 7 Market Estimates and Forecast, By Region, 2021 - 2034 ($ Mn)

- 7.1 Key trends

- 7.2 North America

- 7.2.1 U.S.

- 7.2.2 Canada

- 7.3 Europe

- 7.3.1 Germany

- 7.3.2 UK

- 7.3.3 France

- 7.3.4 Spain

- 7.3.5 Italy

- 7.3.6 Netherlands

- 7.4 Asia Pacific

- 7.4.1 China

- 7.4.2 India

- 7.4.3 Japan

- 7.4.4 Australia

- 7.4.5 South Korea

- 7.5 Latin America

- 7.5.1 Brazil

- 7.5.2 Mexico

- 7.5.3 Argentina

- 7.6 Middle East and Africa

- 7.6.1 Saudi Arabia

- 7.6.2 South Africa

- 7.6.3 UAE

Chapter 8 Company Profiles

- 8.1 Argon Medical Devices

- 8.2 B. Braun Melsungen

- 8.3 Becton, Dickinson, and Company

- 8.4 Boston Scientific

- 8.5 Cardinal Health

- 8.6 Cook Group

- 8.7 Devicor Medical Products

- 8.8 FUJIFILM

- 8.9 Hologic

- 8.10 INRAD

- 8.11 Medtronic

- 8.12 Olympus Corporation

- 8.13 Stryker Corporation