5G企業プライベートネットワーク市場の市場機会、成長促進要因、産業動向分析、2025年~2034年予測

5G Enterprise Private Network Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034- 発行日

- ページ情報

- 英文 170 Pages

- 納期

- 2~3営業日

- 商品コード

- 1721479

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

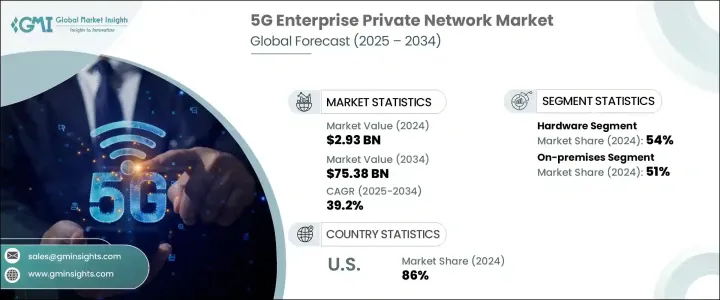

5G企業プライベートネットワークの世界市場規模は、2024年に29億3,000万米ドルとなり、CAGR 39.2%で成長し、2034年には753億8,000万米ドルに達すると予測されています。

各分野の企業は、デジタル運用の厳格な管理、セキュリティの向上、拡張性の強化を目的に、プライベート5Gネットワークの採用を増やしています。この需要の背景には、超高信頼性、低遅延通信への依存の高まりと、シームレスで高速なデータフローへのニーズがあります。プライベート5Gネットワークは、特にミッションクリティカルなアプリケーションにおいて、リアルタイムの意思決定、中断のないデータストリーミング、安全な通信を可能にすることで、企業の接続性を変革しています。

製造、物流、エネルギー、ヘルスケアなどの企業は、これらのネットワークを活用して、インテリジェント・オートメーション、産業用IoT、ロボット工学、遠隔監視システムを導入しています。デジタルトランスフォーメーションの推進は、有利な規制当局の支援や強力な研究開発イニシアティブと相まって、市場の成長をさらに加速させています。スマートシティ、コネクテッドインフラ、エッジコンピューティングへの投資が増加する中、プライベート5Gネットワークは次世代企業戦略の重要な実現要素として台頭しています。広範な5G展開やスマート技術ゾーンの創設など、デジタルインフラを支援する国家レベルの取り組みが、この状況を形成する上で極めて重要な役割を果たしています。こうした開発は、早期導入企業に競争優位性をもたらし、弾力性があり安全性の高いネットワーク・ソリューションを必要とするセクター全体のイノベーションを促進しています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 29億3,000万米ドル |

| 予測金額 | 753億8,000万米ドル |

| CAGR | 39.2% |

ハードウェアは引き続き5G企業プライベートネットワーク分野を支配しており、2024年には世界市場の54%を占め、2034年までのCAGRは39.9%と予測されます。アンテナ、ルーター、スモールセル、基地局などの高性能機器に対するニーズの高まりが、この勢いに拍車をかけています。これらのハードウェア・コンポーネントは、特に製造、ロジスティクス、防衛など、性能とセキュリティに妥協が許されない分野で、スケーラブルで安全なプライベート5Gインフラを展開するために不可欠です。企業は、スムーズで中断のない接続性を確保し、最小限の遅延と最大限の信頼性を要求する高度な使用事例に対応するため、戦略的に堅牢なハードウェアに投資しています。

オンプレミスの導入モデルは、2024年に51%のシェアを獲得して市場をリードしており、今後数年間も強力な地位を維持すると予想されます。防衛、工業製造、ヘルスケアなど、機密データを管理する企業は、制御の強化、データ保護の向上、リアルタイムのデータ管理などの理由から、オンプレミス型ネットワークを好みます。これらのネットワークは、運用の継続性、セキュリティ・リスクの低減、既存の企業システムとのシームレスな統合を可能にするカスタマイズされたインフラを提供します。オンサイトでの展開が好まれる背景には、カスタマイズや厳しい業界規制への対応に対する需要の高まりがあります。

米国は、先進的な研究エコシステム、高い自動化普及率、積極的な規制枠組みによって、2024年の世界市場で86%のシェアを占めています。同国のプライベート5Gネットワークは、エッジコンピューティングとロボティクスが不可欠になりつつある防衛、エネルギー、ヘルスケアなどの重要なセクターにおいて、安全で効率的なオペレーションを促進しています。

世界の5G企業プライベートネットワーク市場の主要企業には、クアルコム、シスコシステムズ、マイクロソフト・アジュール、アクセンチュア、IBM、エヌビディア、ファーウェイ・テクノロジーズ、AT&T、ヒューレット・パッカード・エンタープライズ(HPE)、AWS(アマゾン・ウェブ・サービス)などがあります。これらの企業は、通信事業者やクラウドサービスプロバイダーと強力なパートナーシップを結び、スケーラブルでセキュアな、業界に特化した5Gソリューションを提供しています。また、多くの企業がAIを活用した最適化ツールやエッジ・コンピューティング技術の統合に注力し、ネットワーク・パフォーマンスの向上とリアルタイム需要の充足に取り組んでいます。スマート製造、ロジスティクス、インフラ開拓などのセクター向けにカスタマイズされた製品、戦略的パイロット・プログラム、規制当局との提携は、企業が市場での足跡を強化し、世界企業全体での採用を加速するのに役立っています。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- サプライヤーの情勢

- 機器メーカー

- 通信サービスプロバイダー

- システムインテグレーター

- テクノロジープロバイダー

- エンドユーザー

- 利益率分析

- テクノロジーとイノベーションの情勢

- 特許分析

- 主なニュースと取り組み

- 規制情勢

- 影響要因

- 促進要因

- 低遅延通信の需要の高まり

- エッジコンピューティングの台頭

- データセキュリティとプライバシーのニーズの高まり

- IoTと接続デバイスの急増

- 業界の潜在的リスク&課題

- 初期導入コストが高め

- レガシーシステムとの統合の課題

- 促進要因

- 成長可能性分析

- ポーターの分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 競合ポジショニングマトリックス

- 戦略的展望マトリックス

第5章 市場推計・予測:コンポーネント別、2021-2034

- 主要動向

- ハードウェア

- 無線アクセスネットワーク(RAN)

- コアネットワーク

- エッジコンピューティングインフラストラクチャ

- ソフトウェア

- ネットワーク管理ソフトウェア

- セキュリティソフトウェア

- ネットワークスライシングソフトウェア

- 自動化およびオーケストレーションツール

- サービス

- コンサルティング

- マネージドサービス

- サポートとメンテナンス

第6章 市場推計・予測:展開モード別、2021-2034

- 主要動向

- オンプレミス

- クラウドベース

- ハイブリッド

第7章 市場推計・予測:周波数帯域別、2021-2034

- 主要動向

- サブ6GHz

- ミリ波(mmWave)

第8章 市場推計・予測:組織規模別、2021-2034

- 主要動向

- 大企業

- 中小企業

- 化学物質および危険物

第9章 市場推計・予測:最終用途別、2021-2034

- 主要動向

- 製造業

- ヘルスケア

- 運輸・物流

- 小売り

- エネルギーと公益事業

- スマートシティ

- その他

第10章 市場推計・予測:地域別、2021-2034

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- 英国

- ドイツ

- フランス

- イタリア

- スペイン

- ロシア

- 北欧諸国

- アジア太平洋地域

- 中国

- インド

- 日本

- 韓国

- オーストラリア・ニュージーランド

- 東南アジア

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- アラブ首長国連邦

- サウジアラビア

- 南アフリカ

第11章 企業プロファイル

- Accenture

- AT&T

- AWS(Amazon Web Services)

- BT Group(British Telecom)

- Cisco Systems

- Ericsson

- Hewlett Packard Enterprise(HPE)

- Huawei Technologies

- IBM

- Intel

- Juniper Networks

- Mavenir

- Microsoft Azure

- Nokia

- NVIDIA

- Qualcomm

- Samsung Electronics

- T-Mobile US

- Verizon Communications

- ZTE

目次

The Global 5G enterprise private network market was valued at USD 2.93 billion in 2024 and is estimated to grow at a CAGR of 39.2% to reach USD 75.38 billion by 2034. Enterprises across sectors are increasingly embracing private 5G networks to gain tighter control over their digital operations, improve security, and enhance scalability. The demand is driven by the growing reliance on ultra-reliable, low-latency communication and the need for seamless, high-speed data flow. Private 5G networks are transforming enterprise connectivity by enabling real-time decision-making, uninterrupted data streaming, and secure communication, particularly for mission-critical applications.

Companies in manufacturing, logistics, energy, and healthcare are leveraging these networks to implement intelligent automation, industrial IoT, robotics, and remote monitoring systems. The push for digital transformation, combined with favorable regulatory support and robust R&D initiatives, is further accelerating market growth. With increasing investments in smart cities, connected infrastructure, and edge computing, private 5G networks are emerging as a key enabler of next-gen enterprise strategies. National-level initiatives that support digital infrastructure, including expansive 5G rollouts and the creation of smart technology zones, are playing a pivotal role in shaping this landscape. These developments are creating a competitive advantage for early adopters and fostering innovation across sectors that demand resilient and highly secure network solutions.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $2.93 Billion |

| Forecast Value | $75.38 Billion |

| CAGR | 39.2% |

Hardware continues to dominate the 5G enterprise private network space, accounting for 54% of the global market in 2024, and is projected to grow at a CAGR of 39.9% through 2034. The rising need for high-performance equipment such as antennas, routers, small cells, and base stations is fueling this momentum. These hardware components are essential to deploying scalable and secure private 5G infrastructures, particularly in sectors like manufacturing, logistics, and defense, where performance and security cannot be compromised. Businesses are strategically investing in robust hardware to ensure smooth, uninterrupted connectivity and to accommodate advanced use cases that demand minimal latency and maximum reliability.

The on-premises deployment model led the market with a 51% share in 2024 and is expected to retain a strong position in the coming years. Enterprises that manage sensitive data, including those in defense, industrial manufacturing, and healthcare, prefer on-premises networks due to enhanced control, improved data protection, and real-time data management. These networks provide tailored infrastructure that allows for operational continuity, reduced security risks, and seamless integration with existing enterprise systems. The preference for on-site deployment is further supported by the growing demand for customization and compliance with strict industry regulations.

The United States held an 86% share of the global market in 2024, driven by its advanced research ecosystem, high automation penetration, and proactive regulatory framework. Private 5G networks in the country are facilitating secure and efficient operations across critical sectors like defense, energy, and healthcare, where edge computing and robotics are becoming integral.

Major players in the global 5G enterprise private network market include Qualcomm, Cisco Systems, Microsoft Azure, Accenture, IBM, NVIDIA, Huawei Technologies, AT&T, Hewlett Packard Enterprise (HPE), and AWS (Amazon Web Services). These companies are forging strong partnerships with telecom operators and cloud service providers to deliver scalable, secure, and industry-specific 5G solutions. Many are also focusing on integrating AI-powered optimization tools and edge computing technologies to enhance network performance and meet real-time demands. Tailored offerings for sectors such as smart manufacturing, logistics, and infrastructure development, along with strategic pilot programs and regulatory collaborations, are helping firms strengthen their market footprint and accelerate adoption across global enterprises.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.1.1 Research approach

- 1.1.2 Data collection methods

- 1.2 Base estimates and calculations

- 1.2.1 Base year calculation

- 1.2.2 Key trends for market estimates

- 1.3 Forecast model

- 1.4 Primary research & validation

- 1.4.1 Primary sources

- 1.4.2 Data mining sources

- 1.5 Market definitions

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Supplier landscape

- 3.2.1 Equipment manufacturers

- 3.2.2 Telecom service providers

- 3.2.3 System integrators

- 3.2.4 Technology providers

- 3.2.5 End users

- 3.3 Profit margin analysis

- 3.4 Technology & innovation landscape

- 3.5 Patent analysis

- 3.6 Key news & initiatives

- 3.7 Regulatory landscape

- 3.8 Impact forces

- 3.8.1 Growth drivers

- 3.8.1.1 Rising demand for low-latency communication

- 3.8.1.2 Rise in edge computing

- 3.8.1.3 Growing data security & privacy needs

- 3.8.1.4 Surge in IoT and connected devices

- 3.8.2 Industry pitfalls & challenges

- 3.8.2.1 High initial deployment costs

- 3.8.2.2 Integration challenges with legacy systems

- 3.8.1 Growth drivers

- 3.9 Growth potential analysis

- 3.10 Porter’s analysis

- 3.11 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Component, 2021 - 2034 ($Bn)

- 5.1 Key trends

- 5.2 Hardware

- 5.2.1 Radio Access Network (RAN)

- 5.2.2 Core network

- 5.2.3 Edge computing infrastructure

- 5.3 Software

- 5.3.1 Network management software

- 5.3.2 Security software

- 5.3.3 Network slicing software

- 5.3.4 Automation and orchestration tools

- 5.4 Services

- 5.4.1 Consulting

- 5.4.2 Managed services

- 5.4.3 Support and maintenance

Chapter 6 Market Estimates & Forecast, By Deployment Mode, 2021 - 2034 ($Bn)

- 6.1 Key trends

- 6.2 On-premises

- 6.3 Cloud-based

- 6.4 Hybrid

Chapter 7 Market Estimates & Forecast, By Frequency Band, 2021 - 2034 ($Bn)

- 7.1 Key trends

- 7.2 Sub-6 GHz

- 7.3 Millimeter Wave (mmWave)

Chapter 8 Market Estimates & Forecast, By Organization Size, 2021 - 2034 ($Bn)

- 8.1 Key trends

- 8.2 Large enterprises

- 8.3 SMEs

- 8.4 Chemicals & hazardous materials

Chapter 9 Market Estimates & Forecast, By End Use, 2021 - 2034 ($Bn)

- 9.1 Key trends

- 9.2 Manufacturing

- 9.3 Healthcare

- 9.4 Transportation and logistics

- 9.5 Retail

- 9.6 Energy and utilities

- 9.7 Smart cities

- 9.8 Others

Chapter 10 Market Estimates & Forecast, By Region, 2021 - 2034 ($Bn)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 UK

- 10.3.2 Germany

- 10.3.3 France

- 10.3.4 Italy

- 10.3.5 Spain

- 10.3.6 Russia

- 10.3.7 Nordics

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 South Korea

- 10.4.5 ANZ

- 10.4.6 Southeast Asia

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 MEA

- 10.6.1 UAE

- 10.6.2 Saudi Arabia

- 10.6.3 South Africa

Chapter 11 Company Profiles

- 11.1 Accenture

- 11.2 AT&T

- 11.3 AWS (Amazon Web Services)

- 11.4 BT Group (British Telecom)

- 11.5 Cisco Systems

- 11.6 Ericsson

- 11.7 Hewlett Packard Enterprise (HPE)

- 11.8 Huawei Technologies

- 11.9 IBM

- 11.10 Intel

- 11.11 Juniper Networks

- 11.12 Mavenir

- 11.13 Microsoft Azure

- 11.14 Nokia

- 11.15 NVIDIA

- 11.16 Qualcomm

- 11.17 Samsung Electronics

- 11.18 T-Mobile US

- 11.19 Verizon Communications

- 11.20 ZTE

- 発行日

- 発行

- Global Market Insights Inc.

- ページ情報

- 英文 170 Pages

- 納期

- 2~3営業日