|

市場調査レポート

商品コード

1721448

バイオプラスチック高級パッケージ市場の市場機会、成長促進要因、産業動向分析、2025年~2034年予測Bioplastic Luxury Packaging Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| バイオプラスチック高級パッケージ市場の市場機会、成長促進要因、産業動向分析、2025年~2034年予測 |

|

出版日: 2025年04月02日

発行: Global Market Insights Inc.

ページ情報: 英文 180 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

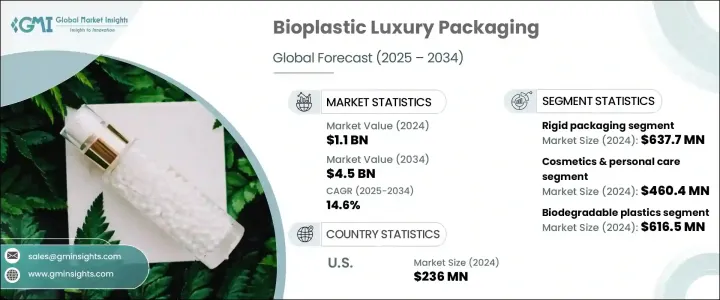

バイオプラスチック高級パッケージの世界市場規模は2024年に11億米ドルとなり、CAGR14.6%で成長し、2034年には45億米ドルに達すると予測されています。

持続可能性が消費者と規制当局の双方にとって重要な優先事項となるにつれ、世界中の高級ブランドは環境配慮型ソリューションに急速に舵を切っています。この勢いは、バイオベースの原料生産への投資の増加や、プラスチック禁止や環境規制の高まりが大きな要因となっています。各地域の政府がより厳しい持続可能性の義務付けを実施しているため、ブランドはブランドの威信を損なうことなく環境フットプリントを削減する代替案を模索せざるを得なくなっています。

バイオプラスチックパッケージングは、高級感という美的感覚と環境に対する責任という価値観が融合した、このシフトに対する説得力のある答えとして台頭してきています。持続可能で高性能なパッケージング・ソリューションに対する消費者の需要の高まりは、この分野におけるイノベーションを加速させています。高級志向の消費者が環境に優しい選択肢を積極的に求める中、ブランドは製品を保護するだけでなく、環境意識の高いバイヤーに響く高級パッケージング・ソリューションを提供することで適応しています。その結果、情勢は急速に世界の高級品業界を定義する動向になりつつあり、従来のプラスチックに代わるリサイクル可能、堆肥化可能、バイオベースの代替品への需要が急増しています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 11億米ドル |

| 予測金額 | 45億米ドル |

| CAGR | 14.6% |

市場セグメンテーションは、硬質包装と軟質包装に区分されます。硬質包装は、頑丈なデザイン、視覚的な魅力、詰め替え可能な用途への適合性により、2024年に6億3,770万米ドルを生み出し、このセグメントをリードしています。香水、化粧品、宝石箱などの高級製品では、バイオPET、PHA、サトウキビ由来プラスチックなどのバイオベースの硬質材料の使用が増加しています。この移行は、欧州連合の単一使用プラスチック指令や拡大生産者責任(EPR)プログラムのような規制枠組みによってさらに強化されており、高級ブランドはリサイクル可能な代替品や生分解性代替品の採用を推進しています。

最終用途産業別では、化粧品・パーソナルケア分野がバイオプラスチック高級パッケージ市場で最大のシェアを占めており、2024年の市場規模は4億6,040万米ドルです。美容・スキンケアブランドは、環境基準と消費者の嗜好の両方に合致する詰め替え容器と生分解性フィルムに強く注目し、持続可能なパッケージングのイノベーションを主導しています。バイオベースのPET、PHA、セルロースベースのフィルムなどの素材は、高級スキンケアアイテム、化粧品、香水の包装に一般的に使用され、製品の完全性を確保すると同時に、視覚的な魅力を高めています。

米国バイオプラスチック高級パッケージ市場だけでも、消費者の意識の高まりや、米国プラスチック規制法やEPR義務化などの規制イニシアチブによって、2024年には2億3,600万米ドルの売上が見込まれています。環境に優しいパッケージングへの需要が急増し続ける中、ブランドは環境コンプライアンスと市場の期待に先んじるため、生分解性とリサイクル可能なソリューションを急速に採用しています。

世界市場の主要企業には、Bio Futura、Biome Bioplastics、NatureWorks LLC、FKuR、Tetra Pak International S.A.、Stora Enso、Sealed Air Corporation、Constantia Flexibles、Corbion、Genpak、Walki Group Oy、ITC Packaging、Novamont S.p.A.、J. Landworth Company、Xiamen Changsu Industrial Co.これらの企業は、最先端の持続可能なパッケージング・イノベーションを開拓するため、研究開発への投資、バイオベース材料の採用拡大、パートナーシップの形成に積極的に取り組んでいます。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- 業界への影響要因

- 促進要因

- バイオベース原料生産の拡大

- 循環型経済とリサイクルイノベーションへの投資

- プラスチック禁止と政府規制がバイオプラスチックの需要を牽引

- バイオベースポリマーの進歩

- 持続可能な包装に対する消費者の嗜好の高まり

- 業界の潜在的リスク&課題

- 高い生産コスト

- パフォーマンスの制限

- 促進要因

- 成長可能性分析

- 規制情勢

- テクノロジーの情勢

- 将来の市場動向

- ギャップ分析

- ポーターの分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 主要市場企業の競合分析

- 競合ポジショニングマトリックス

- 戦略ダッシュボード

第5章 市場推計・予測:材質別、2021-2034

- 主要動向

- 生分解性プラスチック

- バイオベースの非生分解性プラスチック

第6章 市場推計・予測:製品タイプ別、2021-2034

- 主要動向

- 硬質包装

- フレキシブル包装

第7章 市場推計・予測:最終用途産業別、2021-2034

- 主要動向

- 化粧品・パーソナルケア

- ファッション&アクセサリー

- 食品と飲料

- 家電

- 高級品小売とギフト

第8章 市場推計・予測:地域別、2021-2034

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- スペイン

- イタリア

- オランダ

- アジア太平洋地域

- 中国

- インド

- 日本

- オーストラリア

- 韓国

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- サウジアラビア

- 南アフリカ

- アラブ首長国連邦

第9章 企業プロファイル

- Amcor plc

- Bio Futura

- Biome Bioplastics

- Constantia Flexibles

- Corbion

- FKuR

- Futamura Group

- Genpak

- IIC AG

- ITC Packaging

- J. Landworth Company

- NatureWorks LLC

- Novamont S.p.A.

- Sealed Air Corporation

- Stora Enso

- Tetra Pak International S.A.

- TIPA LTD

- Walki Group Oy

- Xiamen Changsu Industrial Co.、Ltd.

The Global Bioplastic Luxury Packaging Market was valued at USD 1.1 billion in 2024 and is estimated to grow at a CAGR of 14.6% to reach USD 4.5 billion by 2034. As sustainability becomes a core priority for both consumers and regulators, luxury brands across the globe are rapidly pivoting toward eco-conscious solutions. This momentum is largely driven by increasing investments in bio-based raw material production and the mounting wave of plastic bans and environmental regulations. Governments across regions are enforcing stricter sustainability mandates, compelling brands to explore alternatives that reduce their environmental footprint without compromising brand prestige.

Bioplastic packaging is emerging as a compelling answer to this shift, blending the aesthetics of luxury with the values of environmental responsibility. Growing consumer demand for sustainable, high-performance packaging solutions is accelerating innovation in the sector. With luxury consumers actively seeking eco-friendly options, brands are adapting by offering premium packaging solutions that not only protect products but also resonate with environmentally aware buyers. As a result, bioplastic luxury packaging is fast becoming a defining trend in the global luxury landscape, driving a surge in demand for recyclable, compostable, and bio-based alternatives to traditional plastic.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $1.1 Billion |

| Forecast Value | $4.5 Billion |

| CAGR | 14.6% |

The bioplastic luxury packaging market is segmented into rigid and flexible packaging formats. Rigid packaging leads the segment, generating USD 637.7 million in 2024, thanks to its sturdy design, visual appeal, and suitability for refillable applications. High-end products such as perfumes, cosmetics, and jewelry boxes increasingly use rigid bio-based materials like bio-PET, PHA, and sugarcane-derived plastics. This transition is further reinforced by regulatory frameworks like the European Union's Single-Use Plastics Directive and Extended Producer Responsibility (EPR) programs, which are pushing luxury brands to adopt recyclable and biodegradable alternatives.

On the basis of end-use industries, the cosmetics and personal care segment commands the largest share of the bioplastic luxury packaging market, valued at USD 460.4 million in 2024. Beauty and skincare brands are leading the charge in sustainable packaging innovation, with a strong focus on refillable containers and biodegradable films that align with both environmental standards and consumer preferences. Materials such as bio-based PET, PHA, and cellulose-based films are commonly used in the packaging of high-end skincare items, cosmetics, and perfumes, ensuring product integrity while enhancing visual appeal.

The U.S. Bioplastic Luxury Packaging Market alone is expected to generate USD 236 million in 2024, driven by growing awareness among consumers and reinforced by regulatory initiatives such as the U.S. Plastic Regulation Act and EPR mandates. As demand for eco-friendly packaging continues to soar, brands are rapidly adopting biodegradable and recyclable solutions to stay ahead of environmental compliance and market expectations.

Leading companies in the global market include Bio Futura, Biome Bioplastics, NatureWorks LLC, FKuR, Tetra Pak International S.A., Stora Enso, Sealed Air Corporation, Constantia Flexibles, Corbion, Genpak, Walki Group Oy, ITC Packaging, Novamont S.p.A., J. Landworth Company, Xiamen Changsu Industrial Co., Ltd., TIPA LTD, and Futamura Group. These players are actively investing in R&D, scaling up bio-based material adoption, and forming partnerships to pioneer cutting-edge, sustainable packaging innovations.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Base estimates and calculations

- 1.3.1 Base year calculation

- 1.3.2 Key trends for market estimation

- 1.4 Forecast model

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.5.2 Data mining sources

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Expansion of bio-based raw material production

- 3.2.1.2 Investment in circular economy & recycling innovation

- 3.2.1.3 Plastic bans & government regulations driving bioplastic demand

- 3.2.1.4 Advances in bio-based polymers

- 3.2.1.5 Growing consumer preference for sustainable packaging

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High production costs

- 3.2.2.2 Performance limitations

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.5 Technology landscape

- 3.6 Future market trends

- 3.7 Gap analysis

- 3.8 Porter’s analysis

- 3.9 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategy dashboard

Chapter 5 Market Estimates and Forecast, By Material Type, 2021 - 2034 (USD Million & Kilo Tons)

- 5.1 Key trends

- 5.2 Biodegradable plastics

- 5.3 Bio-based, non-biodegradable plastics

Chapter 6 Market Estimates and Forecast, By Product Type, 2021 - 2034 (USD Million & Kilo Tons)

- 6.1 Key trends

- 6.2 Rigid packaging

- 6.3 Flexible packaging

Chapter 7 Market Estimates and Forecast, By End Use Industry, 2021 - 2034 (USD Million & Kilo Tons)

- 7.1 Key trends

- 7.2 Cosmetics & personal care

- 7.3 Fashion & accessories

- 7.4 Food & beverages

- 7.5 Consumer electronics

- 7.6 Luxury retail & gifting

Chapter 8 Market Estimates and Forecast, By Region, 2021 - 2034 (USD Million & Kilo Tons)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Netherlands

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.6 Middle East and Africa

- 8.6.1 Saudi Arabia

- 8.6.2 South Africa

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 Amcor plc

- 9.2 Bio Futura

- 9.3 Biome Bioplastics

- 9.4 Constantia Flexibles

- 9.5 Corbion

- 9.6 FKuR

- 9.7 Futamura Group

- 9.8 Genpak

- 9.9 IIC AG

- 9.10 ITC Packaging

- 9.11 J. Landworth Company

- 9.12 NatureWorks LLC

- 9.13 Novamont S.p.A.

- 9.14 Sealed Air Corporation

- 9.15 Stora Enso

- 9.16 Tetra Pak International S.A.

- 9.17 TIPA LTD

- 9.18 Walki Group Oy

- 9.19 Xiamen Changsu Industrial Co., Ltd.