炭化ケイ素半導体デバイスの市場機会、成長促進要因、産業動向分析、2025~2034年予測

Silicon Carbide Semiconductor Devices Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034- 発行日

- ページ情報

- 英文 168 Pages

- 納期

- 2~3営業日

- 商品コード

- 1721414

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

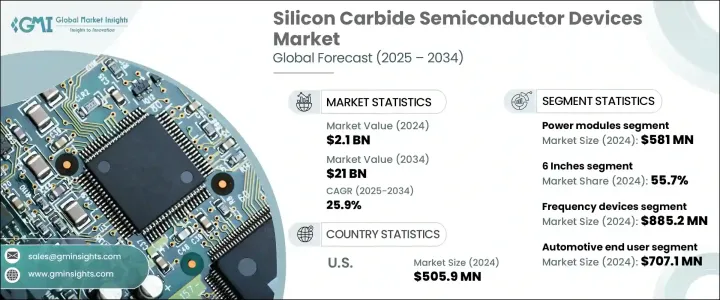

世界の炭化ケイ素半導体デバイス市場は、2024年に21億米ドルと評価され、CAGR 25.9%で成長し、2034年には210億米ドルに達すると推定されています。

この例外的な成長は、脱炭素化への世界の強い推進力と、特に輸送と発電部門におけるクリーンエネルギー技術の採用に起因しています。産業界や政府がエネルギー効率や持続可能性、長期的なコスト削減を優先させる中、炭化ケイ素(SiC)半導体は高性能パワーエレクトロニクスの未来像としてますます注目されています。その優れた熱伝導性、高い絶縁破壊電界、高い周波数での動作能力により、過酷な動作環境下での信頼性が要求されるアプリケーションでは欠かせないものとなっています。スマートグリッドや再生可能エネルギー設備から産業用ドライブや急速充電インフラに至るまで、SiCベースのデバイスは運用基準と期待性能を再定義しています。

世界の需要は、電気自動車(EV)、航空宇宙および防衛システム、大規模な送電網の近代化構想におけるSiC技術の統合の高まりによって引き続き促進されています。EVへのシフトが加速していることは特に重要であり、自動車メーカーは航続距離の延長と充電時間の短縮を実現した自動車を提供する必要に迫られています。SiCデバイスは、エネルギー損失を最小限に抑え、電力変換効率を向上させ、小型軽量システムを可能にすることで、こうした要求に応えるのに役立ちます。SiC半導体の役割は、エネルギー出力とシステムの耐久性を最適化するために高い効率性と堅牢性が不可欠なソーラー・インバータや風力タービンでも拡大しています。一方、防衛・航空宇宙分野では、ミッションクリティカルで高温環境下でも堅牢な性能を発揮するSiCベースの電力システムへの支持が高まっています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 21億米ドル |

| 予測金額 | 210億米ドル |

| CAGR | 25.9% |

市場はコンポーネントによって区分され、パワーモジュールが2024年に5億8,100万米ドルを占め、リードしています。これらのモジュールは、コンパクトなアーキテクチャ、外部冷却の必要性の低減、EVドライブトレイン、ポータブル電子機器、産業用電源など様々な最終用途での高効率化により、広く採用されています。EV販売ブームにより、超高速充電ソリューションのニーズも同時に高まっており、低スイッチング損失と卓越した電圧ハンドリングにより、SiCパワーモジュールが得意とする分野です。

もう一つの重要なセグメントはウエハーサイズで、6インチウエハーが2024年に55.7%のシェアを獲得し、市場を独占すると予想されています。これらのウエハーは、より高いスループットと生産経済性の向上をサポートし、自動車産業や再生可能エネルギー産業における高電圧でエネルギー効率の高いデバイスの製造に適した選択肢となっています。

米国の炭化ケイ素半導体デバイス市場は2024年に5億590万米ドルに達し、クリーンエネルギーの移行と最先端のモビリティ・ソリューションに戦略的に注力していることが背景にあります。米国を拠点とするEVメーカーは、エネルギー効率と車両性能を高めるためにSiCベースのシステムを採用し、高速充電と航続距離延長に対する消費者需要の高まりに対応しています。

この分野の主要企業には、オンセミ、STマイクロエレクトロニクス、ローム・セミコンダクター、ウルフスピード、インフィニオン・テクノロジーズなどがあります。これらの企業は、製造コストを削減しながらデバイスの性能を向上させるため、研究開発に多額の投資を行っています。生産能力の拡大、自動車OEMとの提携、再生可能エネルギー企業との協力は、依然として市場戦略の中心となっています。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- バリューチェーンに影響を与える要因

- 利益率分析

- ディスラプション

- 将来の展望

- 製造業者

- 販売代理店

- サプライヤーの情勢

- 利益率分析

- 主なニュースと取り組み

- 規制情勢

- 影響要因

- 促進要因

- 民生用電子機器におけるSiC半導体デバイスの新たな利用

- 電気自動車の需要の急増

- 産業オートメーションへの傾向の高まり

- 航空宇宙および防衛アプリケーションにおける炭化ケイ素半導体デバイスの適用拡大

- 電力網近代化と再生可能エネルギープロジェクトの増加

- 業界の潜在的リスク&課題

- 新興市場での認知度と採用が限られている

- シリコンと窒化ガリウム(GaN)との競合

- 促進要因

- 成長可能性分析

- ポーターの分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 競合ポジショニングマトリックス

- 戦略的展望マトリックス

第5章 市場推計・予測:コンポーネント別、2021-2034

- 主要動向

- ショットキーダイオード

- FET/MOSFETトランジスタ

- 集積回路

- 整流器/ダイオード

- パワーモジュール

- その他

第6章 市場推計・予測ウエハーサイズ別、2021-2034

- 主要動向

- 1インチから4インチ

- 6インチ

- 8インチ

第7章 市場推計・予測:製品別、2021-2034

- 主要動向

- 光電子デバイス

- パワー半導体

- 周波数デバイス

第8章 市場推計・予測:最終用途別、2021-2034

- 主要動向

- 自動車

- エネルギーと電力

- 家電

- 航空宇宙および防衛

- 医療機器

- データおよび通信機器

- その他

第9章 市場推計・予測:地域別、2021-2034

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- 英国

- ドイツ

- フランス

- イタリア

- スペイン

- ロシア

- アジア太平洋地域

- 中国

- インド

- 日本

- 韓国

- オーストラリア

- ラテンアメリカ

- ブラジル

- メキシコ

- 中東・アフリカ

- 南アフリカ

- サウジアラビア

- アラブ首長国連邦

第10章 企業プロファイル

- Alpha &Omega Semiconductor

- Analog Devices

- Bosch Semiconductors

- Coherent Corp.

- Diodes Incorporated

- Fuji Electric

- GeneSiC Semiconductor

- Infineon Technologies

- Littelfuse

- Microchip Technology

- Mitsubishi Electric

- NXP Semiconductors

- onsemi

- Power Integrations

- Qorvo

- ROHM Semiconductor

- Semikron Danfoss

- Solitron Devices

- STMicroelectronics

- Toshiba Electronic Devices &Storage

- Vishay Intertechnology

- WeEn Semiconductors

- Wolfspeed

目次

The Global Silicon Carbide Semiconductor Devices Market was valued at USD 2.1 billion in 2024 and is estimated to grow at a CAGR of 25.9% to reach USD 21 billion by 2034. This exceptional growth stems from a strong global push toward decarbonization and the adoption of clean energy technologies, especially in the transportation and power generation sectors. As industries and governments prioritize energy efficiency, sustainability, and long-term cost savings, silicon carbide (SiC) semiconductors are increasingly seen as the future of high-performance power electronics. Their superior thermal conductivity, high breakdown electric field, and ability to operate at higher frequencies make them critical in applications requiring reliability under harsh operating environments. From smart grids and renewable energy installations to industrial drives and fast-charging infrastructure, SiC-based devices are redefining operational standards and performance expectations.

Global demand continues to be fueled by the rising integration of SiC technology in electric vehicles (EVs), aerospace and defense systems, and large-scale grid modernization initiatives. The accelerating shift to EVs is particularly significant, as automakers are under pressure to deliver vehicles with extended driving ranges and reduced charging times. SiC devices help meet these demands by minimizing energy losses, improving power conversion efficiency, and enabling compact, lightweight systems. The role of SiC semiconductors is also expanding in solar inverters and wind turbines, where high efficiency and ruggedness are critical to optimize energy output and system durability. Meanwhile, defense and aerospace sectors increasingly favor SiC-based power systems for their robust performance in mission-critical and high-temperature environments.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $2.1 Billion |

| Forecast Value | $21 Billion |

| CAGR | 25.9% |

The market is segmented based on components, with power modules leading the charge, accounting for USD 581 million in 2024. These modules are widely adopted for their compact architecture, reduced need for external cooling, and elevated efficiency across various end-use applications, including EV drivetrains, portable electronics, and industrial power supplies. The boom in EV sales has simultaneously heightened the need for ultra-fast charging solutions, a domain where SiC power modules excel thanks to their low switching losses and exceptional voltage handling.

Another pivotal segment is wafer size, with 6-inch wafers expected to dominate the market, capturing a 55.7% share in 2024. These wafers support higher throughput and improved production economics, making them a preferred choice for manufacturing high-voltage, energy-efficient devices across automotive and renewable energy industries.

The U.S. Silicon Carbide Semiconductor Devices Market reached USD 505.9 million in 2024, backed by the nation's strategic focus on clean energy transitions and cutting-edge mobility solutions. U.S.-based EV makers are adopting SiC-based systems to boost energy efficiency and vehicle performance, addressing growing consumer demand for faster charging and longer range.

Key players in this space include onsemi, STMicroelectronics, ROHM Semiconductor, Wolfspeed, and Infineon Technologies. These companies are heavily investing in R&D to enhance device performance while reducing manufacturing costs. Capacity expansions, partnerships with automotive OEMs, and collaborations with renewable energy firms remain central to their market strategies.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope & definitions

- 1.2 Base estimates & calculations

- 1.3 Forecast calculations

- 1.4 Data sources

- 1.4.1 Primary

- 1.4.2 Secondary

- 1.4.2.1 Paid sources

- 1.4.2.2 Public sources

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021-2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Factor affecting the value chain

- 3.1.2 Profit margin analysis

- 3.1.3 Disruptions

- 3.1.4 Future outlook

- 3.1.5 Manufacturers

- 3.1.6 Distributors

- 3.2 Supplier landscape

- 3.3 Profit margin analysis

- 3.4 Key news & initiatives

- 3.5 Regulatory landscape

- 3.6 Impact forces

- 3.6.1 Growth drivers

- 3.6.1.1 Emerging use of SiC semiconductor devices in consumer electronics

- 3.6.1.2 Surge in demand for electric vehicles

- 3.6.1.3 Rising inclination towards industrial automation

- 3.6.1.4 Increasing application of silicon carbide semiconductor devices in aerospace and defense applications

- 3.6.1.5 Growing number of grid modernization and renewable energy projects

- 3.6.2 Industry pitfalls & challenges

- 3.6.2.1 Limited awareness and adoption in emerging markets

- 3.6.2.2 Competition from silicon and gallium nitride (GaN)

- 3.6.1 Growth drivers

- 3.7 Growth potential analysis

- 3.8 Porter’s analysis

- 3.9 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Component, 2021-2034 (USD Million)

- 5.1 Key trends

- 5.2 Schottky diodes

- 5.3 FET/MOSFET transistors

- 5.4 Integrated circuits

- 5.5 Rectifiers/diodes

- 5.6 Power modules

- 5.7 Others

Chapter 6 Market Estimates & Forecast, By Wafer Size, 2021-2034 (USD Million)

- 6.1 Key trends

- 6.2 1 inch to 4 inches

- 6.3 6 inches

- 6.4 8 inches

Chapter 7 Market Estimates & Forecast, By Product, 2021-2034 (USD Million)

- 7.1 Key trends

- 7.2 Optoelectronic devices

- 7.3 Power semiconductors

- 7.4 Frequency devices

Chapter 8 Market Estimates & Forecast, By End Use, 2021-2034 (USD Million)

- 8.1 Key trends

- 8.2 Automotive

- 8.3 Energy & power

- 8.4 Consumer electronics

- 8.5 Aerospace & defense

- 8.6 Medical devices

- 8.7 Data & communication devices

- 8.8 Others

Chapter 9 Market Estimates & Forecast, By Region, 2021-2034 (USD Million)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 UK

- 9.3.2 Germany

- 9.3.3 France

- 9.3.4 Italy

- 9.3.5 Spain

- 9.3.6 Russia

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 South Korea

- 9.4.5 Australia

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.6 MEA

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 Alpha & Omega Semiconductor

- 10.2 Analog Devices

- 10.3 Bosch Semiconductors

- 10.4 Coherent Corp.

- 10.5 Diodes Incorporated

- 10.6 Fuji Electric

- 10.7 GeneSiC Semiconductor

- 10.8 Infineon Technologies

- 10.9 Littelfuse

- 10.10 Microchip Technology

- 10.11 Mitsubishi Electric

- 10.12 NXP Semiconductors

- 10.13 onsemi

- 10.14 Power Integrations

- 10.15 Qorvo

- 10.16 ROHM Semiconductor

- 10.17 Semikron Danfoss

- 10.18 Solitron Devices

- 10.19 STMicroelectronics

- 10.20 Toshiba Electronic Devices & Storage

- 10.21 Vishay Intertechnology

- 10.22 WeEn Semiconductors

- 10.23 Wolfspeed

- 発行日

- 発行

- Global Market Insights Inc.

- ページ情報

- 英文 168 Pages

- 納期

- 2~3営業日