エッジ人工知能チップ市場の市場機会、成長促進要因、産業動向分析、2025年~2034年予測

Edge Artificial Intelligence Chips Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034- 発行日

- ページ情報

- 英文 145 Pages

- 納期

- 2~3営業日

- 商品コード

- 1721411

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

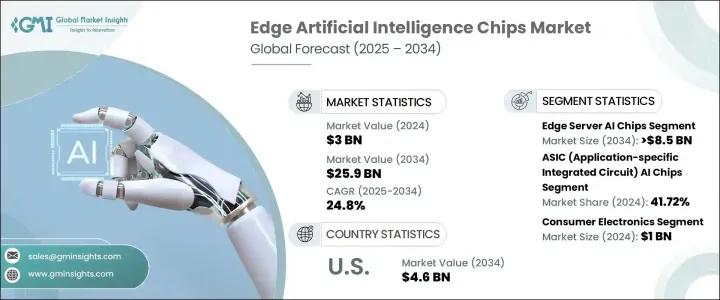

エッジ人工知能チップの世界市場規模は、2024年に30億米ドルとなり、CAGR 24.8%で成長し、2034年には259億米ドルに達すると推定されます。

この著しい成長は、コンピューティング・パラダイムにおけるダイナミックな変化を反映しており、デバイス・レベルでのリアルタイム・インテリジェンスが急速に標準になりつつあります。企業が業務のデジタル化を進める中、ローカルでデータを処理できる高性能AIチップセットの需要が急増しています。この進化は、自律走行、スマート製造、精密ヘルスケアなど、クラウドのレイテンシーに依存することなく瞬時に意思決定を行わなければならない分野で特に顕著です。エッジAIチップは、スマート・デバイスがソースでデータを処理、分析、行動することを可能にし、より速い応答時間とデータ・プライバシーの向上を提供します。

AIが家電、産業システム、スマートインフラに深く浸透するにつれ、スケーラブルでエネルギー効率に優れたAIハードウェアの需要が高まっています。さらに、製造技術の進歩、コンポーネントの小型化、5Gネットワークへのアクセスの拡大により、世界中でエッジAIソリューションの展開が加速しています。企業はエッジAIを、ロボット工学、拡張知能、インテリジェント監視における変革能力を解き放つ鍵と見なすようになってきています。分散型インテリジェンスとエッジコンピューティングの組み合わせは、データの使用方法とセキュリティの確保方法を再定義し、チップメーカーとシステムインテグレーターに大きなチャンスをもたらしています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 30億米ドル |

| 予測金額 | 259億米ドル |

| CAGR | 24.8% |

市場は、オンデバイスAIチップとエッジサーバーAIチップに展開別に区分されます。エッジサーバーAIチップは、産業界が低レイテンシのAI操作とローカライズされたデータ処理を優先する傾向が強まっていることから、2034年までに85億米ドルを創出すると予測されています。スマートシティのリアルタイム交通監視、製造業の予知保全、ヘルスケアの高度診断などの使用事例が、堅牢なエッジサーバーの需要を押し上げています。また、5Gインフラの展開により、エッジサーバーへのアクセス性と帯域幅が強化され、エンドユーザーの近くで複雑なAIワークロードをホストすることがより現実的になっています。

チップの種類では、特定用途向け集積回路(ASIC)が2024年に41.72%のシェアを獲得し、業界を席巻しています。これらのチップは、ターゲットとするAIアプリケーションに比類ない性能を提供し、音声認識、コンピュータビジョン、NLPなどの機能で最有力候補となっています。そのエネルギー効率と処理速度は、大量導入のためのスケーラブルでコスト効率に優れたソリューションを必要とするAIハードウェア開発者を引き付け続けています。

米国エッジ人工知能チップ市場の2024年の市場規模は46億米ドルで、自律システム、軍事グレードの技術、スマート製造におけるイノベーションが主な原動力となっています。大手ハイテク企業は、ヘルスケア・ウェアラブル、自動セキュリティ、産業用ロボティクス向けの高度な機能を開発するため、AIチップの研究開発に多額の投資を行っています。CHIPS Actのような政府のイニシアチブは、半導体開発に資金を提供し、重要なAI技術のサプライチェーンの弾力性を確保することで、成長をさらに増幅させています。

世界のエッジ人工知能チップ市場の主要企業には、Qualcomm Technologies、NVIDIA Corporation、Arm Limited、Advanced Micro Devices, Inc.、Broadcom Inc.、Apple、STマイクロエレクトロニクス、Texas Instruments Incorporated、MediaTek Inc.、Lattice Semiconductor、Mythic、Marvell、Synaptics Incorporated、BrainChip, Inc.、HAILO TECHNOLOGIES LTD、Huawei Cloud Computing Technologies Co.各社は、チップの消費電力を削減し、処理効率を高めるための研究開発に積極的に投資しています。多くの企業は、IoT、自律走行車、スマートインフラ分野からの高まる需要に対応するため、製造事業を拡大しています。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- 業界への影響要因

- 促進要因

- 半導体需要の増加

- IoT導入の急増

- 低遅延処理のニーズの高まり

- 5Gネットワークの拡大

- 家電製品におけるAIの需要の高まり

- 業界の潜在的リスク&課題

- 高い消費電力と熱管理

- 複雑なハードウェアとソフトウェアの統合

- 促進要因

- 成長可能性分析

- 規制情勢

- テクノロジーの情勢

- 将来の市場動向

- ギャップ分析

- ポーターの分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 主要市場企業の競合分析

- 競合ポジショニングマトリックス

- 戦略ダッシュボード

第5章 市場推計・予測:チップタイプ別、2021-2034

- 主要動向

- ASIC(特定用途向け集積回路)AIチップ

- GPU(グラフィックス・プロセッシング・ユニット)AIチップ

- CPU(中央処理装置)AIチップ

- FPGA(フィールドプログラマブルゲートアレイ)AIチップ

- ニューロモルフィックAIチップ

第6章 市場推計・予測:展開別、2021-2034

- 主要動向

- デバイス上のエッジAIチップ

- エッジサーバーAIチップ

第7章 市場推計・予測:最終用途産業別、2021-2034

- 主要動向

- 家電

- 自動車・輸送

- ヘルスケアおよび医療機器

- 小売・eコマース

- 製造および産業オートメーション

- 通信

- その他

第8章 市場推計・予測:地域別、2021-2034

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- スペイン

- イタリア

- アジア太平洋地域

- 中国

- インド

- 日本

- オーストラリア・ニュージーランド

- 韓国

- ラテンアメリカ

- ブラジル

- メキシコ

- 中東・アフリカ

- サウジアラビア

- 南アフリカ

- アラブ首長国連邦

第9章 企業プロファイル

- Advanced Micro Devices、Inc.

- Apple

- Arm Limited

- BrainChip、Inc.

- Broadcom Inc.

- HAILO TECHNOLOGIES LTD

- Huawei Cloud Computing Technologies Co.、Ltd

- Intel Corporation

- Lattice Semiconductor

- Marvell

- MediaTek Inc

- Mythic

- NVIDIA Corporation

- Qualcomm Technologies

- STMicroelectronics

- Synaptics Incorporated

- Texas Instruments Incorporated

目次

The Global Edge Artificial Intelligence Chips Market was valued at USD 3 billion in 2024 and is estimated to grow at a CAGR of 24.8% to reach USD 25.9 billion by 2034. This significant growth reflects a dynamic shift in computing paradigms, where real-time intelligence at the device level is rapidly becoming the norm. As enterprises continue to digitize operations, the demand for high-performance AI chipsets that can process data locally is surging. This evolution is particularly pronounced in sectors such as autonomous driving, smart manufacturing, and precision healthcare, where decisions must be made instantly without reliance on cloud latency. Edge AI chips enable smart devices to process, analyze, and act on data at the source, offering faster response times and improved data privacy.

With AI penetrating deeper into consumer electronics, industrial systems, and smart infrastructure, the demand for scalable, energy-efficient AI hardware is intensifying. Furthermore, advancements in fabrication technology, miniaturization of components, and growing access to 5G networks are accelerating the deployment of edge AI solutions worldwide. Companies are increasingly viewing edge AI as the key to unlocking transformative capabilities in robotics, augmented reality, and intelligent surveillance. The combination of decentralized intelligence and edge computing is redefining how data is used and secured, presenting a tremendous opportunity for chipmakers and system integrators alike.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $3 Billion |

| Forecast Value | $25.9 Billion |

| CAGR | 24.8% |

The market is segmented by deployment into on-device and edge server AI chips. Edge server AI chips are projected to generate USD 8.5 billion by 2034 as industries increasingly prioritize low-latency AI operations and localized data processing. Use cases like real-time traffic monitoring in smart cities, predictive maintenance in manufacturing, and advanced diagnostics in healthcare are pushing demand for robust edge servers. The rollout of 5G infrastructure is also enhancing edge server accessibility and bandwidth, making them more viable for hosting complex AI workloads close to end-users.

In terms of chip type, application-specific integrated circuits (ASICs) dominate the landscape, capturing a 41.72% share in 2024. These chips offer unmatched performance for targeted AI applications, making them a top choice for functions like speech recognition, computer vision, and NLP. Their energy efficiency and processing speed continue to attract AI hardware developers who need scalable, cost-effective solutions for mass deployment.

The U.S. Edge Artificial Intelligence Chips Market was valued at USD 4.6 billion in 2024, largely driven by innovation in autonomous systems, military-grade technology, and smart manufacturing. Leading tech firms are heavily investing in AI chip R&D to develop advanced capabilities for healthcare wearables, automated security, and industrial robotics. Government initiatives such as the CHIPS Act are further amplifying growth by funding semiconductor development and ensuring supply chain resilience for critical AI technologies.

Leading companies in the Global Edge Artificial Intelligence Chips Market include Qualcomm Technologies, NVIDIA Corporation, Arm Limited, Advanced Micro Devices, Inc., Broadcom Inc., Apple, STMicroelectronics, Texas Instruments Incorporated, MediaTek Inc., Lattice Semiconductor, Mythic, Marvell, Synaptics Incorporated, BrainChip, Inc., HAILO TECHNOLOGIES LTD, Huawei Cloud Computing Technologies Co., Ltd, and Intel Corporation. Companies are actively investing in R&D to reduce chip power consumption and enhance processing efficiency. Many are expanding manufacturing operations to meet escalating demands from the IoT, autonomous vehicle, and smart infrastructure sectors.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Base estimates and calculations

- 1.3.1 Base year calculation

- 1.3.2 Key trends for market estimation

- 1.4 Forecast model

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.5.2 Data mining sources

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increasing demand for semiconductors

- 3.2.1.2 Surge in IoT adoption

- 3.2.1.3 Rising need for low-latency processing

- 3.2.1.4 Expansion of 5G networks

- 3.2.1.5 Growing demand for AI in consumer electronics

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High power consumption and thermal management

- 3.2.2.2 Complex hardware and software integration

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.5 Technology landscape

- 3.6 Future market trends

- 3.7 Gap analysis

- 3.8 Porter’s analysis

- 3.9 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategy dashboard

Chapter 5 Market Estimates and Forecast, By Chip Type, 2021 - 2034 ($ Mn)

- 5.1 Key trends

- 5.2 ASIC (Application-Specific Integrated Circuit) AI Chips

- 5.3 GPU (Graphics Processing Unit) AI Chips

- 5.4 CPU (Central Processing Unit) AI Chips

- 5.5 FPGA (Field-Programmable Gate Array) AI Chips

- 5.6 Neuromorphic AI Chips

Chapter 6 Market Estimates and Forecast, By Deployment, 2021 - 2034 ($ Mn)

- 6.1 Key trends

- 6.2 On-Device Edge AI Chips

- 6.3 Edge Server AI Chips

Chapter 7 Market Estimates and Forecast, By End Use Industry, 2021 - 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Consumer electronics

- 7.3 Automotive & transportation

- 7.4 Healthcare & medical devices

- 7.5 Retail & e-commerce

- 7.6 Manufacturing & industrial automation

- 7.7 Telecommunications

- 7.8 Others

Chapter 8 Market Estimates and Forecast, By Region, 2021 - 2034 ($ Mn)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 ANZ

- 8.4.5 South Korea

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.6 Middle East and Africa

- 8.6.1 Saudi Arabia

- 8.6.2 South Africa

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 Advanced Micro Devices, Inc.

- 9.2 Apple

- 9.3 Arm Limited

- 9.4 BrainChip, Inc.

- 9.5 Broadcom Inc.

- 9.6 HAILO TECHNOLOGIES LTD

- 9.7 Huawei Cloud Computing Technologies Co., Ltd

- 9.8 Intel Corporation

- 9.9 Lattice Semiconductor

- 9.10 Marvell

- 9.11 MediaTek Inc

- 9.12 Mythic

- 9.13 NVIDIA Corporation

- 9.14 Qualcomm Technologies

- 9.15 STMicroelectronics

- 9.16 Synaptics Incorporated

- 9.17 Texas Instruments Incorporated

- 発行日

- 発行

- Global Market Insights Inc.

- ページ情報

- 英文 145 Pages

- 納期

- 2~3営業日