ペット用OTC薬市場の機会、成長促進要因、産業動向分析、2025年~2034年の予測

OTC Pet Medication Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034- 発行日

- ページ情報

- 英文 130 Pages

- 納期

- 2~3営業日

- 商品コード

- 1716544

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

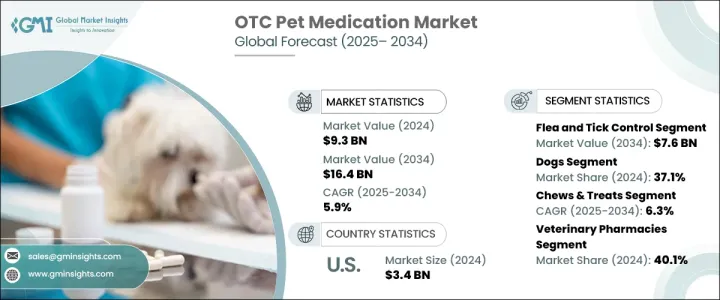

ペット用OTC薬の世界市場は、2024年に93億米ドルに達し、2025年から2034年にかけてCAGR 5.9%で成長すると予想されています。

同市場の成長の主な要因は、ペットの飼い主数の増加とペットの人間化の動向の高まりです。この変化により、より優れたヘルスケア・ソリューションや予防的ウェルネス製品に対する需要が高まっています。ペットの飼い主は、ペットの全体的な健康状態を改善するために、高品質で入手しやすく、効果的な市販薬(OTC)を積極的に求めるようになっています。予防医療に対する意識の高まりと、投与が容易な医薬品の入手可能性が、市場の拡大に大きく寄与しています。

ペットの飼い主が潜在的な健康リスクについて知識を深めるにつれ、関節炎、皮膚アレルギー、消化器系の問題といった一般的な症状に対処する製品に投資するようになっています。この動向は特に先進地域で顕著で、可処分所得が高く、ペットの健康を重視する傾向が強いため、ペットヘルスケアへの支出が増加しています。さらに、風味のある錠剤やチュアブルなど、投薬処方の革新がコンプライアンスと治療効果を高め、市場の需要をさらに押し上げています。eコマース・プラットフォームの存在感の高まりも、これらの製品をより身近なものとし、世界のペットオーナーに利便性と幅広い選択肢を提供しています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 93億米ドル |

| 予測金額 | 164億米ドル |

| CAGR | 5.9% |

ペットが寄生虫感染症、皮膚疾患、関節痛など様々な健康問題に遭遇するようになり、OTC医薬品のニーズは増加の一途をたどっています。変形性関節症は、ペットに最も多く見られる疾患のひとつで、特に高齢の犬や猫に多く、ペット数のかなりの部分が罹患しています。関節関連の健康問題の発生率が高いことから、関節用サプリメントやその他の治療薬の需要が持続的に高まると予想されます。さらに、寄生虫駆除や皮膚の保護といった予防ヘルスケアへの注目が高まっていることも、OTCソリューションの市場拡大に寄与しています。ペットの飼い主は、ちょっとした健康上の懸念に対処するために自然療法やホメオパシー療法を利用するようになっており、利用可能なOTC製品の種類がさらに多様化しています。

ノミ・マダニ駆除分野は2024年に42億米ドルを占める。ノミやダニが媒介する媒介性疾患の蔓延が増加していることが、効果的な駆除薬への需要を煽っています。ペットの飼育率の上昇と疾病予防に対する関心の高まりが、この分野の急成長を後押ししています。メーカー各社は、塗布のしやすさを確保しながら長期的な保護を提供する高度な製剤を開発しており、このセグメントの継続的な優位性に寄与しています。

ペット用OTC薬市場は、犬、猫、鳥、魚、爬虫類、その他を含むペットの種類に基づいて分類されます。犬は2024年の市場シェアの37.1%を占めています。犬の健康問題の有病率の高さ、ヘルスケア支出の増加、寄生虫感染症にかかりやすくなる屋外への露出などが相まって、メーカーは犬の健康に合わせた医薬品の開発を優先するようになっています。ペットの飼い主は、愛犬の健康を維持するための解決策を求めるようになっており、この分野の持続的な成長を牽引しています。

米国のペット用OTC薬市場は2024年に34億米ドルとなり、予測期間を通じて最大市場であり続けると予想されます。ペットの世話に関する意識の高まりとペットの人間化が米国における市場成長の主な促進要因です。ペットの飼い主は、ペットの健康と幸福を維持するための高度な解決策を求めることに警戒心を強め、積極的になっています。革新的な製剤の入手可能性とeコマース・プラットフォームへのアクセスの増加により、ペット用OTC薬がより身近なものとなり、今後数年間の市場の好調が確実なものとなっています。

目次

第1章 調査手法と調査範囲

第2章 エグゼクティブサマリー

第3章 業界洞察

- エコシステム分析

- 業界への影響要因

- 促進要因

- ペット飼育率の上昇

- ペットの予防ヘルスケア重視の高まり

- 人獣共通感染症の増加

- eコマースとオンライン小売の拡大

- 動物ヘルスケア支出の増加

- 業界の潜在的リスク&課題

- 厳しい規制基準

- 副作用と誤用の可能性

- 促進要因

- 成長の可能性分析

- 規制状況

- 今後の市場動向

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業マトリックス分析

- 主要市場プレーヤーの競合分析

- 競合のポジショニングマトリックス

- 戦略ダッシュボード

第5章 市場推計・予測:医薬品タイプ別、2021年~2034年

- 主要動向

- ノミ・マダニ駆除

- 駆虫薬と寄生虫駆除薬

- 鎮痛・アレルギー治療薬

- 皮膚・被毛ケア

- デンタルケア

- 栄養補助食品

- 行動・不安緩和薬

- その他の投薬タイプ

第6章 市場推計・予測:ペットタイプ別、2021年~2034年

- 主要動向

- 犬

- 猫

- 鳥類

- 魚類・爬虫類

- その他のペット

第7章 市場推計・予測:剤形別、2021年~2034年

- 主要動向

- チューズ&おやつ

- カプセル

- スプレー

- 軟膏

- その他の剤形

第8章 市場推計・予測:流通チャネル別、2021年~2034年

- 主要動向

- 動物薬局

- ペット専門店

- オンライン小売業者

- その他の流通チャネル

第9章 市場推計・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- スペイン

- イタリア

- オランダ

- アジア太平洋

- 中国

- インド

- 日本

- オーストラリア

- 韓国

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- 南アフリカ

- サウジアラビア

- アラブ首長国連邦

第10章 企業プロファイル

- AdvaCare Pharma

- Bimeda

- Boehringer Ingelheim International

- Ceva Sante Animale

- Dechra

- Elanco Animal Health

- Heska Corporation

- Merck &Co.

- Norbrook

- Nutramax Laboratories Consumer Care

- PetIQ

- Phibro Animal Health

- Vetenex Animal Health

- Vetoquinol

- Virbac

- Zoetis

目次

The Global OTC Pet Medication Market reached USD 9.3 billion in 2024 and is expected to grow at a CAGR of 5.9% between 2025 and 2034. The market's growth is primarily fueled by the increasing number of pet owners and the rising trend of pet humanization. This shift has led to heightened demand for better healthcare solutions and preventive wellness products. Pet owners are more proactive in seeking high-quality, accessible, and effective over-the-counter (OTC) medications to improve their pets' overall health. Growing awareness of preventive care and the availability of easy-to-administer medications have significantly contributed to the market expansion.

As pet owners become increasingly informed about potential health risks, they are investing in products that address common conditions such as arthritis, skin allergies, and digestive issues. This trend is particularly prominent in developed regions, where higher disposable income and a strong emphasis on pet well-being drive higher spending on pet healthcare. Moreover, innovations in medication formulations, including flavored tablets and chewables, are enhancing compliance and treatment effectiveness, further boosting market demand. The growing presence of e-commerce platforms has also made these products more accessible, offering convenience and a broader range of options for pet owners globally.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $9.3 Billion |

| Forecast Value | $16.4 Billion |

| CAGR | 5.9% |

As pets encounter a growing range of health issues, including parasitic infections, skin disorders, and joint pain, the need for OTC medications continues to rise. Osteoarthritis is one of the most prevalent conditions in pets, particularly in aging dogs and cats, affecting a significant portion of the pet population. The high incidence of joint-related health problems is expected to drive sustained demand for joint supplements and other therapeutic medications. Additionally, the increasing focus on preventative healthcare, such as parasite control and skin protection, is contributing to the growing market for OTC solutions. Pet owners are turning to natural and homeopathic remedies to address minor health concerns, further diversifying the range of available OTC products.

The flea and tick control segment accounted for USD 4.2 billion in 2024. The increasing prevalence of vector-borne diseases transmitted by fleas and ticks has fueled the demand for effective control medications. Rising pet adoption rates, coupled with growing concerns about disease prevention, are driving this segment's rapid growth. Manufacturers are developing advanced formulations that offer long-lasting protection while ensuring ease of application, contributing to the segment's continued dominance.

The OTC pet medication market is categorized based on pet type, including dogs, cats, birds, fish, reptiles, and others. Dogs accounted for 37.1% of the market share in 2024. The high prevalence of health issues in dogs, combined with increased healthcare spending and outdoor exposure that makes them more vulnerable to parasitic infections, has led manufacturers to prioritize developing medications tailored to canine health. Pet owners are increasingly seeking solutions to ensure their dogs remain healthy, driving sustained growth in this segment.

The U.S. OTC pet medication market was valued at USD 3.4 billion in 2024 and is expected to remain the largest market throughout the forecast period. Growing awareness about pet care and the humanization of pets are key drivers of market growth in the U.S. Pet owners are becoming more vigilant and proactive in seeking advanced solutions to maintain the health and well-being of their pets. The availability of innovative formulations and increasing access to e-commerce platforms are making OTC pet medications more accessible, ensuring strong market performance in the coming years.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Base estimates and calculations

- 1.3.1 Base year calculation

- 1.3.2 Key trends for market estimation

- 1.4 Forecast model

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.5.2 Data mining sources

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising pet ownership rate

- 3.2.1.2 Growing emphasis on preventive healthcare for pets

- 3.2.1.3 Increasing prevalence of zoonotic diseases

- 3.2.1.4 Expansion of e-commerce & online retailing

- 3.2.1.5 Growing animal healthcare expenditure

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Stringent regulatory standards

- 3.2.2.2 Potential side effects & misuse

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.5 Future market trends

- 3.6 Porter's analysis

- 3.7 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company matrix analysis

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategy dashboard

Chapter 5 Market Estimates and Forecast, By Medication Type, 2021 – 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Flea and tick control

- 5.3 Dewormers & parasiticides

- 5.4 Pain relievers & allergy medications

- 5.5 Skin and coat care

- 5.6 Dental care

- 5.7 Nutritional supplements

- 5.8 Behavioral & anxiety relief medications

- 5.9 Other medication types

Chapter 6 Market Estimates and Forecast, By Pet Type, 2021 – 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Dogs

- 6.3 Cats

- 6.4 Birds

- 6.5 Fishes & reptiles

- 6.6 Other pet types

Chapter 7 Market Estimates and Forecast, By Dosage Form, 2021 – 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Chews & treats

- 7.3 Capsules

- 7.4 Sprays

- 7.5 Ointments

- 7.6 Other dosage forms

Chapter 8 Market Estimates and Forecast, By Distribution Channel, 2021 – 2034 ($ Mn)

- 8.1 Key trends

- 8.2 Veterinary pharmacies

- 8.3 Pet specialty stores

- 8.4 Online retailers

- 8.5 Other distribution channels

Chapter 9 Market Estimates and Forecast, By Region, 2021 – 2034 ($ Mn)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Netherlands

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 Middle East and Africa

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 AdvaCare Pharma

- 10.2 Bimeda

- 10.3 Boehringer Ingelheim International

- 10.4 Ceva Sante Animale

- 10.5 Dechra

- 10.6 Elanco Animal Health

- 10.7 Heska Corporation

- 10.8 Merck & Co.

- 10.9 Norbrook

- 10.10 Nutramax Laboratories Consumer Care

- 10.11 PetIQ

- 10.12 Phibro Animal Health

- 10.13 Vetenex Animal Health

- 10.14 Vetoquinol

- 10.15 Virbac

- 10.16 Zoetis

- 発行日

- 発行

- Global Market Insights Inc.

- ページ情報

- 英文 130 Pages

- 納期

- 2~3営業日