|

|

市場調査レポート

商品コード

1716537

紙製軟包装市場の機会、成長促進要因、産業動向分析、2025年~2034年の予測Flexible Paper Packaging Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

|

|||||||

カスタマイズ可能

|

|||||||

| 紙製軟包装市場の機会、成長促進要因、産業動向分析、2025年~2034年の予測 |

|

出版日: 2025年03月26日

発行: Global Market Insights Inc.

ページ情報: 英文 160 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

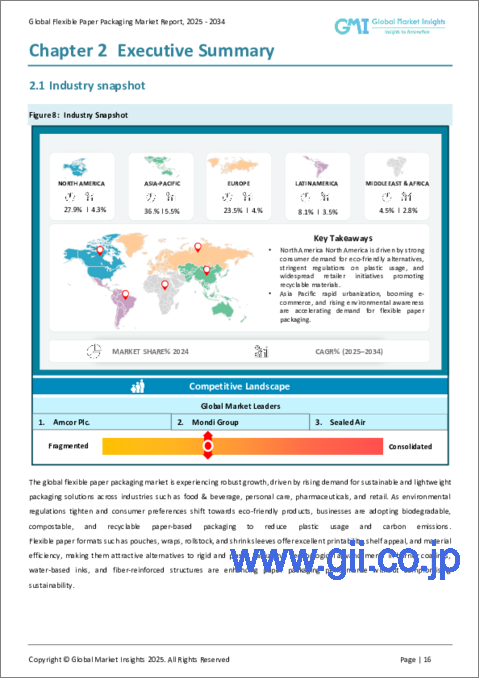

紙製軟包装の世界市場は2024年に693億米ドルに達し、2025年から2034年にかけてCAGR 4.5%で成長すると予測されています。

市場の成長軌道は、特に食品業界において二酸化炭素排出量に対する懸念が高まり、より持続可能なパッケージング・ソリューションへのシフトを促していることが大きな要因となっています。世界の持続可能性への取り組みが勢いを増すにつれて、あらゆる業界の企業が二酸化炭素排出量を削減するために環境に優しい代替品を採用しています。特に飲食品分野では、軽量で生分解性があり、リサイクル可能な紙製軟包装が好まれる選択肢として浮上しています。消費者のエコに対する意識が高まる中、メーカーは消費者の嗜好の変化に合わせた革新的な紙ベースの包装ソリューションを導入することで対応しています。

さらに、eコマースの急速な拡大が軟質紙包装の需要に拍車をかけています。オンライン小売業者は、製品の安全かつコスト効率の高い配送を保証する軽量で保護性の高い素材を求めているからです。廃棄物削減への関心の高まりは、厳しい環境規制の実施と相まって、業界全体で軟質紙包装の採用をさらに加速させています。持続可能性がオプションではなく業界標準になるにつれ、市場参入企業は機能性と環境メリットの両方を提供する先進紙パッケージング材料を生み出すための研究開発に多額の投資を行っています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 693億米ドル |

| 予測金額 | 1,076億米ドル |

| CAGR | 4.5% |

紙製軟包装市場には、ロールストック、パウチ、シュリンクスリーブ、ラップなど様々な製品タイプがあります。このうち、パウチ分野は2024年に276億米ドルを生み出しました。パウチは多用途性、軽量設計、優れたバリア保護により絶大な人気を得ており、飲食品、パーソナルケア業界の包装用途に理想的です。消費者はその便利でリシーラブル、使いやすい特徴からますますパウチに惹かれています。産業界が持続可能で使い勝手の良いパッケージングソリューションを重視し続ける中、パウチの需要は引き続き堅調に推移すると予想されます。さらに、パウチ製造プロセスの技術的進歩により、耐久性が向上し、消費者の全体的な体験が改善されているため、市場での存在感を強めたいブランドにとって、パウチは有力な選択肢となっています。

印刷技術に関しては、軟包装紙市場はグラビア印刷、フレキソ印刷、デジタル印刷、その他に区分されます。フレキソ印刷分野は大幅な成長が見込まれ、2034年までに473億米ドルに達します。フレキソ印刷の人気は、速乾性の低粘度インキを利用する能力からきており、印刷速度の高速化とコスト効率の高い生産工程を可能にしています。この技術は、優れた印刷品質を維持しながら生産効率を最適化しようとするメーカーに強く支持されています。ブランドの認知度と棚へのアピールを高める高品質のパッケージングに対する需要が高まる中、フレキソ印刷は、こうした業界の進化する要件を満たす上で極めて重要な役割を果たすことになるでしょう。さらに、持続可能なインキや印刷方法を重視する傾向が強まっていることも、フレキソ印刷の需要をさらに高め、紙製軟包装市場の成長促進要因として位置づけられています。

米国の紙製軟包装市場は2024年に154億米ドルと評価され、環境的に持続可能な慣行の導入でリードし続けています。米国の拡大生産者責任(EPR)などの政策は、包装分野におけるリサイクル慣行の改善と廃棄物の削減を推進しています。この規制の後押しにより、企業はリサイクル可能で生分解性のある包装資材を採用するようになり、より広範な持続可能性の目標に沿ったものとなっています。環境に優しい包装に対する消費者の意識が高まるにつれ、米国で事業を展開するブランドは、ブランド・ロイヤルティを高める持続可能なソリューションを提供しながら、規制基準を満たすための努力を重ねています。環境保護に対する積極的な姿勢は、企業が収益性と環境責任のバランスを取ろうと努力する中で、軟質紙包装市場の継続的な成長の舞台を整えています。

目次

第1章 調査手法と調査範囲

第2章 エグゼクティブサマリー

第3章 業界洞察

- エコシステム分析

- 業界への影響要因

- 促進要因

- 持続可能な包装に対する需要の高まり

- 硬質包装と比較した費用対効果

- 利便性を求める消費者の増加

- 材料技術の進歩

- 環境に優しいソリューションに対する規制支援

- 落とし穴と課題

- 原材料価格の変動

- 技術革新のための高額な初期資本投資

- 促進要因

- 潜在成長力の分析

- 規制状況

- 技術情勢

- 将来の市場動向

- ギャップ分析

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業シェア分析

- 主要市場プレーヤーの競合分析

- 競合のポジショニングマトリックス

- 戦略ダッシュボード

第5章 市場推計・予測:タイプ別、2021年~2034年

- 主要動向

- パウチ

- ロールストック

- シュリンクスリーブ

- ラップ

- その他

第6章 市場推計・予測:印刷技術別、2021年~2034年

- 主要動向

- フレキソ印刷

- グラビア

- デジタル印刷

- その他

第7章 市場推計・予測:最終用途別、2021年~2034年

- 主要動向

- 飲食品

- 小売・消費財

- 医薬品・ヘルスケア

- パーソナルケア

- その他

第8章 市場推計・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- スペイン

- イタリア

- オランダ

- アジア太平洋

- 中国

- インド

- 日本

- オーストラリア

- 韓国

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- サウジアラビア

- 南アフリカ

- アラブ首長国連邦

第9章 企業プロファイル

- Amcor plc

- Berry Global Group, Inc.

- Constantia Flexibles Group

- Coveris Holdings S.A.

- DS Smith plc

- Graphic Packaging International, LLC

- Huhtamaki Oyj

- International Paper Company

- Mondi Group

- ProAmpac Holdings, Inc.

- Sealed Air Corporation

- Smurfit Kappa Group

- Sonoco Products Company

- UFlex Limited

- WestRock Company

The Global Flexible Paper Packaging Market reached USD 69.3 billion in 2024 and is projected to grow at a CAGR of 4.5% from 2025 to 2034. The market growth trajectory is largely driven by increasing concerns over carbon emissions, particularly in the food industry, prompting a shift toward more sustainable packaging solutions. As global sustainability initiatives gain momentum, companies across industries are adopting environmentally friendly alternatives to reduce their carbon footprint. Flexible paper packaging is emerging as a preferred choice, especially in the food and beverage sectors, due to its lightweight, biodegradable, and recyclable nature. With consumers becoming more conscious of eco-friendly practices, manufacturers are responding by introducing innovative paper-based packaging solutions that align with changing consumer preferences.

Additionally, the rapid expansion of e-commerce is fueling the demand for flexible paper packaging, as online retailers seek lightweight, protective materials that ensure safe and cost-effective delivery of products. The growing focus on waste reduction, coupled with the implementation of stringent environmental regulations, is further accelerating the adoption of flexible paper packaging across industries. As sustainability becomes an industry standard rather than an option, market participants are investing heavily in research and development to create advanced paper packaging materials that offer both functionality and environmental benefits.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $69.3 Billion |

| Forecast Value | $107.6 Billion |

| CAGR | 4.5% |

The flexible paper packaging market encompasses various product types, including roll stock, pouches, shrink sleeves, wraps, and others. Among these, the pouches segment generated USD 27.6 billion in 2024. Pouches are gaining immense popularity due to their versatility, lightweight design, and excellent barrier protection, making them ideal for packaging applications in the food, beverage, and personal care industries. Consumers are increasingly drawn to pouches because of their convenient, resealable, and easy-to-use features. As industries continue to emphasize sustainable, user-friendly packaging solutions, the demand for pouches is anticipated to remain strong. Moreover, technological advancements in pouch manufacturing processes are enhancing their durability and improving the overall consumer experience, making them a go-to choice for brands looking to strengthen their market presence.

In terms of printing technology, the flexible paper packaging market is segmented into categories such as rotogravure, flexography, digital printing, and others. The flexography segment is expected to witness substantial growth, reaching USD 47.3 billion by 2034. Flexography's popularity stems from its ability to utilize low-viscosity inks that dry quickly, enabling faster printing speeds and cost-effective production processes. This technology is highly favored by manufacturers seeking to optimize production efficiency while maintaining superior print quality. With increasing demand for high-quality packaging that enhances brand visibility and shelf appeal, flexography is set to play a pivotal role in meeting these evolving industry requirements. Additionally, the growing emphasis on sustainable inks and printing methods is further bolstering the demand for flexography, positioning it as a key driver of growth in the flexible paper packaging market.

The U.S. Flexible Paper Packaging Market was valued at USD 15.4 billion in 2024 and continues to lead the way in implementing environmentally sustainable practices. U.S. policies such as Extended Producer Responsibility (EPR) are driving improvements in recycling practices and reducing waste in the packaging sector. This regulatory push is encouraging companies to adopt recyclable and biodegradable packaging materials, aligning with broader sustainability goals. As consumer awareness regarding eco-friendly packaging grows, brands operating in the U.S. are making concerted efforts to meet regulatory standards while delivering sustainable solutions that enhance brand loyalty. The country's proactive stance on environmental conservation is setting the stage for continued growth in the flexible paper packaging market as companies strive to balance profitability with environmental responsibility.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Base estimates and calculations

- 1.3.1 Base year calculation

- 1.3.2 Key trends for market estimation

- 1.4 Forecast model

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.5.2 Data mining sources

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Growing demand for sustainable packaging

- 3.2.1.2 Cost-effectiveness compared to rigid packaging

- 3.2.1.3 Increasing consumer preference for convenience

- 3.2.1.4 Advancements in material technology

- 3.2.1.5 Regulatory support for eco-friendly solutions

- 3.2.2 pitfalls and challenges

- 3.2.2.1 Volatility in raw material prices

- 3.2.2.2 High initial capital investment for innovation

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.5 Technology landscape

- 3.6 Future market trends

- 3.7 Gap analysis

- 3.8 Porter's analysis

- 3.9 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategy dashboard

Chapter 5 Market Estimates and Forecast, By Type, 2021 – 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Pouches

- 5.3 Roll stock

- 5.4 Shrink sleeves

- 5.5 Wraps

- 5.6 Others

Chapter 6 Market Estimates and Forecast, By Printing Technology, 2021 – 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Flexography

- 6.3 Rotogravure

- 6.4 Digital printing

- 6.5 Others

Chapter 7 Market Estimates and Forecast, By End Use, 2021 – 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Food and beverage

- 7.3 Retail and consumer goods

- 7.4 Pharmaceuticals and healthcare

- 7.5 Personal care

- 7.6 Others

Chapter 8 Market Estimates and Forecast, By Region, 2021 – 2034 ($ Mn)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Netherlands

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.6 Middle East and Africa

- 8.6.1 Saudi Arabia

- 8.6.2 South Africa

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 Amcor plc

- 9.2 Berry Global Group, Inc.

- 9.3 Constantia Flexibles Group

- 9.4 Coveris Holdings S.A.

- 9.5 DS Smith plc

- 9.6 Graphic Packaging International, LLC

- 9.7 Huhtamaki Oyj

- 9.8 International Paper Company

- 9.9 Mondi Group

- 9.10 ProAmpac Holdings, Inc.

- 9.11 Sealed Air Corporation

- 9.12 Smurfit Kappa Group

- 9.13 Sonoco Products Company

- 9.14 UFlex Limited

- 9.15 WestRock Company