南米の変圧器:市場シェア分析、産業動向・統計、成長予測(2025~2030年)

South America Transformer - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)- 発行日

- ページ情報

- 英文 110 Pages

- 納期

- 2~3営業日

- 商品コード

- 1645081

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 適宜更新あり 本レポートは最新情報反映のため適宜更新し、内容構成変更を行う場合があります。ご検討の際はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

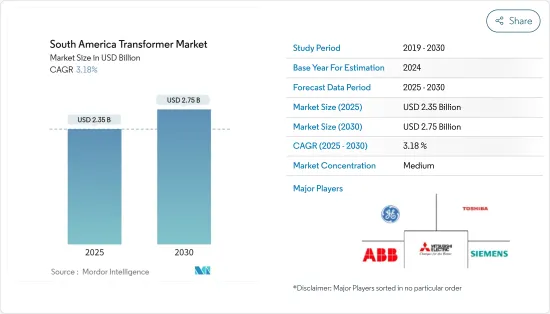

南米の変圧器の市場規模は2025年に23億5,000万米ドルと推定され、予測期間(2025-2030年)のCAGRは3.18%で、2030年には27億5,000万米ドルに達すると予測されます。

主なハイライト

- 長期的には、人口増加に伴う電力需要の増加、再生可能エネルギーによる発電への世界の傾斜、関連する送電インフラの調整といった要因が、予測期間中に南米の変圧器市場を牽引すると予想されます。

- しかし、初期コストの高さや、同地域の社会政治的均衡の脆弱さによる投資家の信頼感の欠如といった課題が、T&D部門への投資流入を抑制すると予想されます。これは予測期間中、同地域の変圧器(特に電力変圧器)需要に悪影響を及ぼす可能性があります。

- スマートグリッド用のスマート変圧器などの技術開発により、変圧器会社の経営に新たな可能性が開かれます。今後数年間、市場関係者には十分なビジネスチャンスが生まれると予想されます。

- ブラジルは予測期間中、南米の変圧器市場で大きな成長が見込まれます。

南米変圧器市場動向

予測期間中、空冷式セグメントが市場を独占する見込み

- 乾式変圧器または空冷式変圧器は、冷却剤として空気を使用するタイプの変圧器です。乾式変圧器には可動部品がなく、環境に優しい温度絶縁システムを採用した静的装置です。乾式変圧器は、油封式変圧器に比べて環境に優しいです。可燃性が低く、火災の危険性も少ないです。高層ビル、空港、スタジアム、ホテル、ショッピングモール、化学・製油所、内陸都市の変電所、農村部、集合住宅など、さまざまな用途で採用されています。

- 南米ではアルゼンチンやブラジルなどで工業化が進んでおり、これが空冷変圧器市場の重要な促進要因となっています。産業が拡大し多様化するにつれて、信頼性が高く堅牢な電気システムへの需要が増加する可能性が高いです。空冷式変圧器は、さまざまな負荷や環境条件を効率的に処理する能力を備えており、産業用途がもたらす課題に対応するのに適しています。

- エネルギー効率と持続可能性を促進する政府の取り組みが、空冷式エネルギー変圧器市場の成長の主な要因となっています。メーカーは変圧器の効率と性能の向上に努めており、技術革新の急増につながっています。

- このような産業の成長は、スマートグリッドや再生可能エネルギープロジェクトの開発と相まって、同地域の空冷式変圧器市場を押し上げると予想されます。例えば、2023年8月、GEヴェルノヴァは、その子会社グリッド・ソリューションズがリオ・グランデ・ド・ノルテ州のサントメ市とキュライス・ノボス市に位置するセーラ・ド・ティグレ風力複合施設向けに2つの500kV空気絶縁変電所(AIS)の建設契約をカサ・ドス・ヴェントスと締結したと発表しました。

- 例えば、アトラス・リニューアブル・エナジー社は2023年11月、ブラジルで902MWの単相プロジェクトを開発するため、ブラジル開発銀行(BNDES)から4億4,780万米ドルを確保したと発表しました。

- 世界エネルギーデータ統計レビューによると、南米では2022年の発電シェアが2021年比で2.6%増加しました。ここ数年の乾式変圧器の需要は、特にブラジル、コロンビア、エクアドル、チリといった国々において、都市化や工業化に伴う電力需要の増加と、乾式変圧器の日々のメンテナンスコストの低さが相まって牽引されてきました。

- 全体として、空冷式変圧器の需要は、南米で電力T&Dインフラの必要性が高まり、多くの危険や環境破壊を伴わずに商業施設や住宅地で使用できるという空冷式変圧器の利点と相まって、予測期間中に増加すると予想されます。

ブラジルは予測期間中に著しい成長が見込まれる

- ブラジルは南米最大のエネルギー消費国です。アルゼンチンと同様、同国のエネルギー部門は主に火力発電所(石油・天然ガス・石炭を含む)に依存しています。世界エネルギー統計レビューによると、2022年には、ブラジルで消費される総エネルギーの50.3%近くが火力発電所で発電され、その他の地域は原子力と再生可能エネルギーで発電されています。

- 運輸と工業は、ブラジルの最終エネルギー消費の75%を占める2大セクターです。国際エネルギー機関(IEA)によると、国家政策シナリオ(STEPS)では、ブラジルのエネルギー消費は2050年までに30%増加すると予想されており、その需要の大半は産業界によるものです。

- 2022年、同国の発電能力は150GWを超え、約677.2テラワット時(TWh)の電力を生み出しました。水力発電は同国で最も利用されている部門であり、2022年の総発電量の約63%を発電しました。その他の分野では、再生可能エネルギーによる発電が約24.2%を占め、残りは火力発電所と原子力発電所によるものです。

- 発電容量の増加は、送配電網インフラへの投資を増加させる可能性が高いです。ブラジル・エネルギー調査庁(EPE)が発表した10カ年拡張計画(PDE 2029)では、2029年まで送電部門に約200億米ドルを投資すると見込まれています。総投資額のうち、140億米ドル近くが送電線に、残りは変電所に投資される見込みです。

- 2022年7月、ブラジル電力規制庁(ANEL)は5,425km以上の送電線を持つ13の送電プロジェクトを発注し、総投資額は29億米ドルを必要としました。これらのプロジェクトは再生可能エネルギーを送電するもので、アクレ州、パラ州、アマパ州、アマゾナス州、バイーア州、マトグロッソ州、マトグロッソ・ド・スル州、ロンドニア州、サンタカタリーナ州、ミナスジェライス州、サンパウロ州、エスピリト・サント州、セルジペ州に建設される予定です。

- 2023年7月、エンギーは同国における1,000kmを超えるトランスミッションの建設に選ばれました。同社は、バイーア州、ミナスジェライス州、エスピリトサント州における送電線の設計、建設、運営・保守を行う30年間のコンセッションを獲得しました。プロジェクトの推定投資額は約5億5,700万米ドルです。

- ブラジル鉱業エネルギー省は、2021年から2031年にかけて、集中型発電に540億米ドル、分散型発電に250億米ドル、トランスミッションに190億米ドルを含む970億米ドルの電力部門への投資を見込む「10カ年エネルギー拡張計画2031」に関する公開協議も開始しました。

- そのため、送電線プロジェクトに対するこのような投資により、今後数年間、ブラジルでは変圧器の需要が創出されると予想されます。

南米の変圧器産業の概要

南米の変圧器市場は細分化されています。同市場の主要企業(順不同)には、ABB Ltd、シーメンスAG、ゼネラル・エレクトリック社、東芝、三菱電機が含まれます。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリスト・サポート

目次

第1章 イントロダクション

- 調査範囲

- 市場の定義

- 調査の前提

第2章 エグゼクティブサマリー

第3章 調査手法

第4章 市場概要

- イントロダクション

- 2029年までの市場規模および需要予測(単位:米ドル)

- 最近の動向と開発

- 政府の規制と政策

- 市場力学

- 促進要因

- 世界の再生可能エネルギー発電への傾斜

- 人口増加に伴う電力需要の増加

- 抑制要因

- 初期コストの高さ

- 促進要因

- サプライチェーン分析

- 業界の魅力度-ポーターのファイブフォース分析

- 供給企業の交渉力

- 消費者の交渉力

- 新規参入業者の脅威

- 代替品の脅威製品・サービス

- 競争企業間の敵対関係

第5章 市場セグメンテーション

- 定格電力別

- 大型

- 中型

- 小型

- 冷却タイプ別

- 空冷

- 油冷式

- フェーズ別

- 単相

- 三相

- 変圧器タイプ別

- 電力用変圧器

- 配電変圧器

- 地域別

- アルゼンチン

- ブラジル

- チリ

- コロンビア

- その他南米

第6章 競合情勢

- M&A、合弁事業、提携、協定

- 主要企業の戦略

- 企業プロファイル

- WEG Industries

- Schneider Electric SE

- Siemens AG

- Hyosung Heavy Industries Corporation

- ABB Ltd

- General Electric Company

- Eaton Corporation PLC

- Hitachi Energy Ltd

- Toshiba Corporation

- HD Hyundai Electric Co. Ltd

- 市場ランキング分析

第7章 市場機会と今後の動向

- スマート変圧器などの技術革新

目次

Product Code: 50002097

The South America Transformer Market size is estimated at USD 2.35 billion in 2025, and is expected to reach USD 2.75 billion by 2030, at a CAGR of 3.18% during the forecast period (2025-2030).

Key Highlights

- Over the long term, factors such as growing power demand in line with the increasing population, a global inclination toward renewable-based power generation, and related adjustments in the transmission infrastructure are expected to drive the transformers market in South America during the forecast period.

- However, challenges like high initial cost and lack of investor confidence due to the fragility of the sociopolitical equilibrium of the region are expected to restrain the inflow of investments in the T&D sector. This may negatively impact the demand for transformers (especially power transformers) in the region during the forecast period.

- Technological developments, such as smart transformers for smart grids, open up new potential for transformer company operations. It is expected to create ample opportunities for market players in the coming years.

- Brazil is expected to witness significant growth in the South American transformer market during the forecast period.

South America Transformer Market Trends

Air-cooled Segment is Expected to Dominate the Market during the Forecast Period

- A dry-type transformer or air-cooled transformer is a type of transformer that uses air as a coolant. A dry-type transformer has no moving parts and is a static device that uses eco-friendly temperature insulation systems. The dry-type transformer is more eco-friendly compared to the oil-filled type transformer. It is less flammable and poses a lesser fire risk. It is employed in various applications, including high-rise buildings, airports, stadiums, hotels, shopping malls, chemical and refinery plants, substations for interior cities, rural areas, and residential complexes.

- The ongoing industrialization in South America in countries like Argentina and Brazil is a crucial driver for the air-cooled transformers market. As industries expand and diversify, the demand for reliable and robust electrical systems is likely to increase. Air-cooled transformers, with their ability to efficiently handle varying loads and environmental conditions, are well-suited to meet the challenges posed by industrial applications.

- Government initiatives to promote energy efficiency and sustainability have been a major factor in the growth of the air-cooled energy transformer market. Manufacturers have been striving to improve the efficiency and performance of their transformers, leading to a surge in technological innovation.

- This industrial growth, coupled with the development of smart grids and renewable energy projects, is expected to boost the market for air-cooled transformers in the region. For instance, in August 2023, GE Vernova announced that its subsidiary Grid Solutions had signed a contract with Casa dos Ventos for the construction of two 500 kV air-insulated substations (AIS) for the Serra do Tigre Wind Complex located in the municipalities of Sao Tome and Currais Novos in the state of Rio Grande do Norte.

- For instance, in November 2023, Atlas Renewable Energy announced that the company had secured USD 447.8 million from the Brazilian Development Bank (BNDES) to develop a 902MW single-phase project in Brazil.

- According to the Statistical Review of World Energy Data, in South America, the share of electricity generation increased by 2.6% in 2022 compared to 2021. The demand for dry-type transformers over the past years has been driven by the increasing demand for electricity on account of urbanization and industrialization, coupled with the low daily maintenance cost of dry-type transformers, especially in countries like Brazil, Colombia, Ecuador, and Chile.

- Overall, the demand for air-cooled transformers is expected to increase during the forecast period as the need for power T&D infrastructure increases in South America, coupled with the advantages of the air-cooled transformer to be used in commercial and residential places without many hazards and environmental damage.

Brazil is Expected to Witness Significant Growth during the Forecast Period

- Brazil is the largest energy consumer in South America. Like Argentina, the country's energy sector mainly relies on thermal power plants (including oil, natural gas, and coal). According to the Statistical Review of World Energy, in 2022, nearly 50.3% of the total energy consumed in Brazil was generated from thermal power plants, while the rest was generated through nuclear and renewable.

- Transportation and industry are the two most significant sectors that account for 75% of final energy consumption in Brazil. According to the International Energy Agency (IEA), in the Stated Policies Scenario (STEPS), the country is expected to witness 30% growth in energy consumption by 2050, with most demand coming from the industries.

- In 2022, the country had more than 150 GW of power generating capacity, which generated nearly 677.2 terawatt-hours (TWh) of electricity. Hydroelectric was the most utilized sector in the country, generating nearly 63% of the total electricity in 2022. Among the other sectors, renewable generated around 24.2% of the electricity, while the rest was generated from thermal and nuclear power plants.

- Growth in generation capacity is likely to increase investment in transmission and distribution grid infrastructure. Under the 10-year expansion plan (PDE 2029) published by the Brazilian Energy Research Agency (EPE), the country is expected to invest around USD 20 billion in the electricity transmission sector until 2029. Out of the total investment, nearly USD 14 billion will be in the transmission lines, while the remaining is expected to be in the substations.

- In July 2022, the Brazilian Electricity Regulatory Agency (ANEL) awarded 13 power transmission projects with more than 5,425 km of lines, requiring a total investment of USD 2.9 billion. The projects are likely to transmit renewable energy and are expected to be built in the Acre, Para, Amapa, Amazonas, Bahia, Mato Grosso, Mato Grosso do Sul, Rondonia, Santa Catarina, Minas Gerais, Sao Paulo, Espirito Santo, and Sergipe.

- In July 2023, Engie was selected to build more than 1,000 km of power transmission lines in the country. The company received a 30-year concession to design, construct, and offer operations and maintenance of the transmission lines in the states of Bahia, Minas Gerais, and Espirito Santo. The estimated investment of the project would be around USD 557 million.

- The Brazilian Ministry of Mines and Energy also initiated a public consultation on the Ten-Year Energy Expansion Plan 2031, which foresees the investment of USD 97 billion in the electricity sector over 2021-2031, including USD 54 billion in centralized generation, USD 25 billion in distributed generation, and USD 19 billion in transmission.

- Thus, such investments in transmission line projects are anticipated to create demand for transformers in Brazil in the upcoming years.

South America Transformer Industry Overview

The South American transformer market is semi-fragmented. Some of the major players in the market (in no particular order) include ABB Ltd, Siemens AG, General Electric Company, Toshiba Corporation, and Mitsubishi Electric Corporation.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Scope of the Study

- 1.2 Market Definition

- 1.3 Study Assumptions

2 EXECUTIVE SUMMARY

3 RESEARCH METHODOLOGY

4 MARKET OVERVIEW

- 4.1 Introduction

- 4.2 Market Size and Demand Forecast in USD, till 2029

- 4.3 Recent Trends and Developments

- 4.4 Government Policies and Regulations

- 4.5 Market Dynamics

- 4.5.1 Drivers

- 4.5.1.1 Global Inclination toward Renewable-based Power Generation

- 4.5.1.2 Increased Power Demand in Line with the Increasing Population

- 4.5.2 Restraints

- 4.5.2.1 High Initial Cost

- 4.5.1 Drivers

- 4.6 Supply Chain Analysis

- 4.7 Industry Attractiveness - Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Consumers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes Products and Services

- 4.7.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 By Power Rating

- 5.1.1 Large

- 5.1.2 Medium

- 5.1.3 Small

- 5.2 By Cooling Type

- 5.2.1 Air Cooled

- 5.2.2 Oil Cooled

- 5.3 By Phase

- 5.3.1 Single Phase

- 5.3.2 Three Phase

- 5.4 By Transformer Type

- 5.4.1 Power Transformer

- 5.4.2 Distribution Transformer

- 5.5 By Geography

- 5.5.1 Argentina

- 5.5.2 Brazil

- 5.5.3 Chile

- 5.5.4 Colombia

- 5.5.5 Rest of South America

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Strategies Adopted by Leading Players

- 6.3 Company Profiles

- 6.3.1 WEG Industries

- 6.3.2 Schneider Electric SE

- 6.3.3 Siemens AG

- 6.3.4 Hyosung Heavy Industries Corporation

- 6.3.5 ABB Ltd

- 6.3.6 General Electric Company

- 6.3.7 Eaton Corporation PLC

- 6.3.8 Hitachi Energy Ltd

- 6.3.9 Toshiba Corporation

- 6.3.10 HD Hyundai Electric Co. Ltd

- 6.4 Market Ranking Analysis

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Technological Innovations like Smart Transformers

南米の変圧器:市場シェア分析、産業動向・統計、成長予測(2025~2030年)

- 発行日

- 発行

- Mordor Intelligence

- ページ情報

- 英文 110 Pages

- 納期

- 2~3営業日