|

市場調査レポート

商品コード

1716487

使い捨てプレート市場の機会、成長促進要因、産業動向分析、2025年~2034年の予測Disposable Plates Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| 使い捨てプレート市場の機会、成長促進要因、産業動向分析、2025年~2034年の予測 |

|

出版日: 2025年03月05日

発行: Global Market Insights Inc.

ページ情報: 英文 220 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

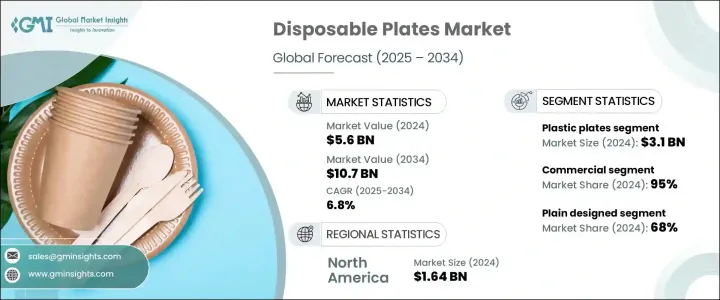

世界の使い捨てプレート市場は2024年に56億米ドルに達し、2025年から2034年にかけてCAGR 6.8%で拡大すると予測されています。

市場成長の主な要因は、持続可能な生活へのシフトの高まりと、従来の食器に代わる環境に優しい食器への需要の高まりです。消費者の環境意識の高まりに伴い、生分解性、堆肥化可能、リサイクル素材から作られた使い捨てプレートへの嗜好が顕著になっています。カーボンフットプリントを削減し、使い捨てプラスチック廃棄物を最小限に抑えることへの関心が高まっていることが、この市場の軌道を形成する重要な促進要因となっています。さらに、フードデリバリー・サービス、ケータリング・ビジネス、クイックサービス・レストランの急増が、便利で持続可能なダイニング・ソリューションへのニーズを高めています。

持続可能性と倫理的調達に沿った製品を優先する消費者が増える中、メーカーはサトウキビバガス、竹、ヤシの葉、コーンスターチベースの素材など再生可能な資源からプレートを開発することで対応しています。これらの環境に優しいプレートは、耐久性や美観を損なうことなく、実用的な代替品を提供します。さらに、プラスチック廃棄物の抑制や環境に配慮した包装の奨励を目的とした政府規制の増加は、市場プレーヤーに新たな機会を生み出しています。大規模なイベント、企業の集まり、公共の場でエコ・フレンドリー・プレートの採用が増加しているのは、環境責任に対する幅広い文化的シフトを反映しています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 56億米ドル |

| 予測金額 | 107億米ドル |

| CAGR | 6.8% |

市場はプラスチック、アルミ、紙、その他素材など製品タイプ別に区分され、紙皿は2025年から2034年にかけてCAGR 7.3%が見込まれます。紙皿は、生分解性、廃棄の容易さ、幅広い食品との適合性により、大きな人気を集めています。消費者はますますプラスチック皿から離れつつあり、プラスチック皿は環境に悪影響を与えるとして厳しい監視の目を向けられています。業界では、植物由来のプラスチックから作られた製品や、プラスチックの特性を模倣しながらも有毒な残留物を残さずに自然に分解されるバイオコーティング素材など、革新的な生分解性代替品への移行が急速に進んでいます。その結果、紙皿は、実用的で環境に配慮したソリューションを目指す消費者と企業の両方にとって、好ましい選択肢として浮上しています。

最終用途に基づき、使い捨てプレート市場は住宅用と商業用に分類され、2024年には商業用が全体のシェアの95%を占める。商業分野には、給食業者、ケータリング会社、飲食品センターなどが含まれ、その利便性と費用対効果の高さから、使い捨てプレートの高い需要を牽引し続けています。これらの施設では、丈夫さ、エレガントな外観、漏れたり割れたりすることなく熱い食べ物も冷たい食べ物も保持できることに惹かれて、ヤシの葉プレートを採用するところが増えています。このような持続可能なオプションを使用することで、企業は環境意識の高い顧客にアピールすることができ、それによってブランドの評判を高めることもできます。

米国の使い捨てプレート市場は76%のシェアを占め、2024年には16億4,000万米ドルを稼ぎ出します。米国市場は、環境持続可能性への強い後押しと、環境に優しい製品への顕著な消費者シフトから利益を得ています。テイクアウトの食事や飲料の人気とともに、外出の多いライフスタイルのペースが増加していることが、同国における使い捨てプレートの需要増に大きく寄与しています。消費者が利便性と環境への影響を優先する中、使い捨て皿のような使い捨て製品は、現代的でペースの速い生活に沿った実用的なソリューションを提供し続けています。

目次

第1章 調査手法と調査範囲

第2章 エグゼクティブサマリー

第3章 業界洞察

- エコシステム分析

- バリューチェーンに影響を与える要因。

- 利益率分析

- ディスラプション

- 将来の展望

- 製造業者

- 流通業者

- サプライヤーの状況

- 主なニュースと取り組み

- 規制状況

- 影響要因

- 促進要因

- 環境意識の高まり

- 環境にやさしい製品に対する消費者の需要

- 業界の潜在的リスク&課題

- 再利用可能な代替品へのシフト

- 従来のプラスチックとの競合

- 促進要因

- 成長可能性分析

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業シェア分析

- 競合のポジショニング・マトリックス

- 戦略展望マトリックス

第5章 市場推計・予測:製品タイプ別、2021年~2034年

- 主要動向

- プラスチックプレート

- アルミプレート

- 紙製プレート

- その他(リーフプレート、麦わらプレートなど)

第6章 市場推計・予測:デザイン別、2021年~2034年

- 主要動向

- コンパートメント

- プレーン

第7章 市場推計・予測:価格別、2021年~2034年

- 主要動向

- 低価格

- 中価格

- 高価格

第8章 市場推計・予測:最終用途別、2021年~2034年

- 主要動向

- 住宅用

- 商業

- 飲食品

- ホテル・カフェ

- ホスピタリティとイベント

- その他(クイックサービスレストランなど)

第9章 市場推計・予測:流通チャネル別、2021年~2034年

- 主要動向

- オンライン

- 企業ウェブサイト

- eコマース

- オフライン

- スーパーマーケット/ハイパーマーケット

- 専門店

- その他(外食業者など)

第10章 市場推計・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- 英国

- ドイツ

- フランス

- イタリア

- スペイン

- ロシア

- アジア太平洋

- 中国

- インド

- 日本

- 韓国

- オーストラリア

- ラテンアメリカ

- ブラジル

- メキシコ

- 中東・アフリカ

- UAE

- サウジアラビア

- 南アフリカ

第11章 企業プロファイル

- D&W Fine Pack

- Dart Container Corporation

- Dopla

- Duni

- Fast Plast

- Genpak

- Georgia-Pacific

- Hotpack Group

- Huhtamaki

- International Paper

- Pactiv

- Polar Plastic

- Poppies Europe

- Seow Khim Polythelene

- Vegware

The Global Disposable Plates Market reached USD 5.6 billion in 2024 and is projected to expand at a CAGR of 6.8% from 2025 to 2034. The market growth is largely fueled by the rising shift toward sustainable living and the increasing demand for eco-friendly alternatives to traditional tableware. With growing environmental awareness among consumers, there is a notable preference for disposable plates made from biodegradable, compostable, and recycled materials. The expanding focus on reducing carbon footprints and minimizing single-use plastic waste has been a key driver shaping this market's trajectory. Additionally, the surge in food delivery services, catering businesses, and quick-service restaurants has amplified the need for convenient and sustainable dining solutions.

As more consumers prioritize products aligned with sustainability and ethical sourcing, manufacturers are responding by developing plates from renewable resources such as sugarcane bagasse, bamboo, palm leaves, and cornstarch-based materials. These eco-friendly plates offer a practical alternative without compromising on durability and aesthetics. Furthermore, increasing governmental regulations aimed at curbing plastic waste and encouraging green packaging practices are creating new opportunities for market players. The rising adoption of eco-friendly plates at large-scale events, corporate gatherings, and public venues reflects a broader cultural shift toward environmental responsibility.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $5.6 Billion |

| Forecast Value | $10.7 Billion |

| CAGR | 6.8% |

The market is segmented by product type, including plastic, aluminum, paper, and other materials, with paper plates expected to witness a 7.3% CAGR from 2025 to 2034. Paper plates are gaining massive popularity due to their biodegradable nature, ease of disposal, and compatibility with a wide range of food products. Consumers are increasingly steering away from plastic plates, which are under heavy scrutiny for their adverse environmental impact. The industry is seeing a rapid shift toward innovative biodegradable alternatives, including products made from plant-based plastics and bio-coated materials that mimic the properties of plastic but break down naturally without leaving toxic residues. As a result, paper plates are emerging as the preferred choice for both consumers and businesses aiming for practical and eco-conscious solutions.

Based on end-use, the disposable plates market is classified into residential and commercial sectors, with commercial applications accounting for 95% of the overall share in 2024. The commercial segment, which includes food service providers, catering companies, and beverage centers, continues to drive high demand for disposable plates due to their convenience and cost-effectiveness. Increasingly, these establishments are adopting palm leaf plates, drawn to their sturdiness, elegant appearance, and ability to hold both hot and cold foods without leakage or breakage. The use of such sustainable options also allows businesses to appeal to environmentally aware customers, thereby enhancing their brand reputation.

U.S. Disposable Plates Market dominated the global landscape with a 76% share, generating USD 1.64 billion in 2024. The U.S. market benefits from a strong push toward environmental sustainability and a marked consumer shift toward eco-friendly products. The increasing pace of on-the-go lifestyles, along with the popularity of takeout meals and beverages, has significantly contributed to the rising demand for disposable plates in the country. With consumers prioritizing convenience and environmental impact, single-use products such as disposable plates continue to offer practical solutions that align with modern, fast-paced living.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope & definitions

- 1.2 Base estimates & calculations

- 1.3 Forecast calculations.

- 1.4 Data sources

- 1.4.1 Primary

- 1.4.2 Secondary

- 1.4.2.1 Paid sources

- 1.4.2.2 Public sources

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021-2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Factor affecting the value chain.

- 3.1.2 Profit margin analysis.

- 3.1.3 Disruptions

- 3.1.4 Future outlook

- 3.1.5 Manufactures

- 3.1.6 Distributors

- 3.2 Supplier landscape

- 3.3 Key news & initiatives

- 3.4 Regulatory landscape

- 3.5 Impact forces

- 3.5.1 Growth drivers

- 3.5.1.1 Increased environmental awareness

- 3.5.1.2 Consumer demand for eco-friendly products

- 3.5.2 Industry pitfalls & challenges

- 3.5.2.1 Shift toward reusable alternatives

- 3.5.2.2 Competition from traditional plastics

- 3.5.1 Growth drivers

- 3.6 Growth potential analysis

- 3.7 Porter's analysis

- 3.8 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Product Type, 2021-2034 (USD Billion) (Million Units)

- 5.1 Key trends

- 5.2 Plastic plates

- 5.3 Aluminum plates

- 5.4 Paper plates

- 5.5 Others (leaf plates, wheat straw plates etc.)

Chapter 6 Market Estimates & Forecast, By Design, 2021-2034 (USD Billion) (Million Units)

- 6.1 Key trends

- 6.2 Compartmental

- 6.3 Plain

Chapter 7 Market Estimates & Forecast, By Price, 2021-2034 (USD Billion) (Million Units)

- 7.1 Key trends

- 7.2 Low

- 7.3 Medium

- 7.4 High

Chapter 8 Market Estimates & Forecast, By End Use, 2021-2034 (USD Billion) (Million Units)

- 8.1 Key trends

- 8.2 Residential

- 8.3 Commercial

- 8.3.1 Food & beverage

- 8.3.2 Hotels and cafes

- 8.3.3 Hospitality and events

- 8.3.4 Others (quick-service restaurants etc.)

Chapter 9 Market Estimates & Forecast, By Distribution Channel, 2021-2034 (USD Billion) (Million Units)

- 9.1 Key trends

- 9.2 Online

- 9.2.1 Company websites

- 9.2.2 E-commerce

- 9.3 Offline

- 9.3.1 Supermarkets/hypermarkets

- 9.3.2 Specialty stores

- 9.3.3 Others (foodservice suppliers etc.)

Chapter 10 Market Estimates & Forecast, By Region, 2021-2034 (USD Billion) (Million Units)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 UK

- 10.3.2 Germany

- 10.3.3 France

- 10.3.4 Italy

- 10.3.5 Spain

- 10.3.6 Russia

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 South Korea

- 10.4.5 Australia

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.6 MEA

- 10.6.1 UAE

- 10.6.2 Saudi Arabia

- 10.6.3 South Africa

Chapter 11 Company Profiles

- 11.1 D&W Fine Pack

- 11.2 Dart Container Corporation

- 11.3 Dopla

- 11.4 Duni

- 11.5 Fast Plast

- 11.6 Genpak

- 11.7 Georgia-Pacific

- 11.8 Hotpack Group

- 11.9 Huhtamaki

- 11.10 International Paper

- 11.11 Pactiv

- 11.12 Polar Plastic

- 11.13 Poppies Europe

- 11.14 Seow Khim Polythelene

- 11.15 Vegware