|

市場調査レポート

商品コード

1698232

紙コップ市場の機会、成長促進要因、産業動向分析、2025年~2034年の予測Paper Cups Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025-2034 |

||||||

カスタマイズ可能

|

|||||||

| 紙コップ市場の機会、成長促進要因、産業動向分析、2025年~2034年の予測 |

|

出版日: 2025年02月27日

発行: Global Market Insights Inc.

ページ情報: 英文 180 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

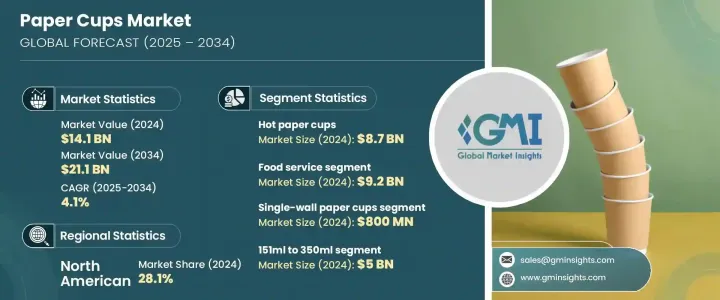

世界の紙コップ市場は2024年に141億米ドルと評価され、2025年から2034年にかけてCAGR 4.1%で成長すると予測されています。

この拡大には、便利で持ち運び可能な飲料オプションに対する消費者需要の増加と、世界のスペシャルティコーヒーショップや独立系カフェの人気の高まりが拍車をかけています。都市消費者のライフスタイル嗜好の進化と持続可能性への世界の後押しが、革新的で環境に優しい紙コップ・ソリューションへのニーズを後押ししています。より多くの消費者が職人的でプレミアムなコーヒー体験を求める中、カフェやクイックサービスレストランは高品質で持続可能な紙コップを採用することで対応しています。こうした動向は、環境に配慮したパッケージングへの業界全体のシフトを反映しており、消費者の期待と規制要件の両方を満たすことを目指す紙カップメーカーに有利な機会を生み出しています。

持続可能性が重視されるようになったことで、従来のプラスチックコーティング紙コップに代わる生分解性や堆肥化可能な紙コップへの投資が増加しています。使い捨てプラスチックに対する政府の規制が強化される中、メーカーは環境への影響を抑えながら優れた断熱性を提供するバイオベースやポリ乳酸(PLA)素材のコーティングを施した紙コップを積極的に開発しています。さらに、消費者の健康意識の高まりから、化学物質を含まず、リサイクル可能な紙コップが好まれるようになり、様々な最終用途分野での需要がさらに高まっています。また、企業はブランディングとカスタマイズの重要性を認識しており、顧客エンゲージメントとマーケティング活動を強化する印刷されたブランド紙コップの需要急増につながっています。これらの要因が総合的に世界の紙コップ市場の力強い成長軌道に寄与しています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 141億米ドル |

| 予測金額 | 211億米ドル |

| CAGR | 4.1% |

紙コップ市場は、ホット紙コップとコールド紙コップの2つの主要カテゴリーに区分されます。2024年には、ホット紙コップ分野は87億米ドルの売上高を占め、コーヒーや紅茶などの外出先でのホット飲料の需要急増がその原動力となっています。都市化とペースの速いライフスタイルが、特にクイックサービス・レストランやカフェでのホット飲料消費の増加に大きく寄与しています。このセグメントにおける持続可能なソリューションの必要性から、メーカーは従来のポリエチレン(PE)コーティングから環境に優しい代替品へと移行し、断熱性と持続可能性の両方を高めています。消費者の嗜好が進化を続ける中、保温性の向上やこぼれにくい蓋など、カップのデザインにおけるイノベーションが支持を集め、市場の成長をさらに強めています。

市場はまた、最終用途に基づいて分類されており、外食、施設、家庭の各セグメントが含まれます。外食産業セグメントは、クイックサービスレストランの急速な拡大、宅配・持ち帰りサービスの急増、使い捨てでありながら持続可能な飲料包装を好む消費者習慣の進化などが追い風となり、2024年の評価額が92億米ドルで市場をリードしました。さらに、プラスチック廃棄物処理に関する規制圧力の高まりが、生分解性と堆肥化可能な紙コップの採用を加速させており、市場の需要をさらに押し上げています。

北米紙コップ市場は2024年に28.1%のシェアを占めたが、これは持続可能な包装材料に対する消費者の嗜好の高まりと、外出先での飲料市場の拡大によるものです。使い捨てプラスチックの禁止など、プラスチック廃棄物の削減を目的とした政府の取り組みが、この地域全体で環境に優しい紙コップの採用を大幅に後押ししています。企業はこうした持続可能性の動向にますます歩調を合わせるようになっており、市場の今後の成長見通しを強めています。

目次

第1章 調査手法と調査範囲

第2章 エグゼクティブサマリー

第3章 業界洞察

- エコシステム分析

- 業界への影響要因

- 促進要因

- コンビニエンス&オンザゴー飲料への需要の高まり

- 持続可能で環境に優しいパッケージング

- 紙カップコーティング技術の進歩

- スペシャルティコーヒーショップと独立系カフェの成長

- カスタマイズとブランディングの機会

- 業界の潜在的リスク&課題

- 原材料価格の変動

- サプライチェーンの混乱

- 促進要因

- 成長可能性分析

- 規制状況

- 技術情勢

- 将来の市場動向

- ギャップ分析

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業シェア分析

- 主要市場プレーヤーの競合分析

- 競合のポジショニングマトリックス

- 戦略ダッシュボード

第5章 市場推計・予測:タイプ別、2021年~2034年

- 主要動向

- ホット用紙コップ

- コールド用紙コップ

第6章 市場推計・予測:ウォールタイプ別、2021年~2034年

- 主要動向

- シングルウォール紙コップ

- ダブルウォール紙コップ

- トリプルウォール紙コップ

第7章 市場推計・予測:容量別、2021~2034年

- 主要動向

- 150mlまで

- 151~350ml

- 351~500ml

- 500ml以上

第8章 市場推計・予測:最終用途別、2021年~2034年

- 主要動向

- フードサービス

- クイックサービスレストラン(QSR)

- カフェ・喫茶店

- その他

- アイスクリーム・パーラー、FSR

- 施設

- 家庭

第9章 市場推計・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- スペイン

- イタリア

- オランダ

- アジア太平洋

- 中国

- インド

- 日本

- オーストラリア

- 韓国

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- サウジアラビア

- 南アフリカ

- アラブ首長国連邦

第10章 企業プロファイル

- Bender

- Converpack

- Dart Container

- Detmold

- Dispo

- Genpak

- Georgia-Pacific

- Golden Paper Cups

- Graphic Packaging

- Grupo Phoenix

- Huhtamaki

- Ishwara

- Nippon Paper

- Printed Cup Company

- Seda

- Stanpac

- Stora Enso

- Tekni-Plex

- Westrock

The Global Paper Cups Market was valued at USD 14.1 billion in 2024 and is projected to grow at a CAGR of 4.1% from 2025 to 2034. This expansion is fueled by increasing consumer demand for convenient, portable beverage options and the rising popularity of specialty coffee shops and independent cafes worldwide. The evolving lifestyle preferences of urban consumers, coupled with the global push toward sustainability, are driving the need for innovative and eco-friendly paper cup solutions. As more consumers seek out artisanal and premium coffee experiences, cafes and quick-service restaurants are responding by adopting high-quality, sustainable paper cups. These trends reflect a broader industry shift toward environmentally responsible packaging, creating lucrative opportunities for paper cup manufacturers aiming to meet both consumer expectations and regulatory requirements.

The growing emphasis on sustainability has led to increased investment in biodegradable and compostable alternatives to traditional plastic-coated paper cups. With mounting government regulations on single-use plastics, manufacturers are actively developing paper cups with coatings made from bio-based and polylactic acid (PLA) materials, which offer superior insulation while reducing environmental impact. Additionally, rising health awareness among consumers has led to a preference for chemical-free, recyclable paper cups, further driving demand across various end-use sectors. Businesses are also recognizing the importance of branding and customization, leading to a surge in demand for printed and branded paper cups that enhance customer engagement and marketing efforts. These factors collectively contribute to the strong growth trajectory of the global paper cups market.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $14.1 Billion |

| Forecast Value | $21.1 Billion |

| CAGR | 4.1% |

The paper cups market is segmented into two main categories: hot and cold paper cups. In 2024, the hot paper cups segment accounted for USD 8.7 billion in revenue, driven by the surging demand for on-the-go hot beverages such as coffee and tea. Urbanization and fast-paced lifestyles have significantly contributed to the increased consumption of hot beverages, particularly from quick-service restaurants and cafes. The need for sustainable solutions in this segment has led manufacturers to shift from conventional polyethylene (PE) coatings to eco-friendly alternatives, enhancing both insulation and sustainability. As consumer preferences continue to evolve, innovations in cup design, including improved heat retention and spill-resistant lids, are gaining traction, further strengthening market growth.

The market is also categorized based on end-use applications, including foodservice, institutional, and household segments. The foodservice segment led the market with a valuation of USD 9.2 billion in 2024, fueled by the rapid expansion of quick-service restaurants, the surge in food delivery and takeaway services, and evolving consumer habits favoring disposable yet sustainable beverage packaging. Additionally, increasing regulatory pressures on plastic waste disposal are accelerating the adoption of biodegradable and compostable paper cups, further bolstering market demand.

North America Paper Cups Market accounted for a 28.1% share in 2024, driven by the growing consumer preference for sustainable packaging materials and the expanding market for on-the-go beverages. Government initiatives aimed at reducing plastic waste, including bans on single-use plastics, have significantly boosted the adoption of eco-friendly paper cups across the region. Businesses are increasingly aligning with these sustainability trends, reinforcing the market's growth outlook in the years to come.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Base estimates and calculations

- 1.3.1 Base year calculation

- 1.3.2 Key trends for market estimation

- 1.4 Forecast model

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.5.2 Data mining sources

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rise in demand for convenience & on-the-go beverages

- 3.2.1.2 Sustainable and eco-friendly packaging

- 3.2.1.3 Advancements in paper cup coating technologies

- 3.2.1.4 Growth of specialty coffee shops & independent cafes

- 3.2.1.5 Customization & branding opportunities

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Fluctuating raw material price

- 3.2.2.2 Supply chain disruption

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.5 Technology landscape

- 3.6 Future market trends

- 3.7 Gap analysis

- 3.8 Porter’s analysis

- 3.9 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategy dashboard

Chapter 5 Market Estimates and Forecast, By Type, 2021 – 2034 (USD Billion & Kilo Tons)

- 5.1 Key trends

- 5.2 Hot paper cups

- 5.3 Cold paper cups

Chapter 6 Market Estimates and Forecast, By Wall Type, 2021 – 2034 (USD Billion & Kilo Tons)

- 6.1 Key trends

- 6.2 Single wall paper cups

- 6.3 Double wall paper cups

- 6.4 Triple wall paper cups

Chapter 7 Market Estimates and Forecast, By Capacity, 2021 – 2034 (USD Billion & Kilo Tons)

- 7.1 Key trends

- 7.2 Up to 150 ml

- 7.3 151 to 350 ml

- 7.4 351 to 500 ml

- 7.5 Above 500 ml

Chapter 8 Market Estimates and Forecast, By End Use, 2021 – 2034 (USD Billion & Kilo Tons)

- 8.1 Key trends

- 8.2 Foodservice

- 8.2.1 Quick service restaurants (QSRs)

- 8.2.2 Cafes and coffee shops

- 8.2.3 Others

- 8.2.3.1 Ice cream parlour, FSR

- 8.3 Institutional

- 8.4 Household

Chapter 9 Market Estimates and Forecast, By Region, 2021 – 2034 (USD Billion & Kilo Tons)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Netherlands

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 Middle East and Africa

- 9.6.1 Saudi Arabia

- 9.6.2 South Africa

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 Bender

- 10.2 Converpack

- 10.3 Dart Container

- 10.4 Detmold

- 10.5 Dispo

- 10.6 Genpak

- 10.7 Georgia-Pacific

- 10.8 Golden Paper Cups

- 10.9 Graphic Packaging

- 10.10 Grupo Phoenix

- 10.11 Huhtamaki

- 10.12 Ishwara

- 10.13 Nippon Paper

- 10.14 Printed Cup Company

- 10.15 Seda

- 10.16 Stanpac

- 10.17 Stora Enso

- 10.18 Tekni-Plex

- 10.19 Westrock