|

市場調査レポート

商品コード

1708244

自動車用プレミアムタイヤ市場の機会、成長促進要因、産業動向分析、2025年~2034年の予測Automotive Premium Tires Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| 自動車用プレミアムタイヤ市場の機会、成長促進要因、産業動向分析、2025年~2034年の予測 |

|

出版日: 2025年03月31日

発行: Global Market Insights Inc.

ページ情報: 英文 180 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

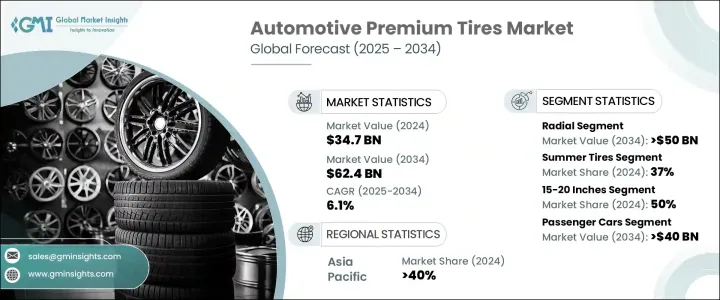

自動車用プレミアムタイヤの世界市場規模は2024年に347億米ドルとなり、2025年から2034年にかけてCAGR 6.1%で成長すると予測されています。

この成長の主な要因は、高級車や高性能車に対する需要の増加であり、自動車メーカーは車の性能、快適性、安全性を高めるために優れたタイヤ品質を優先しています。消費者の嗜好が先進的なドライビングダイナミクスを提供する自動車へとシフトする中、プレミアムタイヤメーカーはトレッドコンパウンドの強化、先進的なゴム配合、サイドウォール構造の改良といった技術革新を続けています。電気自動車(EV)の採用が増加していることも市場拡大に寄与しています。EV用に設計されたプレミアムタイヤは転がり抵抗が小さく、効率が向上し、騒音が低減されるからです。

持続可能なモビリティの重視により、プレミアムタイヤ分野の研究開発活動が活発化しています。タイヤメーカーは、環境に優しい原材料、革新的なトレッド設計、最先端技術を取り入れ、優れたグリップ力、長寿命、燃費効率を提供する製品を生み出しています。ブレーキ性能の向上、騒音レベルの低下、路面グリップの向上など、高性能タイヤの利点に対する消費者の意識の高まりが、市場の成長をさらに加速させています。さらに、規制当局が安全性と燃費に関する規制を強化しているため、自動車メーカーは厳しい基準を満たした高品質のタイヤを車両に装備することを余儀なくされています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 347億米ドル |

| 予測金額 | 624億米ドル |

| CAGR | 6.1% |

市場はタイヤの構造によってラジアルタイヤとバイアスタイヤに区分されます。2024年には、ラジアルタイヤが市場シェアの80%を占め、2034年には500億米ドルの市場規模が見込まれます。ラジアルタイヤは柔軟性が高く、トラクションに優れ、トレッド寿命が長いため、プレミアムタイヤ市場で好まれています。スチールベルト構造は熱の蓄積を最小限に抑え、燃費を向上させ、タイヤの寿命を延ばします。ラジアルタイヤは、高速走行時の安定性と厳しい走行条件下でも形状を維持する能力から、高性能車の需要が増加する中、依然として好んで選ばれており、市場の拡大にさらに拍車をかけています。

市場はまた、夏用タイヤ、冬用タイヤ、オールシーズンタイヤ、全地形対応タイヤ、その他を含むタイヤタイプ別に分類されます。2024年には、夏用タイヤが37%の市場シェアを占め、これは温暖な条件下で卓越したトラクションとブレーキ性能を発揮するタイヤであることが背景にあります。特殊なトレッドコンパウンドと転がり抵抗を最小限に抑える設計により、夏用タイヤは燃費を向上させ、自動車のハンドリングを改善します。高級セダンや高性能車では、優れたコーナリング性能と高速安定性を実現するためにサマータイヤが頻繁に使用されています。特に温暖な気候の地域で高級車の販売が増加しており、高性能夏用タイヤの需要を引き続き押し上げています。

アジア太平洋地域は、2024年の自動車用プレミアムタイヤの世界市場シェアの40%を占めています。同地域の可処分所得の増加、急速な都市化、高級セダン、SUV、スポーツモデルの需要拡大が市場成長の主な要因となっています。その結果、耐久性に優れた高性能タイヤのニーズが急増し、メーカー各社はプレミアムタイヤのポートフォリオを拡大する必要に迫られています。主要タイヤ企業は、優れたタイヤ品質、安全性の向上、高度なドライビング・ダイナミクスを求める消費者需要の増加に対応するため、アジア太平洋全域の生産施設と流通ネットワークに投資しています。

目次

第1章 調査手法と調査範囲

第2章 エグゼクティブサマリー

第3章 業界洞察

- エコシステム分析

- サプライヤーの状況

- 原材料サプライヤー

- メーカー

- 技術プロバイダー

- サービス・プロバイダー

- 流通業者

- 最終用途

- 利益率分析

- 技術とイノベーションの展望

- 特許分析

- 主要ニュースとイニシアチブ

- 規制状況

- 価格動向

- コスト内訳分析

- 影響要因

- 促進要因

- 高級車と高性能車への需要の高まり

- 電気自動車の採用増加

- 高度な安全機能と耐久性の高い高性能タイヤに対する消費者の嗜好の高まり

- オンライン小売と専売ブランドディーラーの拡大

- 業界の潜在的リスク&課題

- プレミアムタイヤの初期コストの高さ

- 原材料価格の変動

- 促進要因

- 成長可能性分析

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業シェア分析

- 競合のポジショニング・マトリックス

- 戦略展望マトリックス

第5章 市場推計・予測:タイヤ別、2021年~2034年

- 主要動向

- 夏用タイヤ

- 冬用タイヤ

- オールシーズンタイヤ

- オールテレーンタイヤ

- その他

第6章 市場推計・予測:タイヤ構造別、2021年~2034年

- 主要動向

- ラジアル

- バイアス

第7章 市場推計・予測:技術別、2021年~2034年

- 主要動向

- ランフラット技術

- セルフシールタイヤ

- エコタイヤ

- ノイズ低減技術

- その他

第8章 市場推計・予測:リムサイズ別、2021年~2034年

- 主要動向

- 15インチ以下

- 15~20インチ

- 20インチ以上

第9章 市場推計・予測:車両別、2021年~2034年

- 主要動向

- 乗用車

- SUV

- セダン

- ハッチバック

- 商用車

- 小型商用車(LCV)

- 中型商用車(MCV)

- 大型商用車(HCV)

第10章 市場推計・予測:販売チャネル別、2021年~2034年

- 主要動向

- OEM

- アフターマーケット

第11章 市場推計・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- 英国

- ドイツ

- フランス

- スペイン

- イタリア

- ロシア

- 北欧

- アジア太平洋

- 中国

- インド

- 日本

- 韓国

- ニュージーランド

- 東南アジア

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- UAE

- 南アフリカ

- サウジアラビア

第12章 企業プロファイル

- Apollo Tyres

- Bridgestone

- CEAT

- Continental

- Cooper Tire &Rubber

- Dunlop Tires

- Falken Tire

- Goodyear Tire &Rubber

- Hankook

- Kumho Tire

- Maxxis Tires

- Michelin

- MRF

- Nitto Tire

- Nokian

- Pirelli

- Sumitomo Rubber Industries

- Toyo Tire

- Vredestein Bande

- Yokohama Rubber

The Global Automotive Premium Tires Market was valued at USD 34.7 billion in 2024 and is projected to grow at a CAGR of 6.1% between 2025 and 2034. This growth is largely driven by the increasing demand for luxury vehicles and high-performance cars, with automakers prioritizing superior tire quality to enhance vehicle performance, comfort, and safety. As consumer preferences shift toward vehicles offering advanced driving dynamics, premium tire manufacturers continue to innovate with enhanced tread compounds, advanced rubber formulations, and improved sidewall structures. The rising adoption of electric vehicles (EVs) also contributes to market expansion, as premium tires designed for EVs offer low rolling resistance, improved efficiency, and noise reduction.

The emphasis on sustainable mobility has led to an increase in research and development activities in the premium tires sector. Tire manufacturers are incorporating environmentally friendly raw materials, innovative tread designs, and cutting-edge technology to create products that offer superior grip, extended lifespan, and fuel efficiency. The growing consumer awareness of the benefits of high-performance tires, including improved braking capabilities, lower noise levels, and better road grip, further accelerates market growth. Additionally, regulatory bodies are enforcing stricter safety and fuel efficiency norms, compelling automakers to equip vehicles with high-quality tires that meet stringent standards.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $34.7 Billion |

| Forecast Value | $62.4 Billion |

| CAGR | 6.1% |

The market is segmented based on tire construction into radial and bias designs. In 2024, radial tires accounted for 80% of the market share and are expected to generate USD 50 billion by 2034. Radial tires are preferred in the premium tire market due to their enhanced flexibility, superior traction, and extended tread life. The steel-belted construction minimizes heat buildup, improving fuel efficiency and prolonging tire lifespan. As the demand for performance vehicles increases, radial tires remain the preferred choice for their high-speed stability and ability to maintain shape under challenging driving conditions, further fueling market expansion.

The market is also categorized by tire types, including summer tires, winter tires, all-season tires, all-terrain tires, and others. In 2024, summer tires held a 37% market share, driven by their ability to provide exceptional traction and braking performance in warm conditions. With specialized tread compounds and designs that minimize rolling resistance, summer tires enhance fuel economy and improve vehicle handling. Luxury sedans and high-performance cars frequently utilize summer tires to achieve superior cornering capabilities and high-speed stability. The increasing sales of luxury vehicles, particularly in regions with warmer climates, continue to boost demand for high-performance summer tires.

Asia Pacific accounted for 40% of the global automotive premium tires market share in 2024. The region's rising disposable income, rapid urbanization, and growing demand for high-end sedans, SUVs, and sports models are major contributors to market growth. As a result, the need for durable, high-performance tires has surged, prompting manufacturers to expand their premium tire portfolios. Leading tire companies are investing in production facilities and distribution networks across Asia Pacific to cater to the increasing consumer demand for superior tire quality, enhanced safety, and advanced driving dynamics.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.1.1 Research approach

- 1.1.2 Data collection methods

- 1.2 Base estimates and calculations

- 1.2.1 Base year calculation

- 1.2.2 Key trends for market estimates

- 1.3 Forecast model

- 1.4 Primary research & validation

- 1.4.1 Primary sources

- 1.4.2 Data mining sources

- 1.5 Market definitions

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Supplier landscape

- 3.2.1 Raw material suppliers

- 3.2.2 Manufacturers

- 3.2.3 Technology providers

- 3.2.4 Service providers

- 3.2.5 Distributors

- 3.2.6 End use

- 3.3 Profit margin analysis

- 3.4 Technology & innovation landscape

- 3.5 Patent analysis

- 3.6 Key news & initiatives

- 3.7 Regulatory landscape

- 3.8 Price trends

- 3.9 Cost breakdown analysis

- 3.10 Impact forces

- 3.10.1 Growth drivers

- 3.10.1.1 Growing demand for luxury and high-performance vehicles

- 3.10.1.2 Increasing adoption of electric vehicles

- 3.10.1.3 Rising consumer preference for advanced safety features and durable high-performance tires

- 3.10.1.4 Expansion of online retail and exclusive brand dealerships

- 3.10.2 Industry pitfalls & challenges

- 3.10.2.1 High initial cost of premium tires

- 3.10.2.2 Fluctuations in raw material prices

- 3.10.1 Growth drivers

- 3.11 Growth potential analysis

- 3.12 Porter's analysis

- 3.13 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Tire, 2021 - 2034 ($Bn, Units)

- 5.1 Key trends

- 5.2 Summer tires

- 5.3 Winter tires

- 5.4 All-season tires

- 5.5 All terrain tires

- 5.6 Others

Chapter 6 Market Estimates & Forecast, By Tire Construction, 2021 - 2034 ($Bn, Units)

- 6.1 Key trends

- 6.2 Radial

- 6.3 Bias

Chapter 7 Market Estimates & Forecast, By Technology, 2021 - 2034 ($Bn, Units)

- 7.1 Key trends

- 7.2 Run-flat technology

- 7.3 Self-sealing tires

- 7.4 Eco-friendly tires

- 7.5 Noise reduction technology

- 7.6 Others

Chapter 8 Market Estimates & Forecast, By Rim Size, 2021 - 2034 ($Bn, Units)

- 8.1 Key trends

- 8.2 Below 15 inches

- 8.3 15-20 inches

- 8.4 Above 20 inches

Chapter 9 Market Estimates & Forecast, By Vehicle, 2021 - 2034 ($Bn, Units)

- 9.1 Key trends

- 9.2 Passenger cars

- 9.2.1 SUV

- 9.2.2 Sedan

- 9.2.3 Hatchback

- 9.3 Commercial vehicles

- 9.3.1 Light Commercial Vehicles (LCV)

- 9.3.2 Medium Commercial Vehicles (MCV)

- 9.3.3 Heavy Commercial Vehicles (HCV)

Chapter 10 Market Estimates & Forecast, By Sales Channel, 2021 - 2034 ($Bn, Units)

- 10.1 Key trends

- 10.2 OEM

- 10.3 Aftermarket

Chapter 11 Market Estimates & Forecast, By Region, 2021 - 2034 ($Bn, Units)

- 11.1 Key trends

- 11.2 North America

- 11.2.1 U.S.

- 11.2.2 Canada

- 11.3 Europe

- 11.3.1 UK

- 11.3.2 Germany

- 11.3.3 France

- 11.3.4 Spain

- 11.3.5 Italy

- 11.3.6 Russia

- 11.3.7 Nordics

- 11.4 Asia Pacific

- 11.4.1 China

- 11.4.2 India

- 11.4.3 Japan

- 11.4.4 South Korea

- 11.4.5 ANZ

- 11.4.6 Southeast Asia

- 11.5 Latin America

- 11.5.1 Brazil

- 11.5.2 Mexico

- 11.5.3 Argentina

- 11.6 MEA

- 11.6.1 UAE

- 11.6.2 South Africa

- 11.6.3 Saudi Arabia

Chapter 12 Company Profiles

- 12.1 Apollo Tyres

- 12.2 Bridgestone

- 12.3 CEAT

- 12.4 Continental

- 12.5 Cooper Tire & Rubber

- 12.6 Dunlop Tires

- 12.7 Falken Tire

- 12.8 Goodyear Tire & Rubber

- 12.9 Hankook

- 12.10 Kumho Tire

- 12.11 Maxxis Tires

- 12.12 Michelin

- 12.13 MRF

- 12.14 Nitto Tire

- 12.15 Nokian

- 12.16 Pirelli

- 12.17 Sumitomo Rubber Industries

- 12.18 Toyo Tire

- 12.19 Vredestein Bande

- 12.20 Yokohama Rubber