|

市場調査レポート

商品コード

1708223

倉庫自動化市場の機会、成長促進要因、産業動向分析、2025年~2034年の予測Warehouse Automation Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| 倉庫自動化市場の機会、成長促進要因、産業動向分析、2025年~2034年の予測 |

|

出版日: 2025年03月26日

発行: Global Market Insights Inc.

ページ情報: 英文 185 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

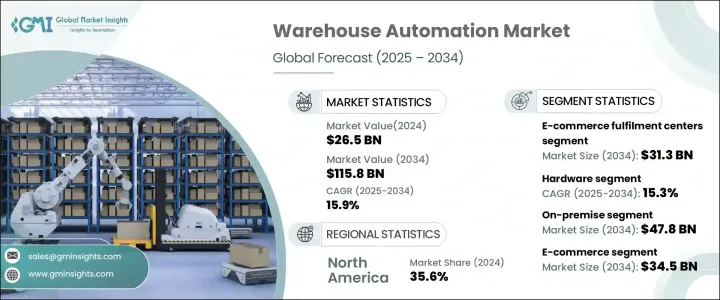

世界の倉庫自動化市場の2024年の市場規模は265億米ドルで、倉庫施設全体の合理化されたコスト効率の高いオペレーションへのニーズの高まりにより、2025年から2034年にかけてCAGR 15.9%で成長すると予測されています。

企業が労働力不足の深刻化やeコマース需要の急増に取り組む中、多くの企業が自律移動ロボット(AMR)や自動保管・検索システム(AS/RS)などの自動化技術に目を向け、日常的なプロセスを最適化しています。これらの技術は、業務効率を高めるだけでなく、人件費を削減し、人的ミスを軽減することで、迅速な注文処理と在庫管理の改善につながります。

納期短縮と完璧なオペレーションへの期待の高まりに対応しようとする企業の動きから、市場は自動化への大きなシフトを目の当たりにしています。さらに、クラウドベースの倉庫管理システム(WMS)と予測分析の採用が拡大していることで、企業はデータ主導の意思決定を行い、ロジスティクス・プロセスをさらに改善できるようになっています。都市部では、当日または翌日配達の急増する需要に対応するために設計されたマイクロ・フルフィルメント・センターがますます目立ってきていることも、倉庫自動化市場の成長加速に寄与しています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 265億米ドル |

| 予測金額 | 1,158億米ドル |

| CAGR | 15.9% |

ロボット工学と人工知能(AI)の進歩は、注文処理速度と業務精度の向上を促進することで、倉庫業務を変革しています。企業は、在庫をより効果的に管理し、ピッキングと仕分けの精度を高め、作業ミスを減らすために、AI主導のソリューションに多額の投資を行っています。AIとセンサーを活用したシステムを倉庫オートメーションに統合することで、ロボットビジョンシステムや高速コンベアなどのイノベーションが重要な役割を果たし、マテリアルハンドリングの効率が向上しています。モノのインターネット(IoT)とAI技術を組み込んで予知保全を可能にし、さまざまな倉庫コンポーネント間のシームレスな連携を確保する企業が増えており、その結果、拡張性と革新性が高まっています。

市場は、ハードウェア、ソフトウェア、サービスの3つの中核要素に区分されます。ロボット工学、コンベアシステム、自動ストレージソリューションを含むハードウェアセグメントは、2034年までに15.3%のCAGRで成長すると予測されています。AIを活用したロボット工学やセンサーを搭載したシステムが重視されるようになり、マテリアルハンドリングに革命をもたらし、プロセスを効率化し、ダウンタイムを最小限に抑えます。企業が倉庫スペースの利用率を最大化し、業務処理能力を向上させることに注力する中、AIを搭載したハードウェアソリューションの需要は高まり続けています。

倉庫の種類も市場の拡大に極めて重要な役割を果たしており、eコマース・フルフィルメントがその先頭を走っています。eコマース・フルフィルメント分野は、オンラインショッピングの急成長と、より迅速で正確な注文処理の必要性に後押しされ、2034年までに313億米ドルに達すると予想されています。このセグメントの主な動向は、スペース効率の高い保管システムの導入と、即日または翌日配達に対する消費者の期待の高まりに応えるための都市部でのマイクロ・フルフィルメント・センターの設立です。自動化システムは、ピッキング、仕分け、梱包プロセスを合理化するために広く利用されており、フルフィルメントセンターが大規模なオペレーションを最小限のエラーで処理することを可能にしています。AI主導のオーケストレーションシステムはワークフローをさらに強化し、在庫精度の向上とサプライチェーン管理の改善を可能にしています。

北米の倉庫自動化市場は2024年に35.6%のシェアを占め、同地域では倉庫効率を改善するためにロボット工学やAIを活用したソリューションの導入が急増しています。同地域の企業は、保管、ピッキング、マテリアルハンドリングプロセスを強化し、手作業への依存を軽減する自律型システムの導入に注力しています。企業は、ペースの速いeコマースの状況で競争力を維持しようと努力しており、最先端の倉庫自動化ソリューションの採用が増加していることが、市場全体の成長と技術的進歩に寄与しています。

目次

第1章 調査手法と調査範囲

第2章 エグゼクティブサマリー

第3章 業界洞察

- エコシステム分析

- 業界への影響要因

- 促進要因

- eコマースの成長とオムニチャネル小売の拡大

- 業務効率化とコスト削減の必要性

- コールドチェーンや生鮮品の自動化が進む飲食品業界

- 倉庫効率向上のためのロボットやAIへの投資の増加

- 保管とコンプライアンス強化のための医薬品・ヘルスケア業界

- 業界の潜在的リスク&課題

- 高額な初期投資と導入コスト

- サイバーセキュリティリスクとデータプライバシーへの懸念

- 促進要因

- 潜在成長力の分析

- 規制状況

- 技術動向

- 今後の市場動向

- ギャップ分析

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業シェア分析

- 主要市場プレーヤーの競合分析

- 競合のポジショニングマトリックス

- 戦略ダッシュボード

第5章 市場推計・予測:コンポーネント別、2021年~2034年

- 主要動向

- ハードウェア

- ソフトウェア

- サービス

第6章 市場推計・予測:倉庫タイプ別、2021年~2034年

- 主要動向

- eコマースフルフィルメントセンター

- 小売流通センター

- 冷蔵倉庫

- 製造倉庫

- サードパーティー・ロジスティクス(3PL)倉庫

第7章 市場推計・予測:展開モード別、2021年~2034年

- 主要動向

- オンプレミス

- クラウドベース

- ハイブリッド

第8章 市場推計・予測:技術別、2021年~2034年

- 主要動向

- 自動保管・検索システム(AS/RS)

- 自律移動ロボット(AMR)

- 無人搬送車(AGV)

- コンベア・仕分けシステム

- ロボットピッキング&ハンドリングシステム

- 倉庫管理・実行ソフトウェア

第9章 市場推計・予測:用途別、2021年~2034年

- 主要動向

- オーダーフルフィルメント自動化

- 在庫追跡・管理

- 対人(GTP)ソリューション

- パレタイジングとデパレタイジング

- 自動パッケージング&ラベリング

- リバースロジスティクスと返品処理

第10章 市場推計・予測:最終用途産業別、2021年~2034年

- 主要動向

- eコマース

- 飲食品

- 小売・消費財

- ヘルスケア

- 自動車

- 工業

- その他

第11章 市場推計・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- スペイン

- イタリア

- オランダ

- アジア太平洋

- 中国

- インド

- 日本

- オーストラリア

- 韓国

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- サウジアラビア

- 南アフリカ

- アラブ首長国連邦

第12章 企業プロファイル

- 6 River Systems

- AutoStore

- Bastian Solutions

- Daifuku

- Dematic

- Element Logic

- Fives

- Fortna

- Gebhardt Intralogistics

- Honeywell

- Kardex

- Knapp

- Korber

- Locus Robotics

- Murata Machinery

- Savoye

- SSI Schaefer

- Stow Robotics

- Swisslog

- Symbotic

- System Logistics

- Vanderlande

- Witron

The Global Warehouse Automation Market was valued at USD 26.5 billion in 2024 and is anticipated to grow at a CAGR of 15.9% from 2025 to 2034, driven by the increasing need for streamlined, cost-effective operations across warehouse facilities. As businesses grapple with rising labor shortages and surging e-commerce demand, many are turning to automation technologies such as autonomous mobile robots (AMRs) and automatic storage and retrieval systems (AS/RS) to optimize routine processes. These technologies not only enhance operational efficiency but also reduce labor costs and mitigate human errors, leading to faster order fulfillment and improved inventory management.

The market is witnessing a substantial shift toward automation as businesses seek to address the rising expectations for shorter delivery times and flawless operations. Additionally, the growing adoption of cloud-based warehouse management systems (WMS) and predictive analytics is enabling organizations to make data-driven decisions that further refine their logistics processes. The increasing prominence of micro-fulfillment centers in urban areas, designed to meet the surging demand for same-day or next-day deliveries, is also contributing to the accelerated growth of the warehouse automation market.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $26.5 Billion |

| Forecast Value | $115.8 Billion |

| CAGR | 15.9% |

Advancements in robotics and artificial intelligence (AI) are transforming warehouse operations by driving improvements in order fulfillment speed and operational precision. Companies are investing heavily in AI-driven solutions to manage inventory more effectively, boost picking and sorting accuracy, and reduce operational errors. The integration of AI and sensor-powered systems into warehouse automation is enhancing material handling efficiency, with innovations such as robotic vision systems and high-speed conveyors playing a critical role. Businesses are increasingly incorporating the Internet of Things (IoT) and AI technologies to enable predictive maintenance and ensure seamless coordination between various warehouse components, resulting in greater scalability and innovation.

The market is segmented into three core components: hardware, software, and services. The hardware segment, which includes robotics, conveyor systems, and automated storage solutions, is projected to grow at a CAGR of 15.3% by 2034. A growing emphasis on AI-driven robotics and sensor-equipped systems is revolutionizing material handling, making processes more efficient, and minimizing downtime. As companies focus on maximizing warehouse space utilization and improving operational throughput, the demand for AI-powered hardware solutions continues to rise.

Warehouse types are also playing a pivotal role in the market's expansion, with e-commerce fulfillment leading the way. The e-commerce fulfillment segment is expected to reach USD 31.3 billion by 2034, fueled by the rapid growth of online shopping and the need for faster, more accurate order processing. A key trend within this segment is the implementation of space-efficient storage systems and the establishment of micro-fulfillment centers in urban locations to meet rising consumer expectations for same-day or next-day delivery. Automated systems are being widely used to streamline picking, sorting, and packaging processes, enabling fulfillment centers to handle large-scale operations with minimal errors. AI-driven orchestration systems are further enhancing workflows, allowing for better inventory accuracy and improved supply chain management.

North America Warehouse Automation Market accounted for a 35.6% share in 2024, with the region experiencing a surge in the adoption of robotics and AI-powered solutions to improve warehouse efficiency. Businesses across the region are focusing on implementing autonomous systems to enhance storage, picking, and material handling processes, reducing the reliance on manual labor. With companies striving to stay competitive in the fast-paced e-commerce landscape, the increased adoption of cutting-edge warehouse automation solutions is contributing to the overall growth and technological advancement of the market.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Base estimates and calculations

- 1.3.1 Base year calculation

- 1.3.2 Key trends for market estimation

- 1.4 Forecast model

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.5.2 Data mining sources

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Expansion of e-commerce growth and omnichannel retailing

- 3.2.1.2 Need for operational efficiency and cost reduction

- 3.2.1.3 Food & beverage industry increasing automation for cold chain and perishable goods

- 3.2.1.4 Rising investments in robotics and AI to enhance warehouse efficiency

- 3.2.1.5 Pharmaceutical & healthcare sectors enhancing storage and compliance

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High initial investment and implementation costs

- 3.2.2.2 Cybersecurity risks and data privacy concerns

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.5 Technology landscape

- 3.6 Future market trends

- 3.7 Gap analysis

- 3.8 Porter's analysis

- 3.9 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategy dashboard

Chapter 5 Market Estimates & Forecast, By Component, 2021-2034 (USD Billion)

- 5.1 Key trends

- 5.2 Hardware

- 5.3 Software

- 5.4 Services

Chapter 6 Market Estimates & Forecast, By Warehouse Type, 2021-2034 (USD Billion)

- 6.1 Key trends

- 6.2 E-commerce fulfillment centers

- 6.3 Retail distribution centers

- 6.4 Cold storage warehouses

- 6.5 Manufacturing warehouses

- 6.6 Third-party logistics (3PL) warehouses

Chapter 7 Market Estimates & Forecast, By Deployment Mode, 2021-2034 (USD Billion)

- 7.1 Key trends

- 7.2 On-premise

- 7.3 Cloud-based

- 7.4 Hybrid

Chapter 8 Market Estimates & Forecast, By Technology, 2021-2034 (USD Billion)

- 8.1 Key trends

- 8.2 Automated storage and retrieval systems (AS/RS)

- 8.3 Autonomous mobile robots (AMRs)

- 8.4 Automated guided vehicles (AGVs)

- 8.5 Conveyor & sortation systems

- 8.6 Robotic picking & handling systems

- 8.7 Warehouse management & execution software

Chapter 9 Market Estimates & Forecast, By Application, 2021-2034 (USD Billion)

- 9.1 Key trends

- 9.2 Order fulfillment automation

- 9.3 Inventory tracking & management

- 9.4 Goods-to-person (GTP) solutions

- 9.5 Palletizing & depalletizing

- 9.6 Automated packaging & labeling

- 9.7 Reverse logistics & returns handling

Chapter 10 Market Estimates & Forecast, By End Use Industry, 2021-2034 (USD Billion)

- 10.1 Key trends

- 10.2 E-commerce

- 10.3 Food & beverage

- 10.4 Retail & consumer goods

- 10.5 Healthcare

- 10.6 Automotive

- 10.7 Industrial

- 10.8 Others

Chapter 11 Market Estimates and Forecast, By Region, 2021 – 2034 (USD Billion)

- 11.1 Key trends

- 11.2 North America

- 11.2.1 U.S.

- 11.2.2 Canada

- 11.3 Europe

- 11.3.1 Germany

- 11.3.2 UK

- 11.3.3 France

- 11.3.4 Spain

- 11.3.5 Italy

- 11.3.6 Netherlands

- 11.4 Asia Pacific

- 11.4.1 China

- 11.4.2 India

- 11.4.3 Japan

- 11.4.4 Australia

- 11.4.5 South Korea

- 11.5 Latin America

- 11.5.1 Brazil

- 11.5.2 Mexico

- 11.5.3 Argentina

- 11.6 Middle East and Africa

- 11.6.1 Saudi Arabia

- 11.6.2 South Africa

- 11.6.3 UAE

Chapter 12 Company Profiles

- 12.1 6 River Systems

- 12.2 AutoStore

- 12.3 Bastian Solutions

- 12.4 Daifuku

- 12.5 Dematic

- 12.6 Element Logic

- 12.7 Fives

- 12.8 Fortna

- 12.9 Gebhardt Intralogistics

- 12.10 Honeywell

- 12.11 Kardex

- 12.12 Knapp

- 12.13 Korber

- 12.14 Locus Robotics

- 12.15 Murata Machinery

- 12.16 Savoye

- 12.17 SSI Schaefer

- 12.18 Stow Robotics

- 12.19 Swisslog

- 12.20 Symbotic

- 12.21 System Logistics

- 12.22 Vanderlande

- 12.23 Witron