フレキシブルIBC(中間バルクコンテナ)市場の機会、成長促進要因、産業動向分析、2025年~2034年の予測

Flexible Intermediate Bulk Container (FIBC) Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034- 発行日

- ページ情報

- 英文 180 Pages

- 納期

- 2~3営業日

- 商品コード

- 1708126

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

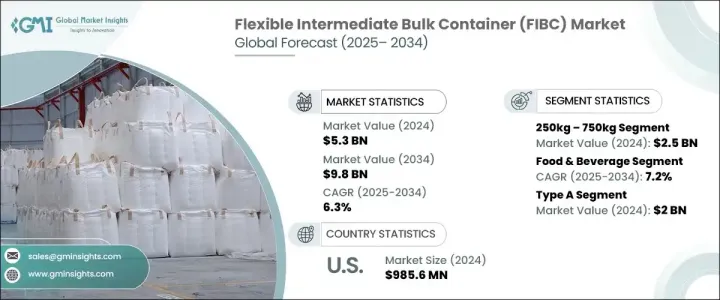

フレキシブルIBC(中間バルクコンテナ)の世界市場は、2024年に53億米ドルと評価され、2025年から2034年にかけてCAGR 6.3%で成長すると予測されています。

医薬品、飲食品、化学、農業、建設などの業界からの需要の増加が、この拡大に拍車をかけています。これらのコンテナは、バルクマテリアルハンドリングのための費用対効果に優れ、耐久性があり、軽量なソリューションを提供するため、複数のセクターで好まれる選択肢となっています。さらに、世界の貿易の急増、工業化の進展、厳しい包装規制が市場の成長に大きく寄与しています。

世界中の企業が効率性と持続可能性を重視し続ける中、FIBCはその環境に優しい特性、再利用可能性、国際包装規格への適合性により支持を集めています。特に先進地域では、持続可能なバルク包装への嗜好が高まっており、市場拡大をさらに後押ししています。eコマースの台頭も、オンライン小売業者やロジスティクス企業がコスト効率が高く安全なバルク輸送のためにFIBCを採用するケースが増えていることから、極めて重要な役割を果たしています。医薬品や食品加工などの分野では、FIBCは汚染のない保管と輸送を保証し、厳格な衛生・安全規制を遵守します。さらに、耐湿性、UVプロテクト、帯電防止バッグなど、FIBC技術の絶え間ない革新により、多様な産業ニーズへの適応性が高まっています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 53億米ドル |

| 予測金額 | 98億米ドル |

| CAGR | 6.3% |

250kg~750kgのセグメントは2024年に25億米ドルを生み出し、主に農業、食品加工、建設などの中規模産業に対応しています。これらのコンテナは、大量の商品を扱うためのコスト効率の高いソリューションを提供すると同時に、人件費を削減し、業務効率を向上させる。衛生的で汚染のないパッケージングに対する需要は、特に安全性と規制遵守が最優先される食品、化学、医薬品など、さまざまな産業で高まっています。これらの分野で先進バルクパッケージングソリューションの採用が増加していることから、今後10年間はこのセグメントの上昇基調が維持されると予想されます。

主要な応用分野の中でも、飲食品産業は最も急成長している分野として際立っており、2025年から2034年にかけてCAGR 7.2%で拡大すると予測されています。衛生的な食品包装に関する政府の規制強化が、穀物、豆類、その他の食品商品の世界の取引の増加と相まって、この成長を牽引しています。信頼性が高く大容量のバルク包装ソリューションに対するニーズが、食品セクターにおけるFIBCの需要増につながっています。さらに、耐タンパー性、耐湿性、紫外線遮蔽オプションなど、FIBCの素材と設計の進歩がその魅力を高め、長距離輸送中の製品の完全性を保証しています。

米国のフレキシブルIBC(中間バルクコンテナ)市場は、医薬品、食品、化学業界からの旺盛な需要に牽引され、2024年には9億8,560万米ドルを創出しました。持続可能性に関する規制の強化に加え、費用対効果が高く環境に優しいパッケージング・ソリューションへのシフトが進んでいることが、市場の成長を後押ししています。米国内の企業は効率的なマテリアルハンドリングを優先しており、FIBCは運用コストの削減と生産性の向上に適した選択肢として浮上しています。食品加工、医薬品、化学薬品などの業界では、持続可能で衛生的な包装への関心が高まっており、バルクフーズコンテナの需要はさらに高まっています。

目次

第1章 調査手法と調査範囲

第2章 エグゼクティブサマリー

第3章 業界洞察

- エコシステム分析

- 業界への影響要因

- 促進要因

- 国際貿易の拡大

- 持続可能で環境に優しい包装

- eコマース産業の活況

- 費用対効果と業務効率

- 食品・医薬品業界の成長

- 業界の潜在的リスク&課題

- サプライチェーンの混乱

- 原材料価格の変動

- 促進要因

- 潜在成長力の分析

- 規制状況

- 技術情勢

- 将来の市場動向

- ギャップ分析

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業シェア分析

- 主要市場プレーヤーの競合分析

- 競合のポジショニングマトリックス

- 戦略ダッシュボード

第5章 市場推計・予測:製品タイプ別、2021年~2034年

- 主要動向

- タイプA(非導電性、非静電性)

- タイプB(非導電性,制限静電性)

- タイプC(導電性FIBC、接地型)

- タイプD(静電気消散性、アースなし)

第6章 市場推計・予測:容量別、2021年~2034年

- 主要動向

- 250k未満

- 250kg以上750kg未満

- 750kg以上

第7章 市場推計・予測:最終用途別、2021年~2034年

- 主要動向

- 飲食品

- 化学品

- 医薬品

- 鉱業

- 建設

- その他

第8章 市場推計・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- スペイン

- イタリア

- オランダ

- アジア太平洋

- 中国

- インド

- 日本

- オーストラリア

- 韓国

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- サウジアラビア

- 南アフリカ

- アラブ首長国連邦

第9章 企業プロファイル

- Bag Corp

- Berry Global Group, Inc.

- Bulk Container Europe BV

- Bulk Lift International

- C.L. Smith

- FlexiblePackagingSolutions.com

- Global-Pak

- Halsted

- Intertape Polymer Group

- Isbir Sentetik

- Jumbo Bag Limited

- Langston Companies Inc.

- LC Packaging International BV

- Masterpack Group

- Palmetto Industries International Inc.

- Rishi FIBC Solutions

- Taihua Group

目次

The Global Flexible Intermediate Bulk Container Market was valued at USD 5.3 billion in 2024 and is projected to grow at a CAGR of 6.3% between 2025 and 2034. The increasing demand from industries such as pharmaceuticals, food and beverage, chemicals, agriculture, and construction is fueling this expansion. These containers offer cost-effective, durable, and lightweight solutions for bulk material handling, making them a preferred choice across multiple sectors. Additionally, the surge in global trade, rising industrialization, and stringent packaging regulations have significantly contributed to the market's growth.

As businesses worldwide continue to emphasize efficiency and sustainability, FIBCs are gaining traction due to their eco-friendly properties, reusability, and compliance with international packaging standards. The growing preference for sustainable bulk packaging, particularly in developed regions, is further supporting market expansion. The rise of e-commerce has also played a pivotal role as online retailers and logistics companies increasingly adopt FIBCs for cost-effective and secure bulk transportation. In sectors such as pharmaceuticals and food processing, these containers ensure contamination-free storage and transit, adhering to strict hygiene and safety regulations. Moreover, continuous innovations in FIBC technology, including moisture-resistant, UV-protected, and anti-static bags, are making them more adaptable to diverse industrial needs.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $5.3 Billion |

| Forecast Value | $9.8 Billion |

| CAGR | 6.3% |

The 250kg-750kg segment generated USD 2.5 billion in 2024, primarily catering to medium-sized industries such as agriculture, food processing, and construction. These containers provide a cost-efficient solution for handling large volumes of goods while reducing labor costs and improving operational efficiency. The demand for hygienic and contamination-free packaging is growing across various industries, particularly in food, chemicals, and pharmaceuticals, where safety and regulatory compliance are paramount. The increasing adoption of advanced bulk packaging solutions in these sectors is expected to sustain the segment's upward trajectory over the coming decade.

Among the key application areas, the food and beverage industry stands out as the fastest-growing segment, anticipated to expand at a CAGR of 7.2% from 2025 to 2034. Stricter government regulations regarding hygienic food packaging, coupled with the rising global trade of grains, pulses, and other food commodities, are driving this growth. The need for reliable and large-capacity bulk packaging solutions has led to an increased demand for FIBCs in the food sector. Furthermore, advancements in FIBC materials and designs, including tamper-proof, moisture-resistant, and UV-shielded options, are enhancing their appeal, ensuring product integrity during long-distance transportation.

The United States Flexible Intermediate Bulk Container (FIBC) Market generated USD 985.6 million in 2024, driven by robust demand from the pharmaceutical, food, and chemical industries. Stricter sustainability regulations, coupled with an increasing shift toward cost-effective and environmentally friendly packaging solutions, are propelling market growth. Businesses across the U.S. are prioritizing efficient material handling, with FIBCs emerging as a preferred choice for reducing operational costs and improving productivity. The heightened focus on sustainable and hygienic packaging in industries such as food processing, pharmaceuticals, and chemicals has further strengthened the demand for these bulk containers, positioning the market for steady expansion in the years ahead.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Base estimates and calculations

- 1.3.1 Base year calculation

- 1.3.2 Key trends for market estimation

- 1.4 Forecast model

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.5.2 Data mining sources

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Expansion of international trade

- 3.2.1.2 Sustainable and eco-friendly packaging

- 3.2.1.3 Booming e-commerce industry

- 3.2.1.4 Cost effectiveness and operational efficiency

- 3.2.1.5 Growth in food and pharmaceutical industries

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Supply chain disruption

- 3.2.2.2 Fluctuating price of raw materials

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.5 Technology landscape

- 3.6 Future market trends

- 3.7 Gap analysis

- 3.8 Porter's analysis

- 3.9 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategy dashboard

Chapter 5 Market Estimates and Forecast, By Product Type, 2021 - 2034 (USD Billion & Units)

- 5.1 Key trends

- 5.2 Type A (Non-conductive, Non-static)

- 5.3 Type B (Non-conductive, Limited-static)

- 5.4 Type C (Conductive FIBCs, Grounded)

- 5.5 Type D (Static dissipative, No Grounding)

Chapter 6 Market Estimates and Forecast, By Capacity, 2021 - 2034 (USD Billion & Units)

- 6.1 Key trends

- 6.2 Upto 250 kg

- 6.3 250kg – 750 kg

- 6.4 Above 750 kg

Chapter 7 Market Estimates and Forecast, By End Use, 2021 - 2034 (USD Billion & Units)

- 7.1 Key trends

- 7.2 Food & beverage

- 7.3 Chemicals

- 7.4 Pharmaceuticals

- 7.5 Mining

- 7.6 Construction

- 7.7 Others

Chapter 8 Market Estimates and Forecast, By Region, 2021 - 2034 (USD Billion & Units)

- 9.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Netherlands

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.6 Middle East and Africa

- 8.6.1 Saudi Arabia

- 8.6.2 South Africa

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 Bag Corp

- 9.2 Berry Global Group, Inc.

- 9.3 Bulk Container Europe BV

- 9.4 Bulk Lift International

- 9.5 C.L. Smith

- 9.6 FlexiblePackagingSolutions.com

- 9.7 Global-Pak

- 9.8 Halsted

- 9.9 Intertape Polymer Group

- 9.10 Isbir Sentetik

- 9.11 Jumbo Bag Limited

- 9.12 Langston Companies Inc.

- 9.13 LC Packaging International BV

- 9.14 Masterpack Group

- 9.15 Palmetto Industries International Inc.

- 9.16 Rishi FIBC Solutions

- 9.17 Taihua Group

- 発行日

- 発行

- Global Market Insights Inc.

- ページ情報

- 英文 180 Pages

- 納期

- 2~3営業日