|

市場調査レポート

商品コード

1699397

受動および相互接続電子コンポーネント市場の機会、成長促進要因、産業動向分析、2025年~2034年の予測Passive and Interconnecting Electronic Components Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025-2034 |

||||||

カスタマイズ可能

|

|||||||

| 受動および相互接続電子コンポーネント市場の機会、成長促進要因、産業動向分析、2025年~2034年の予測 |

|

出版日: 2025年02月26日

発行: Global Market Insights Inc.

ページ情報: 英文 190 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

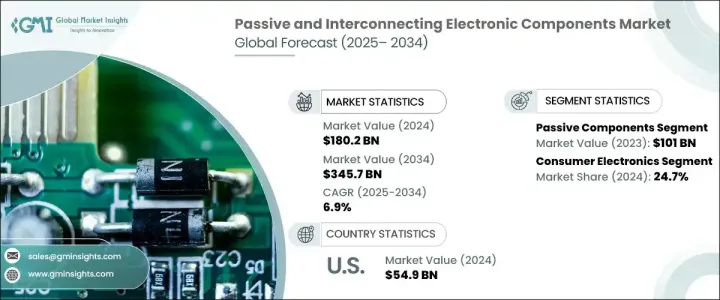

受動および相互接続電子コンポーネントの世界市場は2024年に1,802億米ドルに達し、2025年から2034年にかけてCAGR 6.9%で成長すると予測されています。

この成長の背景には、モノのインターネット(IoT)の採用拡大、カーエレクトロニクスの急速な進歩、複数の業界にわたる高性能電子コンポーネントへの需要の高まりがあります。世界の接続が進むにつれ、産業界はエネルギー効率、自動化、シームレスな接続性を重視するようになり、信頼性の高い電子コンポーネントへのニーズが高まっています。

IoTの統合は、市場情勢を形成する重要な要因となっています。スマートデバイスが日常生活に欠かせないものとなり、高品質の受動コンポーネントや相互接続コンポーネントへの需要が急増し続けています。スマートホームシステム、ウェアラブルデバイス、産業オートメーション、スマートシティはすべて、効率的な性能と接続性を実現するためにこれらの電子コンポーネントに依存しています。データ駆動技術、エッジコンピューティング、クラウドベースのアプリケーションの台頭は、需要をさらに加速させています。さらに、5Gネットワーク、人工知能(AI)、高度通信インフラの普及が進み、弾力性があり高効率の電子コンポーネントへのニーズが高まっています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 1,802億米ドル |

| 予測金額 | 3,457億米ドル |

| CAGR | 6.9% |

自動車分野も市場拡大に大きく貢献しています。現代の自動車は、ADAS(先進運転支援システム)やインフォテインメントから電気自動車(EV)のパワートレインやバッテリー管理システムまで、電子システムへの依存度が高まっています。電気自動車や自律走行車へのシフトは、次世代自動車技術の性能、安全性、長寿命を確保する受動コンポーネントや相互接続コンポーネントへの高い需要を生み出しています。自動車メーカーは、より多くの電子制御ユニット(ECU)、センサー、高速コネクターを統合し、車両の効率性、自動化、ユーザーエクスペリエンスの向上を図っています。

受動コンポーネントセグメントは2023年に1,010億米ドルを生み出し、抵抗器、コンデンサ、インダクタ、トランスなどの必須部品で構成されます。これらの部品は、動作に外部電力を必要としない代わりに、回路内でエネルギーを蓄えたり、吸収したり、散逸させたりします。民生用電子機器、産業用アプリケーション、通信、医療機器において不可欠な役割を担っており、安定した需要を後押ししています。メーカーが小型化とエネルギー効率の向上を優先する中、受動コンポーネントは最新の電子機器の耐久性、性能、信頼性を確保するために不可欠なものとなっています。

受動および相互接続電子コンポーネント市場におけるコンシューマーエレクトロニクス分野の2024年のシェアは24.7%です。スマートフォン、ノートパソコン、家電製品、ウェアラブルデバイスの普及が進み、高品質コンデンサ、抵抗器、コネクタの需要が引き続き高まっています。電子機器が処理速度の高速化、バッテリー寿命の向上、コンパクトな設計で進化するにつれ、メーカーはシームレスな機能を維持するために受動コンポーネントや相互接続コンポーネントへの依存度を高めています。

米国の受動および相互接続電子コンポーネント市場は2024年に549億米ドルに達し、強力な技術進歩、自動化の進展、デジタルインフラへの継続的投資がその原動力となっています。同国は自動車、通信、家電などの分野で技術革新の最前線にあり続け、電子コンポーネントに対する持続的な需要を生み出しています。AI、ロボット工学、スマート製造の導入が進む産業界では、信頼性が高く高性能な受動コンポーネントや相互接続コンポーネントのニーズが今後数年でさらに高まると予想されます。

目次

第1章 調査手法と調査範囲

第2章 エグゼクティブサマリー

第3章 業界洞察

- エコシステム分析

- バリューチェーンに影響を与える要因

- 利益率分析

- ディスラプション

- 将来の展望

- メーカー

- 流通業者

- サプライヤーの状況

- 利益率分析

- 主要ニュース

- 規制状況

- 影響要因

- 促進要因

- モノのインターネット(IoT)の台頭

- 先進カーエレクトロニクスへの需要の高まり

- 家電産業の急拡大

- 再生可能エネルギー・ソリューションの普及

- 業界の潜在的リスク&課題

- 原材料費の高騰

- 環境と持続可能性への懸念

- 促進要因

- 成長可能性分析

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業シェア分析

- 競合のポジショニング・マトリックス

- 戦略展望マトリックス

第5章 市場推計・予測:タイプ別、2021年~2034年

- 主要動向

- 受動

- 抵抗器

- コンデンサ

- インダクタ

- トランス

- その他

- 相互接続

- プリント基板

- コネクター

- スイッチ&リレー

- その他

第6章 市場推計・予測:用途別、2021-2034年

- 主要動向

- コンシューマーエレクトロニクス

- スマートフォン&タブレット

- ノートパソコン&デスクトップ

- テレビ・家電

- その他

- 自動車

- 車載インフォテインメント

- セーフティ&セキュリティシステム

- ドライバー支援システム

- エンジン制御システム

- その他

- ヘルスケア

- 画像処理システム

- 患者モニタリングシステム

- 治療機器

- その他

- IT・通信

- 通信機器

- ネットワーク機器

- 産業機器

- オートメーション&ロボット

- 発電

- 産業用制御システム

- その他

- 航空宇宙・防衛

- 軍事通信

- 兵器システム

- 航空機安全システム

- その他

- その他

第7章 市場推計・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- 英国

- ドイツ

- フランス

- イタリア

- スペイン

- ロシア

- アジア太平洋

- 中国

- インド

- 日本

- 韓国

- オーストラリア

- ラテンアメリカ

- ブラジル

- メキシコ

- 中東・アフリカ

- 南アフリカ

- サウジアラビア

- アラブ首長国連邦

第8章 企業プロファイル

- Amphenol Corporation

- Fenghua(HK)Electronics Ltd.

- Fujitsu Component Limited

- Hirose Electric Co. Ltd

- Hosiden Corporation

- KYOCERA AVX Components Corporation

- Molex Incorporated

- Murata Manufacturing Co., Ltd.

- Nichicon Corporation

- Panasonic Corporation

- Rohm Co., Ltd.

- Samsung Electro-Mechanics Co., Ltd.

- Taiyo Yuden Co., Ltd.

- TDK Corporation

- TE Connectivity Ltd.

- TT Electronics PLC

- United Chemi-Con

- Vishay Intertechnology, Inc.

- Walsin Technology Corporation

- Yageo Corporation

The Global Passive And Interconnecting Electronic Components Market reached USD 180.2 billion in 2024 and is projected to grow at a CAGR of 6.9% between 2025 and 2034. This growth is fueled by the increasing adoption of the Internet of Things (IoT), rapid advancements in automotive electronics, and rising demand for high-performance electronic components across multiple industries. As the world becomes more connected, industries are placing greater emphasis on energy efficiency, automation, and seamless connectivity, driving the need for reliable electronic components.

IoT integration has been a key factor in shaping the market landscape. With smart devices becoming an essential part of everyday life, the demand for high-quality passive and interconnecting components continues to surge. Smart home systems, wearable devices, industrial automation, and smart cities all rely on these electronic components for efficient performance and connectivity. The rise in data-driven technologies, edge computing, and cloud-based applications has further accelerated demand. Additionally, the increasing penetration of 5G networks, artificial intelligence (AI), and advanced telecommunication infrastructure has amplified the need for resilient and high-efficiency electronic components.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $180.2 Billion |

| Forecast Value | $345.7 Billion |

| CAGR | 6.9% |

The automotive sector is also a major contributor to market expansion. Modern vehicles are increasingly dependent on electronic systems, from advanced driver-assistance systems (ADAS) and infotainment to electric vehicle (EV) powertrains and battery management systems. The shift toward electric and autonomous vehicles has created a higher demand for passive and interconnecting components, ensuring performance, safety, and longevity in next-generation automotive technologies. Automakers are integrating more electronic control units (ECUs), sensors, and high-speed connectors to enhance vehicle efficiency, automation, and user experience.

The passive components segment generated USD 101 billion in 2023, comprising essential components such as resistors, capacitors, inductors, and transformers. These components do not require external power to operate but instead store, absorb, or dissipate energy within circuits. Their indispensable role in consumer electronics, industrial applications, telecommunications, and medical devices is fueling steady demand. With manufacturers prioritizing miniaturization and higher energy efficiency, passive components have become critical to ensuring durability, performance, and reliability in modern electronic devices.

The consumer electronics segment in the passive and interconnecting electronic components market accounted for a 24.7% share in 2024. The growing proliferation of smartphones, laptops, home appliances, and wearable devices continues to drive demand for high-quality capacitors, resistors, and connectors. As electronic devices evolve with faster processing speeds, enhanced battery life, and compact designs, manufacturers increasingly depend on passive and interconnecting components to maintain seamless functionality.

The U.S. passive and interconnecting electronic components market reached USD 54.9 billion in 2024, driven by strong technological advancements, increasing automation, and continued investment in digital infrastructure. The country remains at the forefront of innovation in sectors like automotive, telecommunications, and consumer electronics, creating a sustained demand for electronic components. With industries increasingly adopting AI, robotics, and smart manufacturing, the need for reliable, high-performance passive and interconnecting components is expected to rise further in the coming years.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope & definitions

- 1.2 Base estimates & calculations

- 1.3 Forecast calculations

- 1.4 Data sources

- 1.4.1 Primary

- 1.4.2 Secondary

- 1.4.2.1 Paid sources

- 1.4.2.2 Public sources

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021-2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Factor affecting the value chain

- 3.1.2 Profit margin analysis

- 3.1.3 Disruptions

- 3.1.4 Future outlook

- 3.1.5 Manufacturers

- 3.1.6 Distributors

- 3.2 Supplier landscape

- 3.3 Profit margin analysis

- 3.4 Key news & initiatives

- 3.5 Regulatory landscape

- 3.6 Impact forces

- 3.6.1 Growth drivers

- 3.6.1.1 Rise of the Internet of Things (IoT)

- 3.6.1.2 Increasing demand for advanced automotive electronics

- 3.6.1.3 Rapid expansion of the consumer electronics industry

- 3.6.1.4 Proliferation of renewable energy solutions

- 3.6.2 Industry pitfalls & challenges

- 3.6.2.1 High raw material costs

- 3.6.2.2 Environmental and sustainability concerns

- 3.6.1 Growth drivers

- 3.7 Growth potential analysis

- 3.8 Porter's analysis

- 3.9 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Type, 2021-2034 (USD Billion & Unit)

- 5.1 Key trends

- 5.2 Passive

- 5.2.1 Resistors

- 5.2.2 Capacitors

- 5.2.3 Inductors

- 5.2.4 Transformers

- 5.2.5 Others

- 5.3 Interconnecting

- 5.3.1 PCB

- 5.3.2 Connectors

- 5.3.3 Switches & relays

- 5.3.4 Others

Chapter 6 Market Estimates & Forecast, By Application, 2021-2034 (USD Billion & Unit)

- 6.1 Key trends

- 6.2 Consumer electronics

- 6.2.1 Smartphones & tablets

- 6.2.2 Laptops & desktops

- 6.2.3 Televisions & home appliances

- 6.2.4 Others

- 6.3 Automotive

- 6.3.1 In-vehicle infotainment

- 6.3.2 Safety & security systems

- 6.3.3 Driver assistance systems

- 6.3.4 Engine control systems

- 6.3.5 Others

- 6.4 Healthcare

- 6.4.1 Imaging systems

- 6.4.2 Patient monitoring systems

- 6.4.3 Therapeutic equipment

- 6.4.4 Others

- 6.5 IT & telecom

- 6.5.1 Telecom equipment

- 6.5.2 Networking devices

- 6.6 Industrial

- 6.6.1 Automation & robotics

- 6.6.2 Power generation

- 6.6.3 Industrial control systems

- 6.6.4 Others

- 6.7 Aerospace & defense

- 6.7.1 Military communications

- 6.7.2 Weaponry systems

- 6.7.3 Aircraft safety systems

- 6.7.4 Others

- 6.8 Others

Chapter 7 Market Estimates & Forecast, By Region, 2021-2034 (USD Billion & Unit)

- 7.1 Key trends

- 7.2 North America

- 7.2.1 U.S.

- 7.2.2 Canada

- 7.3 Europe

- 7.3.1 UK

- 7.3.2 Germany

- 7.3.3 France

- 7.3.4 Italy

- 7.3.5 Spain

- 7.3.6 Russia

- 7.4 Asia Pacific

- 7.4.1 China

- 7.4.2 India

- 7.4.3 Japan

- 7.4.4 South Korea

- 7.4.5 Australia

- 7.5 Latin America

- 7.5.1 Brazil

- 7.5.2 Mexico

- 7.6 MEA

- 7.6.1 South Africa

- 7.6.2 Saudi Arabia

- 7.6.3 UAE

Chapter 8 Company Profiles

- 8.1 Amphenol Corporation

- 8.2 Fenghua (HK) Electronics Ltd.

- 8.3 Fujitsu Component Limited

- 8.4 Hirose Electric Co. Ltd

- 8.5 Hosiden Corporation

- 8.6 KYOCERA AVX Components Corporation

- 8.7 Molex Incorporated

- 8.8 Murata Manufacturing Co., Ltd.

- 8.9 Nichicon Corporation

- 8.10 Panasonic Corporation

- 8.11 Rohm Co., Ltd.

- 8.12 Samsung Electro-Mechanics Co., Ltd.

- 8.13 Taiyo Yuden Co., Ltd.

- 8.14 TDK Corporation

- 8.15 TE Connectivity Ltd.

- 8.16 TT Electronics PLC

- 8.17 United Chemi-Con

- 8.18 Vishay Intertechnology, Inc.

- 8.19 Walsin Technology Corporation

- 8.20 Yageo Corporation