|

市場調査レポート

商品コード

1699356

自律型船舶市場の機会、成長促進要因、産業動向分析、2025年~2034年の予測Autonomous Ships Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025-2034 |

||||||

カスタマイズ可能

|

|||||||

| 自律型船舶市場の機会、成長促進要因、産業動向分析、2025年~2034年の予測 |

|

出版日: 2025年02月24日

発行: Global Market Insights Inc.

ページ情報: 英文 160 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

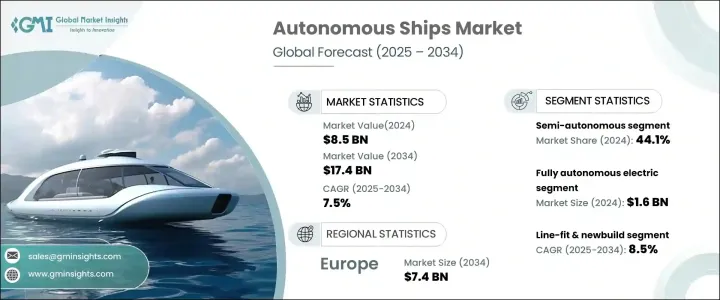

世界の自律型船舶市場は2024年に85億米ドルに達し、2025年から2034年にかけてCAGR 7.5%で成長すると予測されています。

人工知能(AI)と機械学習(ML)技術の採用が増加していることが市場拡大の原動力となっており、自律型船舶の運用方法に革命をもたらしています。メーカーは、GPS、センサー、モノのインターネット(IoT)などの最先端コンポーネントを統合することで、完全自律型船舶の開発に多額の投資を行っています。こうした進歩は自律型船舶の運航効率を大幅に高め、人間の介入を最小限に抑え、より優れた安全基準を確保しています。

自律型海運業界は、よりコスト効率が高く環境に優しいソリューションの必要性によって急速に進化しています。世界の貿易の増加に伴い、海運会社は運航コストを最適化し、安全対策を改善し、排出量を削減する方法をますます模索しています。自律型船舶は、海上オペレーションを合理化し、人為的ミスを最小限に抑えることで、有望な選択肢を提供します。AIを搭載した航行システムは、船舶が環境や航行の変化にリアルタイムで対応することを可能にし、人為的な誤算に伴うリスクを軽減します。さらに、スマート港湾インフラやデジタル海事ソリューションへの投資の増加に見られるように、規制機関は自動化へのシフトを支援しています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 85億米ドル |

| 予測金額 | 174億米ドル |

| CAGR | 7.5% |

市場は船舶のタイプにより、半自律型船舶、完全自律型船舶、遠隔操作型船舶に区分されます。半自律型船舶は2024年の市場シェア44.1%を占め、引き続き安定した需要が見込まれます。これらの船舶は特定の条件下で自律的に機能し、人間のオペレーターへの依存を減らしながら柔軟性を提供することができます。メーカーは、設計を簡素化し、デッキハウスや暖房のようなコストのかかるサブシステムを排除し、設備投資を削減することで、半自律型船舶のコスト効率を高めています。業界が半自律型ソリューションに注力していることは、段階的な自動化を好む傾向が強まっていることを浮き彫りにしており、海運会社は既存の船隊を完全にオーバーホールすることなく技術を導入することができます。

市場のもう1つの主要セグメントは推進技術で、完全電気、ハイブリッド、従来型システムが含まれます。2024年に16億米ドルと評価される完全電動自律型船舶は、ゼロ・エミッション達成に向けた大きな一歩となります。持続可能性が海事産業の中心を占める中、電気推進はさらなる技術革新の原動力になると予想されます。完全電気船は、従来の燃料船よりもクリーンでエネルギー効率の高い代替手段を提供し、世界の二酸化炭素削減目標に合致します。ハイブリッド・システムもまた、燃料効率と航続距離のバランスがとれていることから、長距離航路に適した選択肢として支持を集めています。

ドイツの自律型船舶市場は大幅な成長が見込まれており、2034年までのCAGRは10.1%で拡大すると予測されています。ドイツは自律型船舶技術の最前線にあり、複数の企業が船舶の自律性を高める先進技術を開拓しています。業界が成熟するにつれ、自律型船舶は運航コストの削減、排出量の削減、海上の安全性の向上が期待されます。持続可能性と効率性への注目の高まりは、自律型船舶を世界の海運業界のゲームチェンジャーとして位置づけ、ビジネスと環境の双方に長期的な利益をもたらします。

目次

第1章 調査手法と調査範囲

第2章 エグゼクティブサマリー

第3章 業界洞察

- エコシステム分析

- 業界への影響要因

- 促進要因

- AIと機械学習の進歩

- 労働とオペレーションのコスト削減

- グリーン輸送ソリューションへの需要の高まり

- 政府と海事政策の支援

- 業界の潜在的リスク&課題

- 原材料のサプライチェーンの混乱

- 自律型船舶に対する消費者の信頼問題

- 促進要因

- 成長の可能性分析

- 規制状況

- 技術情勢

- 将来の市場動向

- ギャップ分析

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業シェア分析

- 主要市場プレーヤーの競合分析

- 競合のポジショニングマトリックス

- 戦略ダッシュボード

第5章 市場推計・予測:タイプ別、2021年~2034年

- 主要動向

- 半自律型

- 完全自律型

- 遠隔操作型

第6章 市場推計・予測:推進技術別、2021年~2034年

- 主要動向

- 完全電動

- ハイブリッド

- 従来型

第7章 市場推計・予測:設置別、2021年~2034年

- 主要動向

- ラインフィット&新設

- レトロフィット

第8章 市場推計・予測:最終用途別、2021年~2034年

- 主要動向

- 商用

- 旅客船

- コンテナ船

- タンカー

- その他

- 軍事・防衛

- 潜水艦

- 航空母艦

- 駆逐艦

- フリゲート

第9章 市場推計・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- スペイン

- イタリア

- オランダ

- アジア太平洋

- 中国

- インド

- 日本

- オーストラリア

- 韓国

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- サウジアラビア

- 南アフリカ

- アラブ首長国連邦

第10章 企業プロファイル

- ABB Ltd.

- Aselsan A.S.

- BAE Systems

- DNV GL

- Fugro

- General Electric

- Hyundai Heavy Industries Inc.

- Kongsberg Maritime

- L3Harris Technologies, Inc.

- Mitsui E&S Shipbuilding Co., Ltd.

- Northrop Grumman Corporation

- Praxis Automation Technology B.V.

- RH Marine

- Rolls-Royce Holdings plc

- Samsung Heavy Industries Co., Ltd.

- Sea Machines Robotics, Inc

- Siemens AG

- Ulstein Group ASA

- Valmet

- Vigor Industrial LLC

- Wartsila

The Global Autonomous Ships Market reached USD 8.5 billion in 2024 and is anticipated to grow at a CAGR of 7.5% from 2025 to 2034. The increasing adoption of artificial intelligence (AI) and machine learning (ML) technologies is driving market expansion, revolutionizing the way autonomous vessels operate. Manufacturers are heavily investing in the development of fully autonomous ships by integrating cutting-edge components such as GPS, sensors, and the Internet of Things (IoT). These advancements are significantly enhancing the operational efficiency of autonomous ships, minimizing human intervention, and ensuring better safety standards.

The autonomous shipping industry is evolving rapidly, driven by the need for more cost-efficient and environmentally friendly solutions. With global trade rising, shipping companies are increasingly looking for ways to optimize operational costs, improve safety measures, and reduce emissions. Autonomous vessels offer a promising alternative by streamlining maritime operations and minimizing human error. AI-powered navigation systems enable ships to respond to environmental and navigational changes in real time, reducing the risks associated with human miscalculations. Additionally, regulatory bodies are supporting the shift towards automation, as seen in increasing investments in smart port infrastructures and digital maritime solutions.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $8.5 Billion |

| Forecast Value | $17.4 Billion |

| CAGR | 7.5% |

The market is segmented based on vessel type into semi-autonomous, fully autonomous, and remotely operated ships. Semi-autonomous ships accounted for 44.1% market share in 2024 and continue to see steady demand. These vessels can function autonomously under specific conditions, providing flexibility while reducing reliance on human operators. Manufacturers are making semi-autonomous ships more cost-effective by simplifying design, eliminating costly subsystems like deck houses and heating, and reducing capital investment. The industry's focus on semi-autonomous solutions highlights the growing preference for gradual automation, allowing shipping companies to adopt technology without a complete overhaul of their existing fleets.

Another key segment of the market is propulsion technology, which includes fully electric, hybrid, and conventional systems. Fully electric autonomous ships, valued at USD 1.6 billion in 2024, represent a major step toward achieving zero emissions. With sustainability taking center stage in the maritime industry, electric propulsion is expected to drive further innovation. Fully electric vessels offer a cleaner and more energy-efficient alternative to conventional fuel-powered ships, aligning with global carbon reduction goals. Hybrid systems are also gaining traction as they offer a balance between fuel efficiency and operational range, making them a preferred choice for long-haul shipping routes.

Germany Autonomous Ship Market is poised for substantial growth, projected to expand at a CAGR of 10.1% through 2034. The country is at the forefront of autonomous shipping technology, with multiple companies pioneering advancements that enhance vessel autonomy. As the industry matures, autonomous ships are expected to reduce operational costs, lower emissions, and improve maritime safety. The increasing focus on sustainability and efficiency is positioning autonomous vessels as a game-changer for the global shipping industry, ensuring long-term benefits for both businesses and the environment.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Base estimates and calculations

- 1.3.1 Base year calculation

- 1.3.2 Key trends for market estimation

- 1.4 Forecast model

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.5.2 Data mining sources

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Advancement in AI & Machine learning

- 3.2.1.2 Cost reduction in labour and operations

- 3.2.1.3 Growing demand for green shipping solutions

- 3.2.1.4 Supportive government & maritime policies

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Supply chain disruption of raw materials

- 3.2.2.2 Consumers trust issues in autonomous ship

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.5 Technology landscape

- 3.6 Future market trends

- 3.7 Gap analysis

- 3.8 Porter's analysis

- 3.9 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategy dashboard

Chapter 5 Market Estimates and Forecast, By Type, 2021 – 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Semi-Autonomous

- 5.3 Fully autonomous

- 5.4 Remotely operated

Chapter 6 Market Estimates and Forecast, By Propulsion Technology, 2021 – 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Fully electric

- 6.3 Hybrid

- 6.4 Conventional

Chapter 7 Market Estimates and Forecast, By Fit, 2021 – 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Line-fit & newbuild

- 7.3 Retrofit

Chapter 8 Market Estimates and Forecast, By End Use, 2021 – 2034 ($ Mn)

- 8.1 Key trends

- >8.2 Commercial

- 8.2.1 Passenger ship

- 8.2.2 Container ship

- 8.1.3 Tankers

- 8.2.4 Others

- 8.3 Military & defense

- 8.3.1 Submarines

- 8.3.2 Aircraft carriers

- 8.3.3 Destroyers

- 8.3.4 Frigates

Chapter 9 Market Estimates and Forecast, By Region, 2021 – 2034 ($ Mn)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Netherlands

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 Middle East and Africa

- 9.6.1 Saudi Arabia

- 9.6.2 South Africa

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 ABB Ltd.

- 10.2 Aselsan A.S.

- 10.3 BAE Systems

- 10.4 DNV GL

- 10.5 Fugro

- 10.6 General Electric

- 10.7 Hyundai Heavy Industries Inc.

- 10.8 Kongsberg Maritime

- 10.9 L3Harris Technologies, Inc.

- 10.10 Mitsui E&S Shipbuilding Co., Ltd.

- 10.11 Northrop Grumman Corporation

- 10.12 Praxis Automation Technology B.V.

- 10.13 RH Marine

- 10.14 Rolls-Royce Holdings plc

- 10.15 Samsung Heavy Industries Co., Ltd.

- 10.16 Sea Machines Robotics, Inc

- 10.17 Siemens AG

- 10.18 Ulstein Group ASA

- 10.19 Valmet

- 10.20 Vigor Industrial LLC

- 10.21 Wartsila