商用プラグインサージ保護デバイス市場の機会、成長促進要因、産業動向分析、2025年~2034年の予測

Plug-In Commercial Surge Protection Devices Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025-2034

- 発行日

- ページ情報

- 英文 125 Pages

- 納期

- 2~3営業日

- 商品コード

- 1699326

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

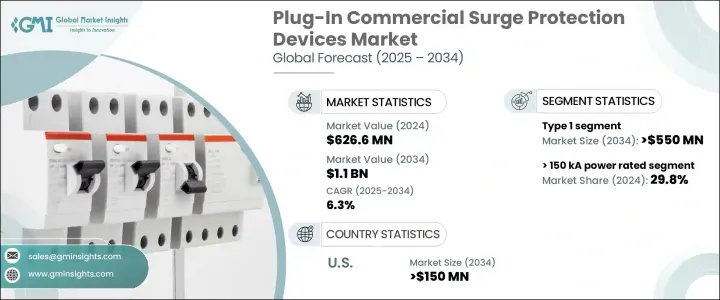

商用プラグインサージ保護デバイスの世界市場は、2024年に6億2,660万米ドルと評価され、電力サージから繊細な電気システムを保護する必要性の高まりにより、2025年から2034年にかけてCAGR 6.3%で拡大すると予測されています。

産業が自動化、クラウドコンピューティング、および高度な機械に大きく依存し続けているため、信頼性の高いサージ保護ソリューションの需要が加速しています。さまざまな分野の企業が、ダウンタイムの最小化、データ損失の防止、電気変動による財務リスクの低減のためにサージ保護を優先しています。商業施設に高度な電子インフラが広く採用されていることが、市場の成長をさらに強めています。

異常気象や送電網の故障による電力障害の急増、ハイテク機器の普及により、サージ保護装置は企業にとって極めて重要な投資となっています。データセンター、ヘルスケア機関、産業施設では、中断のない業務を確保するために、こうしたソリューションの導入が増加しています。さらに、電力品質管理を義務付ける規制の枠組みが、企業に高度な保護メカニズムの導入を促しています。運用効率を重視する業界では、応答時間の短縮と電圧クランプ機能の強化を実現する最先端のサージ保護技術の採用が進んでいます。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 6億2,660万米ドル |

| 予測金額 | 11億米ドル |

| CAGR | 6.3% |

タイプ1の商用プラグインサージ保護デバイスの需要は着実な成長を遂げており、このセグメントは2034年までに5億5,000万米ドルを生み出すと予測されています。この拡大は、高電圧サージに耐え、重要なシステムに堅牢な安全性を提供できる包括的な保護ソリューションに対するニーズによるところが大きいです。企業は、進化する業界標準を満たし、不測の電気障害から貴重な資産を保護するために、高性能サージ保護システムを選択するようになってきています。

電力定格でセグメント化されたこの市場には、50 kA以下、50 kA~100 kA、100 kA~150 kA、150 kA超などのカテゴリーが含まれます。2024年には、150kAを超える定格電力セグメントが29.8%のシェアを占め、これは重要なインフラを保護するために設計された高サージ電流定格システムの導入が増加していることを反映しています。<=50 kAセグメントは、安定した電力環境を必要とするデータセンター、ヘルスケア施設、ITハブからの需要増加により、2034年までに1億9,000万米ドルに達すると予測されています。落雷、雷雨、その他の環境要因の頻度増加により、業界全体で堅牢なサージ保護ソリューションの必要性が高まり続けています。

米国の商用プラグインサージ保護デバイス市場は、2024年に8,610万米ドルに達し、2034年には1億5,000万米ドルに達すると予想されています。同国の市場拡大には、重要インフラを保護する需要の高まりが寄与しており、産業界は高度な電気保護技術に投資しています。北米は2034年まで5.5%を超える成長率で推移すると見られており、電力網の近代化構想や商業空間における高感度電子機器の配備増加に支えられています。データセンター、自動製造プラント、ヘルスケア機関は依然として主要なエンドユーザーであり、電圧サージや電力変動に関連するリスクを軽減するサージ保護システムの採用を促進しています。

目次

第1章 調査手法と調査範囲

- 市場範囲と定義

- 市場推計・予測パラメータ

- 予測計算

- データソース

第2章 エグゼクティブサマリー

第3章 業界洞察

- エコシステム分析

- 規制状況

- 業界への影響要因

- 促進要因

- 業界の潜在的リスク&課題

- 成長ポテンシャル分析

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 戦略的展望

- イノベーションと持続可能性の展望

第5章 市場規模・予測:技術別、2021年~2034年

- 主要動向

- タイプ1

- タイプ2

- タイプ3

第6章 市場規模・予測:定格電力別、2021年~2034年

- 主要動向

- 50 kA以下

- 50 kA~100 kA

- 100 kA~150 kA

- 150 kA超

第7章 市場規模・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- ドイツ

- フランス

- ロシア

- 英国

- イタリア

- スペイン

- オランダ

- オーストリア

- アジア太平洋

- 中国

- 日本

- 韓国

- インド

- オーストラリア

- ニュージーランド

- マレーシア

- インドネシア

- 中東・アフリカ

- サウジアラビア

- アラブ首長国連邦

- カタール

- エジプト

- 南アフリカ

- ナイジェリア

- クウェート

- オマーン

- ラテンアメリカ

- ブラジル

- ペルー

- アルゼンチン

第8章 企業プロファイル

- ABB

- Belkin

- Eaton

- Emerson Electric

- Havells India

- Hubbell

- Infineon Technologies

- JMV

- Legrand

- Leviton Manufacturing

- Maxivolt

- Phoenix Contact

- Schneider Electric

- Signify Holding

- Socomec

- Weidmuller Electronics India

- WenZhou Chuangjie Lightning Protection Electrical

- Wenzhou Wanlai Electric

目次

The Global Plug-In Commercial Surge Protection Devices Market was valued at USD 626.6 million in 2024 and is projected to expand at a CAGR of 6.3% from 2025 to 2034, driven by the increasing need to safeguard sensitive electrical systems from power surges. As industries continue to rely heavily on automation, cloud computing, and advanced machinery, the demand for reliable surge protection solutions is accelerating. Businesses across various sectors are prioritizing surge protection to minimize downtime, prevent data loss, and reduce financial risks caused by electrical fluctuations. The widespread adoption of sophisticated electronic infrastructure in commercial facilities is further strengthening market growth.

The surge in power disruptions due to extreme weather conditions, grid failures, and the growing penetration of high-tech equipment has made surge protection devices a crucial investment for enterprises. Data centers, healthcare institutions, and industrial facilities are increasingly deploying these solutions to ensure uninterrupted operations. Additionally, regulatory frameworks mandating power quality management are pushing businesses to implement advanced protection mechanisms. With a strong emphasis on operational efficiency, industries are adopting cutting-edge surge protection technologies that offer faster response times and enhanced voltage clamping capabilities.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $626.6 Million |

| Forecast Value | $1.1 Billion |

| CAGR | 6.3% |

The demand for Type 1 plug-in commercial surge protection devices is experiencing steady growth, with projections estimating the segment to generate USD 550 million by 2034. This expansion is largely attributed to the need for comprehensive protection solutions that can withstand high-voltage surges and provide robust safety for critical systems. Businesses are increasingly opting for high-performance surge protection systems to meet evolving industry standards and protect valuable assets from unforeseen electrical disturbances.

Segmented by power ratings, the market encompasses categories including <= 50 kA, > 50 kA to 100 kA, > 100 kA to 150 kA, and > 150 kA. In 2024, the > 150 kA power-rated segment accounted for a 29.8% share, reflecting the rising implementation of high-surge current-rated systems designed to protect essential infrastructure. The <= 50 kA segment is projected to reach USD 190 million by 2034, fueled by increasing demand from data centers, healthcare facilities, and IT hubs requiring stable power environments. The growing frequency of lightning strikes, thunderstorms, and other environmental factors continues to amplify the need for robust surge protection solutions across industries.

The U.S. plug-in commercial surge protection devices market reached USD 86.1 million in 2024 and is expected to generate USD 150 million by 2034. The country's market expansion is fueled by the heightened demand for safeguarding critical infrastructure, with industries investing in advanced electrical protection technologies. North America is set to grow at a rate exceeding 5.5% through 2034, supported by power grid modernization initiatives and the increasing deployment of sensitive electronic equipment in commercial spaces. Data centers, automated manufacturing plants, and healthcare institutions remain key end-users, driving the adoption of surge protection systems to mitigate risks associated with voltage surges and power fluctuations.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope & definitions

- 1.2 Market estimates & forecast parameters

- 1.3 Forecast calculation

- 1.4 Data sources

- 1.4.1 Primary

- 1.4.2 Secondary

- 1.4.2.1 Paid

- 1.4.2.2 Public

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Regulatory landscape

- 3.3 Industry impact forces

- 3.3.1 Growth drivers

- 3.3.2 Industry pitfalls & challenges

- 3.4 Growth potential analysis

- 3.5 Porter's analysis

- 3.5.1 Bargaining power of suppliers

- 3.5.2 Bargaining power of buyers

- 3.5.3 Threat of new entrants

- 3.5.4 Threat of substitutes

- 3.6 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Strategic outlook

- 4.3 Innovation & sustainability landscape

Chapter 5 Market Size and Forecast, By Technology, 2021 - 2034 (USD Million & Units)

- 5.1 Key trends

- 5.2 Type 1

- 5.3 Type 2

- 5.4 Type 3

Chapter 6 Market Size and Forecast, By Power Rating, 2021 - 2034 (USD Million & Units)

- 6.1 Key trends

- 6.2 ≤ 50 kA

- 6.3 > 50 kA to 100 kA

- 6.4 > 100 kA to 150 kA

- 6.5 > 150 kA

Chapter 7 Market Size and Forecast, By Region, 2021 - 2034 (USD Million & Units)

- 7.1 Key trends

- 7.2 North America

- 7.2.1 U.S.

- 7.2.2 Canada

- 7.2.3 Mexico

- 7.3 Europe

- 7.3.1 Germany

- 7.3.2 France

- 7.3.3 Russia

- 7.3.4 UK

- 7.3.5 Italy

- 7.3.6 Spain

- 7.3.7 Netherlands

- 7.3.8 Austria

- 7.4 Asia Pacific

- 7.4.1 China

- 7.4.2 Japan

- 7.4.3 South Korea

- 7.4.4 India

- 7.4.5 Australia

- 7.4.6 New Zealand

- 7.4.7 Malaysia

- 7.4.8 Indonesia

- 7.5 Middle East & Africa

- 7.5.1 Saudi Arabia

- 7.5.2 UAE

- 7.5.3 Qatar

- 7.5.4 Egypt

- 7.5.5 South Africa

- 7.5.6 Nigeria

- 7.5.7 Kuwait

- 7.5.8 Oman

- 7.6 Latin America

- 7.6.1 Brazil

- 7.6.2 Peru

- 7.6.3 Argentina

Chapter 8 Company Profiles

- 8.1 ABB

- 8.2 Belkin

- 8.3 Eaton

- 8.4 Emerson Electric

- 8.5 Havells India

- 8.6 Hubbell

- 8.7 Infineon Technologies

- 8.8 JMV

- 8.9 Legrand

- 8.10 Leviton Manufacturing

- 8.11 Maxivolt

- 8.12 Phoenix Contact

- 8.13 Schneider Electric

- 8.14 Signify Holding

- 8.15 Socomec

- 8.16 Weidmuller Electronics India

- 8.17 WenZhou Chuangjie Lightning Protection Electrical

- 8.18 Wenzhou Wanlai Electric

- 発行日

- 発行

- Global Market Insights Inc.

- ページ情報

- 英文 125 Pages

- 納期

- 2~3営業日