|

市場調査レポート

商品コード

1699295

無線アクセスネットワーク市場の機会、成長促進要因、産業動向分析、2025年~2034年の予測Radio Access Network Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025-2034 |

||||||

カスタマイズ可能

|

|||||||

| 無線アクセスネットワーク市場の機会、成長促進要因、産業動向分析、2025年~2034年の予測 |

|

出版日: 2025年02月19日

発行: Global Market Insights Inc.

ページ情報: 英文 170 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

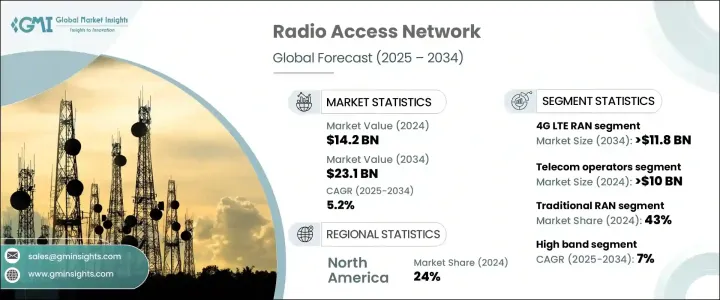

世界の無線アクセスネットワーク市場は、2024年には142億米ドルとなり、2025年から2034年にかけてCAGR 5.2%で成長すると予測されています。

シームレスな通信への需要の高まり、モバイルネットワークの急速な拡大、通信インフラへの継続的な投資が市場の成長を後押ししています。モバイルデータ消費が世界的に急増する中、ネットワークプロバイダーは増加するモバイルユーザーをサポートするため、カバレッジ、容量、効率を優先しています。デジタルトランスフォーメーションの台頭、スマートシティ構想、IoTベースのアプリケーションの普及が、通信事業者にネットワーク機能のアップグレードと最先端技術の導入を促しています。

5G技術の普及は、まだ初期段階とはいえ、ネットワーク・インフラの進歩を加速させています。しかし、4G LTEは依然として支配的な技術であり、何十億ものユーザーに安定した接続性を提供しています。高速インターネット、低遅延通信、優れたネットワーク信頼性への需要が、通信大手各社を戦略的提携や投資を通じてインフラ拡充に駆り立てています。世界各国の政府や規制機関は、有利な政策、周波数帯域の割り当て、資金提供イニシアティブによってネットワーク拡大を支援しており、市場拡大をさらに後押ししています。さらに、人工知能(AI)と機械学習(ML)のネットワーク運用への統合は、効率を改善し、待ち時間を短縮し、最新のRANソリューションをより堅牢で適応性の高いものにしています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 142億米ドル |

| 予測金額 | 231億米ドル |

| CAGR | 5.2% |

4G LTE RANセグメントは2024年に54%の市場シェアを占め、2034年には118億米ドルの市場規模になると予測されています。この優位性は、10年以上にわたって運用されてきた4Gネットワークの広範なカバレッジと信頼性に起因します。5Gの展開にもかかわらず、モバイルユーザーの大半は、そのアクセスのしやすさと安定性により、4G LTEに依存し続けています。モバイル・ネットワーク事業者は、都市部と農村部全体で優れたパフォーマンスを確保するため、4Gインフラの最適化と拡大に多額の投資を行っています。5Gのカバレッジが多くの地域でまだ限定的であることを考えると、4G LTEはモバイル接続のための最も広く使用され、信頼できる選択肢であり続けています。

通信事業者セグメントは2024年に100億米ドルを生み出し、RANインフラへの大規模投資により主導的地位を維持しています。これらの通信事業者は、携帯電話ネットワークの構築、アップグレード、維持において重要な役割を担っており、通信業界の屋台骨を形成しています。周波数帯の取得、基地局、ネットワーク拡張への投資が、引き続き業界の成長を牽引しています。高速接続への需要が高まる中、通信会社はネットワーク性能の向上、低遅延通信の確保、5Gへの移行支援に多大なリソースを割いています。モバイル技術の継続的な進歩により、通信事業者は長期的なネットワークの信頼性と拡張性を重視し、RANインフラへの投資をさらに維持すると思われます。

北米のアクセスネットワーク市場のシェアは24%で、2024年には29億2,000万米ドルに達します。同地域は通信インフラ投資の最前線にあり続け、特に5Gネットワークの拡大に注力しています。スタンドアロン5Gと固定無線アクセス技術の開発が進んでおり、世界のRAN市場における北米のリーダーとしての地位が強化されています。大手通信事業者が次世代ネットワークの革新と大規模展開に注力する中、北米は先進的な接続ソリューションのベンチマークを設定し続けています。

目次

第1章 調査手法と調査範囲

- 調査デザイン

- 調査アプローチ

- データ収集方法

- 基本推定と計算

- 基準年の算出

- 市場推計の主要動向

- 予測モデル

- 1次調査と検証

- 市場範囲と定義

第2章 エグゼクティブサマリー

第3章 業界洞察

- エコシステム分析

- サプライヤーの状況

- メーカー

- テクノロジープロバイダー

- 最終用途

- 利益率分析

- 技術とイノベーションの展望

- 特許分析

- 規制状況

- 使用事例

- 影響要因

- 促進要因

- 5Gネットワークの採用拡大

- モバイル・データ・トラフィックの増加とIoTの拡大

- 政府のイニシアティブと5G周波数割り当て

- オープンRANと仮想化RANの採用拡大

- 企業向けプライベート5Gネットワークの成長

- 業界の潜在的リスク&課題

- 高いインフラコスト

- 周波数割り当てと規制の問題

- 促進要因

- 成長の可能性分析

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業シェア分析

- 競合のポジショニング・マトリックス

- 戦略展望マトリックス

第5章 市場推計・予測:技術別、2021年~2034年

- 主要動向

- 2G RAN

- 3G RAN

- 4G LTE RAN

- 5G RAN

第6章 市場推計・予測:インフラ別、2021年~2034年

- 主要動向

- 従来型RAN

- クラウドRAN

- オープンRAN

- 仮想化RAN

第7章 市場推計・予測:周波数帯域別、2021年~2034年

- 主要動向

- ローバンド(1GHz以下)

- ミッドバンド(1~6GHz)

- ハイバンド(ミリ波、24GHz以上)

第8章 市場推計・予測:最終用途別、2021年~2034年

- 主要動向

- 通信事業者

- 企業

- スマートシティ&公共セクター

- 防衛・セキュリティ

- 産業・製造業

第9章 市場推計・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- 英国

- ドイツ

- フランス

- イタリア

- スペイン

- ロシア

- 北欧

- アジア太平洋

- 中国

- インド

- 日本

- オーストラリア

- 韓国

- 東南アジア

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- UAE

- 南アフリカ

- サウジアラビア

第10章 企業プロファイル

- Airspan Networks

- Altiostar Networks

- ASOCS

- AT&T

- Cisco

- CommScope

- Ericsson

- Fujitsu Limited

- Huawei

- Intel

- Juniper Networks

- Mavenir

- NEC

- Nokia

- Parallel Wireless

- Radisys

- Rakuten Symphony

- Samsung Electronics

- Verizon Communications

- ZTE

The Global Radio Access Network Market was valued at USD 14.2 billion in 2024 and is projected to grow at a CAGR of 5.2% between 2025 and 2034. Increasing demand for seamless connectivity, rapid expansion of mobile networks, and continuous investments in telecommunications infrastructure are fueling market growth. As mobile data consumption surges worldwide, network providers are prioritizing coverage, capacity, and efficiency to support a growing number of mobile users. The rise of digital transformation, smart city initiatives, and the proliferation of IoT-based applications are pushing telecom companies to upgrade their network capabilities and deploy cutting-edge technologies.

The widespread adoption of 5G technology, though still in its early stages, is accelerating advancements in network infrastructure. However, 4G LTE remains the dominant technology, ensuring consistent connectivity for billions of users. The demand for high-speed internet, low-latency communication, and superior network reliability is pushing telecom giants to expand their infrastructure through strategic partnerships and investments. Governments and regulatory bodies worldwide are supporting network expansion with favorable policies, spectrum allocation, and funding initiatives, further driving market expansion. Additionally, the integration of artificial intelligence (AI) and machine learning (ML) into network operations is improving efficiency and reducing latency, making modern RAN solutions more robust and adaptive.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $14.2 Billion |

| Forecast Value | $23.1 Billion |

| CAGR | 5.2% |

The 4G LTE RAN segment held a 54% market share in 2024 and is expected to generate USD 11.8 billion by 2034. This dominance is attributed to the extensive coverage and reliability of 4G networks, which have been operational for over a decade. Despite 5G deployment, the majority of mobile users continue to rely on 4G LTE due to its accessibility and stability. Mobile network operators are heavily investing in optimizing and expanding 4G infrastructure to ensure superior performance across urban and rural areas. Given that 5G coverage is still limited in many regions, 4G LTE remains the most widely used and dependable option for mobile connectivity.

The telecom operators segment generated USD 10 billion in 2024, maintaining a leading position due to massive investments in RAN infrastructure. These operators play a critical role in building, upgrading, and maintaining cellular networks, forming the backbone of the telecommunications industry. Investments in spectrum acquisition, base stations, and network expansion continue to drive industry growth. As demand for high-speed connectivity rises, telecom companies are allocating substantial resources to enhance network performance, ensure low-latency communication, and support the transition toward 5G. Ongoing advancements in mobile technology will further sustain investment in RAN infrastructure, with operators focusing on long-term network reliability and scalability.

North America's access network market accounted for a 24% share, generating USD 2.92 billion in 2024. The region remains at the forefront of telecommunications infrastructure investments, particularly in the expansion of 5G networks. Ongoing developments in standalone 5G and fixed wireless access technologies are reinforcing North America's position as a leader in the global RAN market. With major telecom players focusing on innovation and large-scale deployment of next-generation networks, North America continues to set benchmarks in advanced connectivity solutions.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.1.1 Research approach

- 1.1.2 Data collection methods

- 1.2 Base estimates & calculations

- 1.2.1 Base year calculation

- 1.2.2 Key trends for market estimation

- 1.3 Forecast model

- 1.4 Primary research and validation

- 1.4.1 Primary sources

- 1.4.2 Data mining sources

- 1.5 Market scope & definition

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Manufacturers

- 3.1.3 Technology providers

- 3.1.4 End Use

- 3.1.5 Profit margin analysis

- 3.2 Technology & innovation landscape

- 3.3 Patent analysis

- 3.4 Regulatory landscape

- 3.5 Use cases

- 3.6 Impact forces

- 3.6.1 Growth drivers

- 3.6.1.1 Growing adoption of 5G networks

- 3.6.1.2 Rising mobile data traffic and IoT expansion

- 3.6.1.3 Government initiatives and 5G spectrum allocation

- 3.6.1.4 Increasing adoption of open RAN and virtualized RAN

- 3.6.1.5 Growth in private 5G networks for enterprises

- 3.6.2 Industry pitfalls & challenges

- 3.6.2.1 High infrastructure costs

- 3.6.2.2 Spectrum allocation and regulatory issues

- 3.6.1 Growth drivers

- 3.7 Growth potential analysis

- 3.8 Porter's analysis

- 3.9 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Technology, 2021 - 2034 ($Bn)

- 5.1 Key trends

- 5.2 2G RAN

- 5.3 3G RAN

- 5.4 4G LTE RAN

- 5.5 5G RAN

Chapter 6 Market Estimates & Forecast, By Infrastructure, 2021 - 2034 ($Bn)

- 6.1 Key trends

- 6.2 Traditional RAN

- 6.3 Cloud RAN

- 6.4 Open RAN

- 6.5 Virtualized RAN

Chapter 7 Market Estimates & Forecast, By Frequency Band, 2021 - 2034 ($Bn)

- 7.1 Key trends

- 7.2 Low band (Below 1 GHz)

- 7.3 Mid band (1-6 GHz)

- 7.4 High band (mmWave, 24 GHz and above)

Chapter 8 Market Estimates & Forecast, By End Use, 2021 - 2034 ($Bn)

- 8.1 Key trends

- 8.2 Telecom operators

- 8.3 Enterprises

- 8.4 Smart cities & public sector

- 8.5 Defense & security

- 8.6 Industrial & manufacturing

Chapter 9 Market Estimates & Forecast, By Region, 2021 - 2034 ($Bn)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 UK

- 9.3.2 Germany

- 9.3.3 France

- 9.3.4 Italy

- 9.3.5 Spain

- 9.3.6 Russia

- 9.3.7 Nordics

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.4.6 Southeast Asia

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 MEA

- 9.6.1 UAE

- 9.6.2 South Africa

- 9.6.3 Saudi Arabia

Chapter 10 Company Profiles

- 10.1 Airspan Networks

- 10.2 Altiostar Networks

- 10.3 ASOCS

- 10.4 AT&T

- 10.5 Cisco

- 10.6 CommScope

- 10.7 Ericsson

- 10.8 Fujitsu Limited

- 10.9 Huawei

- 10.10 Intel

- 10.11 Juniper Networks

- 10.12 Mavenir

- 10.13 NEC

- 10.14 Nokia

- 10.15 Parallel Wireless

- 10.16 Radisys

- 10.17 Rakuten Symphony

- 10.18 Samsung Electronics

- 10.19 Verizon Communications

- 10.20 ZTE