|

市場調査レポート

商品コード

1698600

トマト加工市場の機会、成長促進要因、産業動向分析、2025年~2034年の予測Tomato Processing Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025-2034 |

||||||

カスタマイズ可能

|

|||||||

| トマト加工市場の機会、成長促進要因、産業動向分析、2025年~2034年の予測 |

|

出版日: 2025年02月14日

発行: Global Market Insights Inc.

ページ情報: 英文 220 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

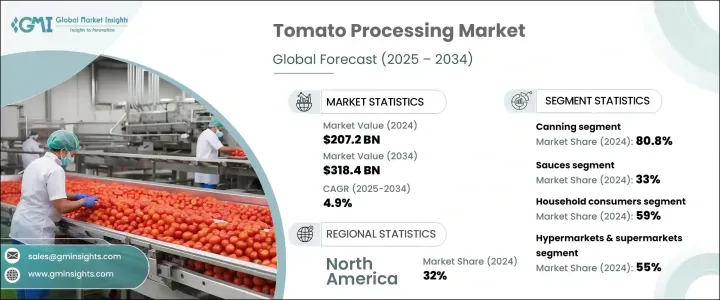

世界のトマト加工市場の2024年の市場規模は2,072億米ドルで、2025年から2034年にかけてCAGR 4.9%で成長すると予測されています。

利便性の高い食品に対する需要の増加と食品サプライチェーンの世界化が、この成長を促進する主な要因です。トマト加工食品は現代の家庭や外食産業に欠かせないものとなっており、生産と市場拡大に拍車をかけています。手軽で簡単な食事を求める消費者の嗜好が、ペースト、ソース、トマト缶のような製品の需要急増につながっています。さらに、スーパーマーケット、ハイパーマーケット、eコマース・プラットフォームなど、近代的な小売の拡大がトマト加工品をより身近なものにし、市場の成長をさらに後押ししています。都市化と食生活の進化により、消費者の行動はパッケージ食品や調理済み食品にシフトしており、市場の勢いはますます強まっています。

トマト加工産業には、パスタ、トマト缶、ダイスカット・トマト、ソース、ケチャップ、ジュース、ピューレ、濃縮トマト、パウダーなど幅広い製品が含まれます。中でもソース類は様々な料理に幅広く使用されているため、2024年の市場シェアの33%を占めています。コンビニエンス・フードの人気が高まるにつれて、すぐに食べられるソースの需要が高まっています。メーカー各社は消費者の嗜好の変化を利用し、オーガニックや減塩の選択肢を導入して健康志向の購買層にアピールしています。クイックサービス・レストランやカジュアル・ダイニング・レストランなどの外食産業は、効率的な食事の準備のために調理済みのトマトベースの製品を利用しているため、依然として市場拡大に大きく貢献しています。食品加工と成分配合の革新は、このセグメントの魅力をさらに高めています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 2,072億米ドル |

| 予測金額 | 3,184億米ドル |

| CAGR | 4.9% |

市場の加工方法には、濃縮、缶詰、果汁抽出、乾燥、ソース製造、冷凍、発酵が含まれます。2024年には缶詰加工が市場の80.8%を占め、CAGR 4.9%で成長すると予測されます。トマト缶詰の利便性と保存期間の長さが、消費者や外食業者の需要を牽引しています。乾燥や冷凍といった他の方法は、製品の耐久性延長を求める消費者を惹きつけ、ジュース抽出は健康志向の消費者にアピールします。濃縮工程ではトマト・ペーストが製造され、多目的な調理材料として役立ちます。発酵トマト製品も、特殊な食品用途向けにニッチ市場が開拓されるにつれて人気を集めています。

市場は、家庭用消費者、工業用食品加工業者、レストランなどのエンドユーザー別に区分されます。家庭用消費者は、入手しやすさと手頃な価格が原動力となり、2024年の市場シェアの59%を占めました。工業部門と外食産業は、安定した高品質のトマト加工品の大量注文が不可欠であるため、拡大を続けています。飲料部門と医薬品部門も、新製品のイノベーションにトマトエキスを取り入れています。オーガニックやプレミアム商品による差別化は、市場競争において重要な役割を果たしています。

流通チャネルには、ハイパーマーケット、スーパーマーケット、専門店、コンビニエンスストアが含まれ、2024年の市場シェアはハイパーマーケットとスーパーマーケットが55%でこのセグメントをリードしています。ハイパーマーケットとスーパーマーケットは、競争力のある価格設定と幅広い品揃えが優位性の一因となっています。専門店はニッチ市場向けにオーガニックやプレミアム・セレクションを提供し、コンビニエンスストアはすぐに食べられるトマト製品に重点を置いています。幅広い品揃えと宅配の利便性を提供するオンライン販売や消費者直販の選択肢も増え続けています。

北米はトマト加工品の旺盛な需要に牽引され、2024年の世界売上高の32%を占め、市場をリードしました。しかし、都市化の進展と可処分所得の増加に支えられ、アジア太平洋地域が最も高い成長を遂げると予想されます。欧州の市場拡大は、持続可能性への取り組み、有機製品需要、食品安全規制の厳格化によって後押しされています。食品技術と流通の継続的な進歩により、世界のトマト加工産業は持続的成長の態勢を整えています。

目次

第1章 調査手法と調査範囲

- 市場範囲と定義

- 基本推定と計算

- 予測計算

- データソース

- 1次調査と検証

第2章 エグゼクティブサマリー

第3章 業界洞察

- エコシステム分析

- バリューチェーンに影響を与える要因

- 利益率分析

- ディスラプション

- 将来の展望

- メーカー

- 流通業者

- サプライヤーの状況

- 利益率分析

- 主要ニュース

- 規制状況

- 影響要因

- 促進要因

- コンビニエンス・フードに対する需要の増大

- 食品サプライチェーンの世界化

- 食品小売チャネルの増加

- 業界の潜在的リスク&課題

- トマト供給の季節変動

- 原材料の価格変動

- 促進要因

- 成長可能性分析

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業シェア分析

- 競合のポジショニング・マトリックス

- 戦略展望マトリックス

第5章 市場推計・予測:製品別、2021年~2034年

- 主要動向

- ソース

- パスタ

- トマト缶

- ケチャップ

- ジュース

- ピューレ

- 角切り・みじん切り

- 濃縮液

- ソース

- パウダー

- その他

第6章 市場推計・予測:加工方法別、2021年~2034年

- 主要動向

- 缶詰

- ソース製造

- 搾汁

- 濃縮

- 乾燥

- 冷凍

- 発酵

- その他

第7章 市場推計・予測:最終用途別、2021年~2034年

- 主要動向

- 家庭用消費者

- 工業用食品加工業者

- 飲料業界

- 製薬業界

- その他

- 外食・フードサービス

第8章 市場推計・予測:流通チャネル別、2021年~2034年

- 主要動向

- ハイパーマーケット・スーパーマーケット

- 食品専門店

- コンビニエンスストア

- その他

第9章 市場推計・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- スペイン

- イタリア

- ロシア

- アジア太平洋

- 中国

- インド

- 日本

- オーストラリア

- 韓国

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- サウジアラビア

- 南アフリカ

- アラブ首長国連邦

第10章 企業プロファイル

- J.G. Boswell Tomato Company

- Campbell Soup Company

- CFT Group

- ConAgra Brands, Inc

- CONESA Group

- Del Monte Foods, Inc

- Food &Biotech Engineers(India)Pvt. Ltd.

- JBT Corporation

- Kagome Co., Ltd.

- Los Gatos Tomato Products

- Morning Star Company

The Global Tomato Processing Market was valued at USD 207.2 billion in 2024 and is estimated to grow at a CAGR of 4.9% from 2025 to 2034. The increasing demand for convenience foods and the globalization of food supply chains are key factors driving this growth. Processed tomato products have become essential in modern households and the food service industry, fueling production and market expansion. Consumer preference for quick and easy meal solutions has led to a surge in demand for products like pastes, sauces, and canned tomatoes, as these are primary ingredients in ready-to-eat and ready-to-cook meals. Additionally, modern retail expansion, including supermarkets, hypermarkets, and e-commerce platforms, has made processed tomato products more accessible, further driving market growth. Urbanization and evolving dietary habits continue to reinforce the market's momentum, with consumer behavior shifting toward packaged and pre-prepared food options.

The tomato processing industry includes a wide range of products such as pasta, canned tomatoes, diced tomatoes, sauces, ketchup, juice, puree, concentrate, and powder. Among these, sauces held 33% of the market share in 2024 due to their extensive use in various cuisines. As convenience foods gain popularity, ready-to-eat sauces are experiencing heightened demand. Manufacturers are capitalizing on shifting consumer preferences by introducing organic and low-sodium options to appeal to health-conscious buyers. The foodservice industry, including quick-service and casual dining restaurants, remains a significant contributor to market expansion, as these establishments rely on pre-prepared tomato-based products for efficient meal preparation. Innovations in food processing and ingredient formulation further enhance the appeal of this segment.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $207.2 Billion |

| Forecast Value | $318.4 Billion |

| CAGR | 4.9% |

Processing methods in the market include concentration, canning, juice extraction, drying, sauce production, freezing, and fermentation. Canning dominated the market in 2024, accounting for 80.8% of the share, and is expected to grow at a 4.9% CAGR. The convenience and long shelf life of canned tomato products drive their demand among consumers and food service providers. Other methods, such as drying and freezing, attract customers looking for extended product durability, while juice extraction appeals to health-conscious consumers. Concentration processes produce tomato paste, which serves as a versatile cooking ingredient. Fermented tomato products are also gaining traction as niche markets develop for specialized food applications.

The market is segmented by end users, including household consumers, industrial food processors, and restaurants. Household consumers accounted for 59% of the market share in 2024, driven by accessibility and affordability. The industrial sector and food service industry continue to expand, as bulk orders for consistent, high-quality processed tomato products remain essential. The beverage and pharmaceutical sectors are also incorporating tomato extracts into new product innovations. Differentiation through organic and premium offerings plays a crucial role in market competition.

Distribution channels include hypermarkets, supermarkets, specialty stores, and convenience stores, with hypermarkets and supermarkets leading the segment at 55% of the market share in 2024. Competitive pricing and a wide product range contribute to their dominance. Specialty stores cater to niche markets with organic and premium selections, while convenience stores focus on ready-to-eat tomato products. Online sales and direct-to-consumer options continue to rise, offering a broader selection and home delivery convenience.

North America led the market in 2024, accounting for 32% of global revenue, driven by a strong demand for processed tomato products. However, the Asia-Pacific region is expected to witness the highest growth, supported by rising urbanization and increasing disposable incomes. Europe's market expansion is fueled by sustainability initiatives, organic product demand, and stricter food safety regulations. With ongoing advancements in food technology and distribution, the global tomato processing industry is poised for sustained growth.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope & definition

- 1.2 Base estimates & calculations

- 1.3 Forecast calculation

- 1.4 Data sources

- 1.4.1 Primary

- 1.4.2 Secondary

- 1.4.2.1 Paid sources

- 1.4.2.2 Public sources

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.5.2 Data mining sources

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021-2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Factor affecting the value chain

- 3.1.2 Profit margin analysis

- 3.1.3 Disruptions

- 3.1.4 Future outlook

- 3.1.5 Manufacturers

- 3.1.6 Distributors

- 3.2 Supplier landscape

- 3.3 Profit margin analysis

- 3.4 Key news & initiatives

- 3.5 Regulatory landscape

- 3.6 Impact forces

- 3.6.1 Growth drivers

- 3.6.1.1 Increasing demand for convenience foods

- 3.6.1.2 Globalization of food supply chains

- 3.6.1.3 Increasing food retail channels

- 3.6.2 Industry pitfalls & challenges

- 3.6.2.1 Seasonal variability in tomato supply

- 3.6.2.2 Price volatility of raw materials

- 3.6.1 Growth drivers

- 3.7 Growth potential analysis

- 3.8 Porter's analysis

- 3.9 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates and Forecast, By Product, 2021 – 2034 (USD Billion) (Kilo Tons)

- 5.1 Key trends

- 5.2 Sauces

- 5.3 Pasta

- 5.4 Canned tomatoes

- 5.5 Ketchup

- 5.6 Juice

- 5.7 Puree

- 5.8 Diced & chopped

- 5.9 Concentrate

- 5.10 Sauce

- 5.11 Powder

- 5.12 Others

Chapter 6 Market Estimates and Forecast, By Processing Method, 2021 – 2034 (USD Billion) (Kilo Tons)

- 6.1 Key trends

- 6.2 Canning

- 6.3 Sauce production

- 6.4 Juice extraction

- 6.5 Concentration

- 6.6 Drying

- 6.7 Freezing

- 6.8 Fermentation

- 6.9 Others

Chapter 7 Market Estimates and Forecast, By End Use, 2021 – 2034 (USD Billion) (Kilo Tons)

- 7.1 Key trends

- 7.2 Household consumers

- 7.3 Industrial food processors

- 7.3.1 Beverage industry

- 7.3.2 Pharmaceutical industry

- 7.3.3 Others

- 7.4 Restaurants & foodservice

Chapter 8 Market Estimates and Forecast, By Distribution Channel, 2021 – 2034 (USD Billion) (Kilo Tons)

- 8.1 Key trends

- 8.2 Hypermarkets & supermarkets

- 8.3 Food specialty stores

- 8.4 Convenience stores

- 8.5 Others

Chapter 9 Market Estimates and Forecast, By Region, 2021 – 2034 (USD Billion) (Kilo Tons)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Russia

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 Middle East and Africa

- 9.6.1 Saudi Arabia

- 9.6.2 South Africa

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 J.G. Boswell Tomato Company

- 10.2 Campbell Soup Company

- 10.3 CFT Group

- 10.4 ConAgra Brands, Inc

- 10.5 CONESA Group

- 10.6 Del Monte Foods, Inc

- 10.7 Food & Biotech Engineers (India) Pvt. Ltd.

- 10.8 JBT Corporation

- 10.9 Kagome Co., Ltd.

- 10.10 Los Gatos Tomato Products

- 10.11 Morning Star Company