|

市場調査レポート

商品コード

1698590

半導体ファウンドリ市場の機会、成長促進要因、産業動向分析、2025年~2034年の予測Semiconductor Foundry Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025-2034 |

||||||

カスタマイズ可能

|

|||||||

| 半導体ファウンドリ市場の機会、成長促進要因、産業動向分析、2025年~2034年の予測 |

|

出版日: 2025年02月14日

発行: Global Market Insights Inc.

ページ情報: 英文 210 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

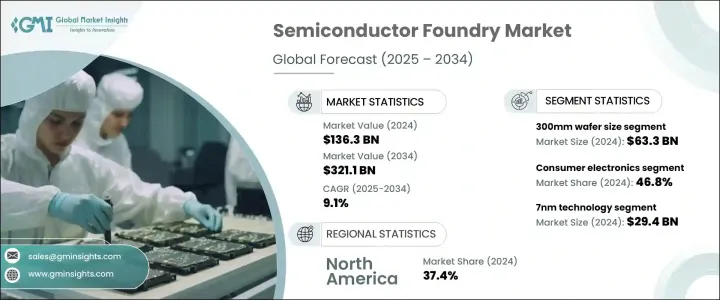

世界の半導体ファウンドリ市場は、2024年に1,363億米ドルと評価され、2034年まで9.1%のCAGRで成長すると予測されます。

市場拡大の原動力は、AIアプリケーションの需要増加とパッケージング技術の先進化です。AIベースのアプリケーションは高い計算能力を必要とするため、GPU、TPU、AIアクセラレータのような専用チップの需要が高まっています。クラウドコンピューティング、自律システム、ヘルスケア、金融技術におけるAIの採用増加により、高度な半導体ソリューションの必要性が高まっています。ディープラーニング、自然言語処理、コンピュータビジョンのワークロードがより複雑になるにつれ、半導体ファウンドリは5nm以下を含む最先端のプロセスノードに投資しています。エネルギー使用を最適化しながら処理能力を向上させようとする企業にとって、高性能でエネルギー効率の高いチップの製造能力を拡大することは依然として優先事項です。

先進パッケージング・ソリューションの革新は、業界の成長をさらに形作るものです。最新の半導体設計は、従来のモノリシック構造では進化するAIやHPCの需要を満たすことが難しく、電力効率と性能の課題に直面しています。2.5D/3D集積やチップレットを含む先進パッケージング手法は、より優れた相互接続、エネルギー効率の改善、優れた演算能力を可能にします。国家プログラムや民間企業の資金援助に支えられたこれらの技術への投資の増加は、高性能半導体ソリューションへの需要を促進しています。技術の進化に伴い、鋳造メーカーは業界内で競争力を維持するため、洗練されたパッケージング技術に注力しています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 1,363億米ドル |

| 予測金額 | 3,211億米ドル |

| CAGR | 9.1% |

自動車産業は半導体ファウンドリの成長に大きく貢献しています。ADAS、EV技術、IoT対応車両システムの統合に伴い、高性能半導体部品のニーズが急増しています。最新の車載用チップは、シームレスなリアルタイムデータ処理と接続性を確保し、自動車の安全性と自動化の強化に不可欠です。車載エレクトロニクスの複雑化により、ADAS、電動ドライブトレイン、インフォテインメントシステム向けの半導体製造への投資が必要となり、この分野の鋳造機会が拡大しています。

ウエハーサイズによる市場セグメンテーションでは、450mmカテゴリの急拡大が示されており、CAGR 10.5%で成長する見込みです。半導体デバイスの高度化に伴い、企業は生産効率とスケーラビリティを向上させるためにより大きなウエハーに移行しています。2024年に633億米ドルと評価される300mmウエハー分野は、ヘテロジニアス集積や3Dスタッキングのようなチップアーキテクチャの進歩により成長が見られます。一方、5GネットワークやスマートフォンのMEMSやRFコンポーネントに不可欠な200mmウエハは、2034年には813億米ドルを超えると予測されています。

同市場は用途別にも分類されており、2024年の市場シェアは家電が46.8%で圧倒しています。IoTデバイスの採用とAI統合の増加が引き続きこのセグメントの需要を牽引しています。通信は、データセンターの拡張と5G展開に後押しされ、CAGR10.9%の成長が見込まれます。自動車分野は2024年に市場の13.6%を占め、EVやADAS搭載車の半導体ソリューション需要を引き続き牽引します。産業用アプリケーションも増加傾向にあり、AI主導の自動化ソリューションが高品位半導体コンポーネントの需要を促進しています。

技術ノードでは、2024年に294億米ドルと評価される7nmプロセス技術が高性能コンピューティングで重要な役割を果たしています。10nmノードはCAGR 9.7%で拡大しており、プレミアムモバイルプロセッサとコンピューティングデバイスに対応しています。14nmノードは、自動車や産業オートメーションのアプリケーションに牽引されて大きく成長しており、2034年には売上高が480億米ドルを超えると予測されています。無線通信インフラで広く使用されている22nmプロセス・ノードはCAGR 7.8%の成長が見込まれ、28nmノードはOLEDディスプレイとネットワーク・ソリューションの需要が続いています。

地域別では、北米が世界市場をリードしており、2024年の市場シェアは37.4%です。この地域の優位性は、強力な半導体製造能力、先端チップ設計への投資、最先端半導体技術の早期導入に起因します。

目次

第1章 調査手法と調査範囲

- 市場範囲と定義

- 基本推定と計算

- 予測計算

- データソース

第2章 エグゼクティブサマリー

第3章 業界洞察

- エコシステム分析

- ベンダー・マトリックス

- 利益率分析

- テクノロジーとイノベーションの展望

- 特許分析

- 主要ニュースと取り組み

- 規制状況

- 影響要因

- 促進要因

- AIアプリケーションの需要急増

- 自動車産業の変革

- 先進パッケージング技術

- ハイパースケールデータセンターの拡大

- 5G技術の採用

- 業界の潜在的リスク&課題

- サプライチェーンの混乱

- 高い研究開発費と資本コスト

- 促進要因

- 成長可能性分析

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業シェア分析

- 競合のポジショニング・マトリックス

- 戦略展望マトリックス

第5章 市場推計・予測:技術ノード別、2021年~2034年

- 主要動向

- 7nm

- 10nm

- 14nm

- 22nm

- 28nm

- 40nm

- 65nm

- 90nm

- その他

第6章 市場推計・予測:用途別、2021年~2034年

- 主要動向

- コンシューマーエレクトロニクス

- 通信機器

- 自動車

- 産業

- その他

第7章 市場推定・予測:ウエハーサイズ別、2021年~2034年

- 主要動向

- 200mm

- 300mm

- 450mm

第8章 市場推計・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- 英国

- ドイツ

- フランス

- イタリア

- スペイン

- その他欧州

- アジア太平洋

- 中国

- インド

- 日本

- 韓国

- ニュージーランド

- その他アジア太平洋地域

- ラテンアメリカ

- ブラジル

- メキシコ

- その他ラテンアメリカ

- 中東・アフリカ

- UAE

- 南アフリカ

- サウジアラビア

- その他中東・アフリカ

第9章 企業プロファイル

- Dongbu Hitek Co. Ltd

- Globalfoundries Inc.

- Hua Hong Semiconductor Limited

- Intel Corporation

- Microchip Technologies Inc.

- NXP Semiconductors NV

- ON Semiconductor Corporation

- Powerchip Technology Corporation

- Renesas Electronics Corporation

- Samsung Electronics Co. Ltd(Samsung Foundry)

- Semiconductor Manufacturing International Corporation(SMIC)

- STMicroelectronics NV

- Texas Instruments Inc.

- Tower Semiconductor Ltd.

- TSMC Limited

- United Microelectronics Corporation (UMC)

- Vanguard International Semiconductor Corporation

- X-FAB Silicon Foundries

The Global Semiconductor Foundry Market, valued at USD 136.3 billion in 2024, is expected to grow at a 9.1% CAGR through 2034. Market expansion is driven by rising demand for AI applications and advancements in packaging technologies. AI-based applications require high-computing capabilities, fueling the demand for specialized chips like GPUs, TPUs, and AI accelerators. Increased adoption of AI in cloud computing, autonomous systems, healthcare, and financial technology has intensified the need for advanced semiconductor solutions. As workloads in deep learning, natural language processing, and computer vision become more complex, semiconductor foundries are investing in cutting-edge process nodes, including 5nm and below. Expanding manufacturing capacity for high-performance, energy-efficient chips remains a priority as companies seek to enhance processing power while optimizing energy use.

Innovations in advanced packaging solutions are further shaping industry growth. Modern semiconductor designs face challenges in power efficiency and performance as traditional monolithic structures struggle to meet evolving AI and HPC demands. Advanced packaging methods, including 2.5D/3D integration and chiplets, enable better interconnects, improved energy efficiency, and superior computing power. Increased investment in these technologies, backed by national programs and private sector funding, is driving demand for high-performance semiconductor solutions. As technology evolves, foundries are focusing on sophisticated packaging techniques to stay competitive in the industry.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $136.3 Billion |

| Forecast Value | $321.1 Billion |

| CAGR | 9.1% |

The automotive sector is significantly contributing to semiconductor foundry growth. With the integration of ADAS, EV technologies, and IoT-enabled vehicle systems, the need for high-performance semiconductor components has surged. Modern automotive chips ensure seamless real-time data processing and connectivity, which are essential for enhanced safety and automation in vehicles. The increasing complexity of automotive electronics necessitates investments in semiconductor manufacturing for ADAS, electric drivetrains, and infotainment systems, expanding foundry opportunities in this sector.

Market segmentation by wafer size indicates rapid expansion in the 450mm category, expected to grow at a 10.5% CAGR. As semiconductor devices become more advanced, companies are turning to larger wafers to increase production efficiency and scalability. The 300mm wafer segment, valued at USD 63.3 billion in 2024, is witnessing growth due to advancements in chip architectures like heterogeneous integration and 3D stacking. Meanwhile, 200mm wafers, essential for MEMS and RF components in 5G networks and smartphones, are projected to surpass USD 81.3 billion by 2034.

The market is also categorized by application, with consumer electronics dominating at 46.8% market share in 2024. Rising IoT device adoption and AI integration continue to drive demand in this segment. Communications is expected to grow at a 10.9% CAGR, propelled by data center expansions and 5G rollouts. The automotive sector, accounting for 13.6% of the market in 2024, continues to drive demand for semiconductor solutions in EVs and ADAS-equipped vehicles. Industrial applications are also on the rise, with AI-driven automation solutions fueling demand for high-grade semiconductor components.

In terms of technology nodes, 7nm process technology, valued at USD 29.4 billion in 2024, plays a crucial role in high-performance computing. The 10nm node is expanding at a 9.7% CAGR, catering to premium mobile processors and computing devices. The 14nm node is growing significantly, driven by applications in automotive and industrial automation, with projected revenues surpassing USD 48 billion by 2034. The 22nm process node, widely used in wireless communication infrastructure, is expected to grow at a 7.8% CAGR, while the 28nm node remains in demand for OLED displays and networking solutions.

Regionally, North America leads the global market, holding 37.4% market share in 2024. The region's dominance is attributed to strong semiconductor manufacturing capabilities, investments in advanced chip design, and early adoption of cutting-edge semiconductor technologies.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope & definition

- 1.2 Base estimates & calculations

- 1.3 Forecast calculation

- 1.4 Data sources

- 1.4.1 Primary

- 1.4.2 Secondary

- 1.4.2.1 Paid sources

- 1.4.2.2 Public sources

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis, 2021 - 2034

- 2.2 Business trends

- 2.2.1 Total addressable market (TAM), 2024-2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Vendor matrix

- 3.3 Profit margin analysis

- 3.4 Technology & innovation landscape

- 3.5 Patent analysis

- 3.6 Key news and initiatives

- 3.7 Regulatory landscape

- 3.8 Impact forces

- 3.8.1 Growth drivers

- 3.8.1.1 Surging demand for AI Applications

- 3.8.1.2 Transformation in Automotive industry

- 3.8.1.3 Advanced Packaging Technologies

- 3.8.1.4 Expansion of Hyperscale Data Centre

- 3.8.1.5 Adoption of 5G technologies

- 3.8.2 Industry pitfalls & challenges

- 3.8.2.1 Supply Chain Disruptions

- 3.8.2.2 High R&D and Capital Costs

- 3.8.1 Growth drivers

- 3.9 Growth potential analysis

- 3.10 Porter's analysis

- 3.10.1 Supplier power

- 3.10.2 Buyer power

- 3.10.3 Threat of new entrants

- 3.10.4 Threat of substitutes

- 3.10.5 Industry rivalry

- 3.11 PESTEL analysis

Chapter 4 Competitive Landscape, 2023

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Technology Node, 2021 - 2034 (USD Billion)

- 5.1 Key trends

- 5.2 7nm

- 5.3 10nm

- 5.4 14nm

- 5.5 22nm

- 5.6 28nm

- 5.7 40nm

- 5.8 65nm

- 5.9 90nm

- 5.10 Others

Chapter 6 Market Estimates & Forecast, By Application, 2021 - 2034 (USD Billion)

- 6.1 Key trends

- 6.2 Consumer electronics

- 6.3 Communication

- 6.4 Automotive

- 6.5 Industrial

- 6.6 Others

Chapter 7 Market Estimates & Forecast, By Wafer Size, 2021 - 2034 (USD Billion)

- 7.1 Key trends

- 7.2 200mm

- 7.3 300mm

- 7.4 450mm

Chapter 8 Market Estimates & Forecast, By Region, 2021 - 2034 (USD Billion)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 UK

- 8.3.2 Germany

- 8.3.3 France

- 8.3.4 Italy

- 8.3.5 Spain

- 8.3.6 Rest of Europe

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 South Korea

- 8.4.5 ANZ

- 8.4.6 Rest of Asia Pacific

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Rest of Latin America

- 8.6 MEA

- 8.6.1 UAE

- 8.6.2 South Africa

- 8.6.3 Saudi Arabia

- 8.6.4 Rest of MEA

Chapter 9 Company Profiles

- 9.1 Dongbu Hitek Co. Ltd

- 9.2 Globalfoundries Inc.

- 9.3 Hua Hong Semiconductor Limited

- 9.4 Intel Corporation

- 9.5 Microchip Technologies Inc.

- 9.6 NXP Semiconductors NV

- 9.7 ON Semiconductor Corporation

- 9.8 Powerchip Technology Corporation

- 9.9 Renesas Electronics Corporation

- 9.10 Samsung Electronics Co. Ltd (Samsung Foundry)

- 9.11 Semiconductor Manufacturing International Corporation (SMIC)

9.12 STMicroelectronics NV

- 9.13 Texas Instruments Inc.

- 9.14 Tower Semiconductor Ltd.

- 9.15 TSMC Limited

- 9.16 United Microelectronics Corporation (UMC)

- 9.17 Vanguard International Semiconductor Corporation

- 9.18 X-FAB Silicon Foundries