|

市場調査レポート

商品コード

2027501

GaN LEDチップ市場の機会、成長要因、業界動向分析、および2026年~2035年の予測GaN LED Chips Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

カスタマイズ可能

|

|||||||

| GaN LEDチップ市場の機会、成長要因、業界動向分析、および2026年~2035年の予測 |

|

出版日: 2026年04月15日

発行: Global Market Insights Inc.

ページ情報: 英文 220 Pages

納期: 2~3営業日

|

概要

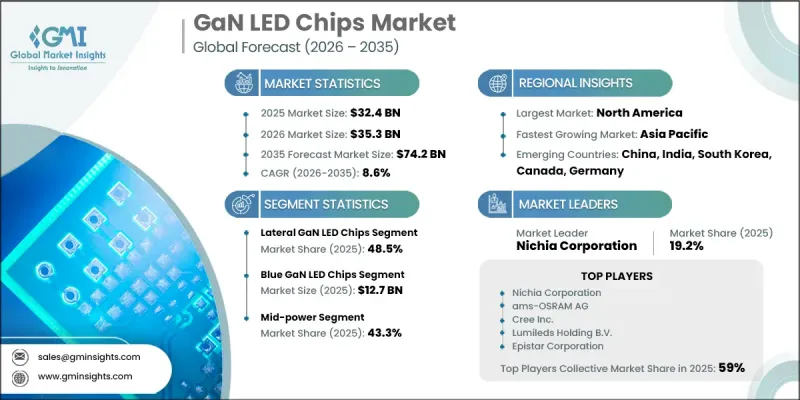

世界のGaN LEDチップ市場は、2025年に324億米ドルと評価され、CAGR 8.6%で成長し、2035年までに742億米ドルに達すると推定されています。

この市場は、高性能な照明およびディスプレイ技術の急速な進歩に牽引され、拡大を続けています。プレミアムディスプレイシステムにおけるミニLEDバックライトの採用拡大は、GaNベースのソリューションに対する需要を大幅に押し上げています。また、AR/VRデバイスやウェアラブル電子機器へのこれらのチップの組み込みが進んでいることも、市場の成長をさらに後押ししています。同時に、商業および産業分野全体で省エネ型照明ソリューションへの注目が高まっていることが、導入を加速させています。都市インフラや屋外環境向けのスマートLEDシステムの開発も、持続的な需要に貢献しています。エピタキシャル成長技術やチップアーキテクチャの継続的な改善により、輝度、効率、および動作寿命が向上しています。先進的なディスプレイ製造への投資の増加や、コンパクトで高密度なLED構成への移行は、民生用電子機器や自動車用途における市場の拡大をさらに後押ししており、GaN LEDチップは次世代の電子・照明エコシステムにおける中核的な基盤技術としての地位を確立しつつあります。

| 市場の範囲 | |

|---|---|

| 開始年 | 2025年 |

| 予測期間 | 2026-2035 |

| 開始時の市場規模 | 324億米ドル |

| 予測額 | 742億米ドル |

| CAGR | 8.6% |

2025年時点で、横型GaN LEDチップセグメントは48.5%のシェアを占めました。このセグメントが主導的な地位にあるのは、コスト効率の高い製造プロセス、確立された生産技術、および低~中出力用途への高い適合性によるものです。その信頼性の高い性能と統合の容易さから、民生用電子機器、自動車用ディスプレイ、一般照明システムなど幅広い分野で採用されており、大規模な生産需要を支えています。

青色GaN LEDチップセグメントは、2025年に127億米ドルに達しました。このセグメントは、ディスプレイのバックライト、一般照明、および高効率照明システムでの広範な利用により、引き続き主導的な地位を維持しています。その優れたエネルギー効率と、蛍光体ベースの白色光変換との互換性により、民生用電子機器や自動車用照明を含む複数の最終用途産業において不可欠な存在となっています。

2025年、北米のGaN LEDチップ市場は38.5%のシェアを占めました。同地域の市場成長は、エネルギー効率に対する規制当局の強い注力と、先進的な照明技術の広範な普及によって支えられています。デジタル制御システムと統合されたスマート照明インフラの導入拡大が、市場浸透を促進しています。商業施設や産業施設におけるコネクテッド照明プラットフォームへの投資増加が、地域の需要をさらに強化しています。高効率照明ソリューションを通じたエネルギー最適化を目指す政府および民間セクターの取り組みも、多様な用途における導入を加速させています。

よくあるご質問

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- サプライヤーの情勢

- 利益率

- コスト構造

- 各段階における付加価値

- バリューチェーンに影響を与える要因

- ディスラプション

- 業界への影響要因

- 促進要因

- プレミアムディスプレイにおけるマイクロLEDの採用拡大

- AR/VRおよびウェアラブルディスプレイからの高い需要

- 省エネ型照明ソリューションへの需要の高まり

- スマートシティ向けLEDインフラプロジェクトの拡大

- LCDパネル向けミニLEDバックライトの成長

- 業界の潜在的リスク&課題

- GaN基板の高い製造コスト

- 高出力アプリケーションにおける熱管理の複雑さ

- 市場機会

- 次世代マイクロLEDテレビへの統合

- 自動車用LiDARおよびセンシング用途への拡大

- 促進要因

- 成長可能性分析

- 規制情勢

- ポーター分析

- PESTEL分析

- 技術およびイノベーションの動向

- 現在の技術動向

- 新興技術

- 価格動向

- 地域別

- 製品別

- 価格戦略

- 新興ビジネスモデル

- コンプライアンス要件

- 特許および知的財産分析

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 地域別

- 市場集中度の分析

- 主要企業の競合ベンチマーキング

- 財務実績の比較

- 売上高

- 利益率

- 研究開発(R&D)

- 製品ポートフォリオの比較

- 製品ラインの幅

- 技術

- イノベーション

- 地域展開の比較

- 世界展開の分析

- サービスネットワークのカバー範囲

- 地域別市場浸透率

- 競合ポジショニングマトリックス

- リーダー

- チャレンジャー

- フォロワー

- ニッチプレイヤー

- 戦略的展望マトリックス

- 財務実績の比較

- 主な発展

- 合併・買収

- 提携および協業

- 技術的進歩

- 事業拡大および投資戦略

- デジタルトランスフォーメーションの取り組み

- 新興/スタートアップ競合企業の動向

第5章 市場推計・予測:発光タイプ別、2022-2035

- 青色GaN LEDチップ

- 緑色GaN LEDチップ

- UV GaN LEDチップ

- その他

第6章 市場推計・予測:チップアーキテクチャ別、2022-2035

- 横型GaN LEDチップ

- 垂直型GaN LEDチップ

- 薄膜GaN LEDチップ

第7章 市場推計・予測:出力クラス別、2022-2035

- 低出力

- 中出力

- 高出力

第8章 市場推計・予測:基板タイプ別、2022-2035

- サファイア

- 炭化ケイ素(SiC)

- シリコン(Si)

- GaN-on-GaN

第9章 市場推計・予測:用途別、2022-2035

- 一般照明

- ディスプレイ用バックライト

- 自動車用照明

- ディスプレイ・サイネージ

- その他

第10章 市場推計・予測:地域別、2022-2035

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- スペイン

- イタリア

- オランダ

- アジア太平洋地域

- 中国

- インド

- 日本

- オーストラリア

- 韓国

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- 南アフリカ

- サウジアラビア

- アラブ首長国連邦

第11章 企業プロファイル

- 世界の主要企業

- Aixtron SE

- Infineon Technologies AG

- Lumileds Holding B.V.

- Cree, Inc.

- ams-OSRAM AG

- Nichia Corporation

- Epistar

- 地域別主要企業

- 北米

- Bridgelux

- Qorvo, Inc.

- Navitas Semiconductor

- Allegro MicroSystems

- アジア太平洋地域

- Fujitsu Ltd.

- Sumitomo Electric Industries, Ltd.

- SemiLEDs Corporation

- Epileds Technologies, Inc.

- 欧州

- Aledia

- 北米

- ニッチプレイヤー/ディスラプター

- Efficient Power Conversion Corporation

- GaNPower International Inc.

- Veeco Instruments Inc.