|

市場調査レポート

商品コード

1665222

直視型LEDディスプレイの市場機会、成長促進要因、産業動向分析、2025~2034年予測Direct View LED Display Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| 直視型LEDディスプレイの市場機会、成長促進要因、産業動向分析、2025~2034年予測 |

|

出版日: 2024年12月17日

発行: Global Market Insights Inc.

ページ情報: 英文 210 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

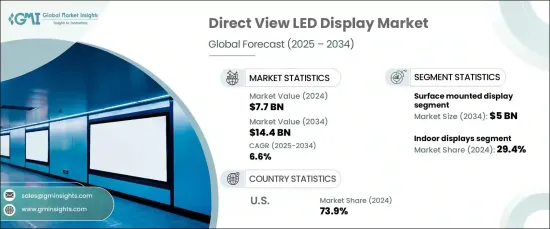

世界の直視型LEDディスプレイ(DVLED)市場は、2024年に77億米ドルに達し、2025~2034年にかけてCAGR 6.6%の堅調な成長が見込まれています。

高解像度でエネルギー効率に優れたディスプレイに対する需要の高まりが、商業、娯楽、小売の各セグメントでこの成長を後押ししています。DVLEDディスプレイは、鮮やかなビジュアル、シームレスなパフォーマンス、卓越した耐久性を提供する能力で有名であり、屋内と屋外の幅広い用途に最適なソリューションになりつつあります。

2024年には、屋内用ディスプレイが29.4%のシェアを獲得し、市場リーダーに浮上しました。そのシャープな解像度、正確な色精度、審美的な魅力により、企業環境、小売スペース、娯楽施設などの用途で高い人気を集めています。より微細なピクセルピッチと500~1,500個の最適化された輝度レベルで設計された屋内用DVLEDシステムは、比類のない鮮明な視覚を提供し、こうした注目度の高いセグメントの需要に応えています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024年 |

| 予測年 | 2025~2034 |

| 開始金額 | 77億米ドル |

| 予測金額 | 144億米ドル |

| CAGR | 6.6% |

技術面では、表面実装型ディスプレイが、そのコンパクトなデザインと優れた耐久性によって、2034年までに50億米ドルを生み出すと予測されています。SMD(Surface Mounted Device)技術を活用したこれらのディスプレイは、LEDチップを回路基板に直接組み込んでおり、輝度、色の一貫性、全体的な性能を高めています。この先進技術は、ダイナミックなデジタルサイネージや大型ディスプレイなど、屋内外の設置に理想的です。

米国市場は2024年、世界のDVLED市場をリードし、73.9%という素晴らしいシェアを占めています。この優位性は、小売、娯楽、商業の各セグメントでDVLEDディスプレイの採用が拡大していることが主因です。小売業では、DVLEDディスプレイをダイナミックな店内サイネージに活用するケースが増えており、視覚的な魅力を高めながら魅力的な顧客体験を創造しています。都市部では、屋外広告がデジタル化され、静的な看板が人目を引くデジタル広告に取って代わられています。エンターテインメント産業もDVLED技術を採用し、スポーツアリーナやコンサート会場、イベントスペースで臨場感あふれる体験を演出しています。

視覚的に印象的でエネルギー効率に優れたディスプレイソリューションへの需要が高まり続ける中、DVLED市場はますます繁栄していくと考えられます。画素密度の技術的進歩とスマート機能の統合が技術革新を促進し、採用を拡大しています。多様なセグメントにまたがる用途により、直視型LEDディスプレイ市場は予測期間中に大きく成長し、変革的なインパクトを与えることになります。

目次

第1章 調査手法と調査範囲

- 市場範囲と定義

- 基本推定と計算

- 予測計算

- データソース

- 1次データ

- 二次資料

- 有料情報源

- 公的情報源

第2章 エグゼクティブサマリー

第3章 産業洞察

- エコシステム分析

- バリューチェーンに影響を与える要因

- 利益率分析

- 変革

- 将来の展望

- メーカー

- 流通業者

- サプライヤーの状況

- 利益率分析

- 主要ニュース

- 規制状況

- 影響要因

- 促進要因

- 高品質の映像体験に対する需要の高まり

- コストの低下と技術の進歩

- 屋外広告やデジタルサイネージにおける採用の増加

- インタラクティブディスプレイの人気上昇

- 産業の潜在的リスク・課題

- 高い初期投資とメンテナンスコスト

- 技術的課題と複雑な統合

- 促進要因

- 成長可能性分析

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業シェア分析

- 競合のポジショニングマトリックス

- 戦略展望マトリックス

第5章 市場推定・予測:ディスプレイタイプ別、2021~2034年

- 主要動向

- 屋内ディスプレイ

- 屋外ディスプレイ

- スタジアムスクリーン

- デジタルサイネージ

第6章 市場推定・予測:技術別、2021~2034年

- 主要動向

- 表面実装ディスプレイ

- チップオンボードディスプレイ

- マイクロLEDディスプレイ

- 量子ドットディスプレイ

第7章 市場推定・予測:用途別、2021~2034年

- 主要動向

- 広告

- スポーツ

- 運輸

- 小売

- 放送

第8章 市場推定・予測:最終用途別、2021~2034年

- 主要動向

- 官公庁

- 商業

- 教育機関

- 住宅用

第9章 市場推定・予測:地域別、2021~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- 英国

- ドイツ

- フランス

- イタリア

- スペイン

- ロシア

- アジア太平洋

- 中国

- インド

- 日本

- 韓国

- オーストラリア

- ラテンアメリカ

- ブラジル

- メキシコ

- 中東・アフリカ

- 南アフリカ

- サウジアラビア

- アラブ首長国連邦

第10章 企業プロファイル

- Absen

- AOTO Electronics

- Barco NV

- Christie Digital Systems

- Daktronics

- Delta Electronics

- INFiLED

- Ledman Optoelectronic

- Leyard Optoelectronic

- LG Electronics

- Lighthouse Technologies

- NEC Display Solutions

- Planar Systems

- ROE Visual

- Samsung Electronics

- Shenzhen Absen Optoelectronic

- Shenzhen Liantronics

- SiliconCore Technology

- Unilumin Group

- Yaham Optoelectronics

The Global Direct View LED Display Market reached USD 7.7 billion in 2024 and is anticipated to grow at a robust CAGR of 6.6% from 2025 to 2034. The increasing demand for high-resolution, energy-efficient displays is fueling this growth across commercial, entertainment, and retail sectors. Renowned for their ability to deliver vibrant visuals, seamless performance, and exceptional durability, DVLED displays are becoming the go-to solution for a wide range of indoor and outdoor applications.

In 2024, indoor displays emerged as the market leader, capturing a 29.4% share. Their sharp resolution, precise color accuracy, and aesthetic appeal make them highly sought after for applications in corporate environments, retail spaces, and entertainment venues. Designed with finer pixel pitches and optimized brightness levels ranging from 500 to 1,500 units, indoor DVLED systems offer unmatched visual clarity, meeting the demands of these high-profile sectors.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $7.7 Billion |

| Forecast Value | $14.4 Billion |

| CAGR | 6.6% |

On the technology front, surface-mounted displays are projected to generate USD 5 billion by 2034, driven by their compact design and superior durability. Leveraging Surface Mounted Device (SMD) technology, these displays feature LED chips directly integrated into circuit boards, enhancing brightness, color consistency, and overall performance. This advanced technology is ideal for both indoor and outdoor installations, including dynamic digital signage and large-format displays.

The U.S. market led the global DVLED landscape in 2024, holding an impressive 73.9% share. This dominance is largely attributed to the growing adoption of DVLED displays across retail, entertainment, and commercial sectors. Retailers are increasingly leveraging these displays for dynamic in-store signage, creating engaging customer experiences while enhancing visual appeal. In urban areas, outdoor advertising is undergoing a digital transformation as static billboards give way to eye-catching digital alternatives. The entertainment industry is also embracing DVLED technology to create immersive experiences in sports arenas, concert venues, and event spaces.

As the demand for visually striking, energy-efficient display solutions continues to rise, the DVLED market is set to flourish. Technological advancements in pixel density and the integration of smart features are driving innovation and expanding adoption. With applications spanning diverse sectors, the direct view LED display market is poised for significant growth and transformative impact over the forecast period.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope & definitions

- 1.2 Base estimates & calculations

- 1.3 Forecast calculations

- 1.4 Data sources

- 1.4.1 Primary

- 1.4.2 Secondary

- 1.4.2.1 Paid sources

- 1.4.2.2 Public sources

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021-2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Factor affecting the value chain

- 3.1.2 Profit margin analysis

- 3.1.3 Disruptions

- 3.1.4 Future outlook

- 3.1.5 Manufacturers

- 3.1.6 Distributors

- 3.2 Supplier landscape

- 3.3 Profit margin analysis

- 3.4 Key news & initiatives

- 3.5 Regulatory landscape

- 3.6 Impact forces

- 3.6.1 Growth drivers

- 3.6.1.1 Increasing demand for high-quality visual experiences

- 3.6.1.2 Declining costs and technological advancements

- 3.6.1.3 Growing adoption in outdoor advertising and digital signage

- 3.6.1.4 Rising popularity of interactive displays

- 3.6.2 Industry pitfalls & challenges

- 3.6.2.1 High initial investment and maintenance costs

- 3.6.2.2 Technical challenges and complex integration

- 3.6.1 Growth drivers

- 3.7 Growth potential analysis

- 3.8 Porter’s analysis

- 3.9 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Display Type, 2021-2034 (USD Billion)

- 5.1 Key trends

- 5.2 Indoor displays

- 5.3 Outdoor displays

- 5.4 Stadium screens

- 5.5 Digital signage

Chapter 6 Market Estimates & Forecast, By Technology, 2021-2034 (USD Billion)

- 6.1 Key trends

- 6.2 Surface mounted display

- 6.3 Chip on board display

- 6.4 MicroLED display

- 6.5 Quantum dot display

Chapter 7 Market Estimates & Forecast, By Application, 2021-2034 (USD Billion)

- 7.1 Key trends

- 7.2 Advertising

- 7.3 Sports

- 7.4 Transportation

- 7.5 Retail

- 7.6 Broadcasting

Chapter 8 Market Estimates & Forecast, By End Use, 2021-2034 (USD Billion)

- 8.1 Key trends

- 8.2 Government

- 8.3 Commercial

- 8.4 Educational

- 8.5 Residential

Chapter 9 Market Estimates & Forecast, By Region, 2021-2034 (USD Billion)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 UK

- 9.3.2 Germany

- 9.3.3 France

- 9.3.4 Italy

- 9.3.5 Spain

- 9.3.6 Russia

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 South Korea

- 9.4.5 Australia

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.6 MEA

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 Absen

- 10.2 AOTO Electronics

- 10.3 Barco NV

- 10.4 Christie Digital Systems

- 10.5 Daktronics

- 10.6 Delta Electronics

- 10.7 INFiLED

- 10.8 Ledman Optoelectronic

- 10.9 Leyard Optoelectronic

- 10.10 LG Electronics

- 10.11 Lighthouse Technologies

- 10.12 NEC Display Solutions

- 10.13 Planar Systems

- 10.14 ROE Visual

- 10.15 Samsung Electronics

- 10.16 Shenzhen Absen Optoelectronic

- 10.17 Shenzhen Liantronics

- 10.18 SiliconCore Technology

- 10.19 Unilumin Group

- 10.20 Yaham Optoelectronics