|

市場調査レポート

商品コード

1698528

環境光センサー市場の機会、成長促進要因、産業動向分析、2025年~2034年の予測Ambient Light Sensor Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025-2034 |

||||||

カスタマイズ可能

|

|||||||

| 環境光センサー市場の機会、成長促進要因、産業動向分析、2025年~2034年の予測 |

|

出版日: 2025年02月05日

発行: Global Market Insights Inc.

ページ情報: 英文 190 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

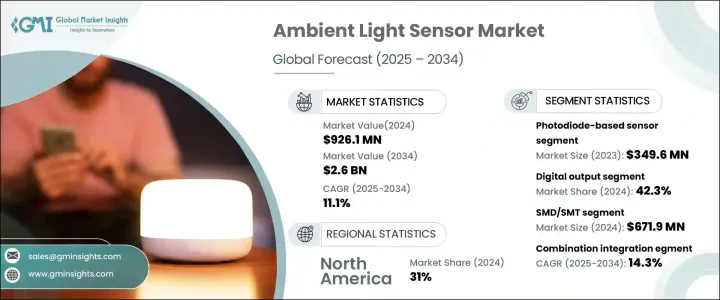

環境光センサーの世界市場は、2024年に9億2,610万米ドルと評価され、家電、自動車、スマートインフラ分野での需要増加を背景に、2025年から2034年にかけて11.1%の堅調なCAGRで拡大すると予測されています。

産業界が自動化、エネルギー効率、ユーザー中心技術をますます優先するようになるにつれ、環境光センサーは最新のデバイスやシステムに不可欠なコンポーネントとなりつつあります。これらのセンサーは、アダプティブ・ディスプレイを強化し、電力消費を最適化し、全体的なエネルギー効率を向上させるため、最新の技術進歩に不可欠なものとなっています。

スマートフォン、タブレット、ノートパソコン、スマートホームデバイスには、自動輝度調整を可能にする環境光センサーが組み込まれており、市場拡大の主な要因となっています。省エネソリューションやシームレスなユーザー体験に対する消費者の嗜好が高まる中、メーカーは画面の見やすさを向上させ、バッテリー寿命を延ばすために高度なセンサーを組み込んでいます。さらに、スマート照明システムの出現は、企業や家庭が周囲の光条件に基づいて照明を動的に調整するインテリジェントなソリューションを求めているため、市場の成長に寄与しています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 9億2,610万米ドル |

| 予測金額 | 26億米ドル |

| CAGR | 11.1% |

自動車産業も市場拡大の主な要因の一つであり、環境光センサーは安全性と快適性を高めるためにADAS(先進運転支援システム)に組み込まれています。これらのセンサーは、ヘッドライトの自動調整、ダッシュボードの照明制御、室内照明の最適化において重要な役割を果たしています。自動車メーカーが視認性の向上と省エネルギーのために最先端技術に投資する中、高性能環境光センサーの需要は急増し続けています。エネルギー効率の高いソリューションを推進する政府の規制や、スマートシティ構想の急速な導入が市場浸透をさらに加速させており、センサーメーカーに新たな機会をもたらしています。

市場はセンサーの種類によってフォトダイオードベース、CMOSベース、赤外線ベースに区分されます。フォトダイオードベースのセンサは、2023年に3億4,960万米ドルを生み出し、光を電気信号に効率的に変換する優れた能力によって人気を集めています。これらのセンサは、民生用電子機器や自動車用アプリケーションで広く使用されており、性能と耐久性が強化されています。一方、赤外線ベースの環境光センサーは、スマートビルディング、温室、偽造品検出システムなどのアプリケーションで採用が増加しており、その高感度と信頼性の恩恵を受けています。

出力タイプにより、市場はアナログ環境光センサーとデジタル環境光センサーに分類されます。デジタルセンサは2024年に42.3%のシェアを占め、急速な技術進歩やスマートデバイスの採用拡大により需要が高まっています。人間中心の照明ソリューションが職場で勢いを増す中、デジタル環境光センサーは明るさの最適化、生産性の向上、エネルギー消費の削減のために導入されています。スマート環境重視の高まりに伴い、デジタルセンサは予測期間を通じて力強い成長を維持すると見られています。

地域別では、北米が2024年に31%のシェアを獲得して市場をリードしており、自動車部門の確立、エネルギー効率規制の厳格化、スマートシティ構想の拡大がその推進力となっています。米国は、スマート家電、革新的な照明ソリューション、自動車技術の絶え間ない進化に対する需要の増加に牽引され、依然として圧倒的なシェアを維持しています。インテリジェントなインフラとエネルギー効率の高いソリューションへの投資が拡大する中、北米の環境光センサー市場は持続的な拡大が見込まれています。

目次

第1章 調査手法と調査範囲

- 市場範囲と定義

- 基本推定と計算

- 予測計算

- データソース

第2章 エグゼクティブサマリー

第3章 業界洞察

- エコシステム分析

- バリューチェーンに影響を与える要因

- 利益率分析

- ディスラプション

- 将来の展望

- メーカー

- 流通業者

- サプライヤーの状況

- 利益率分析

- 主要ニュース

- 規制状況

- 影響要因

- 促進要因

- コンシューマー・エレクトロニクスへの統合の進展

- スマートホーム技術の進歩

- ヘルスケア・アプリケーションの拡大

- エネルギー効率に対する意識の高まり

- 業界の潜在的リスク&課題

- 高度なセンサー技術の高コスト

- 新興国における認知度の低さ

- 促進要因

- 成長可能性分析

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業シェア分析

- 競合のポジショニング・マトリックス

- 戦略展望マトリックス

第5章 市場推計・予測:センサータイプ別、2021年~2034年

- 主要動向

- フォトダイオードベース

- CMOSベース

- 赤外線ベース

第6章 市場推計・予測:出力タイプ別、2021年~2034年

- 主要動向

- アナログ

- デジタル

第7章 市場推計・予測:実装スタイル別、2021年~2034年

- 主要動向

- SMD/SMT

- スルーホール

- その他

第8章 市場推計・予測:集積度別、2021年~2034年

- 主要動向

- ディスクリート

- コンビネーション

第9章 市場推計・予測:アプリケーション別、2021年~2034年

- 主要動向

- 家電

- 自動車

- 産業

- ホームオートメーション

- ヘルスケア

- エンターテイメント

- セキュリティ

- その他

第10章 市場推計・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- 英国

- ドイツ

- フランス

- イタリア

- スペイン

- ロシア

- アジア太平洋

- 中国

- インド

- 日本

- 韓国

- オーストラリア

- ラテンアメリカ

- ブラジル

- メキシコ

- 中東・アフリカ

- 南アフリカ

- サウジアラビア

- アラブ首長国連邦

第11章 企業プロファイル

- Analog Devices(Maxim Integrated)

- ams-OSRAM AG

- Broadcom Inc.

- Everlight Electronics Co., Ltd.

- Honeywell International Inc.

- Melexis NV

- Microchip Technology Inc.

- OmniVision Technologies, Inc.

- ON Semiconductor Corporation

- Panasonic Corporation

- Renesas Electronics Corporation

- ROHM Semiconductor

- Samsung Electronics Co., Ltd.

- Sharp Corporation

- Silicon Labs

- Sony Semiconductor Solutions Corporation

- STMicroelectronics

- Texas Instruments Incorporated

- Vishay Intertechnology

The Global Ambient Light Sensor Market, valued at USD 926.1 million in 2024, is projected to expand at a robust CAGR of 11.1% from 2025 to 2034, driven by rising demand across consumer electronics, automotive, and smart infrastructure sectors. As industries increasingly prioritize automation, energy efficiency, and user-centric technologies, ambient light sensors are becoming an essential component in modern devices and systems. These sensors enhance adaptive displays, optimize power consumption, and improve overall energy efficiency, making them indispensable in the latest technological advancements.

Consumer electronics remain a key driver of market expansion, with smartphones, tablets, laptops, and smart home devices integrating ambient light sensors to enable automatic brightness adjustment. With increasing consumer preference for energy-saving solutions and seamless user experiences, manufacturers are incorporating advanced sensors to enhance screen readability and extend battery life. Additionally, the emergence of smart lighting systems is contributing to market growth as businesses and households seek intelligent solutions that dynamically adjust illumination based on ambient light conditions.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $926.1 Million |

| Forecast Value | $2.6 Billion |

| CAGR | 11.1% |

The automotive industry is another major factor fueling market expansion, with ambient light sensors being integrated into advanced driver-assistance systems (ADAS) to enhance safety and user comfort. These sensors play a crucial role in automatic headlight adjustment, dashboard illumination control, and interior lighting optimization. As automakers invest in cutting-edge technologies for improved visibility and energy conservation, the demand for high-performance ambient light sensors continues to surge. Government regulations promoting energy-efficient solutions and the rapid adoption of smart city initiatives are further accelerating market penetration, creating new opportunities for sensor manufacturers.

The market is segmented by sensor type into photodiode-based, CMOS-based, and infrared-based sensors. Photodiode-based sensors, which generated USD 349.6 million in 2023, are gaining traction due to their superior ability to convert light into electrical signals efficiently. These sensors are extensively used in consumer electronics and automotive applications, offering enhanced performance and durability. Meanwhile, infrared-based ambient light sensors are witnessing increased adoption in applications such as smart buildings, greenhouses, and counterfeit detection systems, benefiting from their high sensitivity and reliability.

Based on output type, the market is categorized into analog and digital ambient light sensors. Digital sensors, which held a 42.3% share in 2024, are seeing heightened demand due to rapid technological advancements and the growing adoption of smart devices. As human-centric lighting solutions gain momentum in workplaces, digital ambient light sensors are being deployed to optimize brightness, improve productivity, and reduce energy consumption. With the rising emphasis on smart environments, digital sensors are expected to maintain strong growth throughout the forecast period.

Geographically, North America led the market with a 31% share in 2024, propelled by a well-established automotive sector, stringent energy efficiency regulations, and expanding smart city initiatives. The United States remains a dominant contributor, driven by increasing demand for smart consumer electronics, innovative lighting solutions, and the continuous evolution of automotive technologies. As investments in intelligent infrastructure and energy-efficient solutions escalate, the North American ambient light sensor market is set for sustained expansion.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope & definitions

- 1.2 Base estimates & calculations

- 1.3 Forecast calculations

- 1.4 Data sources

- 1.4.1 Primary

- 1.4.2 Secondary

- 1.4.2.1 Paid sources

- 1.4.2.2 Public sources

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021-2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Factor affecting the value chain

- 3.1.2 Profit margin analysis

- 3.1.3 Disruptions

- 3.1.4 Future outlook

- 3.1.5 Manufacturers

- 3.1.6 Distributors

- 3.2 Supplier landscape

- 3.3 Profit margin analysis

- 3.4 Key news & initiatives

- 3.5 Regulatory landscape

- 3.6 Impact forces

- 3.6.1 Growth drivers

- 3.6.1.1 Increasing integration in consumer electronics

- 3.6.1.2 Advancements in smart home technologies

- 3.6.1.3 Expansion in healthcare applications

- 3.6.1.4 Rising awareness of energy efficiency

- 3.6.2 Industry pitfalls & challenges

- 3.6.2.1 High costs of advanced sensor technologies

- 3.6.2.2 Limited awareness in emerging economies

- 3.6.1 Growth drivers

- 3.7 Growth potential analysis

- 3.8 Porter's analysis

- 3.9 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Sensor Type, 2021-2034 (USD Million & Unit)

- 5.1 Key trends

- 5.2 Photodiode-based

- 5.3 CMOS-based

- 5.4 Infrared-based

Chapter 6 Market Estimates & Forecast, By Output Type, 2021-2034 (USD Million & Unit)

- 6.1 Key trends

- 6.2 Analog

- 6.3 Digital

Chapter 7 Market Estimates & Forecast, By Mounting Style, 2021-2034 (USD Million & Unit)

- 7.1 Key trends

- 7.2 SMD/SMT

- 7.3 Through hole

- 7.4 Others

Chapter 8 Market Estimates & Forecast, By Integration, 2021-2034 (USD Million & Unit)

- 8.1 Key trends

- 8.2 Discrete

- 8.3 Combination

Chapter 9 Market Estimates & Forecast, By Application, 2021-2034 (USD Million & Unit)

- 9.1 Key trends

- 9.2 Consumer electronics

- 9.3 Automotive

- 9.4 Industrial

- 9.5 Home automation

- 9.6 Healthcare

- 9.7 Entertainment

- 9.8 Security

- 9.9 Others

Chapter 10 Market Estimates & Forecast, By Region, 2021-2034 (USD Million & Unit)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 UK

- 10.3.2 Germany

- 10.3.3 France

- 10.3.4 Italy

- 10.3.5 Spain

- 10.3.6 Russia

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 South Korea

- 10.4.5 Australia

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.6 MEA

- 10.6.1 South Africa

- 10.6.2 Saudi Arabia

- 10.6.3 UAE

Chapter 11 Company Profiles

- 11.1 Analog Devices (Maxim Integrated)

- 11.2 ams-OSRAM AG

- 11.3 Broadcom Inc.

- 11.4 Everlight Electronics Co., Ltd.

- 11.5 Honeywell International Inc.

- 11.6 Melexis NV

- 11.7 Microchip Technology Inc.

- 11.8 OmniVision Technologies, Inc.

- 11.9 ON Semiconductor Corporation

- 11.10 Panasonic Corporation

- 11.11 Renesas Electronics Corporation

- 11.12 ROHM Semiconductor

- 11.13 Samsung Electronics Co., Ltd.

- 11.14 Sharp Corporation

- 11.15 Silicon Labs

- 11.16 Sony Semiconductor Solutions Corporation

- 11.17 STMicroelectronics

- 11.18 Texas Instruments Incorporated

- 11.19 Vishay Intertechnology