|

市場調査レポート

商品コード

1665245

光センサ市場の市場機会、成長促進要因、産業動向分析、2025~2034年予測Light Sensor Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| 光センサ市場の市場機会、成長促進要因、産業動向分析、2025~2034年予測 |

|

出版日: 2024年12月17日

発行: Global Market Insights Inc.

ページ情報: 英文 210 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

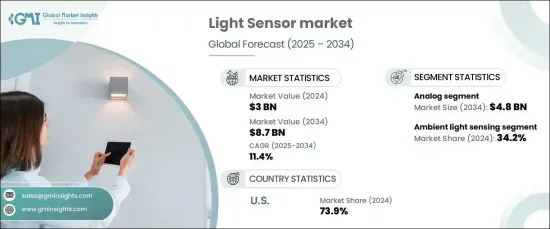

光センサの世界市場は2024年に30億米ドルに達し、2025~2034年のCAGRは11.4%と予測され、大幅な成長が見込まれています。

この目覚しい成長は、高感度、小型、マルチスペクトル光センサの誕生につながった技術の急速な進歩によってもたらされています。これらの技術革新により、より広範なスペクトルの検出や様々な照明条件下での性能向上など、センサの能力が大幅に向上しています。その結果、光センサの用途は複数の産業で拡大し、新たな成長機会を提供しています。

市場はタイプ別に、環境光センシング、近接検知、RGBカラーセンシング、ジェスチャー認識、UV/赤外線(IR)検知に区分されます。このうち、環境光センシングセグメントは2024年に34.2%のシェアを占めて市場をリードしました。環境光センサは、周囲の光強度を測定し、性能を最適化するためにデバイスの設定を調整する上で極めて重要です。これらのセンサは電子機器に広く使用され、ユーザーエクスペリエンスの向上、エネルギー効率の改善、輝度レベルの自動調整と電力節約によるデバイス機能の最適化に役立っています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024年 |

| 予測年 | 2025~2034 |

| 開始金額 | 30億米ドル |

| 予測金額 | 87億米ドル |

| CAGR | 11.4% |

光センサ市場は、出力の観点からアナログセンサとデジタルセンサに分けられます。アナログセンサセグメントは、2034年までに48億米ドルの収益が見込まれています。アナログ光センサは、光強度に比例した連続出力信号を必要とする用途で好まれており、正確でリアルタイムの計測に最適です。その信頼性とアナログシステムとのシームレスな統合により、環境光検出、スマート照明、省エネシステムなどの用途で特に有益です。民生用電子機器、自動車、産業オートメーションなどの産業では、業務効率と性能を向上させるために、こうしたセンサへの依存度が高まっています。

2024年、米国の光センサ市場は世界市場シェアの73.9%を占めました。この優位性は、同国の強力な技術インフラと、民生用電子機器、自動車、医療などの主要セグメントにおける光センサの高い需要によるところが大きいです。IoTデバイスの普及と自律技術の進歩は、先進的光センサのニーズの高まりにさらに貢献しています。さらに、スマートシティプロジェクトやサステイナブルインフラに対する政府の支援は、公共と商業用途における光センサの採用を加速しており、米国が市場リーダーとしての地位をさらに強固なものにしています。

目次

第1章 調査手法と調査範囲

- 市場範囲と定義

- 基本推定と計算

- 予測計算

- データソース

- 1次データ

- 二次資料

- 有料情報源

- 公的情報源

第2章 エグゼクティブサマリー

第3章 産業洞察

- エコシステム分析

- バリューチェーンに影響を与える要因

- 利益率分析

- 変革

- 将来の展望

- メーカー

- 流通業者

- サプライヤーの状況

- 利益率分析

- 主要ニュースと取り組み

- 規制状況

- 影響要因

- 促進要因

- 光センシング技術の技術的進歩

- スマートデバイスとIoT用途の採用増加

- エネルギー効率の高いソリューションと持続可能性への注目の高まり

- 自動車産業と自律走行車の成長

- 産業の潜在的リスク・課題

- 先進的光センシング技術の高コスト

- 統合の複雑さと互換性の問題

- 促進要因

- 成長可能性分析

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業シェア分析

- 競合のポジショニングマトリックス

- 戦略展望マトリックス

第5章 市場推定・予測:タイプ別、2021~2034年

- 主要動向

- 環境光センシング

- 近接センサ

- RGBカラーセンシング

- ジェスチャー認識

- UV/赤外線(IR)検知

第6章 市場推定・予測:出力別、2021~2034年

- 主要動向

- アナログ

- デジタル

第7章 技術別市場推定・予測:技術別、2021~2034年

- 主要動向

- フォトダイオード

- フォトトランジスタ

- 電荷結合素子(CCD)

- 相補型金属酸化膜半導体(CMOS)センサ

第8章 市場推定・予測:最終用途別、2021~2034年

- 主要動向

- 民生用電子機器

- スマートフォン

- テレビ

- タブレット

- ウェアラブル

- 自動車

- 産業用

- その他

第9章 市場推定・予測:地域別、2021~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- 英国

- ドイツ

- フランス

- イタリア

- スペイン

- ロシア

- アジア太平洋

- 中国

- インド

- 日本

- 韓国

- オーストラリア

- ラテンアメリカ

- ブラジル

- メキシコ

- 中東・アフリカ

- 南アフリカ

- サウジアラビア

- アラブ首長国連邦

第10章 企業プロファイル

- Analog Devices, Inc.

- ams-OSRAM AG

- Broadcom Inc.

- Everlight Electronics Co., Ltd.

- Geospace Technologies Corporation

- Hamamatsu Photonics K.K.

- Honeywell International Inc.

- Infineon Technologies AG

- Kyocera Corporation

- Lite-On Technology Corporation

- Microchip Technology Incorporated

- NXP Semiconductors N.V.

- ON Semiconductor Corporation

- OSRAM Opto Semiconductors GmbH

- Panasonic Corporation

- ROHM Semiconductor

- Samsung Electronics Co., Ltd.

- Sharp Corporation

- STMicroelectronics N.V.

- TDK Corporation

- Texas Instruments Incorporated

- Vishay Intertechnology, Inc.

The Global Light Sensor Market reached USD 3 billion in 2024 and is expected to experience substantial growth, with a projected CAGR of 11.4% from 2025 to 2034. This impressive growth is being driven by rapid advancements in technology, which have led to the creation of highly sensitive, compact, and multi-spectral light sensors. These innovations have significantly improved sensor capabilities, such as broader spectrum detection and enhanced performance under various lighting conditions. As a result, the applications of light sensors are expanding across multiple industries, offering new opportunities for growth.

The market is segmented by type into ambient light sensing, proximity detection, RGB color sensing, gesture recognition, and UV/infrared (IR) detection. Among these, the ambient light sensing segment led the market in 2024, holding a 34.2% share. Ambient light sensors are crucial in measuring the surrounding light intensity and adjusting device settings to optimize performance. These sensors are widely used in electronics, helping to enhance user experience, improve energy efficiency, and optimize device functionality by automatically adjusting brightness levels and conserving power.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $3 billion |

| Forecast Value | $8.7 billion |

| CAGR | 11.4% |

In terms of output, the light sensor market is divided into analog and digital sensors. The analog sensor segment is expected to generate USD 4.8 billion in revenue by 2034. Analog light sensors are preferred in applications that require continuous output signals proportional to light intensity, making them ideal for precise and real-time measurements. Their reliability and seamless integration with analog systems make them particularly beneficial in applications such as ambient light detection, smart lighting, and energy-saving systems. Industries like consumer electronics, automotive, and industrial automation are increasingly dependent on these sensors to improve operational efficiency and performance.

In 2024, the U.S. light sensor market accounted for 73.9% of the global market share. This dominance is largely due to the country's strong technological infrastructure and high demand for light sensors in key sectors like consumer electronics, automotive, and healthcare. The growing proliferation of IoT devices and advancements in autonomous technologies further contribute to the rising need for advanced light sensors. Moreover, government support for smart city projects and sustainable infrastructure is accelerating the adoption of light sensors in public and commercial applications, further solidifying the U.S. position as a market leader.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope & definitions

- 1.2 Base estimates & calculations

- 1.3 Forecast calculations

- 1.4 Data sources

- 1.4.1 Primary

- 1.4.2 Secondary

- 1.4.2.1 Paid sources

- 1.4.2.2 Public sources

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021-2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Factor affecting the value chain

- 3.1.2 Profit margin analysis

- 3.1.3 Disruptions

- 3.1.4 Future outlook

- 3.1.5 Manufacturers

- 3.1.6 Distributors

- 3.2 Supplier landscape

- 3.3 Profit margin analysis

- 3.4 Key news & initiatives

- 3.5 Regulatory landscape

- 3.6 Impact forces

- 3.6.1 Growth drivers

- 3.6.1.1 Technological advancements in light sensing technology

- 3.6.1.2 Rising adoption of smart devices and IoT applications

- 3.6.1.3 Increase in energy-efficient solutions and sustainability focus

- 3.6.1.4 Growth in automotive industry and autonomous vehicles

- 3.6.2 Industry pitfalls & challenges

- 3.6.2.1 High cost of advanced light sensing technologies

- 3.6.2.2 Integration complexity and compatibility issues

- 3.6.1 Growth drivers

- 3.7 Growth potential analysis

- 3.8 Porter’s analysis

- 3.9 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Type, 2021-2034 (USD Billion) (Volume Unit)

- 5.1 Key trends

- 5.2 Ambient light sensing

- 5.3 Proximity detector

- 5.4 RGB color sensing

- 5.5 Gesture recognition

- 5.6 UV/infrared light (IR) detection

Chapter 6 Market Estimates & Forecast, By Output, 2021-2034 (USD Billion) (Volume Unit)

- 6.1 Key trends

- 6.2 Analog

- 6.3 Digital

Chapter 7 Market Estimates & Forecast, By Technology, 2021-2034 (USD Billion) (Volume Unit)

- 7.1 Key trends

- 7.2 Photodiodes

- 7.3 Phototransistors

- 7.4 Charge-Coupled devices (CCDs)

- 7.5 Complementary metal-oxide-semiconductor (CMOS) sensors

Chapter 8 Market Estimates & Forecast, By End Use, 2021-2034 (USD Billion) (Volume Unit)

- 8.1 Key trends

- 8.2 Consumer electronics

- 8.2.1 Smartphones

- 8.2.2 Televisions

- 8.2.3 Tablets

- 8.2.4 Wearables

- 8.3 Automotive

- 8.4 Industrial

- 8.5 Other

Chapter 9 Market Estimates & Forecast, By Region, 2021-2034 (USD Billion) (Volume Unit)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 UK

- 9.3.2 Germany

- 9.3.3 France

- 9.3.4 Italy

- 9.3.5 Spain

- 9.3.6 Russia

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 South Korea

- 9.4.5 Australia

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.6 MEA

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 Analog Devices, Inc.

- 10.2 ams-OSRAM AG

- 10.3 Broadcom Inc.

- 10.4 Everlight Electronics Co., Ltd.

- 10.5 Geospace Technologies Corporation

- 10.6 Hamamatsu Photonics K.K.

- 10.7 Honeywell International Inc.

- 10.8 Infineon Technologies AG

- 10.9 Kyocera Corporation

- 10.10 Lite-On Technology Corporation

- 10.11 Microchip Technology Incorporated

- 10.12 NXP Semiconductors N.V.

- 10.13 ON Semiconductor Corporation

- 10.14 OSRAM Opto Semiconductors GmbH

- 10.15 Panasonic Corporation

- 10.16 ROHM Semiconductor

- 10.17 Samsung Electronics Co., Ltd.

- 10.18 Sharp Corporation

- 10.19 STMicroelectronics N.V.

- 10.20 TDK Corporation

- 10.21 Texas Instruments Incorporated

- 10.22 Vishay Intertechnology, Inc.