インターフェースIC市場の機会、成長促進要因、産業動向分析、2025年~2034年の予測

Interface IC Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025-2034- 発行日

- ページ情報

- 英文 200 Pages

- 納期

- 2~3営業日

- 商品コード

- 1698510

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

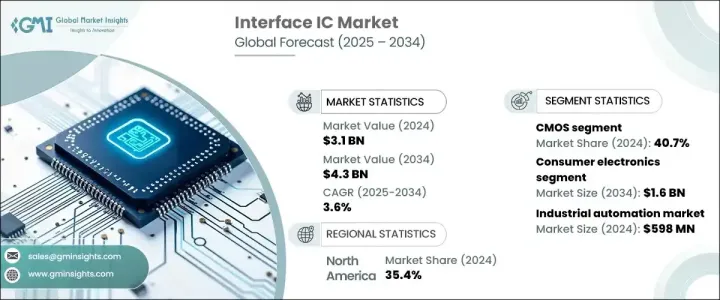

世界のインターフェースIC市場は、2024年には31億米ドルの評価額に達し、2025年から2034年にかけてCAGR 3.6%で成長すると予測されています。

シームレスな接続性、高速データ伝送、エネルギー効率の高い電子システムに対する需要の高まりが、主要産業全体の拡大を促進しています。技術の進歩が加速するなか、インターフェースICは次世代デバイスに不可欠な部品となりつつあり、リアルタイムのデータ交換を最適化し、システム全体の性能を高めています。デジタルトランスフォーメーション、オートメーション、コネクテッドデバイスの採用が進むにつれ、先進的なインターフェースICソリューションへのニーズがさらに高まっています。

特に、電気自動車(EV)や自律走行技術への急速なシフトに伴い、車載アプリケーションにおけるインターフェースICの普及率が高まっていることが、大きな成長要因となっています。これらのコンポーネントは、電子通信と安全システムを管理し、車両ネットワーク内での信頼性と効率性の高いデータ・トランスミッションを確保する上で重要な役割を果たしています。ADAS(先進運転支援システム)の拡大と高性能インフォテインメント・ソリューションの統合は、自動車分野におけるインターフェースICの重要性の高まりをさらに強調しています。さらに、産業オートメーションとスマート製造プロセスは、業務効率の改善とエネルギー消費の削減を目指す企業の需要を引き続き牽引しています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 31億米ドル |

| 予測金額 | 43億米ドル |

| CAGR | 3.6% |

インターフェースIC市場を形成するもう1つの主な要因は、高速データ伝送技術への依存度が高まっていることです。スマートホームオートメーション、モノのインターネット(IoT)デバイス、高解像度ディスプレイの普及に伴い、効率的なシグナルインテグリティと低消費電力ソリューションの必要性が高まっています。通信、民生用電子機器、産業用オートメーションなどの業界では、複数のシステム間でスムーズなデータフローを確保し、高度な機能性と接続性の向上を可能にするインターフェースICに大きく依存しています。産業界が5GネットワークやAIを搭載したシステムへと移行するにつれて、高性能インターフェースICの採用は大幅に増加するとみられます。

技術的には、市場はCMOS、バイポーラ、BiCMOSインターフェースICに区分されます。CMOS技術は、主に民生用電子機器、自動車、産業オートメーションに広く応用されているため、2024年の市場シェアは40.7%で、この分野をリードしています。同セグメントは2023年に12億米ドルを占め、そのコスト効率、低消費電力、高速データ転送機能が牽引しています。メーカーがエネルギー効率とコンパクト設計を優先する中、CMOSベースのインターフェースICの需要は急増し続けています。

エンドユーザー別では、民生用電子機器、自動車、産業用オートメーション、通信、その他に分類されます。民生用電子機器は、2034年までに16億米ドルの売上が見込まれ、市場成長の主要な促進要因としての地位を維持しています。2024年、この分野は世界のインターフェースIC市場の36.2%を占める。スマート・ホーム・オートメーションの採用増加、高解像度OLEDおよびAMOLEDディスプレイの需要拡大、コネクテッド・デバイスの利用拡大が、このセグメントの拡大に寄与しています。ウェアラブル、ワイヤレス充電ソリューション、次世代ディスプレイ技術の普及に伴い、民生用電子機器におけるインターフェースICの役割は引き続き極めて重要です。

米国のインターフェースIC市場は、ADAS搭載車とEVの旺盛な需要に牽引され、2024年には8億4,310万米ドルに達しました。デジタルトランスフォーメーションと産業オートメーションへの投資の増加が市場拡大を加速しています。電子システムの急速な進化と効率的なデータ転送のニーズの高まりにより、インターフェースICの採用は複数の産業で増加し続けています。半導体メーカーの強い存在感と通信技術の継続的な進歩が、この地域の市場成長軌道をさらに強化しています。

目次

第1章 調査手法と調査範囲

第2章 エグゼクティブサマリー

第3章 業界洞察

- エコシステム分析

- 業界への影響要因

- 促進要因

- 家電製品の拡大

- 自動車技術の進歩

- 産業オートメーションの成長

- 通信インフラの拡大

- 業界の潜在的リスク&課題

- 急速な技術進歩

- 統合と互換性の問題

- 促進要因

- 潜在成長力の分析

- 規制状況

- 技術情勢

- 将来の市場動向

- ギャップ分析

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業シェア分析

- 主要市場プレーヤーの競合分析

- 競合のポジショニングマトリックス

- 戦略ダッシュボード

第5章 市場推計・予測:インターフェースタイプ別、2021年~2034年

- 主要動向

- アナログ

- デジタル

- ミックスドシグナル

第6章 市場推計・予測:インターフェース規格別、2021年~2034年

- 主要動向

- シリアル

- パラレル

- 高速

第7章 市場推計・予測:技術別、2021年~2034年

- 主要動向

- CMOS

- バイポーラ

- BiCMOS

第8章 市場推計・予測:用途別、2021年~2034年

- 主要動向

- コンシューマーエレクトロニクス

- 自動車

- 産業オートメーション

- 通信

- その他

第9章 市場推計・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- スペイン

- イタリア

- オランダ

- その他欧州

- アジア太平洋

- 中国

- インド

- 日本

- オーストラリア

- 韓国

- その他アジア太平洋地域

- ラテンアメリカ

- ブラジル

- メキシコ

- その他ラテンアメリカ

- 中東・アフリカ

- サウジアラビア

- 南アフリカ

- アラブ首長国連邦

- その他中東とアフリカ

第10章 企業プロファイル

- Allegro Microsystems

- Analog Devices, Inc.

- Broadcom Inc.

- Cirrus Logic, Inc.

- Diodes Incorporated

- Elmos Semiconductor SE

- IBS Electronic Group

- Ivelta

- Mouser Electronics, Inc.

- Nuvoton Technology Corporation

- NXP Semiconductors N.V.

- ON Semiconductor Corporation

- Renesas Electronics Corporation

- ROHM Semiconductor

- SEIKO Epson Corporation

- Silicon Labs

- STMicroelectronics N.V.

- Symmetry Electronics

- Texas Instruments Incorporated

- Toshiba Corporation

目次

The Global Interface IC Market continues to reach a valuation of USD 3.1 billion in 2024 and is projected to grow at a CAGR of 3.6% between 2025 and 2034. Increasing demand for seamless connectivity, high-speed data transmission, and energy-efficient electronic systems is driving expansion across key industries. As technological advancements accelerate, interface ICs are becoming essential components in next-generation devices, optimizing real-time data exchange and enhancing overall system performance. The increasing adoption of digital transformation, automation, and connected devices is further fueling the need for advanced interface IC solutions.

The rising penetration of interface ICs in automotive applications is a significant growth factor, particularly with the rapid shift toward electric vehicles (EVs) and autonomous driving technology. These components play a critical role in managing electronic communication and safety systems, ensuring reliable and efficient data transmission within vehicle networks. The expansion of advanced driver assistance systems (ADAS) and the integration of high-performance infotainment solutions further underscore the growing importance of interface ICs in the automotive sector. Additionally, industrial automation and smart manufacturing processes continue to drive demand as businesses seek to improve operational efficiency and reduce energy consumption.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $3.1 Billion |

| Forecast Value | $4.3 Billion |

| CAGR | 3.6% |

Another major driver shaping the interface IC market is the increasing reliance on high-speed data transmission technologies. With the proliferation of smart home automation, Internet of Things (IoT) devices, and high-resolution displays, there is a greater need for efficient signal integrity and low-power consumption solutions. Industries such as telecommunications, consumer electronics, and industrial automation rely heavily on interface ICs to ensure smooth data flow across multiple systems, enabling advanced functionalities and enhanced connectivity. As industries transition toward 5G networks and AI-powered systems, the adoption of high-performance interface ICs is set to rise significantly.

In terms of technology, the market is segmented into CMOS, Bipolar, and BiCMOS interface ICs. CMOS technology led the segment in 2024, holding a 40.7% market share, primarily due to its widespread application in consumer electronics, automotive, and industrial automation. The segment accounted for USD 1.2 billion in 2023, driven by its cost-effectiveness, low power consumption, and high-speed data transfer capabilities. As manufacturers prioritize energy efficiency and compact design, the demand for CMOS-based interface ICs continues to surge.

By end-user, the market is categorized into consumer electronics, automotive, industrial automation, telecommunications, and others. Consumer electronics is anticipated to generate USD 1.6 billion by 2034, maintaining its strong position as a key driver of market growth. In 2024, this segment accounted for 36.2% of the global interface IC market. The increasing adoption of smart home automation, growing demand for high-resolution OLED and AMOLED displays, and the expanding use of connected devices contribute to the segment's expansion. With the proliferation of wearables, wireless charging solutions, and next-generation display technologies, the role of interface ICs in consumer electronics remains pivotal.

The United States interface IC market reached USD 843.1 million in 2024, driven by robust demand for ADAS-equipped vehicles and EVs. Increased investment in digital transformation and industrial automation is accelerating market expansion. With the rapid evolution of electronic systems and the growing need for efficient data transfer, the adoption of interface ICs continues to rise across multiple industries. The strong presence of semiconductor manufacturers and continuous advancements in communication technologies further reinforce the market growth trajectory in the region.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Base estimates and calculations

- 1.3.1 Base year calculation

- 1.3.2 Key trends for market estimation

- 1.4 Forecast model

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.5.2 Data mining sources

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Expansion of consumer electronics

- 3.2.1.2 Advancements in automotive technology

- 3.2.1.3 Growth in industrial automation

- 3.2.1.4 Expansion of telecommunication infrastructure

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Rapid technological advancements

- 3.2.2.2 Integration and compatibility issues

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.5 Technology landscape

- 3.6 Future market trends

- 3.7 Gap analysis

- 3.8 Porter's analysis

- 3.9 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategy dashboard

Chapter 5 Market Estimates and Forecast, By Type of Interface, 2021 – 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Analog

- 5.3 Digital

- 5.4 Mixed-Signal

Chapter 6 Market Estimates and Forecast, By Interface Standard, 2021 – 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Serial

- 6.3 Parallel

- 6.4 High-Speed

Chapter 7 Market Estimates and Forecast, By Technology, 2021 – 2034 ($ Mn)

- 7.1 Key trends

- 7.2 CMOS

- 7.3 Bipolar

- 7.4 BiCMOS

Chapter 8 Market Estimates and Forecast, By End-Use, 2021 – 2034 ($ Mn)

- 8.1 Key trends

- 8.2 Consumer electronics

- 8.3 Automotive

- 8.4 Industrial automation

- 8.5 Telecommunications

- 8.6 Others

Chapter 9 Market Estimates and Forecast, By Region, 2021 – 2034 ($ Mn & Units)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Netherlands

- 9.3.7 Rest of Europe

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.4.6 Rest of Asia Pacific

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Rest of Latin America

- 9.6 Middle East and Africa

- 9.6.1 Saudi Arabia

- 9.6.2 South Africa

- 9.6.3 UAE

- 9.6.4 Rest of Middle East & Africa

Chapter 10 Company Profiles

- 10.1 Allegro Microsystems

- 10.2 Analog Devices, Inc.

- 10.3 Broadcom Inc.

- 10.4 Cirrus Logic, Inc.

- 10.5 Diodes Incorporated

- 10.6 Elmos Semiconductor SE

- 10.7 IBS Electronic Group

- 10.8 Ivelta

- 10.9 Mouser Electronics, Inc.

- 10.10 Nuvoton Technology Corporation

- 10.11 NXP Semiconductors N.V.

- 10.12 ON Semiconductor Corporation

- 10.13 Renesas Electronics Corporation

- 10.14 ROHM Semiconductor

- 10.15 SEIKO Epson Corporation

- 10.16 Silicon Labs

- 10.17 STMicroelectronics N.V.

- 10.18 Symmetry Electronics

- 10.19 Texas Instruments Incorporated

- 10.20 Toshiba Corporation

- 発行日

- 発行

- Global Market Insights Inc.

- ページ情報

- 英文 200 Pages

- 納期

- 2~3営業日