|

市場調査レポート

商品コード

1698268

商用電気車両用トラクションモーター市場の機会、成長促進要因、産業動向分析、2025年~2034年の予測Electric Commercial Vehicle Traction Motor Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025-2034 |

||||||

カスタマイズ可能

|

|||||||

| 商用電気車両用トラクションモーター市場の機会、成長促進要因、産業動向分析、2025年~2034年の予測 |

|

出版日: 2025年02月28日

発行: Global Market Insights Inc.

ページ情報: 英文 175 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

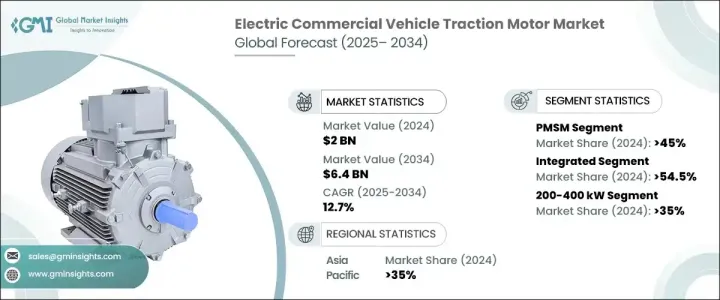

商用電気車両用トラクションモーターの世界市場規模は2024年に20億米ドルとなり、2025年から2034年にかけてCAGR 12.7%で成長すると予測されています。

この業界は、効率、耐久性、性能の進歩によって急速に進化しています。永久磁石同期モータ(PMSM)、スイッチドリラクタンスモータ(SRM)、ラテラルフラックスモータなどの新興モータ技術は、無駄を最小限に抑えながらエネルギー出力を向上させています。高度な冷却システムを備えた炭化ケイ素(SiC)インバータは、エネルギー使用をさらに最適化し、走行距離を延ばし、全体的な性能を向上させています。軽量素材とコンパクト設計によりトルク密度が向上し、大型商用車に理想的なモーターとなっています。一方、急速充電インフラとバッテリー効率の開発により、都市部でも長距離輸送用途でも電気トラック・バスの実用性が向上しています。充電ステーションの増加により、フリートオペレーターの待ち時間が大幅に短縮されています。

商用電気車両用トラクションモーター市場は、モータータイプ、車軸アーキテクチャ、車両カテゴリー、定格出力によって区分されます。PMSMは、高いエネルギー効率、コンパクトな構造、優れた出力により、2024年の総売上の45%以上を占めています。これらのモーターは優れたトルク密度と回生ブレーキを提供するため、電気トラックやバスに好ましい選択肢となっています。車軸アーキテクチャ別では、一体型e-アクスルが2024年の売上シェア54.5%で市場をリードしました。これらのシステムは、モーター、インバーター、トランスミッションを1つのユニットに統合し、重量を減らし、エネルギー効率を高め、電気トラックやバン内のスペースを最適化します。セントラルドライブユニットは、高トルクと耐久性が重要なヘビーデューティー用途には依然として不可欠です。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 20億米ドル |

| 予測金額 | 64億米ドル |

| CAGR | 12.7% |

車両カテゴリー別では、厳しい排出ガス規制と車両電動化の進展により、中型・大型トラックが2024年の市場を独占しました。これらのトラックには、厳しい負荷の下でも効率を維持できる強力で高トルクのトラクション・モーターが必要です。高度な熱管理とモジュール式モーター設計により、信頼性がさらに向上し、総所有コストが削減されています。普及が進むにつれ、メーカーは様々な商用EVセグメントをシームレスに統合するためのスケーラブルなモーター・プラットフォームを開発しています。

定格出力ベースでは、200~400kWのセグメントが2024年に最大のシェアを占め、総売上高の35%以上を占める。このレンジのモーターは長距離電気トラックやバスに最適で、持続可能な物流や貨物輸送をサポートします。100 kW未満のモーターは主に小型電気バンや都市部の配送車に使用され、100~200 kWのモーターは小型・中型トラックに広く使用されています。400 kW以上のカテゴリーは、水素燃料電池車や電動採掘トラックなど、高性能アプリケーション用に確保されています。

アジア太平洋地域は、2024年に世界市場の35%以上を占め、最大のシェアを占めました。中国が支配的なプレーヤーとして台頭し、2034年には18億米ドルに達すると予測され、政策的インセンティブ、技術の進歩、電池と希土類材料の生産における牙城がその燃料となっています。

目次

第1章 調査手法と調査範囲

- 調査デザイン

- 調査アプローチ

- データ収集方法

- 基本推定と計算

- 基準年の算出

- 市場推計の主要動向

- 予測モデル

- 1次調査と検証

- 市場範囲と定義

第2章 エグゼクティブサマリー

第3章 業界洞察

- エコシステム分析

- モーターメーカー

- バッテリーメーカー

- OEMメーカー

- パワーエレクトロニクス・メーカー

- 充電インフラ・プロバイダー

- サプライヤーの状況

- 利益率分析

- 技術と革新の展望

- 特許分析

- 主要ニュースとイニシアチブ

- 新興企業の資金調達分析

- 規制状況

- 影響要因

- 促進要因

- 電気商用車(ECVS)の採用増加

- 厳しい排出規制と持続可能性目標

- モーター効率と技術の進歩

- 充電インフラの拡大とバッテリーの進歩

- 業界の潜在的リスク&課題

- フリート・オペレーターにとって高い初期コストと限られたROI

- サプライチェーンと原材料の制約

- 促進要因

- 成長可能性分析

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業シェア分析

- 競合のポジショニング・マトリックス

- 戦略展望マトリックス

第5章 市場推計・予測:モーター別、2021年~2034年

- 主要動向

- AC誘導モーター

- 永久磁石同期モータ(PMSM)

- スイッチドリラクタンスモーター(SRM)

- DCモーター

第6章 市場推計・予測:自動車別、2021年~2034年

- 主要動向

- ピックアップトラック

- 中型・大型トラック

- バン

- バス

第7章 市場推計・予測:定格出力別、2021年~2034年

- 主要動向

- 100kW未満

- 100-200 kW

- 200-400 kW

- 400kW以上

第8章 市場推計・予測:車軸アーキテクチャ別、2021年~2034年

- 主要動向

- 統合型

- セントラルドライブユニット

第9章 市場推計・予測:トランスミッション別、2021~2034年

- 主要動向

- シングルスピード駆動

- マルチスピードドライブ

第10章 市場推計・予測:設計別、2021年~2034年

- 主要動向

- ラジアル磁束

- 軸方向磁束

第11章 市場推計・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- 英国

- ドイツ

- フランス

- イタリア

- スペイン

- ロシア

- 北欧

- アジア太平洋

- 中国

- インド

- 日本

- オーストラリア

- 韓国

- 東南アジア

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- UAE

- 南アフリカ

- サウジアラビア

第12章 企業プロファイル

- ABB

- Allison Transmission

- BorgWarner

- Bosch

- Continental

- Dana

- Danfoss Editron

- General Electric

- Hitachi Automotive

- Magna

- Mitsubishi Electric

- Nidec

- Siemens

- Skoda Transportation

- Toshiba

- Valeo

- Wabtec

- Wolong Electric

- Yaskawa Electric

- ZF

The Global Electric Commercial Vehicle Traction Motor Market was valued at USD 2 billion in 2024 and is projected to grow at a CAGR of 12.7% from 2025 to 2034. The industry is rapidly evolving, driven by advancements in efficiency, durability, and performance. Emerging motor technologies, including permanent magnet synchronous motors (PMSM), switched reluctance motors (SRM), and lateral flux motors, are enhancing energy output while minimizing waste. Silicon carbide (SiC) inverters with advanced cooling systems are further optimizing energy use, extending driving range, and improving overall performance. Lightweight materials and compact designs are increasing torque density, making motors ideal for heavy-duty commercial vehicles. Meanwhile, developments in fast-charging infrastructure and battery efficiency are improving the practicality of electric trucks and buses for both urban and long-haul applications. The increasing number of charging stations is significantly reducing wait times for fleet operators.

The electric commercial vehicle traction motor market is segmented by motor type, axle architecture, vehicle category, and power rating. PMSM accounted for over 45% of total revenue in 2024 due to its high energy efficiency, compact structure, and superior power output. These motors offer excellent torque density and regenerative braking, making them the preferred choice for electric trucks and buses. On the basis of axle architecture, integrated e-axles led the market with a 54.5% revenue share in 2024. These systems integrate motors, inverters, and transmissions into a single unit, reducing weight, increasing energy efficiency, and optimizing space within electric trucks and vans. Central drive units remain essential for heavy-duty applications where high torque and durability are critical.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $2 Billion |

| Forecast Value | $6.4 Billion |

| CAGR | 12.7% |

By vehicle category, medium and heavy-duty trucks dominated the market in 2024, driven by strict emissions regulations and increasing fleet electrification. These trucks require powerful, high-torque traction motors that maintain efficiency under demanding loads. Advanced thermal management and modular motor designs are further improving reliability and reducing the total cost of ownership. As adoption grows, manufacturers are developing scalable motor platforms for seamless integration across various commercial EV segments.

Based on power rating, the 200-400 kW segment held the largest share in 2024, contributing over 35% of total revenue. Motors in this range are ideal for long-haul electric trucks and buses, supporting sustainable logistics and freight transport. Motors below 100 kW primarily serve compact electric vans and urban delivery vehicles, while 100-200 kW motors are widely used in light and medium-duty trucks. The above 400 kW category is reserved for high-performance applications, including hydrogen fuel cell-powered vehicles and electric mining trucks.

The Asia Pacific region held the largest share of the market in 2024, accounting for over 35% of the global industry. China emerged as the dominant player, projected to reach USD 1.8 billion by 2034, fueled by policy incentives, technological advancements, and its stronghold in battery and rare-earth material production.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.1.1 Research approach

- 1.1.2 Data collection methods

- 1.2 Base estimates & calculations

- 1.2.1 Base year calculation

- 1.2.2 Key trends for market estimation

- 1.3 Forecast model

- 1.4 Primary research and validation

- 1.4.1 Primary sources

- 1.4.2 Data mining sources

- 1.5 Market scope & definition

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Motor manufacturers

- 3.1.2 Battery suppliers

- 3.1.3 OEMs

- 3.1.4 Power electronics suppliers

- 3.1.5 Charging infrastructure providers

- 3.2 Supplier landscape

- 3.3 Profit margin analysis

- 3.4 Technology & innovation landscape

- 3.5 Patent analysis

- 3.6 Key news & initiatives

- 3.7 Startup funding analysis

- 3.8 Regulatory landscape

- 3.9 Impact forces

- 3.9.1 Growth drivers

- 3.9.1.1 Rising adoption of electric commercial vehicles (ECVS)

- 3.9.1.2 Stringent emission regulations & sustainability goals

- 3.9.1.3 Advancements in motor efficiency & technology

- 3.9.1.4 Expansion of charging infrastructure & battery advancements

- 3.9.2 Industry pitfalls & challenges

- 3.9.2.1 High initial cost & limited ROI for fleet operators

- 3.9.2.2 Supply chain & raw material constraints

- 3.9.1 Growth drivers

- 3.10 Growth potential analysis

- 3.11 Porter’s analysis

- 3.12 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Motor, 2021 - 2034 ($Bn, Units)

- 5.1 Key trends

- 5.2 AC induction motors

- 5.3 Permanent magnet synchronous motors (PMSM)

- 5.4 Switched reluctance motors (SRM)

- 5.5 DC motors

Chapter 6 Market Estimates & Forecast, By Vehicle, 2021 - 2034 ($Bn, Units)

- 6.1 Key trends

- 6.2 Pickups trucks

- 6.3 Medium and heavy-duty trucks

- 6.4 Vans

- 6.5 Buses

Chapter 7 Market Estimates & Forecast, By Power Rating, 2021 - 2034 ($Bn, Units)

- 7.1 Key trends

- 7.2 Less than 100 kW

- 7.3 100-200 kW

- 7.4 200-400 kW

- 7.5 Above 400 kW

Chapter 8 Market Estimates & Forecast, By Axle Architecture, 2021 - 2034 ($Bn, Units)

- 8.1 Key trends

- 8.2 Integrated

- 8.3 Central drive unit

Chapter 9 Market Estimates & Forecast, By Transmission, 2021 - 2034 ($Bn, Units)

- 9.1 Key trends

- 9.2 Single-speed drive

- 9.3 Multi-speed drive

Chapter 10 Market Estimates & Forecast, By Design, 2021 - 2034 ($Bn, Units)

- 10.1 Key trends

- 10.2 Radial flux

- 10.3 Axial flux

Chapter 11 Market Estimates & Forecast, By Region, 2021 - 2034 ($Bn, Units)

- 11.1 Key trends

- 11.2 North America

- 11.2.1 U.S.

- 11.2.2 Canada

- 11.3 Europe

- 11.3.1 UK

- 11.3.2 Germany

- 11.3.3 France

- 11.3.4 Italy

- 11.3.5 Spain

- 11.3.6 Russia

- 11.3.7 Nordics

- 11.4 Asia Pacific

- 11.4.1 China

- 11.4.2 India

- 11.4.3 Japan

- 11.4.4 Australia

- 11.4.5 South Korea

- 11.4.6 Southeast Asia

- 11.5 Latin America

- 11.5.1 Brazil

- 11.5.2 Mexico

- 11.5.3 Argentina

- 11.6 MEA

- 11.6.1 UAE

- 11.6.2 South Africa

- 11.6.3 Saudi Arabia

Chapter 12 Company Profiles

- 12.1 ABB

- 12.2 Allison Transmission

- 12.3 BorgWarner

- 12.4 Bosch

- 12.5 Continental

- 12.6 Dana

- 12.7 Danfoss Editron

- 12.8 General Electric

- 12.9 Hitachi Automotive

- 12.10 Magna

- 12.11 Mitsubishi Electric

- 12.12 Nidec

- 12.13 Siemens

- 12.14 Skoda Transportation

- 12.15 Toshiba

- 12.16 Valeo

- 12.17 Wabtec

- 12.18 Wolong Electric

- 12.19 Yaskawa Electric

- 12.20 ZF