|

市場調査レポート

商品コード

1698253

フォンダパリヌクス市場の機会、成長促進要因、産業動向分析、2025年~2034年の予測Fondaparinux Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| フォンダパリヌクス市場の機会、成長促進要因、産業動向分析、2025年~2034年の予測 |

|

出版日: 2025年02月25日

発行: Global Market Insights Inc.

ページ情報: 英文 132 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

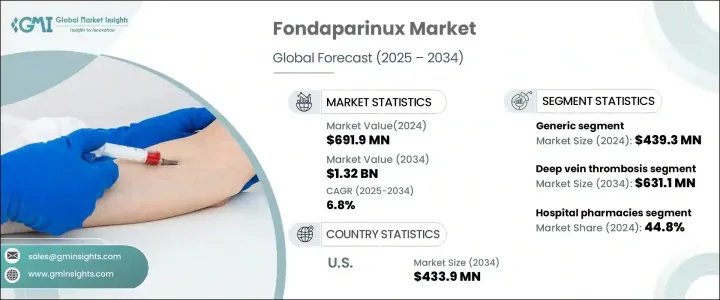

フォンダパリヌクスの世界市場は2024年に6億9,190万米ドルと評価され、2025年から2034年にかけてCAGR 6.8%で拡大すると予測されています。

深部静脈血栓症(DVT)や肺塞栓症(PE)などの血栓塞栓性疾患の発生率の増加や、効果的な抗凝固療法への嗜好の高まりが市場拡大に拍車をかけています。合成抗凝固剤であるフォンダパリヌクスは、血栓の予防と治療において重要な役割を果たしており、ヘパリンによる合併症のリスクが低い標的作用機序を提供しています。整形外科手術を含む外科手術件数の増加は、抗凝固剤治療に対する需要をさらに促進し、このセグメントにおける主要プレーヤーとしてのフォンダパリヌクスの地位を確固たるものにしています。ヘルスケア・インフラの拡大と費用対効果の高い治療選択肢の増加が引き続き市場の成長を支えています。さらに、有利な規制政策と先進的な抗凝固療法の推進が、入院・外来を問わずフォンダパリヌクスの採用を強化しています。

フォンダパリヌクス市場はブランド品とジェネリック品に分けられ、ジェネリック品は手頃な価格で広く使用されているため、支配的な地位を維持しています。2024年、ジェネリック医薬品の売上高は4億3,930万米ドルに達し、市場での存在感を示しました。特に長期の抗凝固療法が必要な症例では、ヘルスケアプロバイダーや患者がブランド薬に代わる費用対効果の高い薬剤を求めるため、フォンダパリヌクスのジェネリック医薬品に対する需要は増加の一途をたどっています。継続的な血栓予防を必要とする患者が増加する中、ジェネリック製剤は利用しやすく予算に見合ったソリューションを提供し、病院、診療所、在宅医療の現場での採用を促進しています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 6億9,190万米ドル |

| 予測金額 | 13億2,000万米ドル |

| CAGR | 6.8% |

用途別セグメントによると、フォンダパリヌクスは深部静脈血栓症(DVT)、肺塞栓症(PE)、急性冠症候群(ACS)の治療に広く使用されています。2024年、DVT分野は市場の47.8%を占め、これは世界のDVT症例の増加を反映しています。高齢者や慢性的な健康状態にある人は血栓形成のリスクが高く、効果的な抗凝固療法が不可欠です。フォンダパリヌクスは、その確実な有効性、予測可能な薬物動態、従来の抗凝固薬とは異なり定期的な血液モニタリングが不要であるという利点から、依然として好ましい治療薬です。

米国のフォンダパリヌクス市場は2024年に2億4,430万米ドルを生み出し、2034年には4億3,390万米ドルに達すると予測されています。この拡大には、整形外科手術の多さ、高齢化、抗凝固療法を必要とする重篤な疾患の増加など、いくつかの要因が寄与しています。高度な治療プロトコルの採用が進み、より安全で効率的な抗凝固薬への需要が高まっていることが、米国におけるフォンダパリヌクスの市場プレゼンスを引き続き押し上げ、現代ヘルスケアにおけるその役割を強化しています。

目次

第1章 調査手法と調査範囲

第2章 エグゼクティブサマリー

第3章 業界洞察

- エコシステム分析

- 業界への影響要因

- 促進要因

- 血栓塞栓性疾患の増加

- 股関節および膝関節移植手術の増加

- 世界の高齢化人口の急増

- 業界の潜在的リスク&課題

- フォンダパリヌクスに伴う副作用

- 促進要因

- 成長可能性分析

- 規制状況

- パイプライン分析

- 今後の市場動向

- ギャップ分析

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業シェア分析

- 企業マトリックス分析

- 主要市場プレーヤーの競合分析

- 競合のポジショニングマトリックス

- 戦略ダッシュボード

第5章 市場推計・予測:製品タイプ別、2021年~2034年

- 主要動向

- ブランド

- ジェネリック

第6章 市場推計・予測:用途別、2021年~2034年

- 主要動向

- 深部静脈血栓症

- 肺塞栓症

- 急性冠症候群

- その他の用途

第7章 市場推計・予測:流通チャネル別、2021~2034年

- 主要動向

- 病院薬局

- 小売薬局

- オンライン薬局

第8章 市場推計・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- スペイン

- イタリア

- オランダ

- アジア太平洋

- 中国

- インド

- 日本

- オーストラリア

- 韓国

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- サウジアラビア

- 南アフリカ

- アラブ首長国連邦

第9章 企業プロファイル

- Abbott Laboratories

- Alchemia

- Apotex

- Aurobindo

- Dr. Reddy’s Laboratories

- Jiangsu Hengrui Medicine

- Lupin Pharmaceuticals

- Sandoz

- ScinoPharm Taiwan

- Viatris

The Global Fondaparinux Market was valued at USD 691.9 million in 2024 and is projected to expand at a CAGR of 6.8% between 2025 and 2034. The market expansion is fueled by the increasing incidence of thromboembolic disorders such as deep vein thrombosis (DVT) and pulmonary embolism (PE), as well as the growing preference for effective anticoagulation therapies. Fondaparinux, a synthetic anticoagulant, plays a vital role in preventing and treating blood clots, offering a targeted mechanism of action with a lower risk of heparin-induced complications. The rising number of surgical procedures, including orthopedic surgeries, further propels the demand for anticoagulant treatments, solidifying fondaparinux's position as a key player in this segment. The expansion of healthcare infrastructure and the increased availability of cost-effective treatment options continue to support market growth. Additionally, favorable regulatory policies and the push for advanced anticoagulant therapies reinforce fondaparinux's adoption across inpatient and outpatient settings.

The fondaparinux market is divided into branded and generic versions, with the generic segment maintaining a dominant position due to its affordability and widespread use. In 2024, the generic segment generated USD 439.3 million in revenue, highlighting its strong market presence. The demand for generic fondaparinux continues to rise as healthcare providers and patients seek cost-effective alternatives to branded drugs, particularly in cases requiring long-term anticoagulation therapy. With an increasing number of patients requiring continued blood clot prevention, generic formulations provide an accessible and budget-friendly solution, driving adoption across hospitals, clinics, and home care settings.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $691.9 Million |

| Forecast Value | $1.32 Billion |

| CAGR | 6.8% |

Segmentation by application reveals that fondaparinux is widely used for treating deep vein thrombosis (DVT), pulmonary embolism (PE), and acute coronary syndrome (ACS). In 2024, the DVT segment accounted for 47.8% of the market, reflecting the growing prevalence of DVT cases worldwide. Older adults and individuals with chronic health conditions face higher risks of clot formation, making effective anticoagulation therapy essential. Fondaparinux remains a preferred treatment due to its reliable efficacy, predictable pharmacokinetics, and the advantage of not requiring routine blood monitoring, unlike certain traditional anticoagulants.

The U.S. fondaparinux market generated USD 244.3 million in 2024 and is projected to reach USD 433.9 million by 2034. Several factors contribute to this expansion, including a high volume of orthopedic procedures, an aging population, and a rising prevalence of critical illnesses that necessitate anticoagulation therapy. The increasing adoption of advanced treatment protocols and the demand for safer, more efficient anticoagulants continue to drive fondaparinux's market presence in the U.S., reinforcing its role in modern healthcare.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Base estimates and calculations

- 1.3.1 Base year calculation

- 1.3.2 Key trends for market estimation

- 1.4 Forecast model

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.5.2 Data mining sources

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising incidence of thromboembolic diseases

- 3.2.1.2 Increase in hip and knee transplant surgeries

- 3.2.1.3 Surge in aging population worldwide

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Side effects associated with fondaparinux

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.5 Pipeline analysis

- 3.6 Future market trends

- 3.7 Gap analysis

- 3.8 Porter’s analysis

- 3.9 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Strategy dashboard

Chapter 5 Market Estimates and Forecast, By Product Type, 2021 – 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Branded

- 5.3 Generic

Chapter 6 Market Estimates and Forecast, By Application, 2021 – 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Deep vein thrombosis

- 6.3 Pulmonary embolism

- 6.4 Acute coronary syndrome

- 6.5 Other applications

Chapter 7 Market Estimates and Forecast, By Distribution Channel, 2021 – 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Hospital pharmacies

- 7.3 Retail pharmacies

- 7.4 Online pharmacies

Chapter 8 Market Estimates and Forecast, By Region, 2021 – 2034 ($ Mn)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Netherlands

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.6 Middle East and Africa

- 8.6.1 Saudi Arabia

- 8.6.2 South Africa

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 Abbott Laboratories

- 9.2 Alchemia

- 9.3 Apotex

- 9.4 Aurobindo

- 9.5 Dr. Reddy’s Laboratories

- 9.6 Jiangsu Hengrui Medicine

- 9.7 Lupin Pharmaceuticals

- 9.8 Sandoz

- 9.9 ScinoPharm Taiwan

- 9.10 Viatris