ペットケア包装の市場機会、成長要因、業界動向分析、および2026年~2035年の予測

Pet Care Packaging Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035- 発行日

- ページ情報

- 英文 176 Pages

- 納期

- 2~3営業日

- 商品コード

- 2038707

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

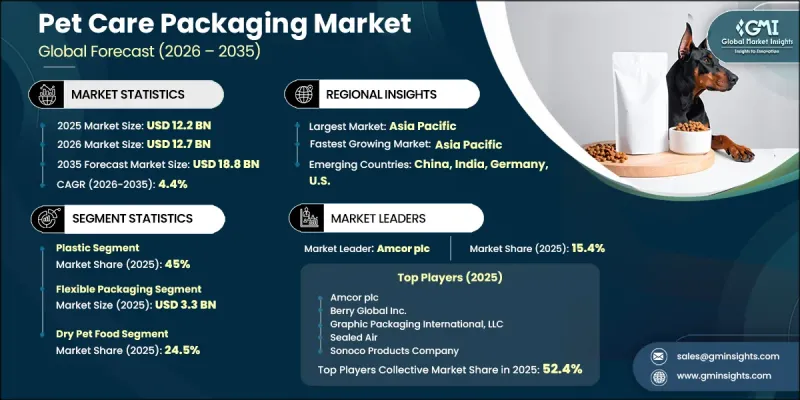

世界のペットケア包装市場は、2025年に122億米ドルと評価され、CAGR 4.4%で成長し、2035年までに188億米ドルに達すると推定されています。

この市場の成長は、世界のペット飼育頭数の増加、伴侶動物の栄養・ヘルスケア製品への支出拡大、そしてプレミアムペットフードの人気高まりによって支えられています。また、オンライン小売チャネルや消費者直販型ペットブランドの拡大も、先進パッケージングへの需要を後押ししています。さらに、扱いやすさ、再封可能、分量調整といった機能を備えた便利なパッケージソリューションに対する消費者の嗜好の高まりが、製品開発の動向を形成しています。同時に、持続可能性への懸念が、環境に優しくリサイクル可能な素材への移行を促進しており、デザインの革新と素材選定の両方に影響を与えています。ペットケア業界において、パッケージングは単なる保護層としてだけでなく、ブランディングや製品差別化のツールとしてもますます重視されるようになっており、世界市場におけるプレミアムなポジショニングと顧客エンゲージメントを支えています。

| 市場範囲 | |

|---|---|

| 開始年 | 2025年 |

| 予測期間 | 2026年~2035年 |

| 開始時の市場規模 | 122億米ドル |

| 予測額 | 188億米ドル |

| CAGR | 4.4% |

ペットケア包装市場は、ペットの飼育率の増加やペットの健康関連製品への支出拡大に牽引されており、これによりパッケージ食品やヘルスケア用品への需要が引き続き高まっています。再封可能なキャップ、耐久性の向上、使いやすい取り扱いなど、機能的な包装機能に対する消費者の嗜好の高まりが、市場の拡大をさらに後押ししています。また、持続可能性も大きな役割を果たしており、メーカーは環境に配慮した素材や革新的な包装デザインへと移行しています。これらの要因が相まって、業界全体でより効率的で機能的、かつ環境に配慮した包装ソリューションの開発が促進されています。

紙および板紙セグメントは、リサイクル可能かつ生分解性のパッケージソリューションに対する需要の高まりに支えられ、2025年から2035年にかけてCAGR 5.6%を記録すると予想されています。ペットフードメーカーや小売業者によるサステナビリティへの取り組みの強化は、ドライフードのパッケージ、ペット用おやつ、二次包装形式において繊維系素材の使用を促進しており、環境に優しい代替品への移行を後押ししています。

ドライペットフードセグメントは、その広範な消費、長い保存期間、およびペットオーナーからの強い支持に牽引され、2025年には24.5%のシェアを占めました。このカテゴリーでは、鮮度、栄養価、および製品の安定性を維持するために、高いバリア性と耐湿性を備えた包装が求められており、これが包装ソリューションに対する一貫した大規模な需要を生み出し続けています。

2025年、北米のペットケア包装市場は34.7%のシェアを占めました。同地域における市場の拡大は、高いペット飼育率と、プレミアムペットフードおよびケア製品への需要増加に支えられています。ペットの「人間化」に対する消費者の強い志向が、地域市場全体において、高品質で機能的かつ視覚的に魅力的な包装ソリューションへのニーズを牽引しています。

よくあるご質問

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- サプライヤーの情勢

- 利益率

- コスト構造

- 各段階における付加価値

- バリューチェーンに影響を与える要因

- ディスラプション

- 業界への影響要因

- 促進要因

- ペットの飼育頭数の増加とペットの「人間化」

- パッケージ化・加工ペットフードへの需要の高まり

- EコマースおよびD2C(消費者直販)ペットブランドの拡大

- 利便性と機能的なパッケージング機能への注目が高まっています

- 持続可能で環境に優しいパッケージングソリューションの採用拡大

- 業界の潜在的リスク&課題

- 持続可能かつ特殊な包装材料の高コスト

- 複雑な規制遵守および包装の標準化要件

- 市場機会

- ペットケア製品におけるスマートかつコネクテッドなパッケージングソリューションの導入

- ニッチなペット栄養分野におけるカスタマイズ型および小ロット包装の拡大

- 促進要因

- 成長可能性分析

- 規制情勢

- 北米

- 欧州

- アジア太平洋地域

- ラテンアメリカ

- 中東・アフリカ

- ポーター分析

- PESTEL分析

- 技術およびイノベーションの動向

- 現在の技術動向

- 新興技術

- 価格動向

- 地域別

- 製品別

- 価格戦略

- 新興ビジネスモデル

- コンプライアンス要件

- 特許および知的財産分析

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 地域別

- 北米

- 欧州

- アジア太平洋

- ラテンアメリカ

- 中東・アフリカ

- 市場集中度の分析

- 地域別

- 主要企業の競合ベンチマーキング

- 財務実績の比較

- 売上高

- 利益率

- 研究開発

- 製品ポートフォリオの比較

- 製品ラインの幅

- 技術

- イノベーション

- 地域展開の比較

- 世界展開の分析

- サービスネットワークのカバー範囲

- 地域別市場浸透率

- 競合ポジショニングマトリックス

- リーダー

- チャレンジャー

- フォロワー

- ニッチプレイヤー

- 戦略的展望マトリックス

- 財務実績の比較

- 主な発展

- 合併・買収

- パートナーシップおよび提携

- 技術的進歩

- 事業拡大および投資戦略

- デジタルトランスフォーメーションの取り組み

- 新興/スタートアップ競合企業の動向

第5章 市場推計・予測:素材タイプ別、2022年~2035年

- プラスチック

- 紙・板紙

- 金属

- 複合素材/ラミネート

第6章 市場推計・予測:包装タイプ別、2022年~2035年

- フレキシブル包装

- 硬質プラスチック容器

- 折りたたみ式カートン

- 硬質金属容器

- 段ボール箱

- チューブ

第7章 市場推計・予測:用途別、2022年~2035年

- ドライペットフード

- ウェットペットフード

- ペット用おやつ

- ペット用トイレ砂

- ペット用ヘルスケア・サプリメント

- ペットグルーミング用品

第8章 市場推計・予測:地域別、2022年~2035年

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- スペイン

- イタリア

- ロシア

- アジア太平洋

- 中国

- インド

- 日本

- オーストラリア

- 韓国

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- 南アフリカ

- サウジアラビア

- アラブ首長国連邦

第9章 企業プロファイル

- 世界の主要企業

- Amcor plc

- Berry Global Inc.

- Graphic Packaging International, LLC

- Sealed Air

- Sonoco Products Company

- 地域別主要企業

- 北米

- Plastek Group

- PPC Flex Company Inc.

- Printpack

- ProAmpac

- Silgan Holdings

- WestRock Company

- Winpak LTD.

- アジア太平洋地域

- ATID Packaging

- 欧州

- Constantia Flexibles

- Coveris

- DS Smith

- Huhtamaki

- Mondi

- NNZ Group BV

- Smurfit Kappa

- Trivium Packaging

- 北米

- 発行日

- 発行

- Global Market Insights Inc.

- ページ情報

- 英文 176 Pages

- 納期

- 2~3営業日