|

|

市場調査レポート

商品コード

1684776

小型トラックの市場機会、成長促進要因、産業動向分析、2025年~2034年予測Light Duty Truck Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

|

|||||||

カスタマイズ可能

|

|||||||

| 小型トラックの市場機会、成長促進要因、産業動向分析、2025年~2034年予測 |

|

出版日: 2025年01月08日

発行: Global Market Insights Inc.

ページ情報: 英文 180 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

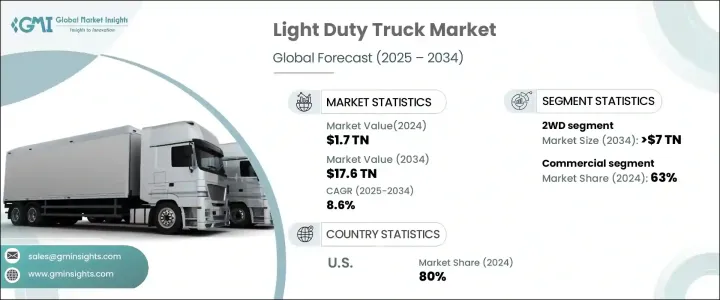

世界の小型トラック市場は2024年に1兆7,000億米ドルと評価され、2025年から2034年にかけて8.6%のCAGRで堅調な成長が見込まれています。

この目覚ましい成長はいくつかの要因に起因していますが、中でも最も注目すべきはeコマース業界の活況で、効率的なラストマイル配送ソリューションに対する需要が大幅に高まっています。オンラインショッピングが消費者行動を支配し続ける中、多用途で信頼性が高く、費用対効果の高い車両に対するニーズはかつてないほど高まっています。貨物容量、燃費効率、適応性を兼ね備えた小型トラックは、企業にも個人にも好まれる選択肢として浮上してきました。さらに、個人と商業の両方のニーズを満たすその能力は、燃費効率の高い技術の進歩と相まって、これらのトラックを環境意識の高い消費者にとって特に魅力的なものにしています。都市と農村の両方の環境における性能は、その魅力をさらに高め、企業が進化し続ける市場で競争力を維持するために必要な柔軟性を提供します。

市場は、2WD、4WD、AWDなど、駆動形態によって区分されます。このうち、2WDセグメントは2024年に市場シェアの45%を占め、2034年には7兆米ドルを生み出すと予測されています。2WD人気の高まりは、手頃な価格と性能の最適なバランスを提供する費用対効果と優れた燃費効率に起因しています。このため、能力を妥協することなく、実用的で価値志向の車を求める消費者や企業にとって好ましい選択肢となっています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024年 |

| 予測年 | 2025年~2034年 |

| 開始金額 | 1兆7,000億米ドル |

| 予測金額 | 17兆6,000億米ドル |

| CAGR | 8.6% |

用途別では、市場は商業部門と産業部門に分かれ、2024年の市場シェアは商業部門が63%と圧倒的です。小型トラックは、その手頃な価格、低いメンテナンス要件、より重い代替品と比べた燃費の良さから、商業用途で非常に好まれています。そのサイズと容量により、小口配送から大型でかさばる貨物輸送まで理想的な輸送が可能となり、企業は機敏で効率的であり続けることができます。

地域別では、米国の小型トラック市場は2024年に80%という驚異的なシェアを獲得しました。この成長の原動力は北米全域の都市化であり、都市は急速に拡大し、十分な貨物スペースを確保しながら混雑した都市部の道路を移動できる車両に対する需要が生まれています。企業が市街地内での機動性と実用性の両方を提供する信頼性の高い配送ソリューションを求める中、小型トラックは、商業業務に不可欠なソリューションを提供し、市場を独占し続ける構えです。

目次

第1章 調査手法と調査範囲

- 調査デザイン

- 調査アプローチ

- データ収集方法

- 基本推定と計算

- 基準年の算出

- 市場推計の主要動向

- 予測モデル

- 一次調査と検証

- 一次ソース

- データマイニングソース

- 市場範囲・定義

第2章 エグゼクティブサマリー

第3章 業界洞察

- 業界エコシステム分析

- 原材料プロバイダー

- 部品メーカー

- メーカー

- 技術プロバイダー

- 最終顧客

- サプライヤーの状況

- 利益率分析

- 技術革新の状況

- 特許分析

- 主要ニュース・イニシアチブ

- 規制状況

- コスト分析

- 影響要因

- 成長促進要因

- 迅速で便利な配送に対する需要の高まり

- 商品の輸送・流通ニーズの高まり

- トラック製造の進歩

- 建設・インフラ活動の増加

- 業界の潜在的リスク・課題

- 小型トラックへの高い初期投資

- 燃料費の上昇

- 成長促進要因

- 成長可能性分析

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業市場シェア分析

- 競合のポジショニングマトリックス

- 戦略展望マトリックス

第5章 市場推計・予測:ドライブ構成別、2021年~2034年

- 主要動向

- 2WD

- 4WD

- AWD

第6章 市場推計・予測:燃料別、2021年~2034年

- 主要動向

- ガソリン

- ディーゼル

- 電気

第7章 市場推計・予測:用途別、2021~2034年

- 主要動向

- 商業用

- 産業用

第8章 市場推計・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- 英国

- ドイツ

- フランス

- イタリア

- スペイン

- ロシア

- 北欧

- アジア太平洋

- 中国

- インド

- 日本

- オーストラリア

- 韓国

- 東南アジア

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- UAE

- 南アフリカ

- サウジアラビア

第9章 企業プロファイル

- Daimler

- Flat

- Ford

- Freightliner

- GM

- Hino

- Hyundai

- Isuzu

- Kenworth

- Mack Trucks

- Ram

- Renault

- Tata

- Toyota

- Volkswagen

The Global Light Duty Truck Market was valued at USD 1.7 trillion in 2024 and is expected to grow at a robust CAGR of 8.6% between 2025 and 2034. This impressive growth can be attributed to several factors, the most notable being the booming e-commerce industry, which has significantly heightened the demand for efficient last-mile delivery solutions. As online shopping continues to dominate consumer behavior, the need for versatile, reliable, and cost-effective vehicles has never been greater. Light-duty trucks, with their combination of cargo capacity, fuel efficiency, and adaptability, have emerged as the preferred choice for businesses and individuals alike. Furthermore, their ability to meet both personal and commercial needs, coupled with advancements in fuel-efficient technologies, makes these trucks especially appealing to environmentally conscious consumers. Their performance in both urban and rural settings further enhances their appeal, providing businesses with the flexibility they require to stay competitive in an ever-evolving market.

The market is segmented based on drive configuration, including 2WD, 4WD, and AWD. Among these, the 2WD segment accounted for 45% of the market share in 2024 and is projected to generate USD 7 trillion by 2034. The rise of 2WD's popularity can be credited to its cost-effectiveness and superior fuel efficiency, which provide an optimal balance of affordability and performance. This makes it a preferred option for consumers and businesses seeking practical, value-oriented vehicles without compromising on capability.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $1.7 Trillion |

| Forecast Value | $17.6 Trillion |

| CAGR | 8.6% |

In terms of application, the market is split into commercial and industrial segments, with the commercial sector commanding a dominant 63% market share in 2024. Light-duty trucks are highly favored in commercial applications due to their affordability, lower maintenance requirements, and better fuel economy compared to heavier alternatives. Their size and capacity make them ideal for transporting goods, from small deliveries to larger, bulkier shipments, ensuring businesses can remain agile and efficient.

Regionally, the U.S. market for light-duty trucks held an impressive 80% share in 2024. This growth is driven by urbanization across North America, where cities are rapidly expanding and creating a demand for vehicles that can navigate congested urban streets while providing ample cargo space. As businesses seek reliable delivery solutions that offer both mobility and practicality within city limits, light-duty trucks are poised to continue dominating the market, providing essential solutions for commercial operations.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.1.1 Research approach

- 1.1.2 Data collection methods

- 1.2 Base estimates & calculations

- 1.2.1 Base year calculation

- 1.2.2 Key trends for market estimation

- 1.3 Forecast model

- 1.4 Primary research and validation

- 1.4.1 Primary sources

- 1.4.2 Data mining sources

- 1.5 Market scope & definition

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Raw material providers

- 3.1.2 Component providers

- 3.1.3 Manufacturers

- 3.1.4 Technology providers

- 3.1.5 End customers

- 3.2 Supplier landscape

- 3.3 Profit margin analysis

- 3.4 Technology & innovation landscape

- 3.5 Patent analysis

- 3.6 Key news & initiatives

- 3.7 Regulatory landscape

- 3.8 Cost analysis

- 3.9 Impact forces

- 3.9.1 Growth drivers

- 3.9.1.1 Increasing demand for fast & convenient delivery

- 3.9.1.2 Rising need for transportation and distribution of goods

- 3.9.1.3 Growing advancements in truck manufacturing

- 3.9.1.4 Rising construction and infrastructure activities

- 3.9.2 Industry pitfalls & challenges

- 3.9.2.1 High initial investments in light-duty trucks

- 3.9.2.2 Rising fuel costs

- 3.9.1 Growth drivers

- 3.10 Growth potential analysis

- 3.11 Porter’s analysis

- 3.12 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Drive Configuration, 2021 - 2034 ($Bn, Units)

- 5.1 Key trends

- 5.2 2WD

- 5.3 4WD

- 5.4 AWD

Chapter 6 Market Estimates & Forecast, By Fuel, 2021 - 2034 ($Bn, Units)

- 6.1 Key trends

- 6.2 Gasoline

- 6.3 Diesel

- 6.4 Electric

Chapter 7 Market Estimates & Forecast, By Application, 2021 - 2034 ($Bn, Units)

- 7.1 Key trends

- 7.2 Commercial

- 7.3 Industrial

Chapter 8 Market Estimates & Forecast, By Region, 2021 - 2034 ($Bn, Units)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 UK

- 8.3.2 Germany

- 8.3.3 France

- 8.3.4 Italy

- 8.3.5 Spain

- 8.3.6 Russia

- 8.3.7 Nordics

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.4.6 Southeast Asia

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.6 MEA

- 8.6.1 UAE

- 8.6.2 South Africa

- 8.6.3 Saudi Arabia

Chapter 9 Company Profiles

- 9.1 Daimler

- 9.2 Flat

- 9.3 Ford

- 9.4 Freightliner

- 9.5 GM

- 9.6 Hino

- 9.7 Hyundai

- 9.8 Isuzu

- 9.9 Kenworth

- 9.10 Mack Trucks

- 9.11 Ram

- 9.12 Renault

- 9.13 Tata

- 9.14 Toyota

- 9.15 Volkswagen