|

市場調査レポート

商品コード

1913353

鉛蓄電池リサイクル市場の機会、成長促進要因、産業動向分析、2026年~2035年の予測Lead Acid Battery Recycling Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

カスタマイズ可能

|

|||||||

| 鉛蓄電池リサイクル市場の機会、成長促進要因、産業動向分析、2026年~2035年の予測 |

|

出版日: 2025年12月18日

発行: Global Market Insights Inc.

ページ情報: 英文 112 Pages

納期: 2~3営業日

|

概要

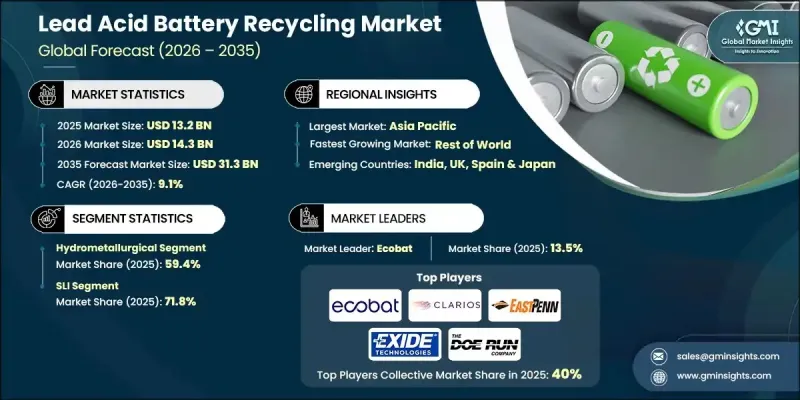

世界の鉛蓄電池リサイクル市場は、2025年に132億米ドルと評価され、2035年までにCAGR 9.1%で成長し、313億米ドルに達すると予測されています。

電気化の動向の加速と、輸送、エネルギー貯蔵、産業システムにおける鉛蓄電池の使用増加がこの成長を牽引しています。鉛蓄電池のリサイクルとは、使用済み電池を体系的に回収・処理し、鉛、プラスチック部品、電解液などの再利用可能な材料を回収するプロセスです。この取り組みは資源効率の向上、環境リスクの低減、そして世界の持続可能性目標との整合性を支えます。リサイクルプロセスは、汚染の削減、安全な廃棄物処理の確保、そして進化するコンプライアンス要件への対応において重要な役割を果たしています。電池消費量の増加と環境監視の強化が相まって、世界のリサイクル活動の加速につながっています。政府や規制機関は体系的な電池廃棄物管理手法を強化し、長期的な市場成長を支える枠組みを構築するとともに、複数の最終用途産業における循環型経済の導入を促進しています。

| 市場範囲 | |

|---|---|

| 開始年 | 2025年 |

| 予測年度 | 2026-2035 |

| 開始時価値 | 132億米ドル |

| 予測金額 | 313億米ドル |

| CAGR | 9.1% |

自動車、電源バックアップシステム、産業インフラにおける鉛蓄電池の導入増加に伴い、リサイクル量が大幅に増加しております。エネルギー貯蔵需要の拡大に伴い、リサイクルは材料サプライチェーンの重要な要素となり、新規採掘資源への依存度低減に貢献しております。環境保護と材料回収に焦点を当てた規制枠組みは、メーカーやリサイクル業者に対し、責任ある使用済み電池管理手法の推進を継続的に促しております。

湿式冶金リサイクル分野は2025年に59.4%のシェアを占め、2035年までCAGR9.2%で拡大が見込まれます。この手法は、他のリサイクルプロセスと比較して排出量が少なく、廃棄物発生量が抑えられ、エネルギー要求が低いことから、選択されるケースが増加しています。環境規制への適合を支援しながら高純度の金属回収を実現する能力により、持続可能な運営に注力するリサイクル事業者にとって重要な技術選択肢となっています。

SLIセグメントは2025年に71.8%のシェアを占め、2026年から2035年にかけてCAGR 9%で成長すると予想されます。自動車セクターからの継続的な需要と安定した交換サイクルが、一貫したリサイクル量を支えています。バッテリー廃棄に関する環境規制の強化は、この応用分野における責任ある回収手法と材料再利用をさらに促進しています。

北米鉛蓄電池リサイクル市場は92.3%のシェアを占め、2035年までに43億米ドル規模に成長すると予測されています。厳格な環境規制の施行、エネルギー貯蔵需要の増加、鉛曝露に伴う健康リスク低減への注目の高まりが、先進的なリサイクル手法と運用効率の向上を支えています。

よくあるご質問

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- 業界のエコシステム

- 原材料の入手可能性と調達分析

- 製造能力評価

- サプライチェーンの回復力とリスク要因

- 流通ネットワーク分析

- 規制情勢

- 業界への影響要因

- 促進要因

- 業界の潜在的リスク&課題

- 成長可能性分析

- コスト構造分析

- ポーター分析

- PESTEL分析

- 新たな機会と動向

- デジタル化とIoT統合

- 新興市場への進出

- 投資分析と将来展望

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析:地域別

- 北米

- 欧州

- アジア太平洋地域

- 世界のその他の地域

- 戦略的ダッシュボード

- 戦略的取り組み

- 企業ベンチマーキング

- イノベーションと技術動向

第5章 市場規模・予測:プロセス別、2022-2035

- 火法冶金

- 湿式冶金

- 物理的/機械的

第6章 市場規模・予測:用途別、2022-2035

- SLI

- 据置型

- その他

第7章 市場規模・予測:地域別、2022-2035

- 北米

- 米国

- カナダ

- 欧州

- 英国

- スペイン

- ドイツ

- フランス

- アジア太平洋地域

- 中国

- 韓国

- 日本

- インド

- 世界のその他の地域

第8章 企業プロファイル

- Amara Raja

- Aqua Metals

- Battery Recyclers of America

- BPL Nigeria Limited

- Cirba Solutions

- Clarios

- Doe Run Company

- East Penn Manufacturing Company

- Ecobat

- EnerSys

- Engitec Technologies

- Exide Technologies

- Glencore

- GME Recycling

- Gopher Resource LLC

- Gravita India

- Interstate Batteries