|

市場調査レポート

商品コード

1636236

SLI用鉛蓄電池-市場シェア分析、産業動向、成長予測(2025~2030年)Lead Acid Battery For SLI Applications - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| SLI用鉛蓄電池-市場シェア分析、産業動向、成長予測(2025~2030年) |

|

出版日: 2025年01月05日

発行: Mordor Intelligence

ページ情報: 英文 124 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

概要

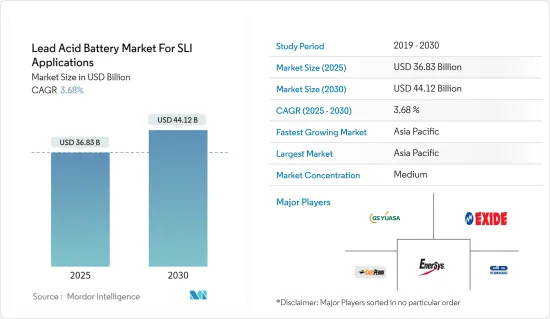

SLI用鉛蓄電池市場は、予測期間(2025~2030年)にCAGR 3.68%で、2025年の368億3,000万米ドルから2030年には441億2,000万米ドルに成長すると予測されます。

主要ハイライト

- 中期的には、自動車産業からの需要増加や鉛蓄電池リサイクル施設の増加といった要因が、予測期間中の市場を牽引するとみられます。

- 一方、代替技術との競合が予測期間中の市場成長を阻害するとみられます。

- 技術の進歩は今後数年間、市場に大きなビジネス機会をもたらすと予想されます。

- アジア太平洋は、同地域の様々な国で電気自動車の普及率が高まっているため、市場を独占すると推定されます。

鉛蓄電池市場の動向

自動車産業における需要の高まり

- 自動車産業は、北米、欧州、アジア太平洋を中心とした様々な地域における主要産業の一つです。これらの地域では都市化が進んでおり、自動車需要を牽引しているため、SLI電池の世界最大市場の一つとなっています。

- 鉛蓄電池は、世界中の自動車やトラックなど、従来の内燃機関自動車に搭載されるすべてのSLI電池用途に選択されている技術です。鉛蓄電池は、従来の自動車におけるSLI用途で最も経済的に実行可能な量産技術です。自動車用SLI電池の90%以上が鉛蓄電池ベースであり、産業用据置型と原動機用途の90%以上(蓄電容量ベース)が鉛蓄電池ベースです。

- 2023年の乗用車生産台数は中国が約2,610万台で世界首位。第2位の日本は約780万台を生産しました。これらの国々には、SLI電池の主要消費者であるGS Yuasa CorporationやCamel Groupなど、世界最大級の自動車メーカーもあります。

- 世界中で、特に開発途上地域で自動車保有台数が拡大するにつれて、従来の内燃機関(ICE)車に電力を供給するためのSLI用電池のニーズも並行して高まっています。

- 従来の内燃エンジン車の市場は今後20年から25年の間に縮小すると予想されるが、自動車の代替技術では、車内のさまざまな電子機器や安全機能に電力を供給するためにSLIタイプの鉛蓄電池が引き続き使用されると予想されます。先進的な鉛ベースの電池(吸収ガラスマットまたは強化浸水型電池)は、主要なマイクロハイブリッド車の燃費を改善するためのスタート-ストップ機能を記載しています。スタートストップシステムでは、内燃エンジン(ICE)がブレーキングや休息時に自動的に停止し、燃料消費を最大5~10%削減します。

- OICA(Organisation Internationale des Constructeurs d'Automobiles)によると、乗用車の世界販売台数は2023年に6,527万台に達します。商用車の販売台数は2023年に2,745万台に達します。これは、SLI(始動、照明、点火)用途の鉛蓄電池を含む自動車部品の需要が旺盛であることを示しています。

- これらの自動車は、エンジン始動や車載電子機器への電力供給といった重要な機能をSLI電池に依存しているため、販売台数が引き続き多いことが鉛蓄電池の需要を牽引しています。このような自動車の生産と販売の急増は、世界のSLI用鉛蓄電池市場を維持し、場合によっては押し上げると予想されます。

中国が市場を独占する見込み

- 中国の鉛蓄電池市場は、特に始動・照明・点火(SLI)用途で大きな成長が見込まれます。この市場拡大の主因は、パンデミック後の回復と拡大を続ける堅調な自動車産業です。

- 自動車産業は信頼性が高く、費用対効果の高い電池を求めているため、鉛蓄電池はSLI用途に適しています。これらの電池は、自動車の始動モーター、ライト、点火システムの電源として不可欠であり、高性能と長寿命を保証します。

- OICA(Organisation Internationale des Constructeurs d'Automobiles)によると、中国の乗用車販売台数は2023年に2,606万台に達します。商用車の販売台数は2023年に403万台に達しました。このため、SLI用途の鉛蓄電池を含む自動車部品の需要が生まれました。

- リサイクルプロセスの改善や電池性能の向上など、鉛蓄電池技術の革新により、鉛蓄電池の競合は高まっています。リチウムイオン電池の人気が高まっているにもかかわらず、鉛蓄電池はその確立されたサプライチェーンと費用対効果により、依然として関連性があります。

- 自動車用電池のアフターマーケットは拡大しており、消費者は既存の電池を交換したりアップグレードしたりすることが増えています。この動向は、SLIカテゴリの需要を維持し、市場の持続的成長を確保する上で極めて重要です。Johnson Controls International PLC、Exide Technologies Inc.、Amara Raja Batteries Ltd.などの企業が市場を主要リードしており、競合を維持するために戦略的拡大と技術革新に注力しています。

- 全体として、中国の鉛蓄電池市場は成長軌道を維持すると予想されます。継続的な進歩と自動車産業からの安定した需要、電気自動車の普及と先進的エネルギー貯蔵ソリューションの必要性の高まりが、この成長を促進すると予想されます。

SLI用鉛蓄電池産業概要

SLI用鉛蓄電池市場はセグメント化されています。主要参入企業には、GS Yuasa Corporation、C&D Technologies Inc.、East Penn Manufacturing Co. Inc.、EnerSys、Exide Technologiesなどがあります(順不同)。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査範囲

- 市場の定義

- 調査の前提

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場概要

- イントロダクション

- 2029年までの市場規模と需要予測(単位:10億米ドル)

- 最近の動向と開発

- 政府の規制と施策

- 市場力学

- 促進要因

- 自動車産業における需要拡大

- 鉛蓄電池のリサイクル増加

- 抑制要因

- 代替技術との競合

- 促進要因

- サプライチェーン分析

- ポーターのファイブフォース分析

- 供給企業の交渉力

- 消費者の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係

第5章 市場セグメンテーション

- 技術別

- 浸水型

- VRLA(バルブ制御式鉛蓄電池)

- 地域別

- 北米

- 米国

- カナダ

- その他の北米

- 欧州

- ドイツ

- フランス

- スペイン

- ノルディック

- トルコ

- ロシア

- その他の欧州

- アジア太平洋

- 中国

- インド

- 日本

- 韓国

- マレーシア

- タイ

- インドネシア

- ベトナム

- その他のアジア太平洋

- 南米

- ブラジル

- アルゼンチン

- コロンビア

- その他の南米

- 中東・アフリカ

- サウジアラビア

- アラブ首長国連邦

- 南アフリカ

- エジプト

- ナイジェリア

- カタール

- その他の中東・アフリカ

- 北米

第6章 競合情勢

- M&A、合弁事業、提携、協定

- 主要企業の戦略

- 企業プロファイル

- Johnson Controls International PLC

- Exide Technologies

- EnerSys

- East Penn Manufacturing Co. Inc.

- GS Yuasa Corporation

- Leoch International Technology Limited

- C&D Technologies Inc.

- NorthStar Battery Company LLC

- Camel Group Co. Ltd

- FIAMM Energy Technology SpA

- 市場ランキング/シェア分析

第7章 市場機会と今後の動向

- 技術の進歩

目次

Product Code: 50003504

The Lead Acid Battery Market For SLI Applications Industry is expected to grow from USD 36.83 billion in 2025 to USD 44.12 billion by 2030, at a CAGR of 3.68% during the forecast period (2025-2030).

Key Highlights

- Over the medium term, factors such as the growing demand from the automotive industry and rising lead-acid battery recycling facilities are expected to drive the market during the forecast period.

- On the other hand, competition from alternative technologies is likely to hinder market growth during the forecast period.

- Nevertheless, technological advancements are expected to provide significant opportunities for the market in the coming years.

- Asia-Pacific is estimated to dominate the market due to the increasing adoption rate of electric vehicles across various countries in the region.

Lead Acid Battery Market Trends

Growing Demand in the Automotive Industry

- Automotive is one of the major industries in various regions, particularly in North America, Europe, and Asia-Pacific. Growing urbanization in these regions is driving the demand for automobiles, thus making it one of the largest markets for SLI batteries globally.

- A lead-acid battery is the technology of choice for all SLI battery applications in conventional combustion engine vehicles, such as cars and trucks, worldwide. Lead-acid batteries are the most economically viable mass-market technology for SLI applications in traditional vehicles. Over 90% of automotive SLI batteries are lead-acid based, and over 90% (by storage capacity) of industrial stationary and motive applications.

- In 2023, China led the world in passenger car production, with approximately 26.1 million units manufactured. Japan, the second-highest producer, produced around 7.8 million units. These countries are also home to some of the world's largest automobile manufacturers, such as GS Yuasa Corporation and Camel Group Co. Ltd, the major SLI battery consumers.

- With expanding vehicle ownership worldwide, especially in developing regions, there is a parallel rise in the need for SLI batteries to power traditional internal combustion engine (ICE) vehicles.

- Although the market for conventional internal combustion engine vehicles is expected to decline over the next 20 to 25 years, replacement car technologies are expected to continue using SLI-type lead-acid batteries to power various electronics and safety features within the vehicle. Advanced lead-based batteries (absorbent glass mat or enhanced flooded batteries) provide start-stop functionality to improve fuel efficiency in major micro-hybrid vehicles. In start-stop systems, the internal combustion engine (ICE) automatically shuts down under braking and rest, reducing fuel consumption by up to 5-10%.

- According to the OICA (Organisation Internationale des Constructeurs d'Automobiles), the global vehicle sales for passenger cars reached 65.27 million in 2023. The vehicle sales for commercial vehicles reached 27.45 million in 2023. This indicates a robust demand for automotive components, including lead-acid batteries for SLI (starting, lighting, and ignition) applications.

- As these vehicles rely on SLI batteries for essential functions like starting the engine and powering onboard electronics, the continued high sales volumes drive the demand for lead-acid batteries. This vehicle production and sales surge is expected to sustain and possibly boost the global lead-acid battery market for SLI applications.

China is Expected to Dominate the Market

- The lead-acid battery market in China, especially for starting, lighting, and ignition (SLI) applications, is set to witness significant growth. This expansion is primarily driven by the robust automotive industry, which continues to recover and expand post-pandemic.

- The automotive industry's demand for reliable, cost-effective batteries makes lead-acid batteries a preferred choice for SLI applications. These batteries are integral to powering start motors, lights, and ignition systems in vehicles, ensuring high performance and longevity.

- According to OICA (Organisation Internationale des Constructeurs d'Automobiles), China's vehicle sales for passenger cars reached 26.06 million in 2023. The sales for commercial vehicles reached 4.03 million in 2023. This created a demand for automotive components, including lead-acid batteries for SLI applications.

- Innovations in lead-acid battery technology, such as improved recycling processes and enhanced battery performance, have made these batteries more competitive. Despite the growing popularity of lithium-ion batteries, lead-acid batteries remain relevant due to their established supply chain and cost-effectiveness.

- The aftermarket for automotive batteries is growing, with consumers increasingly replacing and upgrading their existing batteries. This trend is critical for maintaining demand in the SLI category and ensuring sustained market growth. Companies like Johnson Controls International PLC, Exide Technologies Inc., and Amara Raja Batteries Ltd are leading the market, focusing on strategic expansions and technological innovations to retain their competitive edge.

- Overall, the lead-acid battery market in China is expected to maintain its growth trajectory. Continuous advancements and steady demand from the automotive industry, along with the increasing adoption of electric vehicles and the need for advanced energy storage solutions, are expected to drive this growth.

Lead Acid Battery Industry Overview

The lead acid battery market for SLI applications is fragmented. Some of the major players include (not in particular order) GS Yuasa Corporation, C&D Technologies Inc., East Penn Manufacturing Co. Inc., EnerSys, and Exide Technologies.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Scope of Study

- 1.2 Market Definition

- 1.3 Study Assumption

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET OVERVIEW

- 4.1 Introduction

- 4.2 Market Size and Demand Forecast in USD billion, till 2029

- 4.3 Recent Trends and Developments

- 4.4 Government Policies and Regulations

- 4.5 Market Dynamics

- 4.5.1 Drivers

- 4.5.1.1 Growing Demand in the Automotive Industry

- 4.5.1.2 Increasing Lead-acid Battery Recycling

- 4.5.2 Restraints

- 4.5.2.1 Competition from Alternative Technologies

- 4.5.1 Drivers

- 4.6 Supply Chain Analysis

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Consumers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes Products and Services

- 4.7.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 By Technology

- 5.1.1 Flooded

- 5.1.2 VRLA (Valve Regulated Lead-acid)

- 5.2 By Geography

- 5.2.1 North America

- 5.2.1.1 United States

- 5.2.1.2 Canada

- 5.2.1.3 Rest of North America

- 5.2.2 Europe

- 5.2.2.1 Germany

- 5.2.2.2 France

- 5.2.2.3 Spain

- 5.2.2.4 NORDIC

- 5.2.2.5 Turkey

- 5.2.2.6 Russia

- 5.2.2.7 Rest of Europe

- 5.2.3 Asia-Pacific

- 5.2.3.1 China

- 5.2.3.2 India

- 5.2.3.3 Japan

- 5.2.3.4 South Korea

- 5.2.3.5 Malaysia

- 5.2.3.6 Thailand

- 5.2.3.7 Indonesia

- 5.2.3.8 Vietnam

- 5.2.3.9 Rest of Asia-Pacific

- 5.2.4 South America

- 5.2.4.1 Brazil

- 5.2.4.2 Argentina

- 5.2.4.3 Colombia

- 5.2.4.4 Rest of South America

- 5.2.5 Middle East and Africa

- 5.2.5.1 Saudi Arabia

- 5.2.5.2 United Arab Emirates

- 5.2.5.3 South Africa

- 5.2.5.4 Egypt

- 5.2.5.5 Nigeria

- 5.2.5.6 Qatar

- 5.2.5.7 Rest of Middle East and Africa

- 5.2.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Strategies Adopted by Leading Players

- 6.3 Company Profiles

- 6.3.1 Johnson Controls International PLC

- 6.3.2 Exide Technologies

- 6.3.3 EnerSys

- 6.3.4 East Penn Manufacturing Co. Inc.

- 6.3.5 GS Yuasa Corporation

- 6.3.6 Leoch International Technology Limited

- 6.3.7 C&D Technologies Inc.

- 6.3.8 NorthStar Battery Company LLC

- 6.3.9 Camel Group Co. Ltd

- 6.3.10 FIAMM Energy Technology SpA

- 6.4 Market Ranking/Share Analysis

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Technological Advancements