|

市場調査レポート

商品コード

1635459

欧州の鉛蓄電池:市場シェア分析、産業動向・統計、成長予測(2025~2030年)Europe Lead-acid Battery - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 欧州の鉛蓄電池:市場シェア分析、産業動向・統計、成長予測(2025~2030年) |

|

出版日: 2025年01月05日

発行: Mordor Intelligence

ページ情報: 英文 110 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

概要

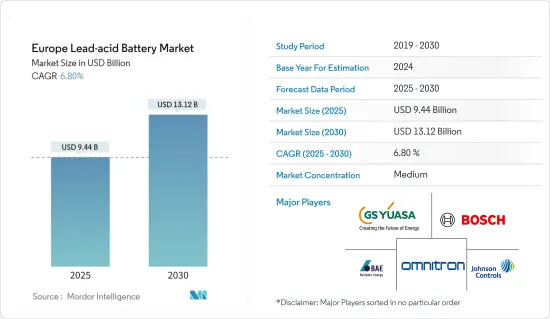

欧州の鉛蓄電池の市場規模は2025年に94億4,000万米ドルと推定され、2030年には131億2,000万米ドルに達すると予測され、予測期間(2025-2030年)のCAGRは6.8%です。

主なハイライト

- 中期的には、自動車セクターの成長やバッテリーエネルギー貯蔵システム(BESS)の採用といった要因が、予測期間中の欧州の鉛蓄電池市場を牽引すると予想されます。

- 一方、リチウムイオン電池の採用増加や電気自動車販売の増加は、今後数年間の鉛蓄電池市場の成長を抑制する可能性が高いです。

- とはいえ、オフグリッド太陽光発電設備投資の増加は、欧州の鉛蓄電池市場に大きなビジネスチャンスをもたらすと推定されます。

- ドイツは自動車メーカーのプレゼンスが高いため、欧州の鉛蓄電池市場を独占する可能性が高いです。

欧州の鉛蓄電池の市場動向

市場を独占するSLIバッテリーセグメント

- 始動・照明・点火(SLI)バッテリーは、過去100年間ほとんどすべての自動車に搭載されてきました。一般に、SLIバッテリーは、自動車のエンジン始動や軽い電気負荷の実行など、短時間の電力供給用に使用されます。

- SLIバッテリーは自動車用に設計されているため、常に自動車の充電システムと一緒に搭載されており、自動車が使用されているときは常にバッテリーに充電と放電の連続サイクルがあることになります。12ボルト・バッテリーは50年以上にわたって最も一般的に使用されてきたが、その平均電圧は14ボルトに近いです。

- また、電気通信業界は、電話やインターネット・サービスのトランスミッションのために、主に携帯電話タワーやフィールド設備の精巧なネットワークに依存しています。効率的な運用のために、これらのタワーや現場施設は、一定で信頼性の高い電力供給を必要とします。通常、電力網からの電力は、有線ネットワークでは-48ボルト、無線ネットワークでは+24ボルトの直流(DC)電力に変換されます。電気通信業界で使用されるバッテリーには、VRLA、NiCd、Li-ionなどがあります。

- ここ数年、SLIバッテリーは、欧州地域の自動車セクターのOEMやアフターマーケットからの需要が伸びているため、大きな需要があります。これらのバッテリーは主に、高性能、長寿命、コスト効率を確保しながら、始動モーター、照明、点火システム、その他の内燃機関の電源として利用されています。

- さらに、2022年には、ドイツ、フランス、英国が乗用車販売の主要国です。ドイツの乗用車販売台数は約265万台、フランスは約160万台、英国は約160万台です。

- また、EU全体で2022年に新車販売された乗用車は約930万台で、前年より4.6%減少しました。しかし、古い自動車の古いSLIバッテリーの交換が市場を牽引すると予想されます。

- 以上のことから、SLI電池部門は予測期間中、欧州の鉛蓄電池市場を独占すると予想されます。

市場を独占するドイツ

- ドイツは世界最大の乗用車・商用車製造国の一つです。数十年にわたり、自動車産業はドイツ経済の主要部門です。

- さらに、すべての主要自動車メーカーがドイツに進出していることから、ドイツは自動車産業のイノベーション・ハブとして世界的に認知されています。2022年、ドイツは欧州第一の自動車市場となり、製造される乗用車の約26%、新車登録台数の約20%を占める。

- また、2022年6月、ドイツは、EUが2035年までに同地域でICE車の新車を禁止することに反対する声を上げました。ICE車は、フォルクスワーゲン、BMW、メルセデスといったドイツの大手企業が製造する自動車ストックのかなりの部分を占めています。さらに、ドイツの乗用車販売台数は2022年に約265万台に達しました。

- ドイツは世界でも高度に発展した市場と考えられており、欧州連合(EU)の金融大国でもあります。そのため、データセンターの数も多く、2023年末現在、国内には522以上のデータセンターが稼動しています。さらに、自動化と5Gネットワークの開発により、データセンターの需要はドイツにあります。

- ドイツでは、自動車、データセンター、通信産業への投資の増加により、鉛蓄電池の需要が高まっています。リチウムイオン電池のような代替品も存在するが、鉛蓄電池の需要はこれらすべての産業でまだ多いです。鉛蓄電池は長寿命で安全性が高く、長期的に見ても性能が良いため、データセンター、自動車、通信業界では第一の選択肢となっています。

- このように、ドイツにおける自動車およびデータセンター産業におけるこれらすべての開発は、予測期間中、鉛蓄電池市場を牽引すると思われます。

欧州の鉛蓄電池産業の概要

欧州の鉛蓄電池市場は半断片化しています。同市場の主要企業(順不同)には、BAE Batterien GmbH、Exide Technologies Inc.、GS Yuasa Corporation、Johnson Controls International PLC、Omnitron Griese GmbHなどがあります。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査範囲

- 市場の定義

- 調査の前提

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場概要

- イントロダクション

- 2029年までの市場規模および需要予測(単位:米ドル)

- 最近の動向と開発

- 政府の規制と政策

- 市場力学

- 促進要因

- 自動車販売の増加

- 電池エネルギー貯蔵システム(BESS)の採用拡大

- 抑制要因

- リチウムイオン電池重視の高まり

- 促進要因

- サプライチェーン分析

- ポーターのファイブフォース分析

- 供給企業の交渉力

- 消費者の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係の強さ

第5章 市場セグメンテーション

- 用途別

- SLI(始動、点灯、点火)用電池

- 据置型電池(電気通信、UPS、エネルギー貯蔵システム(ESS)など)

- ポータブルバッテリー(家電製品など)

- その他の用途

- 技術別

- 浸水型

- VRLA(バルブ制御鉛蓄電池)

- 地域別

- ドイツ

- 英国

- フランス

- スペイン

- イタリア

- ノルディック

- トルコ

- ロシア

- その他欧州

第6章 競合情勢

- M&A、合弁事業、提携、協定

- 主要企業の戦略

- 企業プロファイル

- Johnson Controls International PLC

- Exide Technologies Inc.

- GS Yuasa Corporation

- Robert Bosch GmbH

- Omnitron Griese GmbH

- BAE Batterien GmbH

- Amara Raja Batteries Ltd

- Leoch International Technology Limited

- Panasonic Corporation

- Market Ranking/Share Analysis

第7章 市場機会と今後の動向

- オフグリッドソーラー設置投資の増加

目次

Product Code: 91997

The Europe Lead-acid Battery Market size is estimated at USD 9.44 billion in 2025, and is expected to reach USD 13.12 billion by 2030, at a CAGR of 6.8% during the forecast period (2025-2030).

Key Highlights

- Over the medium term, factors such as the growing automotive sector and adoption of battery energy storage systems (BESS) are expected to drive the lead-acid battery market in Europe during the forecast period.

- On the other note, rising adoption of lithium-ion batteries and increasing electric vehicle sales are likely to restrain the growth of the lead-acid battery market over the coming years.

- Nevertheless, increased off-grid solar installation investment is estimated to provide a significant opportunity for the lead acid market in Europe.

- Germany is likely to dominate the lead acid battery market in Europe due to the higher presence of automobile manufacturers in the country.

Europe Lead-acid Battery Market Trends

SLI Battery Segment to Dominate the Market

- Starting, lighting, and ignition (SLI) batteries have been in almost every car for the past 100 years. Generally, SLI batteries are used for short power bursts, such as starting a car engine or running light electrical loads.

- SLI batteries are designed for automobiles and, therefore, are always installed with the vehicle's charging system, which means that there is a continuous cycle of charge and discharge in the battery whenever the vehicle is in use. The 12-volt batteries have been the most commonly used for more than 50 years; however, their average voltage is close to 14-volt.

- Also, the telecom industry is primarily dependent on an elaborate network of mobile phone towers and field facilities for the transmission of phone calls and internet services. For their efficient operations, these towers and field facilities require a constant and highly reliable supply of electric power, usually from the electrical grid converted to direct current (DC) power at -48 volts for wired networks and +24 volts for wireless networks. The batteries used in the telecom industry include VRLA, NiCd, and Li-ion, among others.

- In the last couple of years, the SLI batteries witnessed significant demand due to the growing demand from OEMs and aftermarkets from the automotive sector in the European region. These batteries primarily mostly utilized power start motors, lights, ignition systems, or other internal combustion engines while ensuring high performance, long life, and cost-efficiency.

- Moreover, in 2022, Germany, France and United kingdom are the leading countries in terms of sales of passengers cars. Germany's passenger car sales amounted to around 2.65 million units. in fracne it was around 1.6 million and United kingdom is was around 1.6 million.

- Also, around 9.3 million new passenger cars were sold across the European Union in 2022, which is 4.6% less than the previous year. However, the replacement of the old SLI batteries in old vehicles is anticipated to drive the the market.

- Owing to the above points, SLI Battery Segement is expected to dominate Europe lead-acid battery market during the forecast period.

Germany to Dominate the Market

- Germany is one of the world's largest manufacturing countries for passenger and commercial vehicles. For several decades the automobile industry has been a key sector in the German economy.

- Moreover, Germany has been recognized worldwide as an Innovation hub for the automotive industry, as all major automobile manufacturers have a presence in the country. In 2022, Germany is Europe's number one automotive market, accounting for around 26% of all passenger cars manufactured and approximately 20% of all new car registrations.

- Also, In June 2022, Germany, raised its voice against the EU ban on new ICE vehicles in the region by 2035. The ICE vehicles form a considerable part of the vehicle stock manufactured by major players in Germany like Volkswagen, BMW, and Mercedes. Moreover, Germany's passenger car sales amounted to around 2.65 million units in 2022.

- Germany is considered a highly developed market in the world, and it is the financial powerhouse of the European Union. This, resulting a higher number of data centres, and as of the end of 2023, there were more than 522 active data centres in the country. Furthermore, due to automation and development meant of the 5G network, the demand for the data centre is in Germany.

- The demand for lead acid batteries is rising in Germany due to increased investment in the automobile, data centre and telecommunication industry. Though there is the presence of substitutes, such as lithium-ion batteries, there is still more demand for lead acid batteries from all these industries. The lead acid battery has a long life, safety and good performance in the long run, which makes them the first choices in the data centre, automobile and telecommunication industry.

- Thus all these development in Germany in the automobile and data centre industry is likely to drive the lead acid market during the forecast period.

Europe Lead-acid Battery Industry Overview

The Europe lead-acid battery market is semi fragmented. Some of the key players (in no particular order) in the market include BAE Batterien GmbH, Exide Technologies Inc., GS Yuasa Corporation, Johnson Controls International PLC, Omnitron Griese GmbH, etc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Scope of Study

- 1.2 Market Definition

- 1.3 Study Assumptions

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET OVERVIEW

- 4.1 Introduction

- 4.2 Market Size and Demand Forecast in USD, till 2029

- 4.3 Recent Trends and Developments

- 4.4 Government Policies and Regulations

- 4.5 Market Dynamics

- 4.5.1 Drivers

- 4.5.1.1 Increasing Sales of Automobiles

- 4.5.1.2 Growing Adoption of Battery Energy Storage Systems (BESS)

- 4.5.2 Restraints

- 4.5.2.1 Rising Emphasis on Lithium-Ion Batteries

- 4.5.1 Drivers

- 4.6 Supply Chain Analysis

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Consumers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitute Products and Services

- 4.7.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 Application

- 5.1.1 SLI (Starting, Lighting, Ignition) Batteries

- 5.1.2 Stationary Batteries (Telecom, UPS, Energy Storage Systems (ESS), etc.)

- 5.1.3 Portable Batteries (Consumer Electronics, etc.)

- 5.1.4 Other Applications

- 5.2 Technology

- 5.2.1 Flooded

- 5.2.2 VRLA (Valve Regulated Lead-acid)

- 5.3 Geography

- 5.3.1 Germany

- 5.3.2 United Kingdom

- 5.3.3 France

- 5.3.4 Spain

- 5.3.5 Italy

- 5.3.6 NORDIC

- 5.3.7 Turkey

- 5.3.8 Russia

- 5.3.9 Rest of Europe

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers & Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Strategies Adopted by Leading Players

- 6.3 Company Profiles

- 6.3.1 Johnson Controls International PLC

- 6.3.2 Exide Technologies Inc.

- 6.3.3 GS Yuasa Corporation

- 6.3.4 Robert Bosch GmbH

- 6.3.5 Omnitron Griese GmbH

- 6.3.6 BAE Batterien GmbH

- 6.3.7 Amara Raja Batteries Ltd

- 6.3.8 Leoch International Technology Limited

- 6.3.9 Panasonic Corporation

- 6.4 Market Ranking/Share Analysis

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Increased Off-Grid Solar Installation Investment