|

市場調査レポート

商品コード

1684572

PCRプラスチック包装の市場機会、成長促進要因、産業動向分析、2025年~2034年予測PCR Plastic Packaging Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| PCRプラスチック包装の市場機会、成長促進要因、産業動向分析、2025年~2034年予測 |

|

出版日: 2025年01月06日

発行: Global Market Insights Inc.

ページ情報: 英文 250 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

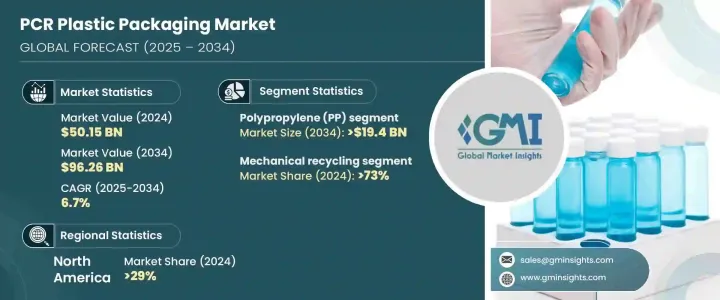

世界のPCRプラスチック包装市場は、2024年に501億5,000万米ドルと評価され、2025年から2034年にかけてCAGR6.7%で成長すると予測されています。

この市場は、持続可能性がビジネスの中心的な焦点となり、未使用プラスチックの代替品への需要が増加し続けているため、大きな成長を目の当たりにしています。様々な業界の企業が、環境目標に沿い、環境に優しい製品に対する消費者の期待に応えるため、PCRプラスチックの採用を増やしています。循環型経済へのシフトとプラスチック廃棄物管理に関する規制強化が、市場の拡大をさらに後押ししています。

市場はプラスチックタイプによって、ポリエチレンテレフタレート(PET)、ポリエチレン(PE)、ポリスチレン(PS)、ポリ塩化ビニル(PVC)、ポリプロピレン(PP)、バイオベースプラスチックに区分されます。なかでもポリプロピレン(PP)の成長が最も速く、CAGR8.4%で成長し、2034年には194億米ドルに達すると予測されています。PPは、その汎用性、強度、幅広い用途、特に食品、ヘルスケア、消費財の包装で支持を集めています。この材料は熱や化学薬品に強いため、高い安全性と性能基準が求められる包装ソリューションにとって信頼できる選択肢となっています。さらに、軽量で耐久性のある包装材料への注目の高まりが、市場におけるPPの需要をさらに押し上げています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024年 |

| 予測年 | 2025年~2034年 |

| 開始金額 | 501億5,000万米ドル |

| 予測金額 | 962億6,000万米ドル |

| CAGR | 6.7% |

PCRプラスチック包装市場は、リサイクル方法によってもメカニカルリサイクルとケミカルリサイクルに分けられます。メカニカルリサイクル分野は2024年に73%の最大シェアを占めました。メカニカルリサイクルは、そのコスト効率と確立された手法により引き続きリードしています。このプロセスでは、プラスチックの化学構造を変えることなく物理的に再加工するため、PET、PP、PEといった一般的な材料に適しています。リサイクルのインフラが改善し、リサイクル率の高い包装に対する消費者の需要が高まるにつれ、この分野は今後数年間も優位性を保つと予想されます。ケミカルリサイクルはまだ新興ではありますが、混合プラスチックや汚染プラスチックの処理能力で注目されており、将来的に市場成長の新たな機会を開く可能性があります。

2024年のPCRプラスチック包装市場のシェアは、北米が29%を占めました。米国では、環境に優しい製品に対する需要の高まりと、州レベルの環境規制を遵守する必要性により、市場が急成長しています。企業は持続可能性への取り組みの一環としてPCRプラスチックの採用を増やしており、カーボンフットプリントの削減とリサイクルの促進に貢献しています。このシフトは、特に食品、飲料やパーソナルケア製品のような業界で顕著であり、生産サイクルの中でリサイクルや再利用が容易な包装資材を使用することが強く求められています。この地域が技術革新に注力し、高度なリサイクル技術に投資することで、世界市場での地位がさらに強化されることが期待されます。

全体として、PCRプラスチック包装市場は、進化する消費者の選好、規制の枠組み、リサイクル技術の進歩に支えられ、大幅な成長を遂げようとしています。企業が持続可能性を優先し続ける中、PCRプラスチックの採用は加速し、バリューチェーン全体の利害関係者に新たな機会をもたらすと思われます。

目次

第1章 調査手法と調査範囲

- 市場範囲と定義

- 基本推定と計算

- 予測計算

- データソース

- 一次

- 二次

- 有料ソース

- 公的ソース

第2章 エグゼクティブサマリー

第3章 業界洞察

- 業界エコシステム分析

- バリューチェーンに影響を与える要因

- 変革

- 将来の展望

- メーカー

- 流通業者

- 利益率分析

- 主なニュースと取り組み

- 規制状況

- 影響要因

- 成長促進要因

- 包装ソリューションにおけるリサイクル材料の採用加速

- 拡大生産者責任(EPR)プログラムの拡大

- 消費財における再生ペットボトル需要の増加

- 需要促進とリサイクル能力の拡大におけるペットの重要な役割

- 循環型経済原則に対するブランドのコミットメント

- 業界の潜在的リスク・課題

- 多材料包装のリサイクルの複雑さ

- プレミアム製品におけるリサイクル材料への否定的な認識

- 成長促進要因

- 成長可能性分析

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業市場シェア分析

- 競合のポジショニングマトリックス

- 戦略展望マトリックス

第5章 市場推計・予測:プラスチックタイプ別、2021年~2034年

- 主要動向

- ポリエチレンテレフタレート(PET)

- ポリエチレン(PE)

- ポリスチレン(PS)

- ポリ塩化ビニル(PVC)

- ポリプロピレン(PP)

- バイオベースプラスチック

第6章 市場推計・予測:リサイクル別、2021年~2034年

- 主要動向

- メカニカルリサイクル

- ケミカルリサイクル

第7章 市場推計・予測:用途別、2021年~2034年

- 主要動向

- ボトル・トレー

- 袋・サック

- パウチ・小袋

- カップ・ジャー

- クラムシェル

- タブ

- その他

第8章 市場推計・予測:最終用途産業別、2021年~2034年

- 主要動向

- コンシューマーエレクトロニクス

- 消費財

- 化粧品・パーソナルケア

- 家庭用品・クリーニング

- その他

- 食品・飲料

- ヘルスケア・医薬品

- 小売

- その他

第9章 市場推計・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- 英国

- ドイツ

- フランス

- イタリア

- スペイン

- ロシア

- アジア太平洋

- 中国

- インド

- 日本

- 韓国

- オーストラリア

- ラテンアメリカ

- ブラジル

- メキシコ

- 中東・アフリカ

- 南アフリカ

- サウジアラビア

- アラブ首長国連邦

第10章 企業プロファイル

- 3plastics

- Amcor

- Berry Global

- Cambrian Packaging

- Evergreen Resources

- Glenroy

- Longdapac

- Mondi

- Proampac

- PTT Global Chemical

- Red Pack

- Regent Plast

- Sanle Plastic

- Udinc

- Winpak

The Global PCR Plastic Packaging Market was valued at USD 50.15 billion in 2024 and is expected to grow at a CAGR of 6.7% between 2025 and 2034. This market is witnessing significant growth as sustainability becomes a core focus for businesses, and the demand for alternatives to virgin plastics continues to rise. Companies across various industries are increasingly adopting PCR plastics to align with environmental goals and meet consumer expectations for eco-friendly products. The shift toward circular economies and stricter regulations on plastic waste management are further driving the market's expansion.

The market is segmented by plastic type into polyethylene terephthalate (PET), polyethylene (PE), polystyrene (PS), polyvinyl chloride (PVC), polypropylene (PP), and bio-based plastics. Among these, polypropylene (PP) is expected to see the fastest growth, projected to grow at a CAGR of 8.4%, reaching USD 19.4 billion by 2034. PP is gaining traction due to its versatility, strength, and wide range of applications, especially in packaging for food, healthcare, and consumer goods. The material's resistance to heat and chemicals makes it a reliable option for packaging solutions that require high safety and performance standards. Additionally, the growing focus on lightweight and durable packaging materials is further boosting the demand for PP in the market.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $50.15 Billion |

| Forecast Value | $96.26 Billion |

| CAGR | 6.7% |

The PCR plastic packaging market is also divided by recycling method into mechanical recycling and chemical recycling. The mechanical recycling segment held the largest share of 73% in 2024. Mechanical recycling continues to lead due to its cost-efficiency and established methods. This process involves physically reprocessing plastics without changing their chemical structure, making them suitable for common materials such as PET, PP, and PE. As recycling infrastructure improves and consumer demand for packaging with high recycled content rises, this segment is expected to maintain its dominance in the coming years. Chemical recycling, while still emerging, is gaining attention for its ability to handle mixed and contaminated plastics, which could open new opportunities for market growth in the future.

North America accounted for a 29% share of the PCR plastic packaging market in 2024. In the United States, the market is growing rapidly, driven by increasing demand for eco-friendly products and the need to comply with state-level environmental regulations. Companies are increasingly adopting PCR plastics as part of their sustainability initiatives, helping to reduce carbon footprints and promote recycling. This shift is particularly evident in industries like food, beverages, and personal care products, where there is a strong emphasis on using packaging materials that can be easily recycled and reused in production cycles. The region's focus on innovation and investment in advanced recycling technologies is expected to further strengthen its position in the global market.

Overall, the PCR plastic packaging market is poised for substantial growth, supported by evolving consumer preferences, regulatory frameworks, and advancements in recycling technologies. As businesses continue to prioritize sustainability, the adoption of PCR plastics is likely to accelerate, creating new opportunities for stakeholders across the value chain.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope & definitions

- 1.2 Base estimates & calculations

- 1.3 Forecast calculations

- 1.4 Data sources

- 1.4.1 Primary

- 1.4.2 Secondary

- 1.4.2.1 Paid sources

- 1.4.2.2 Public sources

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021-2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Factor affecting the value chain

- 3.1.2 Disruptions

- 3.1.3 Future outlook

- 3.1.4 Manufacturers

- 3.1.5 Distributors

- 3.2 Profit margin analysis

- 3.3 Key news & initiatives

- 3.4 Regulatory landscape

- 3.5 Impact forces

- 3.5.1 Growth drivers

- 3.5.1.1 Accelerated adoption of recycled content in packaging solutions

- 3.5.1.2 Expansion of extended producer responsibility (EPR) programs

- 3.5.1.3 Increased demand for recycled pet bottles in consumer goods

- 3.5.1.4 Pet's crucial role in driving demand and expanding recycling capacity

- 3.5.1.5 Brand commitment to circular economy principles

- 3.5.2 Industry pitfalls & challenges

- 3.5.2.1 Complexity in recycling multi-material packaging

- 3.5.2.2 Negative perceptions of recycled materials in premium products

- 3.5.1 Growth drivers

- 3.6 Growth potential analysis

- 3.7 Porter's analysis

- 3.8 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Plastic Type, 2021-2034 (USD Billion & Kilo Tons)

- 5.1 Key trends

- 5.2 Polyethylene terephthalate (PET)

- 5.3 Polyethylene (PE)

- 5.4 Polystyrene (PS)

- 5.5 Polyvinyl chloride (PVC)

- 5.6 Polypropylene (PP)

- 5.7 Bio-based plastics

Chapter 6 Market Estimates & Forecast, By Recycling, 2021-2034 (USD Billion & Kilo Tons)

- 6.1 Key trends

- 6.2 Mechanical recycling

- 6.3 Chemical recycling

Chapter 7 Market Estimates & Forecast, By Application, 2021-2034 (USD Billion & Kilo Tons)

- 7.1 Key trends

- 7.2 Bottles & trays

- 7.3 Bags & sacks

- 7.4 Pouches & sachets

- 7.5 Cups & jars

- 7.6 Clamshells

- 7.7 Tubs

- 7.8 Others

Chapter 8 Market Estimates & Forecast, By End Use Industry, 2021-2034 (USD Billion & Kilo Tons)

- 8.1 Key trends

- 8.2 Consumer electronics

- 8.3 Consumer goods

- 8.3.1 Cosmetics & personal care

- 8.3.2 Household & cleaning products

- 8.3.3 Others

- 8.4 Food & beverage

- 8.5 Healthcare & pharmaceutical

- 8.6 Retail

- 8.7 Others

Chapter 9 Market Estimates & Forecast, By Region, 2021-2034 (USD Billion & Kilo Tons)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 UK

- 9.3.2 Germany

- 9.3.3 France

- 9.3.4 Italy

- 9.3.5 Spain

- 9.3.6 Russia

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 South Korea

- 9.4.5 Australia

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.6 MEA

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 3plastics

- 10.2 Amcor

- 10.3 Berry Global

- 10.4 Cambrian Packaging

- 10.5 Evergreen Resources

- 10.6 Glenroy

- 10.7 Longdapac

- 10.8 Mondi

- 10.9 Proampac

- 10.10 PTT Global Chemical

- 10.11 Red Pack

- 10.12 Regent Plast

- 10.13 Sanle Plastic

- 10.14 Udinc

- 10.15 Winpak