|

市場調査レポート

商品コード

2038749

循環型ポリマー市場の機会、成長要因、業界動向分析、および2026年~2035年の予測Circular Polymers Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

カスタマイズ可能

|

|||||||

| 循環型ポリマー市場の機会、成長要因、業界動向分析、および2026年~2035年の予測 |

|

出版日: 2026年04月30日

発行: Global Market Insights Inc.

ページ情報: 英文 310 Pages

納期: 2~3営業日

|

概要

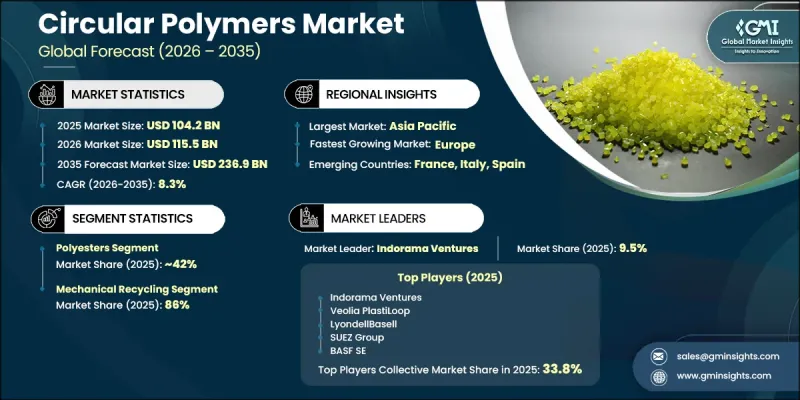

世界の循環型ポリマー市場は、2025年に1,042億米ドルと評価され、CAGR 8.3%で成長し、2035年までに2,369億米ドルに達すると推定されています。

各セクターにおいて、持続可能性への優先度が高まるにつれ、材料の使用形態が再構築され、この業界は引き続き勢いを増しています。企業は、廃棄物を最小限に抑え、ライフサイクルパフォーマンスを向上させるため、資源効率の高い取り組みをますます採用しています。消費者の環境意識の高まりにより、特に包装や消費財において、リサイクル可能かつ再利用可能な材料への移行が加速しています。循環型ポリマーは、製品の耐久性を維持しつつプラスチック廃棄物を削減できることから、好ましい代替品として台頭しています。リサイクルインフラの進展に加え、選別、洗浄、再処理技術の革新により、材料の品質と実用性が向上しています。リサイクル素材の使用を促進し、環境に配慮した生産を奨励する規制枠組みも、市場の拡大をさらに後押ししています。産業の持続可能性目標と消費者の期待との整合性が高まっていることで、製造、自動車、包装業界全体での採用が強化され、長期的な成長のための強固な基盤が築かれています。

| 市場範囲 | |

|---|---|

| 開始年 | 2025年 |

| 予測期間 | 2026年~2035年 |

| 開始時点の市場規模 | 1,042億米ドル |

| 予測額 | 2,369億米ドル |

| CAGR | 8.3% |

機械的リサイクル部門は、そのコスト効率と確立されたインフラに支えられ、2025年には86%のシェアを占めました。この方法は、化学組成を変えることなくプラスチック廃棄物を再利用可能な材料に変換する物理的処理技術に依存しており、広く使用されているポリマーに非常に適しています。その簡便性、拡張性、および既存システムとの互換性により、多岐にわたる産業においてその優位性を強め続けています。

ポリエステルセグメントは2025年に42%のシェアを占め、2035年までCAGR7.2%で成長すると予測されています。その優れたリサイクル性、耐久性、適応性により、幅広い用途で好まれる選択肢となっています。包装や繊維生産における持続可能な素材への需要の高まりが、ポリエステルベースの循環型ソリューションの採用を後押しし続けています。

北米の循環型ポリマー市場は、2026年から2035年にかけてCAGR7.8%で成長すると予想されています。同地域の成長は、環境規制の強化、リサイクル能力の向上、および持続可能性に対する消費者の意識の高まりによって牽引されています。先進的なリサイクルシステムや環境に配慮した製造手法への投資が、地域市場の拡大をさらに後押ししています。

よくあるご質問

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- サプライヤーの情勢

- 利益率

- 各段階における付加価値

- バリューチェーンに影響を与える要因

- ディスラプション

- 業界への影響要因

- 促進要因

- カーボンフットプリントを削減するために再生材料を使用することへの、様々な業界における意識の高まり

- 包装業界におけるリサイクル可能素材の採用拡大が、市場を牽引しています

- 再生プラスチックを促進するための好ましい取り組み

- 業界の潜在的リスク&課題

- 高いリサイクルコストが循環型ポリマーの収益性を阻害しています

- 消費者の認知度が低いため、再生ポリマーの需要が減少しています

- 市場機会

- 規制面での支援の拡大が、循環型ポリマーの採用を促進しています

- 持続可能な包装ソリューションに対する世界の需要の高まり

- 促進要因

- 成長可能性分析

- 規制情勢

- 北米

- 欧州

- アジア太平洋地域

- ラテンアメリカ

- 中東・アフリカ

- ポーター分析

- PESTEL分析

- 価格動向

- 地域別

- ポリマー種別

- 今後の市場動向

- 技術およびイノベーションの動向

- 現在の技術動向

- 新興技術

- 特許動向

- 貿易統計(HSコード)

- 主要輸入国

- 主要輸出国

- 持続可能性と環境面

- 持続可能な取り組み

- 廃棄物削減戦略

- 生産におけるエネルギー効率

- 環境配慮型イニシアチブ

- カーボンフットプリントへの配慮

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 地域別

- 北米

- 欧州

- アジア太平洋地域

- ラテンアメリカ

- 中東・アフリカ(MEA)

- 地域別

- 主要市場企業の競合分析

- 競合ポジショニングマトリックス

- 主な発展

- 合併・買収

- パートナーシップおよび提携

- 新製品の発売

- 事業拡大計画

第5章 市場推計・予測:ポリマー種別、2022-2035

- ポリエステル

- PET(ポリエチレンテレフタレート)

- PTT(ポリトリメチレンテレフタレート)

- PBT(ポリブチレンテレフタレート)

- ポリオレフィン

- ポリエチレン(PE)

- ポリプロピレン(PP)

- ビニル系ポリマー

- PVC(ポリ塩化ビニル)

- PVA(ポリビニルアルコール)

- スチレン系樹脂

- ポリスチレン(PS)

- ABS(アクリロニトリル・ブタジエン・スチレン)

- SAN(スチレン・アクリロニトリル)

- エンジニアリング・特殊ポリマー

- ポリアミド(PA/ナイロン)

- ポリカーボネート(PC)

- その他のエンジニアリングポリマー

第6章 市場推計・予測:リサイクル技術別、2022-2035

- 機械的リサイクル

- 使用済み消費者リサイクル(PCR)

- 産業由来再生材(PIR)

- 化学的リサイクル

- 熱分解

- 脱重合

- 溶剤を用いた精製

- ガス化

- バイオベース循環型ポリマー

- ドロップイン型バイオベースポリマー

- 新規バイオポリマー

第7章 市場推計・予測:用途別、2022-2035

- 包装

- 食品用包装

- 非食品用包装

- フレキシブル包装

- 硬質包装

- 建築・建設

- 断熱材

- 配管・給排水システム

- プロファイル・金物

- 床材、デッキ材、屋根材

- 自動車

- 内装部品

- 外装部品

- エンジンルーム部品

- 構造・安全部品

- 電気・電子

- 民生用電子機器

- ケーブル・配線

- 部品・コネクタ

- 白物家電・家電製品

- 農業

- フィルム

- 灌漑システム

- 容器・保管

- 繊維・アパレル

- ポリエステル繊維(rPET)

- ナイロン繊維(再生PA)

- 不織布

- 消費財・その他

- 家具・家庭用品

- 玩具・レクリエーション用品

- その他の用途

第8章 市場推計・予測:地域別、2022-2035

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- スペイン

- イタリア

- その他欧州地域

- アジア太平洋地域

- 中国

- インド

- 日本

- オーストラリア

- 韓国

- その他アジア太平洋地域

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- その他ラテンアメリカ地域

- 中東・アフリカ

- サウジアラビア

- 南アフリカ

- アラブ首長国連邦

- その他中東・アフリカ地域

第9章 企業プロファイル

- Amcor

- BASF SE

- Brightmark

- Carbios

- Eastman

- Enka

- Gr3n

- Indorama Ventures

- KW Plastics

- Loop Industries

- LyondellBasell

- MBA Polymers

- Plastic Energy

- Plastipak

- PureCycle Technologies

- SUEZ Group

- Veolia PlastiLoop